| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 28.70 % |

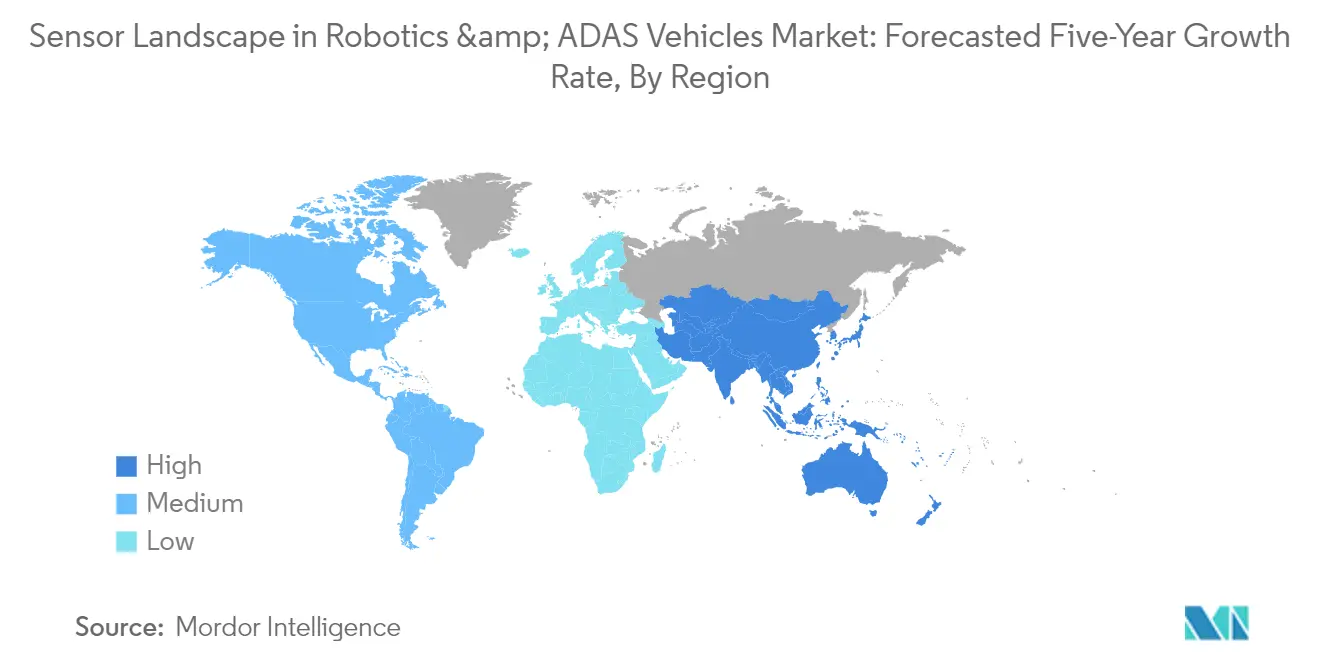

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

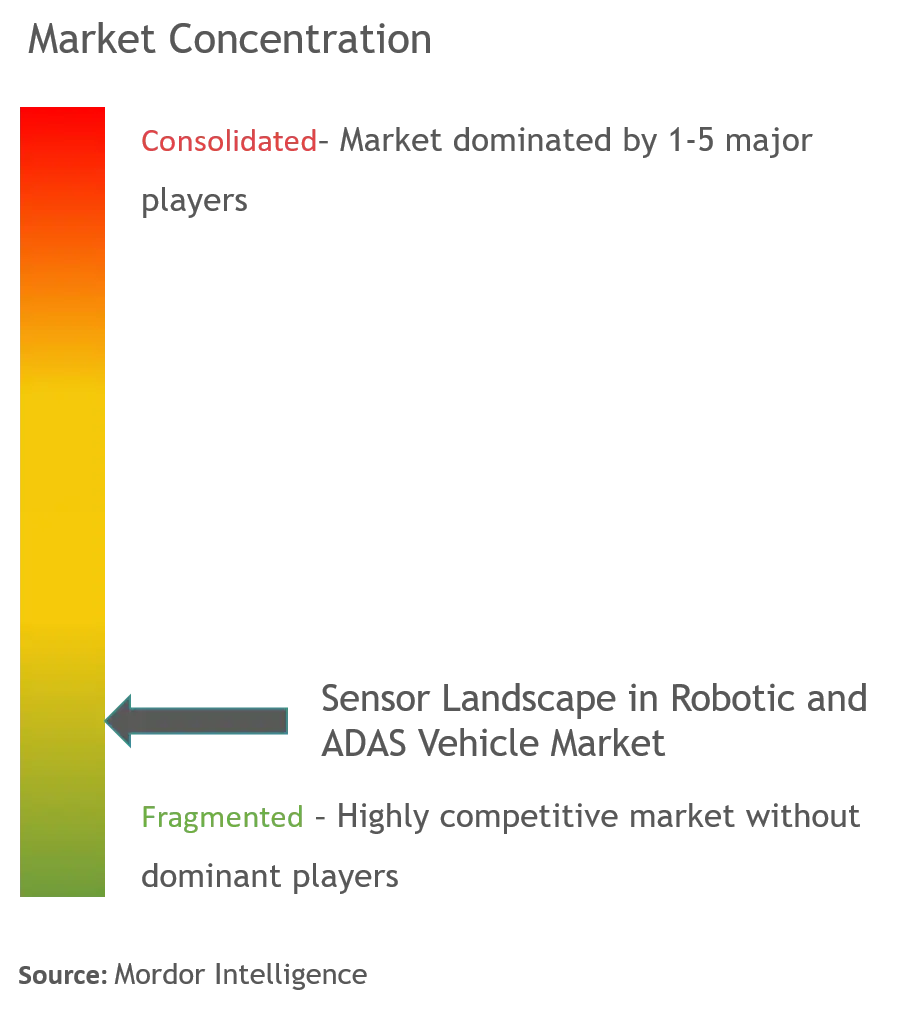

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Sensor Landscape in Robotics and ADAS Vehicles Market Analysis

The Sensor Landscape in Robotics and ADAS Vehicles Market is expected to register a CAGR of 28.7% during the forecast period.

The automotive industry is undergoing a transformative shift toward autonomous and connected vehicles, driven by the critical need to address road safety concerns. According to the World Health Organization, auto accidents are responsible for 1.3 million deaths annually, with the National Highway Traffic Safety Administration reporting that 94% of these accidents are caused by human error. This stark reality has catalyzed the development of advanced sensing technologies, with industry leaders like Valeo demonstrating significant progress by producing over 1.5 billion ADAS sensors by 2022. The integration of these automotive sensors has become increasingly sophisticated, with vehicles now utilizing multiple sensor types including camera sensors, radar sensors, lidar sensors, and ultrasonic sensors, with some advanced models featuring more than 20 sensors mounted in different locations.

The technological landscape is experiencing rapid evolution through strategic partnerships and innovations. A significant development occurred in September 2023 when Mobileye Global Inc. partnered with Valeo to develop software-defined imaging radars for next-generation driver assist and autonomous driving technology features. This collaboration exemplifies the industry's move toward more sophisticated sensing solutions, with imaging radar emerging as a crucial enabler for hands-off ADAS solutions. The industry's commitment to innovation is further evidenced by companies like Luminar Technologies, which maintained 210 patent issues pending as of 2022, demonstrating the intense focus on developing proprietary autonomous vehicle sensor technologies.

