Semiconductor Laser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

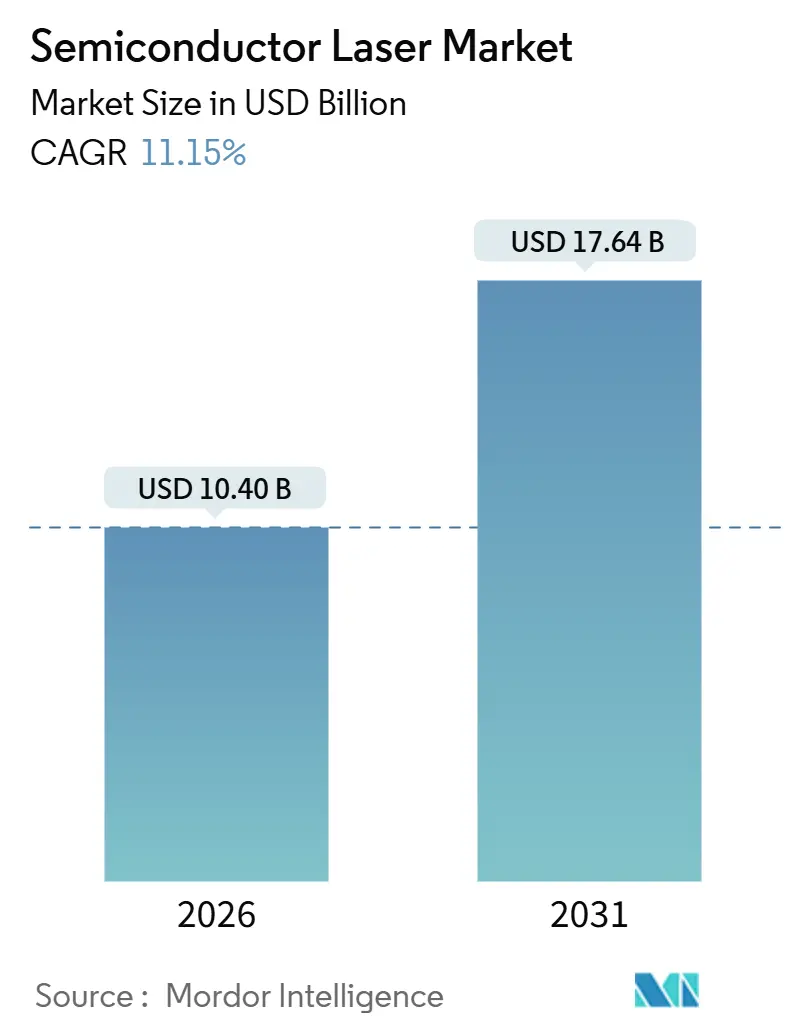

| Market Size (2026) | USD 10.40 Billion |

| Market Size (2030) | USD 17.64 Billion |

| Growth Rate (2026 - 2031) | 11.15% CAGR |

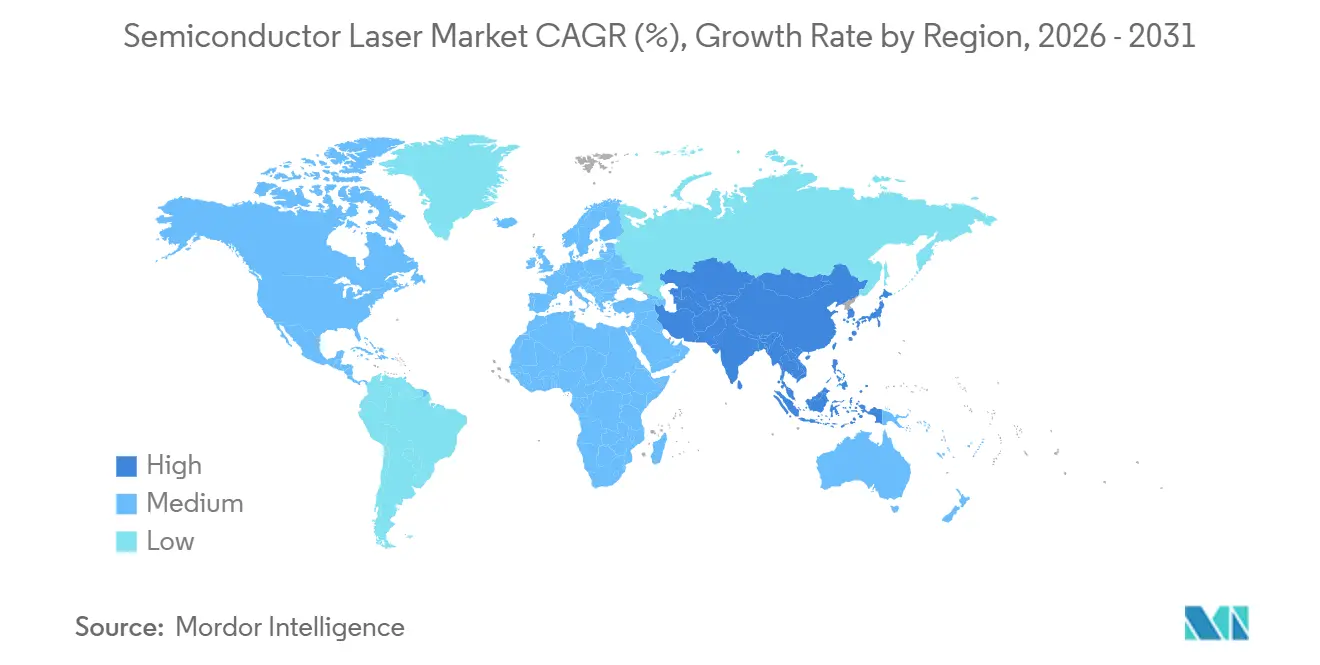

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Semiconductor Laser Market Analysis by Mordor Intelligence

