Semiconductor Industry Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

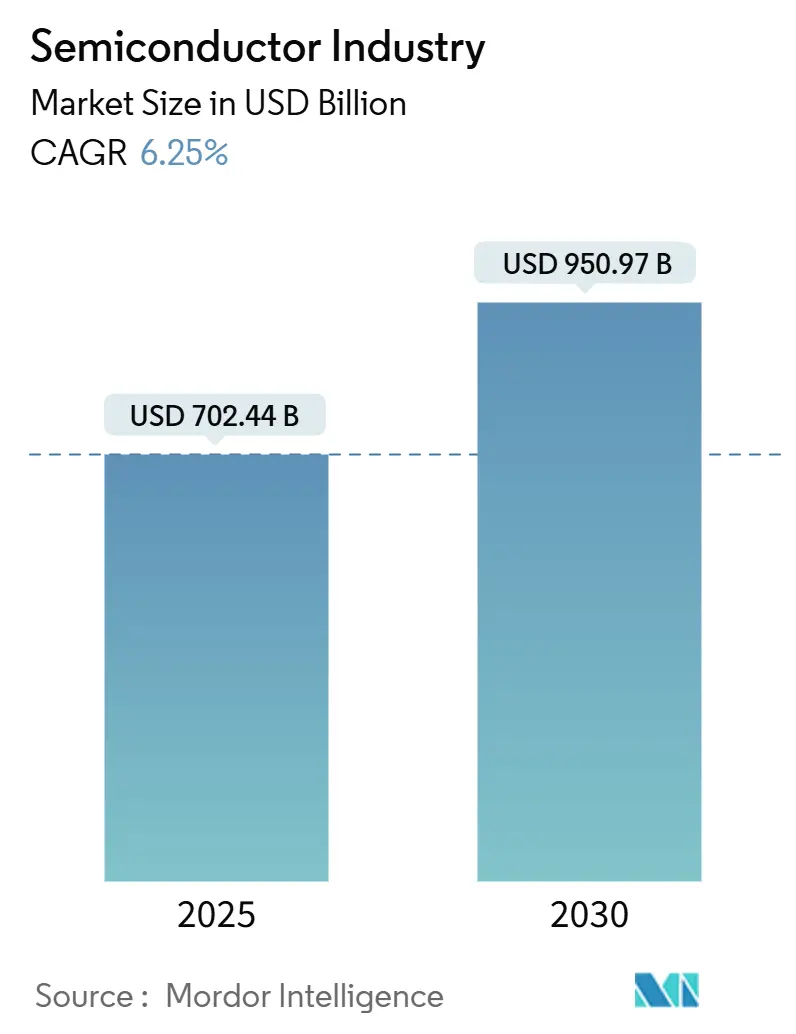

| Market Size (2025) | USD 702.44 Billion |

| Market Size (2030) | USD 950.97 Billion |

| Growth Rate (2025 - 2030) | 6.25% CAGR |

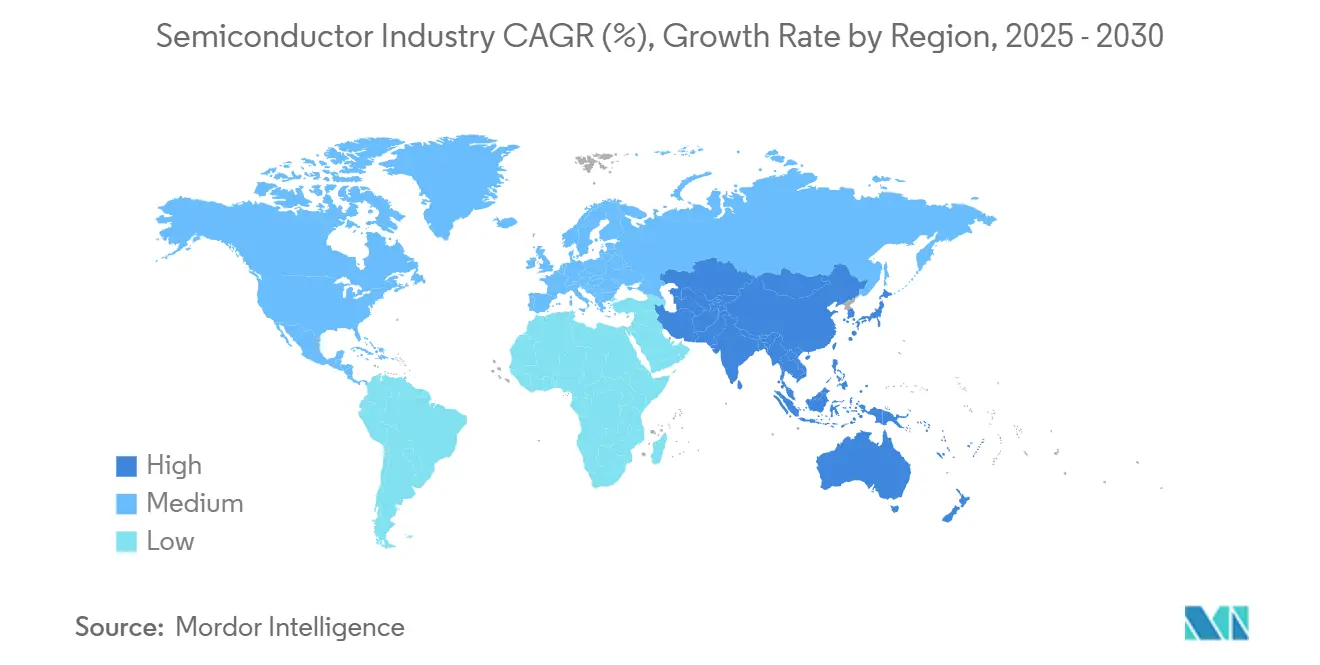

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

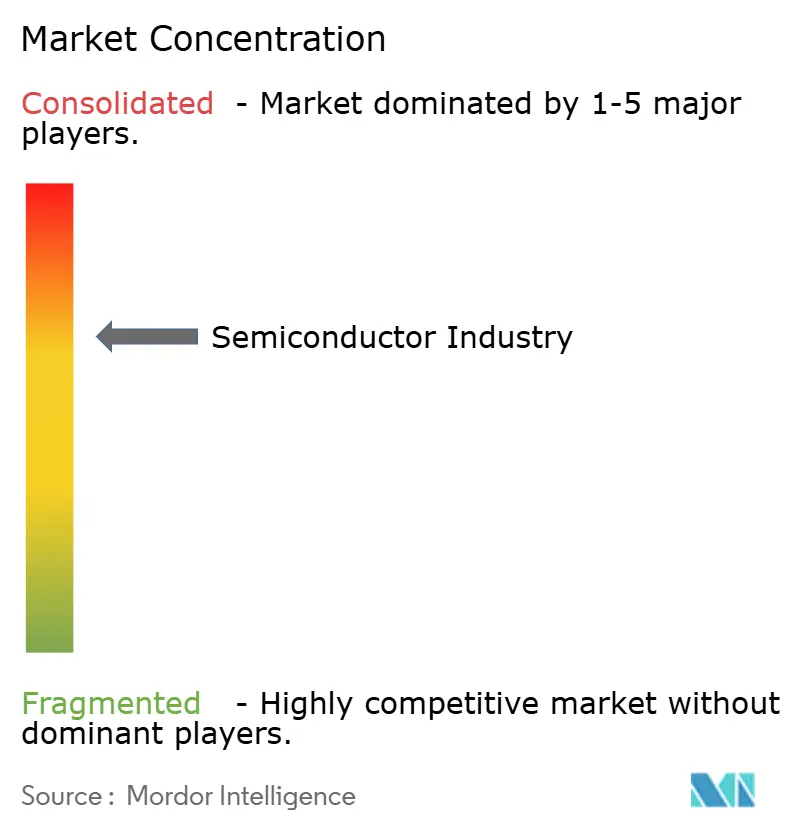

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Semiconductor Industry Analysis by Mordor Intelligence

The global semiconductor market size was valued at USD 702.44 billion in 2025 and is forecast to reach USD 950.97 billion by 2030, expanding at a 6.25% CAGR across the period. Unit shipments were 1.04 trillion in 2025 and are projected to climb to 1.43 trillion by 2030 at a 6.47% volume CAGR. Momentum stems from concurrent waves of artificial intelligence (AI), edge computing, and automotive electrification that are reshaping design priorities, capital-expenditure patterns, and supply-chain footprint. Asia-Pacific continued to anchor more than four-fifths of semiconductor market revenue in 2024, while foundry leaders raced to commercialize 3 nm and 2 nm processes that meet the power-efficiency demands of next-generation data-center and automotive platforms. At the same time, heterogeneous integration and chiplet-based architectures reduced development cost profiles and accelerated time-to-market, supporting a new layer of ecosystem specialization. Water, power, and talent constraints in advanced fabs incentivized geographic diversification, driving the semiconductor market toward a more distributed yet deeply interconnected production model.