Regional markets are showcasing remarkable progress in autonomous vehicle implementation, particularly in the Middle East. In September 2023, Dubai launched its first round of robotaxis, deploying five fully autonomous electric vehicles operated by Cruise, a General Motors subsidiary, for testing on an 8 km stretch in the Jumeirah district. This was followed by the UAE's groundbreaking decision in July 2023 to grant WeRide a license for testing self-driving vehicles, marking a significant step toward autonomous driving technology adoption in the region. In Europe, notable advancement came in May 2023 when Bosch received approval from the German Federal Transport Authority to test Level 4 driverless cars on public roads in all weather conditions, becoming one of the first companies to receive such comprehensive testing permissions.

The industry is witnessing a surge in collaborative efforts to accelerate technological advancement and standardization. Major automotive manufacturers and technology providers are forming strategic alliances to pool resources and expertise, particularly in sensor fusion technologies. These partnerships are focusing on developing integrated solutions that combine multiple sensor types to create enhanced ADAS capabilities, including cross-traffic assistance and obstacle avoidance. The trend toward sensor fusion is particularly evident in the development of environmental models that combine data from radar sensors, lidar sensors, camera sensors, and other robotic sensors to create a comprehensive understanding of the vehicle's surroundings, enabling more reliable and safer autonomous driving capabilities.

