Market Trends of Semiconductor Silicon Wafer Industry

The Consumer Electronics Segment is Expected to Occupy a Significant Market Share

- In the current market scenario, many electronic devices, including laptops, smartphones, computers, etc., still use ICs and other semiconductor devices manufactured from silicon substances. Although silicon is still dominating primary applications in the consumer electronics market, new materials have replaced the previous substrates and packaging for a few uses.

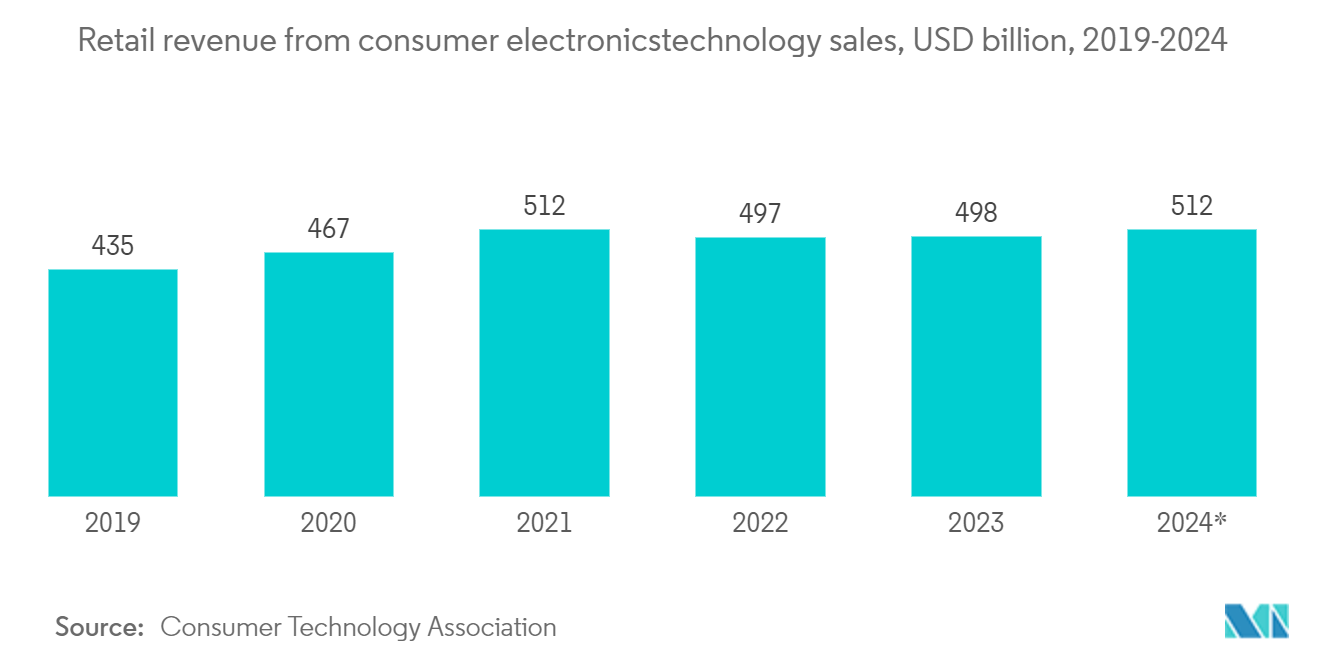

- According to the Consumer Technology Association's (CTA) 'US Consumer Technology Sales and Forecast' study, CTA expects that 5G-enabled smartphone devices will reach 2.1 million units and cross USD 1.9 billion in revenue with triple-digit increases through 2021. Apple announced a contribution of USD 350 billion to the US economy by 2023 and promised 2.4 million jobs over the next five years, which comprises new investments and its existing spending with domestic companies for supply and manufacturing. The company is a prominent player in the consumer electronics industry. Hence, the announcement is expected to propel the demand for semiconductor silicon wafers.

- Recently, the Singapore-MIT Alliance for Research and Technology (SMART), MIT's research enterprise in Singapore, announced the successful development of a commercially viable way to manufacture integrated silicon III-V chips with powerful performance III-V devices inserted into their design.

- In most devices nowadays, silicon-based CMOS chips are primarily used for computing, but they are not efficient for communications and illumination, resulting in low efficiency and heat generation. Thus, current 5G mobile devices on the market get very hot upon use and shut down after a short time. However, combining III-V semiconductor devices with silicon in a commercially viable way is one of the most complex challenges the semiconductor industry faces.