Key Report Takeaways

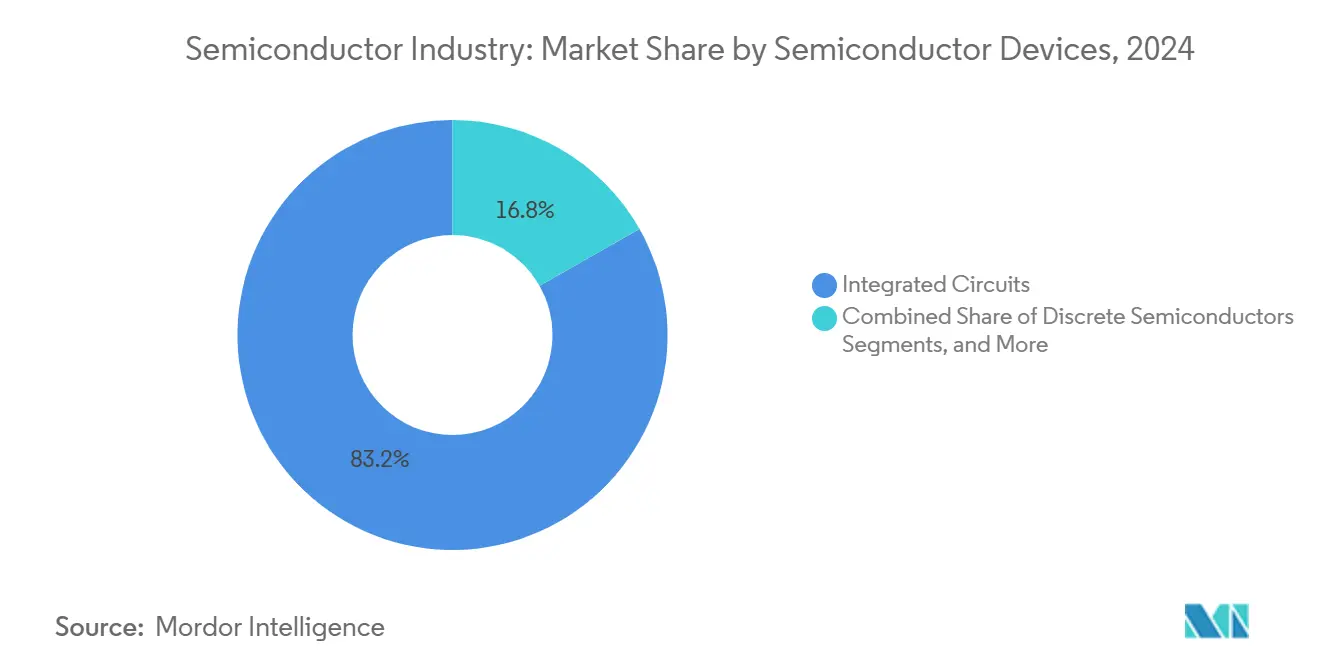

- By semiconductor device, integrated circuits captured 83.2% of the semiconductor market share in 2024; the same segment is projected to post a 6.7% CAGR through 2030.

- By technology node, the 5 nm platform led with 34.3% of the semiconductor market share in 2024, while the 3 nm node is projected to expand at an 8.7% CAGR to 2030.