Sensor Landscape in Robotics and ADAS Vehicles Market Trends

Rising Awareness of Safety & Stringent Regulations

The automotive industry is witnessing a significant push towards enhanced safety features, driven by concerning statistics and stringent government regulations. According to the National Highway Traffic Safety Administration (NHTSA) research, approximately 94% of serious crashes are due to human error, highlighting the critical need for advanced safety systems in vehicles. In response to these statistics, governments worldwide are implementing strict safety regulations. For instance, as of mid-2022, the European Union mandated that all new cars entering the market must be equipped with advanced safety systems, including intelligent speed assistance, alcohol interlock installation facilitation, driver drowsiness warning systems, and advanced driver distraction detection systems.

The regulatory landscape continues to evolve with significant developments in 2023. In September 2023, Dubai initiated its first round of robotaxis, implementing five fully autonomous electric taxis operated by Cruise, a General Motors subsidiary, marking a significant step in safety-oriented autonomous driving technology. Additionally, Euro NCAP, a government-backed organization that rates cars for safety, has announced plans to require driver monitoring systems from 2023/2024 for vehicles to achieve a five-star safety rating. These developments are complemented by recent industry partnerships, such as the May 2023 collaboration between Porsche AG and Mobileye Global Inc., focusing on manufacturing premium advanced driver assistance systems for upcoming models, demonstrating the industry's commitment to enhanced safety features.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for ADAS Features in Vehicles May Propel Market Growth

The increasing integration of Advanced Driver Assistance Systems (ADAS) features is revolutionizing vehicle safety and the driving experience, supported by significant technological advancements and industry collaborations. In September 2023, Mobileye Global Inc. partnered with Valeo to develop software-defined imaging radar sensors for next-generation driver assist and automated driving features, highlighting the industry's focus on enhancing ADAS capabilities. This trend is further evidenced by strategic developments such as TDK Corporation's January 2023 announcement of full-scale production of the IAM-20685, the smallest ASIL-B monolithic 6-axis MEMS IMU developed for ADAS and autonomous car systems.

The automotive industry's commitment to ADAS advancement is demonstrated through various strategic partnerships and technological innovations in 2023. For instance, in August 2023, Toyota subsidiary Hino Motors Ltd and Daimler-owned Mitsubishi Fuso Truck and Bus Corp. combined their truck businesses in Japan to accelerate the development of CASE (Connected/Autonomous/Automated/Shared/Electric) technology. Additionally, companies like Omnivision are pushing technological boundaries, as evidenced by their September 2023 launch of the OX08D10 8-megapixel CMOS camera sensors with TheiaCel™ technology, specifically designed to enhance automotive safety through improved resolution and image quality in exterior cameras for ADAS and autonomous driving applications. These developments indicate a strong industry-wide commitment to advancing ADAS sensor features and capabilities.