Understand The Key Trends Shaping This Market

Download PDF

North America is Expected to Hold a Significant Share

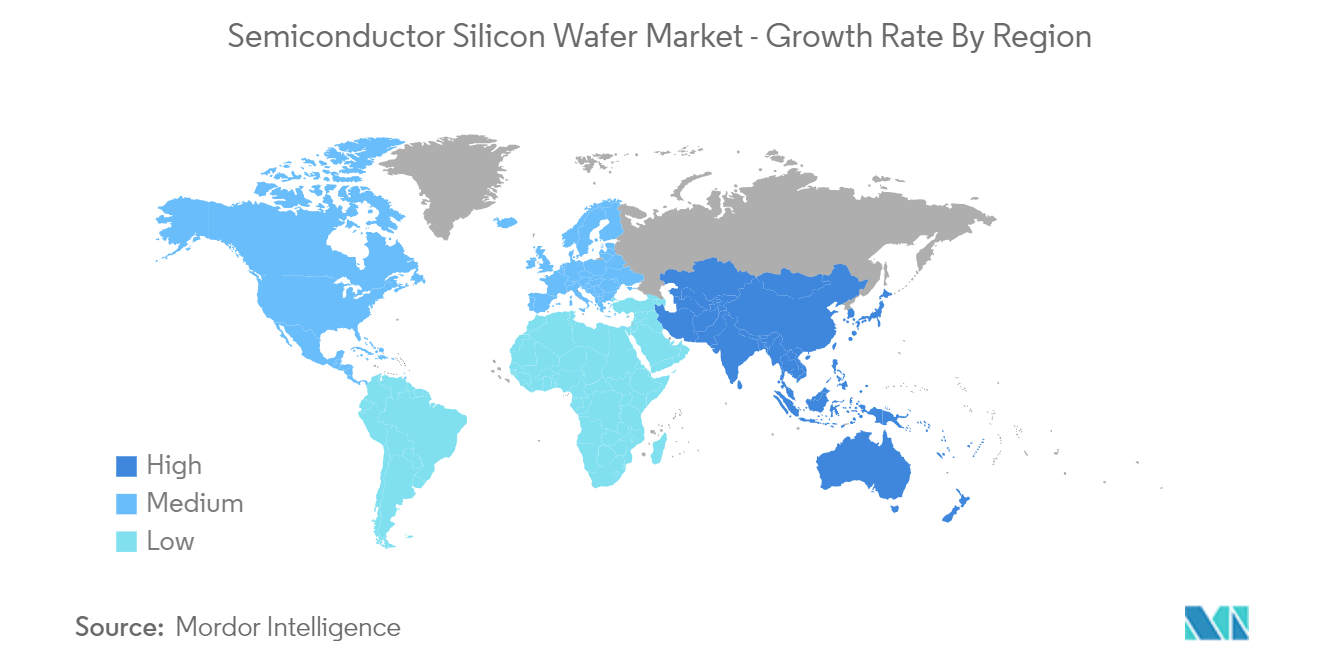

- North America is expected to be a significant revenue contributor to the market by 2021, as fabless semiconductor companies are the prominent customers for semiconductor foundries and wafer players. Fabless companies make chip designs exclusively and market them without a fabrication plant.

- The major fabless companies in the region are AMD, Broadcom, Apple, Qualcomm, Marvell, NVIDIA, and Xilinx. North America has presented a crucial role in advanced semiconductor system design and manufacturing. The region has been witnessing increased activity in establishing semiconductor wafer foundries. TSMC announced that it would spend a total of USD 12 billion from 2021 to 2029 to build a 12-inch wafer plant to manufacture chips using the advanced 5 nm process. Moreover, tech supply chains will continue to shift even after Donald Trump, who pressed foreign companies to invest and create jobs in America, was defected by Joe Biden.

- The electronics industry in the region has been growing steadily and holds a prominent share in several enterprises operating in the design and fabless space. According to the US Census Bureau, the industry revenue of semiconductors and other electronic components in the United States during 2019 stood at USD 100.08 billion, and it is expected to reach USD 105.16 billion by 2023. Smartphones are among the most significant contributors to semiconductor consumption in the consumer electronics sector. In recent years, the region has witnessed consistent growth in smartphone sales.

- Moreover, the United States is home to some of the world's major automotive players, which are investing in electric vehicles and the self-driving potential of cars, which demand high-performance ICs. This is one of the major factors driving the demand for the semiconductor silicon wafers market.

Get Analysis on Important Geographic Markets

Download PDF