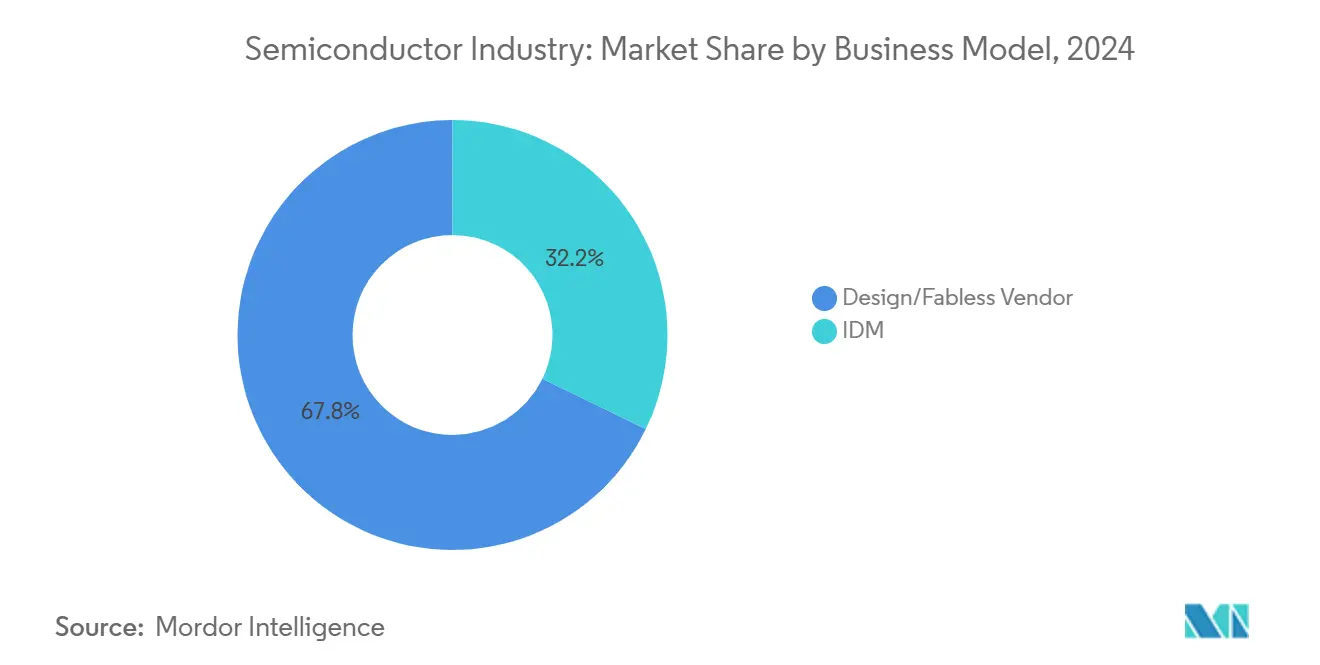

- By business model, the fabless segment accounted for 67.8% share of the semiconductor market size in 2024 and is forecast to grow at an 8.1% CAGR through 2030.

- By end-user industry, communication equipment held 28.7% of the semiconductor market size in 2024; government-grade aerospace and defense applications register the fastest projected CAGR at 7.36% to 2030.

- By geography, Asia-Pacific generated 81.3% of total revenue in 2024 and is pacing the global semiconductor market with a regional CAGR of 6.9% between 2025-2030.

Global Semiconductor Industry Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive data-center demand for AI accelerators | +1.8% | North America, China, Western Europe | Medium term (2-4 years) |

| Ubiquitous edge-AI in consumer IoT devices | +1.2% | North America, Western Europe, East Asia | Medium term (2-4 years) |

| Automotive zonal-architecture migration | +0.9% | Europe, North America, China, Japan | Long term (≥ 4 years) |

| On-shoring incentives across the US, EU, India, MENA | +0.7% | North America, Europe, India, Middle East and North Africa | Medium term (2-4 years) |

| Heterogeneous integration cost-down inflection | +0.5% | Advanced manufacturing hubs | Medium term (2-4 years) |

| Chiplet marketplace commercialization (UCIe/IP) | +0.4% | North America, East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive data-center demand for AI accelerators

Hyperscale operators scaled capital spending around graphics processing units (GPUs) and other AI accelerators that enable large-language-model training and inference. TSMC reported a record surge in high-performance computing wafer starts, and management disclosed that AI processors will approach one-fifth of corporate revenue by 2028.[1]Taiwan Semiconductor Manufacturing Co., “2024 Annual Report,” tsmc.com The appetite for compute density is rippling through the memory hierarchy as high-bandwidth memory (HBM) becomes a default pairing with AI accelerators, pushing leading DRAM houses to allocate additional capacity to HBM stacks. Power envelopes near 2–3 kW per rack are forcing data-center operators to redesign electrical distribution and liquid-cooling loops, which in turn stimulates demand for advanced power-management and sensor ICs. This tight coupling between compute, memory, and infrastructure firmly positions the semiconductor market as the backbone of AI-first digital transformation.