Segment Analysis: TYPE

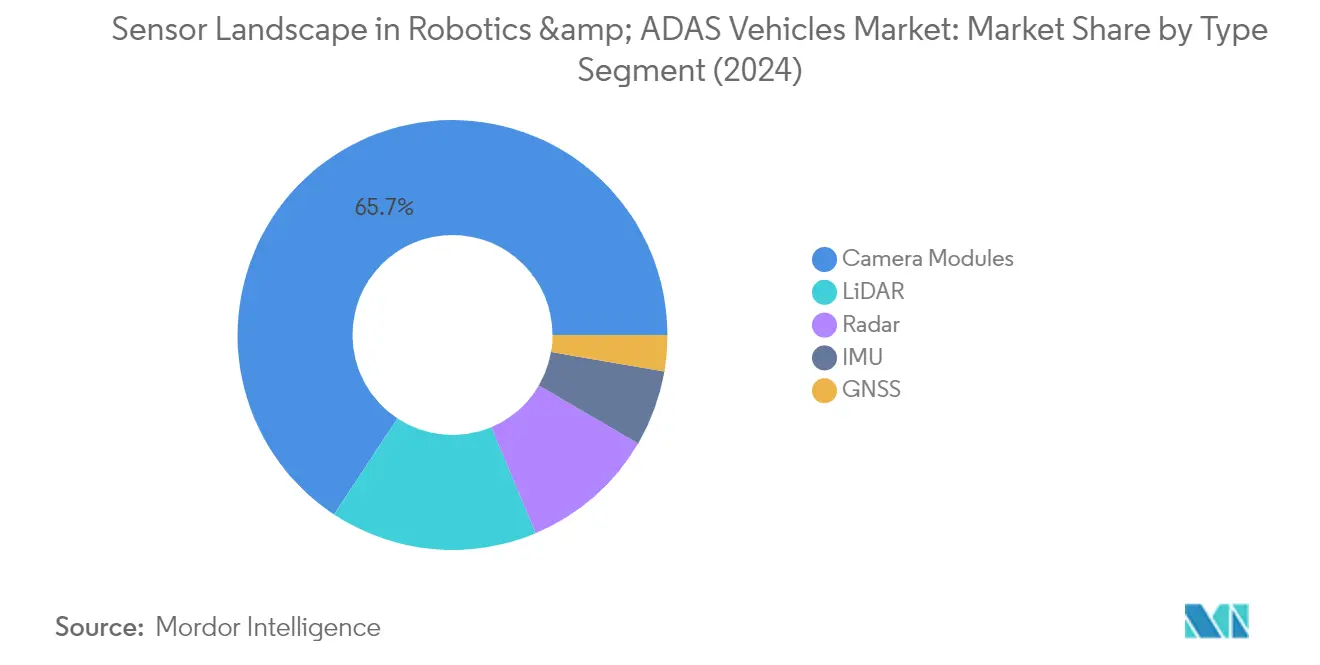

Camera Modules Segment in Sensor Landscape for Robotics & ADAS Vehicles Market

Camera modules dominate the camera sensor landscape for the robotics and ADAS vehicles market, commanding approximately 66% market share in 2024. This segment's leadership position is driven by cameras being one of the most crucial components in active safety systems for vehicles. Sensing cameras have become an integral part of modern vehicles, offering features like 360-degree views through multiple tiny cameras positioned at the front, rear, and sides of vehicles. These systems enable critical functionalities such as parking assistance, lane change warnings, and comprehensive environmental monitoring. The segment's growth is primarily attributed to increasing passenger safety concerns and stringent government safety initiatives. Camera modules provide higher performance levels compared to general-purpose driving cameras while maintaining cost-effectiveness, making them particularly attractive for automotive manufacturers implementing ADAS features.

LiDAR Segment in Sensor Landscape for Robotics & ADAS Vehicles Market

The LiDAR sensor segment represents one of the most advanced technologies currently being deployed in self-driving cars and autonomous vehicles. This technology enables crucial functionalities such as navigation, obstacle detection, and collision avoidance in autonomous systems. Major automotive brands like Velodyne and tech companies like Luminar are continuously advancing the state-of-the-art in LiDAR sensor research, with premium automotive manufacturers like Mercedes Benz entering into deeper partnerships in the LiDAR sensor space. The technology's ability to operate in the infrared portion of the spectrum provides much better spatial resolution compared to traditional radar systems, making it essential for achieving higher levels of autonomy. Companies are focusing on developing safer and more reliable autonomous cars by incorporating LiDAR technology to enable advanced capabilities for ADAS features, including pedestrian and bicycle avoidance, lane keep assistance, automatic emergency braking, and traffic jam assist.

Remaining Segments in Sensor Landscape for Robotics & ADAS Vehicles Market

The market's remaining segments include radar sensor, GNSS (Global Navigation Satellite Systems), and Inertial Measurement Units (IMUs), each playing vital roles in creating a comprehensive autonomous vehicle sensor solution for autonomous vehicles. Radar sensors excel in detecting metal objects and measuring distances between vehicles, particularly useful in adverse weather conditions. GNSS provides precise positioning and navigation capabilities, essential for autonomous vehicle operation and route planning. IMUs contribute to vehicle stability and orientation sensing, working in conjunction with other sensors to maintain accurate vehicle positioning and movement data. These technologies complement each other, creating a robust multi-sensor approach that ensures reliable and safe operation of autonomous vehicles across various environmental conditions and use cases.