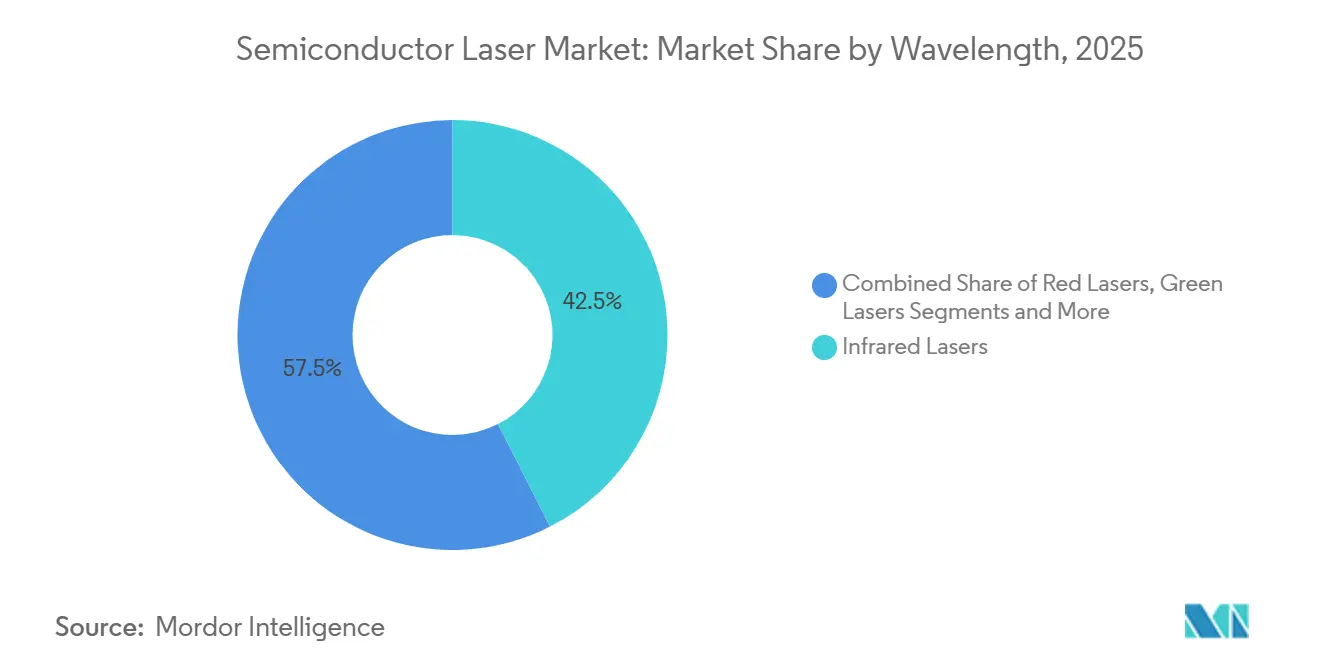

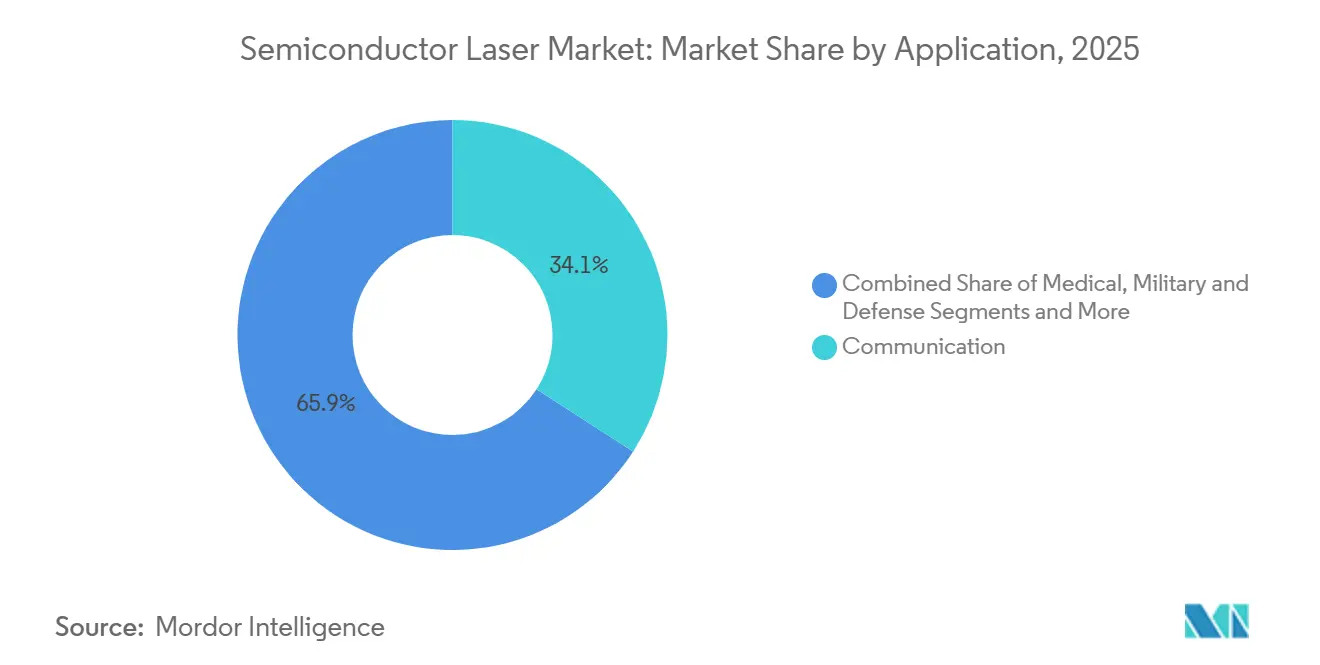

The global semiconductor laser market size was USD 10.40 billion in 2026 and is projected to reach USD 17.64 billion by 2031, representing an 11.15% CAGR over the forecast period. Persistent upgrades to data-center bandwidth, rising automotive safety mandates, and wider consumer adoption of 3D sensing are supporting double-digit revenue expansion, even as compound-semiconductor wafer shortages and thermal-management limits at higher power densities moderate the growth trajectory. Vertical-cavity surface-emitting lasers (VCSELs) held the leading 37.8% share in 2025, propelled by smartphone facial authentication and time-of-flight modules, while quantum cascade lasers (QCLs) are forecast to grow the fastest at a 16.3% CAGR thanks to stronger budgets for industrial gas-sensing and defense chemical-detection systems. Communication applications represented the largest 34.12% revenue slide in 2025, yet automotive end-use is advancing the quickest at 13.2% CAGR as Euro NCAP’s 2025 rules make LiDAR-enabled autonomous emergency braking compulsory. Infrared wavelengths dominated with a 42.5% share, but ultraviolet variants are accelerating at 14.8% CAGR, driven by the demand for extreme-ultraviolet (EUV) lithography tools and medical UV-curable additive manufacturing. Asia-Pacific contributed 48.2% of 2025 revenue, buoyed by China’s gallium-arsenide substrate capacity and Japan’s legacy edge-emitting production; the Middle East is the fastest-growing sub-region at 12.9% CAGR as Saudi Vision 2030 and UAE smart-city programs scale photonics investment.