Ubiquitous edge-AI in consumer IoT devices

Smartphones, wearables, and smart-home appliances increasingly integrate neural-processing units that execute machine-learning models locally, enhancing privacy and reducing cloud latency. The semiconductor market responded with a wave of low-power ASICs and microcontrollers optimized for on-device inference, supporting functions such as voice recognition, gesture control, and real-time translation. As edge-AI workloads move beyond premium smartphones into mid-tier devices, design wins are spreading across a broader set of fabless vendors that leverage specialized foundry processes, including embedded non-volatile memory and advanced packaging. The shift decentralizes compute placement and accelerates the adoption of heterogeneous system-on-chip (SoC) designs that combine CPU, GPU, DSP, and NPU elements on a single substrate.

Automotive zonal-architecture migration (EV and ADAS)

Vehicle electronics are consolidating from scores of standalone electronic control units to a handful of high-performance compute zones linked via gigabit in-vehicle networks. That evolution increases per-vehicle semiconductor content, especially for advanced process nodes at 7 nm and below that deliver the deterministic latency and functional safety demanded by Level-2+ driver-assistance systems. The Automotive SerDes Alliance and the ASRA initiative targeted chiplet-based reference designs for automotive compute domains, fostering a supply chain where base die, accelerators, and security islands can be sourced from different vendors yet assembled within a single package. Long homologation cycles favor suppliers able to guarantee road-map visibility for 10 years or more, reinforcing the strategic importance of secure, multi-node manufacturing footprints.

On-shoring incentives in the US, EU, India and MENA

National industrial policy programs reshaped capital allocation maps across the semiconductor market. The United States CHIPS and Science Act earmarked USD 52 billion in direct grants and USD 100 billion in tax incentives with a goal of doubling domestic leading-edge capacity by 2030. Europe’s Chips Act pursues a similar 20% global-share target, while India’s semiconductor incentive scheme backs greenfield fabs in logic, memory, and advanced packaging. Incentives triggered commitments exceeding USD 540 billion across 28 U.S. states and encouraged parallel investments in equipment, materials, and design ecosystems. Over the medium term, diversified capacity mitigates single-region shock risk, but it also introduces coordination challenges around standards and workforce development.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent lithography bottlenecks below 2 nm | -0.7% | Taiwan, South Korea, United States | Long term (≥ 4 years) |

| Geopolitical export-control escalations | -0.6% | China, United States, Netherlands, Taiwan | Medium term (2-4 years) |

| Water and power scarcity in foundry clusters | -0.4% | Taiwan, Arizona, Israel, Singapore | Medium term (2-4 years) |

| Talent crunch in sub-5 nm process engineering | -0.3% | Advanced manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent lithography bottlenecks below 2 nm

Commercial deployment of sub-2 nm nodes hinges on extreme-ultraviolet (EUV) exposure systems that balance cost, throughput, and yield. ASML’s first High-NA EUV machines carry price tags near USD 380 million per unit and require vibration-free clean-room floors the size of a basketball court. Although prototype tools demonstrated line-width targets, throughput remained a gating factor to high-volume manufacturing, prompting parallel investigation into nanoimprint lithography and directed self-assembly. The capital intensity filters prospective entrants, tightening the competitive circle to a handful of integrated device manufacturers and foundries capable of absorbing multibillion-dollar equipment cycles.

Geopolitical export-control escalations (US-CN, CN-NL)

Successive rounds of export-control measures expanded beyond logic and memory tools into metrology, design software, and maintenance services, directly influencing procurement strategies. A Johns Hopkins University review found that more than 140 Chinese entities faced new licensing hurdles by early 2025, which accelerated local substitution programs and reduced near-term addressable demand for U.S. equipment suppliers.[2]Johns Hopkins University, “Restrictions on Trade with China Harm U.S. Leadership in Technology,” sais.jhu.edu The Netherlands further tightened deep-UV equipment licensing, and multinational chipmakers adopted dual-qualification production plans to mitigate cross-border supply interruptions. The resulting fragmentation raises compliance costs and elongates time-to-market for devices that need truly global sourcing of IP, materials, and talent.

Segment Analysis

By Semiconductor Devices: Integrated circuits sustain leadership amid specialization

Integrated circuits retained their foundational role in the semiconductor market, and their 83.2% revenue position in 2024 underscored the primacy of high-density digital logic and memory in an AI-first economy. This sub-segment is projected to grow at a 6.7% CAGR through 2030, underpinned by server-class CPUs, AI accelerators, and advanced analog front-ends that regulate power consumption in electric vehicles. Dynamic random-access memory suppliers continued to prioritize high-bandwidth variants tuned for AI workloads, while analog IC houses capitalized on the electrification wave across mobility and industrial automation.