Sensor Landscape in Robotics and ADAS Vehicles Geography Segment Analysis

Sensor Landscape in Robotics & ADAS Vehicles Market in North America

The North American sensor landscape for robotics and ADAS vehicles represents approximately 32% of the global market share in 2024, establishing itself as a crucial region for autonomous vehicle technology development. This dominance is primarily driven by extensive research and development facilities, stringent safety regulations, and active engagement of leading players through strategic collaborations. The United States leads the regional market with the highest penetration of ADAS implementation globally and the highest fitment value per vehicle. Major automotive manufacturers across the region are rapidly integrating advanced driver assistance systems as standard features in their vehicle lineups. The region's growth is further supported by increasing consumer awareness about vehicle safety, technological advancements in automotive sensors, and supportive government initiatives promoting autonomous vehicle adoption. The presence of major technology companies and automotive manufacturers, coupled with sophisticated infrastructure and testing facilities, continues to strengthen North America's position in the global market. The region's focus on safety innovations and autonomous driving capabilities has created a robust ecosystem for autonomous vehicle sensors technology development and implementation.

Sensor Landscape in Robotics & ADAS Vehicles Market in Europe

Europe has demonstrated remarkable progress in the sensor landscape for robotics and ADAS vehicles, achieving approximately 8% growth from 2019 to 2024. The region's market is characterized by strong research expertise and increasing demand for driverless vehicles among the consumer base. European automotive manufacturers are at the forefront of implementing cutting-edge ADAS sensors, supported by robust regulatory frameworks and safety standards. The region's market dynamics are shaped by significant investments in research and development, particularly in countries like Germany, France, and the United Kingdom. The presence of leading automotive manufacturers and tier-1 suppliers has created a sophisticated ecosystem for sensor technology development. Europe's commitment to reducing carbon emissions and improving road safety has accelerated the adoption of advanced robotic sensors in vehicles. The region's strong focus on technological innovation, coupled with supportive government policies and infrastructure development, continues to drive market growth. The collaboration between automotive manufacturers, technology providers, and research institutions has established Europe as a key hub for autonomous vehicle technology development.

Sensor Landscape in Robotics & ADAS Vehicles Market in Asia-Pacific

The Asia-Pacific region is poised for exceptional growth in the sensor landscape for robotics and ADAS vehicles, with a projected growth rate of approximately 40% from 2024 to 2029. This remarkable growth trajectory is driven by rapid technological adoption, increasing vehicle production, and strong government support for autonomous vehicle development. China leads the regional market with significant investments in autonomous driving technology and electric vehicle integration. The region's automotive sector is witnessing a transformative shift towards advanced driver assistance systems, supported by increasing consumer awareness and safety regulations. Japan and South Korea contribute significantly to the market's growth through their strong technological capabilities and innovative approaches to sensor development. The presence of major semiconductor manufacturers and sensor technology providers has created a robust supply chain ecosystem. The region's focus on smart city development and intelligent transportation systems further accelerates the adoption of advanced sensor technologies. The combination of technological innovation, manufacturing capabilities, and supportive government policies positions Asia-Pacific as a key growth engine for the global market.

Sensor Landscape in Robotics & ADAS Vehicles Market in Latin America

The Latin American market for robotics and ADAS vehicle sensors is experiencing steady growth, driven by increasing awareness of vehicle safety features and rising disposable income levels. The region's automotive industry is gradually embracing advanced driver assistance systems, with Brazil leading the adoption of these technologies. Major automotive manufacturers are introducing vehicles equipped with advanced camera sensors to meet growing consumer demands for safety and comfort features. The market is characterized by strategic partnerships between local distributors and global sensor manufacturers to enhance technology accessibility. Infrastructure development and improving economic conditions across key countries are creating favorable conditions for market expansion. The region's automotive sector is witnessing a shift towards premium vehicles equipped with advanced safety features, indicating growing acceptance of ADAS technologies. The combination of increasing consumer awareness, economic growth, and technological advancement is reshaping the regional market landscape.

Sensor Landscape in Robotics & ADAS Vehicles Market in Middle-East and Africa

The Middle East and Africa region presents emerging opportunities in the sensor landscape for robotics and ADAS vehicles, driven by increasing urbanization and growing focus on smart transportation solutions. The Gulf Cooperation Council (GCC) countries are leading the adoption of advanced automotive technologies, with significant investments in autonomous vehicle infrastructure. Countries like the United Arab Emirates and Saudi Arabia are actively promoting the integration of autonomous driving technologies through supportive policies and initiatives. The region's focus on developing smart cities and sustainable transportation systems is creating new opportunities for radar sensors deployment. Major automotive manufacturers are introducing vehicles with advanced driver assistance features to cater to the region's growing demand for premium vehicles. The market is characterized by increasing partnerships between global technology providers and local stakeholders to enhance technology adoption. The combination of government support, infrastructure development, and growing consumer awareness is establishing a foundation for sustained market growth in the region.