Key Report Takeaways

- By laser type, VCSELs captured a 37.8% market share of the semiconductor laser market in 2025, while QCLs are set to log the steepest 16.3% CAGR through 2031.

- By application, communication retained the top 34.12% share in 2025, whereas the automotive sector is expanding fastest at a 13.2% CAGR, thanks to LiDAR integration.

- By wavelength, infrared accounted for a dominant 42.5% share in 2025; ultraviolet is forecast to rise at a 14.8% CAGR to 2031.

- By power output, the 100 mW-to-1 W bracket held 46.6% of the semiconductor laser market share in 2025, while devices exceeding 5 W are expected to grow at a 15.7% CAGR over the forecast period.

- By geography, the Asia-Pacific region generated 48.2% of 2025 revenue; the Middle East is leading growth at a 12.9% CAGR due to photonics-rich smart infrastructure programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Semiconductor Laser Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of 3D Sensing in Consumer Electronics | +3.2% | Global, with concentration in Asia-Pacific manufacturing hubs and North America design centers | Short term (≤ 2 years) |

| Emerging Demand from Silicon Photonics Interconnects | +2.8% | North America and Asia-Pacific data-center corridors, spillover to Europe | Medium term (2-4 years) |

| Proliferation of Semiconductor Laser Applications | +2.5% | Global | Medium term (2-4 years) |