Discrete semiconductors, although a smaller share of the semiconductor market, served mission-critical roles in voltage regulation, motor-drive efficiency, and radio-frequency switching. Wide-bandgap transistors based on silicon-carbide and gallium-nitride technologies moved further into traction inverters and fast-charging stations. Optoelectronics revenue benefited from the rollout of machine-vision cameras and lidar assemblies, whereas the sensors and MEMS landscape expanded alongside industrial Internet of Things gateways. Competitive dynamics favored niche depth over portfolio breadth: vendors refined value propositions around performance per watt, extended temperature ranges, and functional safety certification rather than pursuing volume across every device type.

Note: Segment shares of all individual segments available upon report purchase

By Technology Node: 3 nm surges while mature nodes hold essential roles

Node-transition economics bifurcated the semiconductor market into leading-edge and mature-node camps. The 5 nm family delivered 34.3% revenue share in 2024; however, customer migration toward 3 nm processes is forecast to deliver an 8.7% CAGR from 2025-2030. TSMC reported that its 3 nm platform reached mass-production yields and provided 20% of corporate revenue in late 2024. Smartphone application processors and AI-centric system-on-chips were first adopters, and automotive original-equipment manufacturers signaled road-map alignment once functional-safety libraries finish qualification.

Mature geometries at 28 nm and above retained healthy utilization thanks to power-management ICs, microcontrollers, and RF front-ends whose specifications rely more on analog performance, radio characteristics, or embedded Flash, not transistor density. GlobalFoundries, UMC, and specialty foundries leveraged that demand, frequently adding value through radio-frequency optimizations or embedded non-volatile memory. Capital-expenditure differentials widened: greenfield leading-edge fabs crossed USD 20 billion per site, while brownfield mature-node expansions proceeded at lower cost, enabling emerging regions to enter the manufacturing landscape with less financial risk.

By Business Model: Fabless design houses extend innovation lead

Fabless design entities commanded 67.8% revenue share within the semiconductor market in 2024 and are projected to log an 8.1% CAGR to 2030. The model unlocks agility in target-application focus, allowing companies such as NVIDIA and Qualcomm to iterate on AI and connectivity architectures while outsourcing production to foundries with best-in-class process nodes. Chiplet adoption further amplified fabless advantages by lowering monolithic die sizes, thereby reducing tape-out risk and enabling rapid respins for emerging workloads.

Integrated device manufacturers (IDMs) preserved competitive moats in memory and x86 processors, yet even stalwarts pursued hybridized strategies. Intel’s IDM 2.0 plan combined internal wafer capacity with foundry services, while joint-venture agreements allowed shared risk in advanced-node deployments. Design-for-manufacturability teams increasingly coordinated across corporate lines, creating value chains where IP libraries, test-interface standards, and advanced packaging nodes could be licensed or shared to compress development cycles.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Communications remain core; aerospace and defense accelerate

Communications infrastructure and devices represented 28.7% of semiconductor market revenue in 2024, reflecting 5G base-station densification, fiber-to-the-home rollouts, and the first deployments of 6G testbeds. The appetite for low-latency connectivity elevated demand for front-haul optical-module ICs, packet-processing ASICs, and millimeter-wave transceivers. Across the forecast window, growth shifts toward multi-function radios that integrate satellite, sub-6 GHz, and Wi-Fi 7 bands into common basebands.

Aerospace and defense spending is poised for a 7.36% CAGR to 2030, transforming into the fastest-growing vertical. Sovereign supply-chain priorities encouraged domestic sourcing of radiation-hardened logic, secure memory, and high-temperature power devices. Automotive semiconductor content remained on a double-digit trajectory as electrification, advanced driver-assistance systems, and zonal architecture intersected. Data-center build-outs rejuvenated the computing segment, while industrial demand pivoted to predictive-maintenance sensors and real-time control microcontrollers that embed AI inference at the factory edge.

Geography Analysis

Asia-Pacific held 81.3% of semiconductor market revenue in 2024 and is projected to grow at a 6.9% CAGR through 2030. Taiwan’s foundries maintained a dominant share of 3 nm and 5 nm wafer starts, while South Korean leaders accounted for the bulk of DRAM and NAND output. Japan stayed indispensable in photoresists, silicon wafers, and precision materials. Mainland China, despite export-control headwinds, expanded mature-node capacity and invested in indigenous EDA tools, which may account for over one-quarter of the 28 nm supply by 2025.[3]Government of the Netherlands, “Export Control Measures for Semiconductor Equipment,” government.nl

North America experienced a resurgence in domestic fab construction underpinned by the CHIPS and Science Act. Commitments totaling USD 540 billion spanned logic, memory, and advanced packaging, complemented by workforce-training alliances with community colleges and research universities. The region’s chip-design prowess continued to exceed 50% of global fabless sales, with ecosystem depth ranging from IP cores to semiconductor capital equipment.

