Market Size of Sensors In Oil And Gas Industry

| Study Period | 2019 - 2029 |

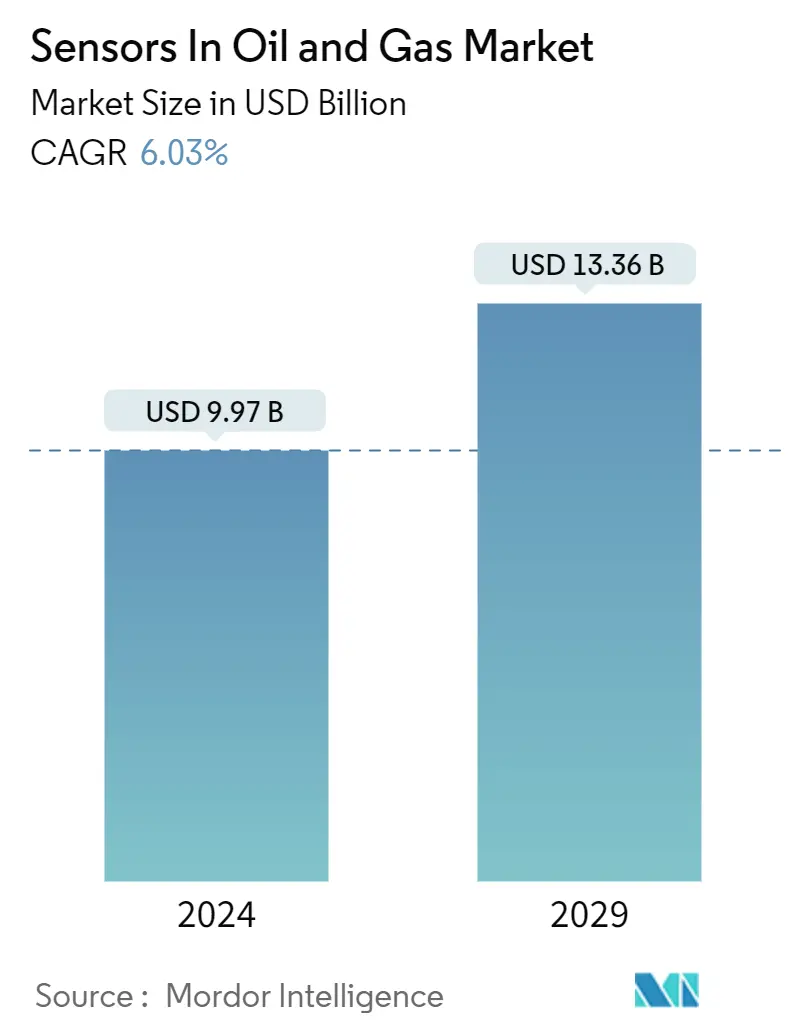

| Market Size (2024) | USD 9.97 Billion |

| Market Size (2029) | USD 13.36 Billion |

| CAGR (2024 - 2029) | 6.03 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Oil & Gas Sensors Market Analysis

The Sensors In Oil And Gas Market size is estimated at USD 9.97 billion in 2024, and is expected to reach USD 13.36 billion by 2029, growing at a CAGR of 6.03% during the forecast period (2024-2029).

- The global economy depends on the oil and gas industry. In addition to producing most of the world's basic energy, the oil and gas sector also serves as a substantial source of raw materials for various chemical goods, such as insecticides, fertilizers, medicines, solvents, and polymers. Control and monitoring are crucial for efficient and stable oil and gas industry operations. It improves productivity, cuts costs, and promotes profitability. The control and monitoring of the oil and gas industry depend heavily on sensors.

- The primary factors influencing market expansion are a greater focus on technical advancement and supportive governmental policies. Growing industrialization and stricter enforcement of various safety and occupational health regulations reduce market value. The market will grow due to increased awareness of air pollution and the growing supply of miniaturized wireless sensors. Another element contributing to the surge of the market is the expansion and growth of the micro-electromechanical sector.

- The rising adoption of IIoT (Industrial Internet of Things) sensors in the oil and gas industry is mainly driven by the need to reduce costs. The installation of these sensors takes less time and costs less, owing to technological advancements and easy assembling options that sensor manufacturers offer to end users.

- The current oil price environment is driving significant changes and difficult decisions across the oil and gas industry. New operating models and strategies that improve CAPEX and OPEX are required to respond to short- and mid-term market supply and demand dynamics. The long-term requirement for sustainable solutions that reinforce safety and environmental performance is a topmost priority. From drill pad to refinery, the application of sensors helps operators achieve a unique balance through a spectrum of upstream, midstream, and downstream technological innovations and solutions.

- Sensor manufacturers are increasingly offering sensors designed with easy assembling options. Owing to technical advancements, the competition among significant manufacturers of sensors and service providers of IoT products is intensifying, thereby boosting the adoption of these in the oil and gas industry.

- Additionally, the oil and gas industry suffers from a skilled labor shortage. The presence of a shallow talent pool has made it complicated for oil and gas companies to hire new employees who possess the technical skills that are required to work on new energy sources. Moreover, stress with the oil prices during COVID-19 and the price war between countries such as Saudi Arabia and Russia was expected to drive oil-producing companies to enhance their production efficiency and increase the demand in the sector.

Oil & Gas Sensors Industry Segmentation

The oil and gas industry operates in a very volatile environment. The oil price fluctuations and the industry's digitization boom have driven the demand for innovation and investment to meet the cost, ease the cost, and optimize the industry's operations. Thus, deploying the sensors is crucial for monitoring specific parameters for the safety and optimization of processes in the oil and gas industry. Wireless sensors are widely used for this due to their low cost, ease of deployment, flexibility, and convenience of operation.

The oil and gas sensors market is segmented by sensor type (gas sensor, temperature sensor, ultrasonic sensor, pressure sensor, flow sensor, level sensor, other sensor types), connectivity (wired, wireless), activity (upstream, midstream, downstream), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Sensor Type | |

| Gas Sensor | |

| Temperature Sensor | |

| Ultrasonic Sensor | |

| Pressure Sensor | |

| Flow Sensor | |

| Level Sensor | |

| Other Sensor Types |

| By Connectivity | |

| Wired | |

| Wireless |

| By Activity | |

| Upstream | |

| Midstream | |

| Downstream |

| By Geography | ||||||

| ||||||

| ||||||

| ||||||

| ||||||

|

Sensors In Oil And Gas Market Size Summary

The oil and gas sensors market is poised for significant growth, driven by the industry's reliance on advanced monitoring and control systems to enhance operational efficiency and safety. As the global economy continues to depend heavily on the oil and gas sector for energy and raw materials, the demand for sensors that facilitate real-time data collection and analysis is increasing. These sensors play a crucial role in optimizing production processes, reducing costs, and ensuring compliance with stringent safety and environmental regulations. The market is further bolstered by technological advancements in sensor design and the growing adoption of the Industrial Internet of Things (IIoT), which enables more efficient and cost-effective sensor deployment across various industry segments.

The market landscape is characterized by intense competition among key players, such as Honeywell International Inc., Siemens AG, and ABB Ltd., who are continually innovating to meet the evolving needs of the oil and gas industry. The European market, in particular, is experiencing robust growth due to stringent emission control requirements and a strong focus on energy efficiency. This has led to increased adoption of gas sensors and other monitoring technologies. Additionally, the industry's shift towards sustainable practices and the integration of smart technologies are driving the demand for advanced sensors that support real-time decision-making and operational optimization. As the sector navigates challenges such as skilled labor shortages and fluctuating oil prices, the role of sensors in enhancing productivity and safety remains paramount.

Sensors In Oil And Gas Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitute Products

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Assessment of Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Sensor Type

-

2.1.1 Gas Sensor

-

2.1.2 Temperature Sensor

-

2.1.3 Ultrasonic Sensor

-

2.1.4 Pressure Sensor

-

2.1.5 Flow Sensor

-

2.1.6 Level Sensor

-

2.1.7 Other Sensor Types

-

-

2.2 By Connectivity

-

2.2.1 Wired

-

2.2.2 Wireless

-

-

2.3 By Activity

-

2.3.1 Upstream

-

2.3.2 Midstream

-

2.3.3 Downstream

-

-

2.4 By Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

-

2.4.2 Europe

-

2.4.2.1 United Kingdom

-

2.4.2.2 Germany

-

2.4.2.3 Rest of Europe

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 India

-

2.4.3.3 Indonesia

-

2.4.3.4 Rest of Asia-Pacific

-

-

2.4.4 Latin America

-

2.4.4.1 Mexico

-

2.4.4.2 Brazil

-

2.4.4.3 Argentina

-

2.4.4.4 Rest of Latin America

-

-

2.4.5 Middle East and Africa

-

2.4.5.1 United Arab Emirates

-

2.4.5.2 Saudi Arabia

-

2.4.5.3 South Africa

-

2.4.5.4 Rest of Middle East and Africa

-

-

-

Sensors In Oil And Gas Market Size FAQs

How big is the Sensors in Oil and Gas Market?

The Sensors in Oil and Gas Market size is expected to reach USD 9.97 billion in 2024 and grow at a CAGR of 6.03% to reach USD 13.36 billion by 2029.

What is the current Sensors in Oil and Gas Market size?

In 2024, the Sensors in Oil and Gas Market size is expected to reach USD 9.97 billion.