| Government-Backed Photonics Manufacturing Initiatives | +1.9% | United States, European Union, China, Japan | Long term (≥ 4 years) |

| Growth in Fiber Laser Adoption | +1.5% | Global, with emphasis on Asia-Pacific and European industrial manufacturing regions | Medium term (2-4 years) |

| Preference for Semiconductor Lasers over Other Light Sources | +1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of 3D Sensing in Consumer Electronics

VCSEL array shipments for time-of-flight and structured-light modules surged as smartphone vendors broadened facial authentication and augmented-reality features, with wall-plug efficiencies topping 45% and reliable operation up to 150 °C without active cooling [1]Source: Nature Photonics, “VCSEL Technology Advances for 3D Sensing Applications,” nature.com . Sony leveraged its back-illuminated sensor expertise to co-package VCSEL dies and CMOS detectors, reducing module footprints by 30% and lowering unit costs to below USD 2 in high-volume orders. Android flagship adoption increased from 18% in 2023 to an estimated 42% in 2025, as manufacturers sought to secure payments and differentiate their products. Euro NCAP cabin-monitoring rules triggered dual-zone VCSEL illuminators that withstand temperatures ranging from -40 °C to +85 °C, thereby tightening epitaxial uniformity requirements. Wearables add another growth vector, with smart glasses and health monitors forecast to exceed 50 million units annually by 2028 as sub-5 mm VCSEL modules enable gesture recognition and non-contact heart-rate sensing.

Emerging Demand from Silicon Photonics Interconnects

Hyperscale operators transitioned from 400G to 800G Ethernet between 2024 and 2025, integrating heterogeneously bonded III-V lasers on silicon to achieve sub-3W lane power and coupling losses of below 0.5 dB. Co-packaged optics place laser arrays directly on switch ASICs, eliminating SerDes bottlenecks and cutting latency by 40 ns, an edge prized for AI training clusters. DARPA committed USD 203 million in 2025 to lift heterogeneous integration yields toward 95%. The current wall-plug efficiency hovers near 10%, falling short of the 20% thermal envelope for air-cooled racks, which has spurred research on quantum-dot gain media and photonic-crystal cavities aimed at achieving 15% by 2027. Kerr frequency combs are displacing discrete arrays, providing 80 channels from one micro-resonator and reducing transceiver bills of materials by 35% in metro networks.

Proliferation of Semiconductor Laser Applications

Automotive body-in-white welding now utilizes 8 kW semiconductor-pumped fiber lasers, whose 100 µm beams enable single-pass welds on 3 mm aluminum without preheating. Medical manufacturers utilize 355 nm UV lasers for sub-10 µm stent cutting, with heat-affected zones of less than 5 µm. Military rangefinders moved to compact semiconductor lasers, slashing system weight by 40% and extending battery life to 72 hours, aligning with NATO soldier-modernization goals. Quantum cascade networks detect methane leaks with a sensitivity of sub-ppb, fulfilling the U.S. EPA's 2024 rule for upstream oil and gas operators. Additive manufacturing leverages 365 nm and 405 nm diodes to cure layers in under 2 seconds, enabling biocompatible implants with <1 µm surface roughness.

Government-Backed Photonics Manufacturing Initiatives

The CHIPS and Science Act earmarks USD 52.7 billion for semiconductors, including USD 300 million for advanced packaging that specifically names photonics. DARPA’s LUMOS program invests USD 10 million to demonstrate monolithic distributed-feedback lasers on silicon. The EU’s Horizon initiative commits EUR 25 million to integrated photonics, targeting <1 dB coupling loss and 200 mm wafer scaling. China’s Phase III Big Fund reserves CNY 200 billion (≈ USD 28 billion) for gallium-nitride and indium-phosphide capacity, with provincial subsidies covering 30% of capex. Japan’s METI launched a JPY 50 billion (~ USD 340 million) photonics program in 2025 to build 6-inch gallium-arsenide pilot lines and cut costs by 20% through automation.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility of Compound Semiconductor Wafers | -1.8% | Global, with acute pressure in North America and Europe, dependent on the Asia-Pacific substrate supply | Short term (≤ 2 years) |

| Thermal Management Challenges at High Power Outputs | -1.3% | Global, most pronounced in industrial and automotive high-power applications | Medium term (2-4 years) |

| Stringent Export Controls on Advanced Photonics | -0.9% | Global, particularly affecting trade between the United States, the European Union, and China | Medium term (2-4 years) |

| Difficulties Regarding Reliability and Testing | -0.7% | Global, with heightened impact in automotive and medical device qualification cycles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility of Compound Semiconductor Wafers

Four suppliers control 78% of global gallium-arsenide wafer capacity, leaving the semiconductor laser market exposed to sudden demand swings. China’s August 2023 curbs on gallium and germanium stretched 6-inch substrate lead times from 12 to 26 weeks and pushed spot prices 40% higher by early 2024. Hyperscale buyers locked long-term indium-phosphide contracts, crowding smaller diode makers toward less flexible gallium-arsenide alternatives. Dual-sourcing requires 18–24 months of AEC-Q100 and Telcordia GR-468-CORE testing, which delays diversification. Scaling from 4- to 6-inch wafers remains capital-intensive; a single MOCVD reactor costs USD 4 million and needs 95% utilization for a 5-year payback.

Thermal Management Challenges at High Power Outputs

Junction temperatures above 100 °C in ≥5 W lasers shift wavelengths by 0.3 nm/°C and reduce quantum efficiency by 15% compared to 25 °C baselines. Thermoelectric coolers add USD 8–12 per module and 3–5 W of parasitic power, tightening system-level efficiency. Achieving <2 K/W thermal resistance in <10 mm² packages needs gold-tin or sintered-silver attach, increasing assembly cost by 25% and lowering yields. Catastrophic optical damage risk climbs when local heating exceeds 150 °C, shortening mean time between failures from 100,000 hours at 25 °C to <20,000 hours at 85 °C. Liquid cooling works in labs but is impractical for consumer and automotive gear, forcing designers to trade output power against reliability and size.

Segment Analysis

By Wavelength: Infrared Scale Anchors Growth While Ultraviolet Accelerates

Infrared lasers accounted for 42.5% of 2025 revenue, underpinning the semiconductor laser market through 850 nm and 1,550 nm devices that dominate consumer 3D sensing and long-haul fiber links [2]Source: Optica Publishing Group, “Miniaturized VCSEL Modules,” opg.optica.org. Ultraviolet variants, although smaller in absolute dollars, will climb at a 14.8% CAGR to 2031 on EUV lithography shipments and medical UV-curable prototyping, pointing to a rising semiconductor laser market size contribution from advanced manufacturing tools.

VCSEL-based infrared modules deliver circular beams that simplify coupling, while QCL-based mid-infrared sources provide tunability for gas sensing. Ultraviolet penetration remains cost-sensitive but emerging 266 nm diodes promise higher yields and longer lifetimes. Regulatory IEC 60825 Class 3B and Class 4 limits demand sophisticated interlocks above 5 mW, influencing design budgets and time to market. As advanced logic nodes migrate below 3 nm, lithography tool vendors will propel ultraviolet demand, reinforcing its double-digit climb within the semiconductor laser market.

Note: Segment shares of all individual segments available upon report purchase

By Laser Type: VCSEL Leadership Faces Quantum Cascade Momentum

VCSELs captured a 37.8% share, thanks to wafer-scale testing that reduces die cost below USD 0.50, thereby safeguarding their leadership in the semiconductor laser market. QCLs, however, are racing ahead at a 16.3% CAGR through 2031, as mid-infrared spectroscopy gains regulatory tailwinds, suggesting a growing impact on the semiconductor laser market size from environmental and defense programs.

Edge-emitting bars retain relevance for multi-kilowatt industrial cutting, yet their 6% CAGR lags. Fiber lasers, although technically outside the pure semiconductor classification, depend on diode pumping and maintain a 9% trajectory. Narrow-linewidth external-cavity diodes fill metrology niches requiring <1 MHz linewidth. Over the forecast period, design wins in automotive LiDAR and gas monitoring will help QCLs erode VCSEL dominance, diversifying revenue streams within the semiconductor laser market.

By Application: Communication Dominance Meets Automotive Upswing

Communication retained the largest 34.12% revenue slice in 2025, leveraging VCSEL-based 100 Gbit short-reach links and 1,550 nm coherent modules for metro spans. Automotive, however, is tracking a 13.2% CAGR, and its expanding sensor suite is set to lift the semiconductor laser market size in safety-critical systems through 2031.

Medical demand advances 8% annually as femtosecond ophthalmic and dermatology systems grow procedure volumes. Military programs sustain a 10% CAGR on airborne rangefinders and directed-energy prototype funding. Industrial automation and instrumentation continue to maintain steady single-digit gains, but LiDAR-driven automotive growth keeps the spotlight on as original-equipment manufacturers secure multi-year contracts.