Europe’s semiconductor market strategy emphasized strategic autonomy. The European Chips Act aimed for a 20% global share by 2030 and concentrated on automotive, industrial, and compound-semiconductor niches suited to regional strengths. New cluster investments in Germany, France, and the Netherlands focused on gallium-nitride power devices and silicon-carbide MOSFETs for renewable-energy inverters. Emerging hubs in India, Brazil, and Gulf Cooperation Council states targeted mature-node logic, outsourced assembly-and-test (OSAT) services, and specialty analog lines. India’s incentive package promoted a full-stack ecosystem from design to packaging, responding to domestic semiconductor imports that reached USD 20.19 billion in 2024.

Competitive Landscape

The semiconductor market exhibits a high-concentration structure in leading-edge foundry, GPU, and HBM segments, contrasted with fragmentation in analog, power discretes, and specialty sensors. TSMC, Samsung Foundry, and Intel collectively monitored the 2 nm and 1.8 nm road-map milestones while competing on advanced packaging throughput. Apple expanded vertical integration by introducing self-designed cellular modems, and several automotive OEMs funded ASIC development centers to safeguard supply continuity.

Chiplet adoption redrew competitive boundaries: interface standards such as Universal Chiplet Interconnect Express (UCIe) enabled third-party IP blocks to integrate into multivendor packages. Marvell, Intel, and Synopsys demonstrated cross-vendor interposer prototypes in 2025, shrinking time-to-qualification for heterogenous systems. Access to precision plating, micro-bump, and hybrid-bonding capacity emerged as a determinant of leadership, partly shifting bargaining power from wafer fabs to advanced packaging houses.

Emerging disruptors addressed lithography cost ceilings with alternative tooling. IBM’s Albany NanoTech complex achieved new yield benchmarks on Low-NA and High-NA EUV flows that promise to simplify patterning at 7 nm, 5 nm, and 2 nm nodes.[4]IBM Research, “New EUV Patterning Yield Benchmarks,” research.ibm.com Concurrently, several startups pursued nanoimprint lithography for specialized markets where the tooling cost outweighs volume. Across analog segments, fab-lite suppliers leveraged proprietary process recipes at specialty foundries to protect margins against commoditization.

Semiconductor Market Leaders

-

Intel Corporation

-

Samsung Electronics Co. Ltd

-

Qualcomm Incorporated

-

SK Hynix Inc.

-

Taiwan Semiconductor Manufacturing Company (TSMC) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TSMC raised its U.S. investment commitment to USD 165 billion, spanning three logic fabs, two packaging plants, and a major R&D center.

- April 2025: GlobalFoundries unveiled a USD 16 billion U.S. expansion plan focused on mature-node and RF capacity for automotive and industrial customers.

- March 2025: TSMC entered joint-venture talks with NVIDIA, Broadcom, Qualcomm, and AMD aimed at aligning advanced-packaging capacity with AI accelerator demand.

- March 2025: IBM and partners at the Albany NanoTech Complex recorded yield breakthroughs for High-NA EUV lithography that will underpin sub-2 nm node commercialization.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the semiconductor market as revenues derived from the sale of new discrete, optoelectronic, sensor/MEMS, and integrated-circuit devices that are designed, fabricated, and packaged for use across communication, computing, industrial, automotive, consumer, and government equipment.

Scope exclusion: Equipment, materials, and foundry contract services are outside this value pool to keep the focus on device shipments only.