Get Analysis on Important Geographic Markets

Download PDF

Sensor Landscape in Robotics and ADAS Vehicles Industry Overview

Top Companies in Sensor Landscape in Robotics & ADAS Vehicles Market

The market features prominent players like Infineon Technologies, NXP Semiconductor, Ouster (Velodyne), Luminar Technologies, and Continental AG leading the innovation curve. These companies are heavily investing in research and development to advance their LiDAR sensor technologies, particularly in LiDAR, radar sensor, and imaging solutions for autonomous vehicles. Strategic partnerships with automotive manufacturers and technology companies have become increasingly common to accelerate market entry and promote infrastructure development. Companies are focusing on expanding their manufacturing capabilities across different geographies to strengthen their supply chains and meet growing demand. The industry is witnessing a significant push towards developing more cost-effective and efficient automotive sensor solutions while maintaining high performance and reliability standards. Market leaders are also emphasizing software integration and data analytics capabilities to provide comprehensive solutions for autonomous vehicle sensor applications.

Consolidated Market with Strong Global Players

The sensor landscape in robotics and ADAS vehicles is characterized by a mix of large multinational conglomerates and specialized technology companies competing for market share. Global players like Bosch, Continental, and Valeo leverage their extensive automotive industry experience and established relationships with OEMs, while specialized companies like Ouster and Luminar focus on developing cutting-edge LiDAR sensor technologies. The market structure shows moderate consolidation, with major players controlling significant market share through their technological capabilities and established distribution networks. Cross-border partnerships and joint ventures have become increasingly common as companies seek to combine complementary strengths and accelerate innovation.

The industry has witnessed several strategic mergers and acquisitions, notably the merger between Ouster and Velodyne, which aims to consolidate the LiDAR sensor industry. Companies are actively pursuing vertical integration strategies to strengthen their position in the value chain, from semiconductor development to final sensor assembly. Regional players are emerging in key markets like China and Japan, focusing on serving local automotive manufacturers while gradually expanding their global presence. The competitive dynamics are further shaped by the entry of technology giants and startups bringing fresh perspectives and innovative solutions to the sensor market.

Innovation and Integration Drive Market Success

Success in the sensor landscape requires a multi-faceted approach combining technological innovation with strategic market positioning. Incumbent players must continue investing in research and development while optimizing their production processes to maintain cost competitiveness. Building strong relationships with automotive manufacturers through early engagement in vehicle development cycles and offering customizable solutions has become crucial. Companies need to develop comprehensive sensor fusion solutions that can integrate multiple sensor types while ensuring reliability and performance under various environmental conditions. The ability to scale production while maintaining quality standards and meeting stringent automotive requirements remains a critical success factor.

For new entrants and challenger companies, differentiation through technological innovation and specialized applications presents opportunities to gain market share. The increasing demand for advanced driver assistance systems and autonomous driving capabilities creates opportunities for companies offering unique radar sensor solutions or cost advantages. Regulatory requirements for vehicle safety features and emissions reduction continue to drive sensor adoption, while standardization efforts influence product development strategies. Companies must also consider the growing importance of cybersecurity and data protection in sensor systems, as these factors increasingly influence customer decisions and regulatory compliance requirements.

Sensor Landscape in Robotics and ADAS Vehicles Market Leaders

-

Infineon Technologies AG

-

NXP Semiconductor N.V.

-

Continental AG

-

ST Microelectronics NV

-

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Sensor Landscape in Robotics and ADAS Vehicles Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

-

4.4 Market Drivers

- 4.4.1 Rising awareness on worker safety & stringent regulations

- 4.4.2 Steady increase in industrial sector in key emerging countries in Asia-Pacific, coupled with expansion projects

-

4.5 Market Challenges

- 4.5.1 Recent outbreak of COVID-19 and marginal decline in spending in key verticals expected to pose a concern to manufacturers

- 4.6 Light Passenger Car and Robotic Vehicle Sales Statistics by Level of Autonomy ?

- 4.7 Key Industry Standards & Regulations

- 4.8 Technological Roadmap for Automotive Sensors (Radar, Camera & LiDAR)

- 4.9 Assessment of Impact of Covid-19 on the Industry

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 LiDAR (Robotic Vehicles Vs. ADAS Vehicles)

- 5.1.2 Radar (Robotics Vehicles Vs. ADAS Vehicles)

- 5.1.3 Camera Modules (Robotics Vehicles Vs. ADAS Vehicles)

- 5.1.4 GNSS (Robotic Vehicles)

- 5.1.5 Inertial Measurement Units (Robotic Vehicles)

-

5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia Pacific

- 5.2.4 Latin America

- 5.2.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Ranking for Top 3 Automotive LiDAR Suppliers

- 6.2 Vendor Ranking for Top 3 Automotive Image Sensor Suppliers

- 6.3 Vendor Ranking for Top 3 Automotive Radar Supplier

-

6.4 Company Profiles

- 6.4.1 Infineon Technologies AG

- 6.4.2 NXP Semiconductor N.V.

- 6.4.3 Ouster Inc.

- 6.4.4 Velodyne LiDAR Inc.

- 6.4.5 Luminar Technologies Inc.

- 6.4.6 Aurora Innovation Inc. (Incl. Blackmore)

- 6.4.7 Waymo LLC

- 6.4.8 Robert Bosch GmbH

- 6.4.9 Continental AG

- 6.4.10 Valeo SA

- 6.4.11 ON Semiconductor Corp

- 6.4.12 Omnivision Technologies Inc.

- 6.4.13 ST Microelectronics NV

- 6.4.14 Texas Instruments Incorporated

- *List Not Exhaustive

7. INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Sensor Landscape in Robotics and ADAS Vehicles Industry Segmentation

Sensor Landscape in robotic and ADAS vehicles is growing at a fast pace owing to rising awareness on worker safety & stringent regulations and steady increase in the industrial sector in key emerging countries in Asia-Pacific, coupled with expansion projects. The market is segmented based on the type of sensors and geography.

| Type | LiDAR (Robotic Vehicles Vs. ADAS Vehicles) |

| Radar (Robotics Vehicles Vs. ADAS Vehicles) | |

| Camera Modules (Robotics Vehicles Vs. ADAS Vehicles) | |

| GNSS (Robotic Vehicles) | |

| Inertial Measurement Units (Robotic Vehicles) | |

| Geography | North America |

| Europe | |

| Asia Pacific | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Sensor Landscape in Robotics and ADAS Vehicles Market Research FAQs

What is the current Sensor Landscape in Robotics and ADAS Vehicles Market size?

The Sensor Landscape in Robotics and ADAS Vehicles Market is projected to register a CAGR of 28.7% during the forecast period (2025-2030)

Who are the key players in Sensor Landscape in Robotics and ADAS Vehicles Market?

Infineon Technologies AG, NXP Semiconductor N.V., Continental AG, ST Microelectronics NV and Texas Instruments Incorporated are the major companies operating in the Sensor Landscape in Robotics and ADAS Vehicles Market.

Which is the fastest growing region in Sensor Landscape in Robotics and ADAS Vehicles Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Sensor Landscape in Robotics and ADAS Vehicles Market?

In 2025, the North America accounts for the largest market share in Sensor Landscape in Robotics and ADAS Vehicles Market.

What years does this Sensor Landscape in Robotics and ADAS Vehicles Market cover?

The report covers the Sensor Landscape in Robotics and ADAS Vehicles Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Sensor Landscape in Robotics and ADAS Vehicles Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Sensor Landscape in Robotics and ADAS Vehicles Research

Mordor Intelligence provides a comprehensive analysis of the autonomous driving technology landscape. We possess deep expertise in automotive sensor systems and their applications. Our extensive research covers the full spectrum of sensing technologies. This includes ultrasonic sensor, lidar sensor, camera sensor, and radar sensor systems that power modern autonomous solutions. The report offers detailed insights into the ultrasonic sensor industry and emerging developments in ADAS sensor technology. It is available as an easy-to-download report PDF.

Stakeholders in the automotive sensor market, radar sensor market, and lidar sensor market gain valuable insights into technology adoption trends and growth opportunities. The analysis includes both robotic sensor applications and autonomous vehicle sensor implementations, with a particular focus on robot vision sensor capabilities. Our research methodology examines the ultrasonic sensor market dynamics across various applications. This provides actionable intelligence for manufacturers, integrators, and end-users in both robotics and ADAS vehicle sectors.