Note: Segment shares of all individual segments available upon report purchase

By Power Output: Mid-Range Prevalence Yields to High-Power Momentum

Lasers rated 100 mW–1 W held 46.6% of the semiconductor laser market share in 2025, anchored by consumer biometrics and short-reach optics. Devices above 5 W will surge at a 15.7% CAGR, thanks to sheet-metal cutting migrations and pulsed automotive LiDAR, which will buoy the overall semiconductor laser market size for industrial and mobility users.

Below-100 mW pointers inch ahead at 4% as smartphones displace handheld scanners. The 1 W–5 W bracket maintains an 8% growth rate, catering to surgical tools and projection systems. Higher-power classes face stricter Class 4 compliance, adding cost and engineering complexity, yet their superior throughput justifies the investment in high-volume manufacturing.

Geography Analysis

The Asia-Pacific region generated 48.2% of 2025 revenue, reflecting China’s 60% share of global VCSEL epitaxial wafers and Japan’s 200 million-unit annual diode output. Samsung’s foundry-scale gallium-arsenide services trim wafer costs by 20%, while India’s 25% subsidy attracts new assembly lines. Singapore, Hong Kong, and Tokyo data center expansions, which require 800 Gbit transceivers, are expected to support a 10.8% regional CAGR, keeping the Asia-Pacific region central to the semiconductor laser market.

North America accounted for 28% of 2025 sales, driven by hyperscale cloud consumption, which comprises 40% of global silicon photonics shipments. The CHIPS Act will fund domestic epitaxial wafers; however, new fabs typically require 36 to 48 months to reach volume production. Canada’s CAD 100 million photonics cluster and Mexico’s duty-free equipment imports under USMCA strengthen continental resilience.

Europe captured 18% revenue, anchored by Germany’s TRUMPF and ams-OSRAM plus Fraunhofer R&D. Horizon funds and UK pilot lines enhance heterogeneous integration, while RoHS and REACH compliance add six-to-twelve-month qualification overhead. The Middle East’s 12.9% CAGR is driven by NEOM’s USD 500 billion investment, which incorporates LiDAR into mobility infrastructure. South America and Africa together supply 6% of the revenue, with Brazil’s.

Competitive Landscape

The semiconductor laser market is moderately concentrated: the top five suppliers, Coherent, Lumentum, ams-OSRAM, IPG Photonics, and TRUMPF, held about 42% of 2025 revenue [3]Source: Coherent Investor Relations, “Merger Integration Update,” investors.coherent.com. Coherent’s 2022 II-VI merger united gallium-nitride and silicon-carbide capabilities across ultraviolet to 10 µm wavelengths. Lumentum and ams-OSRAM are expanding 6-inch VCSEL lines by 2 million wafers annually, dropping per-die costs by 18% and enabling sub-USD 2 automotive modules.

IPG Photonics maintains its fiber-laser leadership through vertical integration and achieves 30% gross margins, despite Chinese competitors undercutting prices by 25%. TRUMPF collaborates with Fraunhofer to co-develop QCL gas sensors, while Coherent invests USD 150 million in Texas silicon-carbide substrates to localize supply and mitigate Asia risks. Technology differentiation centers on epitaxial design: ams-OSRAM’s VCSEL architecture sustains 50% wall-plug efficiency at 150 °C, extending battery life in mobile devices by 30%.

Regional diversification is intensifying. Lumentum’s Thailand assembly plant hedges geopolitical tension, and Sharp’s 405 nm blue-laser ramp addresses automotive headlamp demand. White-space bets include non-invasive glucose monitoring via 9 µm QCLs, a potential USD 3 billion addressable segment pending clinical validation. Hybrid silicon-III-V co-packaged optics remain years out, but DARPA funding indicates strategic persistence.

Semiconductor Laser Industry Leaders

Coherent Corporation

Nichia Corporation

IPG Photonics Corporation

TRUMPF Group

ams-OSRAM AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Coherent committed USD 200 million to expand its New Jersey compound semiconductor fab, adding 50,000 ft² for 6-inch GaAs and InP production, aimed at 2026 volume ramps.

- September 2025: Lumentum secured a USD 180 million multi-year VCSEL supply pact with a European tier-one automotive supplier for driver-monitoring systems starting Jan 2026.

- August 2025: ams-OSRAM opened a Malaysia plant with 3 million VCSEL-module annual capacity, supported by MYR 150 million incentives.

- July 2025: TRUMPF and Fraunhofer began a EUR 12 million QCL program for methane detection at 10 ppb sensitivity.

Global Semiconductor Laser Market Report Scope

Semiconductor lasers based on semiconductor gain media involving optical amplification are achieved by stimulated emission at an interband transition under conditions of a high carrier density in the conduction band. Most of these are laser diodes that are pumped with an electrical current.

The Semiconductor Laser Market Report is Segmented by Wavelength (Infrared, Red, Green, Blue, and Ultraviolet), Laser Type (Edge-Emitting, VCSEL, Quantum Cascade, and Fiber), Application (Communication, Medical, Military and Defense, Industrial, Instrumentation and Sensor, and Automotive), Power Output (Below 100 mW, 100 mW to 1 W, 1 W to 5 W, and Above 5 W), and Geography. Market Forecasts are in Value (USD).

| Infrared Lasers |

| Red Lasers |

| Green Lasers |

| Blue Lasers |

| Ultraviolet Lasers |

| Edge-Emitting Lasers (EEL) |

| Vertical-Cavity Surface-Emitting Lasers (VCSEL) |

| Quantum Cascade Lasers |

| Fiber Lasers |

| Other Types |

| Communication |

| Medical |

| Military and Defense |

| Industrial |

| Instrumentation and Sensor |

| Automotive |

| Other Applications |

| Below 100 mW |

| 100 mW – 1 W |

| 1 W – 5 W |

| Above 5 W |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Wavelength | Infrared Lasers | |

| Red Lasers | ||

| Green Lasers | ||

| Blue Lasers | ||

| Ultraviolet Lasers | ||

| By Laser Type | Edge-Emitting Lasers (EEL) | |

| Vertical-Cavity Surface-Emitting Lasers (VCSEL) | ||

| Quantum Cascade Lasers | ||

| Fiber Lasers | ||

| Other Types | ||

| By Application | Communication | |

| Medical | ||

| Military and Defense | ||

| Industrial | ||

| Instrumentation and Sensor | ||

| Automotive | ||

| Other Applications | ||

| By Power Output | Below 100 mW | |

| 100 mW – 1 W | ||

| 1 W – 5 W | ||

| Above 5 W | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the semiconductor laser market expected to grow through 2031?

Revenue is forecast to rise from USD 10.40 billion in 2026 to USD 17.64 billion by 2031, representing an 11.15% CAGR.

Which laser type will add the most incremental revenue by 2031?

Quantum cascade lasers, projected to expand at a 16.3% CAGR, will generate the largest new revenue pool, particularly in mid-infrared sensing.

Why are automotive applications gaining momentum?

Euro NCAP’s 2025 autonomous emergency braking requirement and wider adoption of LiDAR and driver-monitoring systems are driving a 13.2% CAGR in automotive demand.

What region offers the highest growth rate over the forecast period?

The Middle East leads with a 12.9% CAGR as Saudi Vision 2030 and UAE smart-city projects pour capital into photonics-enabled infrastructure.

What is the key supply-chain risk for laser manufacturers?

Concentrated gallium-arsenide and indium-phosphide wafer supply, accentuated by China’s export restrictions, extends lead times and inflates substrate prices.

How are vendors addressing high-power thermal challenges?

Solutions include gold-tin or sintered-silver die attach, improved heat-sink materials, and efficiency-enhanced epitaxial designs to keep junction temperatures below critical thresholds.