Segmentation Overview

- By Semiconductor Devices

- Discrete Semiconductors

- Diodes

- Transistors

- Power Transistors

- Rectifier and Thyristor

- Other Discrete Devices

- Optoelectronics

- Light-Emitting Diodes (LEDs)

- Laser Diodes

- Image Sensors

- Optocouplers

- Other Device Types

- Sensors and MEMS

- Pressure

- Magnetic Field

- Actuators

- Acceleration and Yaw Rate

- Temperature and Others

- Integrated Circuits

- Analog

- Micro

- Microprocessors (MPU)

- Microcontrollers (MCU)

- Digital Signal Processors

- Logic

- Memory

- Discrete Semiconductors

- By Technology Node (This is only applicable for IC segment and not for Discrete and Optoelectronics Segments)

- < 3nm

- 3nm

- 5nm

- 7nm

- 16nm

- 28nm

- > 28nm

- By Business Model

- IDM

- Design/ Fabless Vendor

- By End-user Industry

- Automotive

- Communication (Wired and Wireless)

- Consumer

- Industrial

- Computing/Data Storage

- Government (Aerospace and Defense)

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interview device designers, foundry planners, OSAT engineers, and large OEM procurement leads across North America, Europe, and Asia. These conversations test preliminary growth drivers (for example, AI accelerator demand and EV penetration), refine average selling price (ASP) assumptions, and verify node-migration timelines gleaned from secondary work.

Desk Research

We begin by mapping the market universe through curated, public-domain datasets from tier-1 bodies such as WSTS, SEMI, the Semiconductor Industry Association, UN Comtrade trade codes, and patent analytics from Questel. Company 10-Ks, quarterly filings, and investor presentations anchor vendor-level revenue splits, which are then complemented with customs shipment logs from Volza and macro indicators from the World Bank. When critical gaps emerge, analysts tap paid repositories like D&B Hoovers for historical financials. This mix lets us gauge both demand signals and supply footprints. The sources cited above are illustrative; dozens of additional publications assist validation and clarification.

Market-Sizing & Forecasting

A top-down construct starts with regional WSTS sales, which are disaggregated by device class, rebuilt into units via sampled ASPs, and then re-stacked by end-use application. Select bottom-up cross-checks, such as wafer starts per month roll-ups, smartphone and light-vehicle production, and 300 mm fab capacity utilization, allow us to reconcile totals and adjust for inventory swings. Key variables feeding the model include quarterly ASP trends, silicon-wafer shipments, technology-node mix shifts, memory price cycles, and OEM unit outlooks. Five-year forecasts apply multivariate regression with lagged GDP and electronics IP set indicators, before scenario analysis tweaks the base case for swing factors like trade controls.

Data Validation & Update Cycle

Outputs pass three analyst reviews: variance checks versus historical ratios, anomaly scrubs against fresh shipment data, and a reconciliation meeting with the lead modeller. We refresh every twelve months and trigger interim updates when supply chain shocks, policy moves, or price inflections materially alter the baseline.

Why Our Semiconductor Industry Size & Share Analysis Baseline Commands Reliability

Published numbers differ because firms choose distinct scopes, device baskets, currency conversions, and refresh cadences.

We focus on pure device revenue in 2025 so decision-makers can benchmark apples to apples.

Key gap drivers generally stem from whether foundry service revenue is rolled in, how aggressively future ASP erosion is baked, and the frequency with which forecasts are recalibrated when inventory sentiment flips.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 702.44 B | Mordor Intelligence | - |

| USD 755.28 B | Global Consultancy A | Includes foundry service fees and applies higher ASP uplift |

| USD 627.76 B | Industry Association B | Excludes sensors and applies conservative smartphone unit outlook |

In short, Mordor analysts balance device-only scope, timely ASP tracking, and annual model refreshes, giving clients a transparent, repeatable baseline rooted in clearly traceable variables.

Key Questions Answered in the Report

What is the current size of the semiconductor market and its growth outlook?

The semiconductor market generated USD 702.44 billion in 2025 and is set to reach USD 950.97 billion by 2030, reflecting a 6.25% CAGR.

Which region will drive most semiconductor market growth through 2030?

Asia-Pacific remains the growth anchor, sustaining 81.3% revenue in 2024 and advancing at a 6.9% regional CAGR during 2025-2030.

How fast is 3 nm technology expected to grow?

Revenue from 3 nm wafers is forecast to expand at an 8.7% CAGR through 2030, outpacing all other node categories.

Why are chiplet and heterogeneous-integration strategies gaining traction?

Chiplets cut development cost 40–60%, shorten time-to-market up to 50%, and enable specialized IP reuse across vendors, driving broad ecosystem adoption.

What impact will on-shoring incentives have on supply-chain risk?

Subsidy-backed capacity additions in the United States, Europe, and India diversify geographic production hubs, thereby mitigating single-region disruption risk over the medium term.

Which end-user vertical shows the fastest semiconductor demand growth?

Government aerospace and defense applications are projected to post a 7.36% CAGR to 2030 as nations prioritize a secure, domestic semiconductor supply.

Page last updated on: