| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 7.67 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Semiconductor Foundry Market Analysis

The Semiconductor Foundry Market is expected to register a CAGR of 7.67% during the forecast period.

The semiconductor foundry market landscape is experiencing significant transformation through unprecedented government support and cross-border collaborations. Governments worldwide are implementing strategic initiatives to strengthen domestic semiconductor manufacturing capabilities while fostering international partnerships. The United States has been particularly active, with the implementation of the CHIPS Act providing USD 52 billion in federal investments to boost domestic semiconductor production, research, development, and production. This has catalyzed major investments from global players, exemplified by TSMC's December 2023 announcement to construct a USD 12 billion factory in Arizona for manufacturing 3nm chips, with Apple and NVIDIA slated as the inaugural customers.

The industry is witnessing a substantial shift in manufacturing capabilities and technological advancement. According to recent industry data, the number of new semiconductor manufacturing facilities starting construction has shown remarkable growth, with 33 new facilities beginning construction in 2022, followed by 28 facilities in 2023. This expansion in manufacturing infrastructure is accompanied by significant technological breakthroughs, particularly in advanced node development. In June 2023, Samsung Electronics achieved a milestone by initiating the production of a 3nm process node applying Gate-All-Around (GAA) transistor architecture, promising substantial improvements in power consumption and performance.

Strategic partnerships and supply chain reorganization are reshaping the industry's competitive landscape. Major foundries are establishing collaborative agreements with technology companies and automotive manufacturers to ensure stable supply chains and meet growing demand across sectors. In January 2023, ZF Friedrichshafen and Wolfspeed announced plans for constructing a USD 3 billion wafer manufacturing facility in Germany, specifically targeting electrical automobile applications. This trend of strategic partnerships is complemented by a broader industry movement toward supply chain transparency, with governments encouraging information sharing among key players to prevent future disruptions.

The industry's trajectory is increasingly influenced by emerging applications and technological convergence. According to Ericsson's latest projections, cellular IoT connections are expected to grow from 1.9 billion in 2022 to 5.5 billion by 2027, representing a CAGR of 19%. This explosive growth in connected devices is driving demand for specialized semiconductor solutions across various applications. The industry is responding through capacity expansion and technological innovation, with major foundries investing in advanced manufacturing processes to support next-generation applications in artificial intelligence, high-performance computing, and automotive electronics. The semiconductor manufacturing industry is thus poised to play a pivotal role in the future of technology.

Semiconductor Foundry Market Trends

Optimization of Semiconductor Processes Through Analytics

Advanced analytics has become a crucial driver in optimizing semiconductor manufacturing processes, with foundries generating massive volumes of data during chip production. The volume of data generated on fab floors expands exponentially with each new node dimension, as leading-edge tools consist of various measuring instruments that routinely identify and gather over 300 sensor inputs. This data explosion has enabled manufacturers to implement sophisticated analytics tools for real-time monitoring, fault detection, and process optimization, significantly improving yield rates and operational efficiency. Companies like TSMC have developed smart diagnosis engines and advanced analytics platforms that have helped maintain reduced cycle times and optimized lead times, with some reporting up to a 50% improvement in cycle times after adopting smart manufacturing practices.

The integration of artificial intelligence and machine learning with manufacturing analytics has revolutionized how foundries approach process control and quality management. Major foundries are increasingly adopting machine learning (ML), automation, and analytics to optimize production processes without compromising quality. For instance, in December 2021, Merck KGaA partnered with Palantir Technologies to launch the Athinia platform, which uses artificial intelligence and big data to address critical issues including chip shortages and supply chain transparency. Similarly, companies like Accenture have introduced specialized analytics solutions for the semiconductor manufacturing industry, with their Semiconductor Manufacturing Analytics solution claiming to reduce machine downtime by 50% while offering a 5% to 15% improvement in manufacturing output through machine and deep learning techniques.

Understand The Key Trends Shaping This Market

Download PDF

Automotive, IoT, and AI Sectors

The explosive growth in connected devices, artificial intelligence applications, and automotive electronics has emerged as a major driver for the semiconductor foundry market. According to Cisco Systems, the number of connected wearable devices in North America reached 439 million in 2022, up from 378.8 million in 2021, demonstrating the rapidly expanding IoT ecosystem. This surge in connected devices has created unprecedented demand for specialized semiconductor solutions, particularly in areas like sensors, connectivity chips, and integrated circuits. The automotive industry's transition toward electric and autonomous vehicles has further accelerated this demand, with modern vehicles requiring sophisticated semiconductor components for features such as blind-spot detection, backup cameras, and essential connectivity features.

The advancement in artificial intelligence and high-performance computing applications has pushed foundries to develop more sophisticated manufacturing processes. This is evidenced by recent developments such as Apple's announcement in January 2023 to develop its new MacBook Air and iMac with the Apple M3 processor, built on a 3-nanometer process. In response to these demands, major foundries are making substantial investments in advanced manufacturing capabilities. For instance, TSMC's decision to produce 3-nanometer chips at its Arizona factory by 2024 demonstrates the industry's commitment to meeting the growing demands of AI and high-performance computing applications. Intel's investment of more than USD 20 billion in creating two new cutting-edge chip facilities in Ohio, announced in January 2022, further underscores the industry's response to the increasing demands from these sectors. The wafer fabrication advancements in these facilities highlight the critical role of the semiconductor foundry industry in supporting technological innovation.

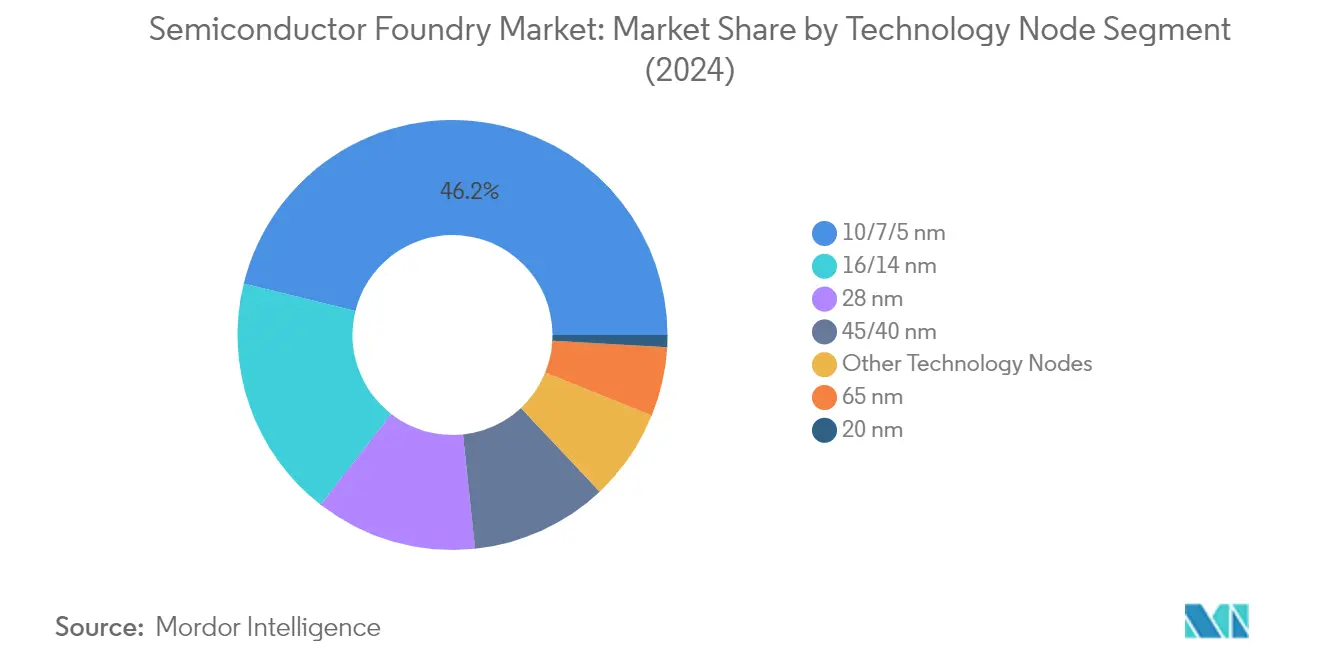

Segment Analysis: By Technology Node

10/7/5 nm Segment in Semiconductor Foundry Market

The 10/7/5 nm segment dominates the semiconductor foundry market, commanding approximately 46% market share in 2024. This segment's prominence is driven by its widespread adoption in cutting-edge applications, including 5G smartphones, high-performance computing, and artificial intelligence systems. Major foundries like TSMC and Samsung are heavily investing in these advanced nodes to meet the growing demand from companies such as Apple, Qualcomm, and NVIDIA. The technology's ability to deliver superior performance while maintaining power efficiency makes it particularly attractive for premium mobile processors and data center applications. The segment's leadership is further strengthened by increasing demand for artificial intelligence and machine learning applications, which require the high computational capabilities offered by these advanced nodes. The role of wafer foundry is crucial in this segment, providing the necessary infrastructure for advanced semiconductor manufacturing.

10/7/5 nm Segment Growth in Semiconductor Foundry Market

The 10/7/5 nm segment is projected to maintain its position as the fastest-growing segment in the semiconductor foundry market, with an expected growth rate of approximately 9% during 2024-2029. This exceptional growth is fueled by the increasing adoption of 5G technology, artificial intelligence applications, and high-performance computing solutions. Leading foundries are expanding their production capabilities and making substantial investments in research and development to enhance the performance and efficiency of these advanced nodes. The segment's growth is further supported by the rising demand for advanced mobile processors, automotive semiconductors, and data center applications. The continuous innovation in chip design and manufacturing processes, coupled with the increasing need for more powerful and energy-efficient computing solutions, is expected to drive sustained growth in this segment. The integration of logic foundry and IC foundry services is pivotal in supporting this growth trajectory.

Remaining Segments in Technology Node Market

The semiconductor foundry market encompasses several other important technology nodes, including 16/14 nm, 20 nm, 28 nm, 45/40 nm, and 65 nm, each serving specific market needs and applications. The 16/14 nm node remains crucial for mainstream mobile and computing applications, while the 28 nm node continues to be significant for automotive and industrial applications. The 45/40 nm and 65 nm nodes maintain their relevance in various consumer electronics and IoT devices, offering cost-effective solutions for less demanding applications. The mature nodes benefit from well-established manufacturing processes and lower production costs, making them particularly attractive for applications where cutting-edge performance is not critical. These segments collectively provide a comprehensive range of solutions catering to diverse market requirements across different industries and applications. The role of memory foundry and specialty foundry is significant in these segments, offering tailored solutions for specific industry needs.

Segment Analysis: By Application

Consumer Electronics and Communication Segment in Semiconductor Foundry Market

The Consumer Electronics and Communication segment continues to dominate the semiconductor foundry market, commanding approximately 48% market share in 2024. This segment's prominence is driven by the increasing adoption of consumer electronics devices like smartphones, laptops, earphones, and wearables, as well as the rapid deployment of 5G technology. The growth in this segment is further supported by major technological advancements, with companies like Apple developing next-generation processors built on advanced nanometer processes. The deployment of 5G has significantly enhanced wireless data communication bandwidth, latency, and the density of connected devices, creating substantial demand for semiconductor foundry services. Additionally, the segment's growth is bolstered by the rising internet penetration, proliferation of smart devices, and increasing consumer disposable income, particularly in emerging economies. The role of advanced foundry services is crucial in meeting the sophisticated demands of this segment.

Automotive Segment in Semiconductor Foundry Market

The Automotive segment is emerging as the fastest-growing segment in the semiconductor foundry market, with a projected growth rate of approximately 9% during 2024-2029. This remarkable growth is primarily attributed to the increasing integration of advanced electronics in modern vehicles, particularly in electric and autonomous vehicles. The automotive industry's transition toward electric mobility and the integration of Advanced Driver Assistance Systems (ADAS) is creating unprecedented demand for semiconductor components. Major automotive manufacturers are increasingly focusing on developing their semiconductor capabilities, with companies establishing strategic partnerships with foundries to ensure a stable chip supply. The segment's growth is further accelerated by the rising demand for features such as blind-spot detection, backup cameras, and essential connectivity features in vehicles.

Remaining Segments in Semiconductor Foundry Market by Application

The remaining segments in the semiconductor foundry market include High-Performance Computing (HPC), Industrial, and Other Applications, each serving distinct market needs. The HPC segment is particularly significant, driven by the growing adoption of AI, ML, and data analytics across various industries. The Industrial segment is benefiting from the increasing adoption of the Industrial Internet of Things (IIoT) and Industry 4.0 initiatives, which require advanced semiconductor solutions for automation and connectivity. Other applications encompass diverse sectors such as medical devices, aerospace, and IT infrastructure, contributing to the market's overall diversity. These segments collectively demonstrate the widespread application of semiconductor foundry services across multiple industries, highlighting the market's broad impact on technological advancement.

Semiconductor Foundry Market Geography Segment Analysis

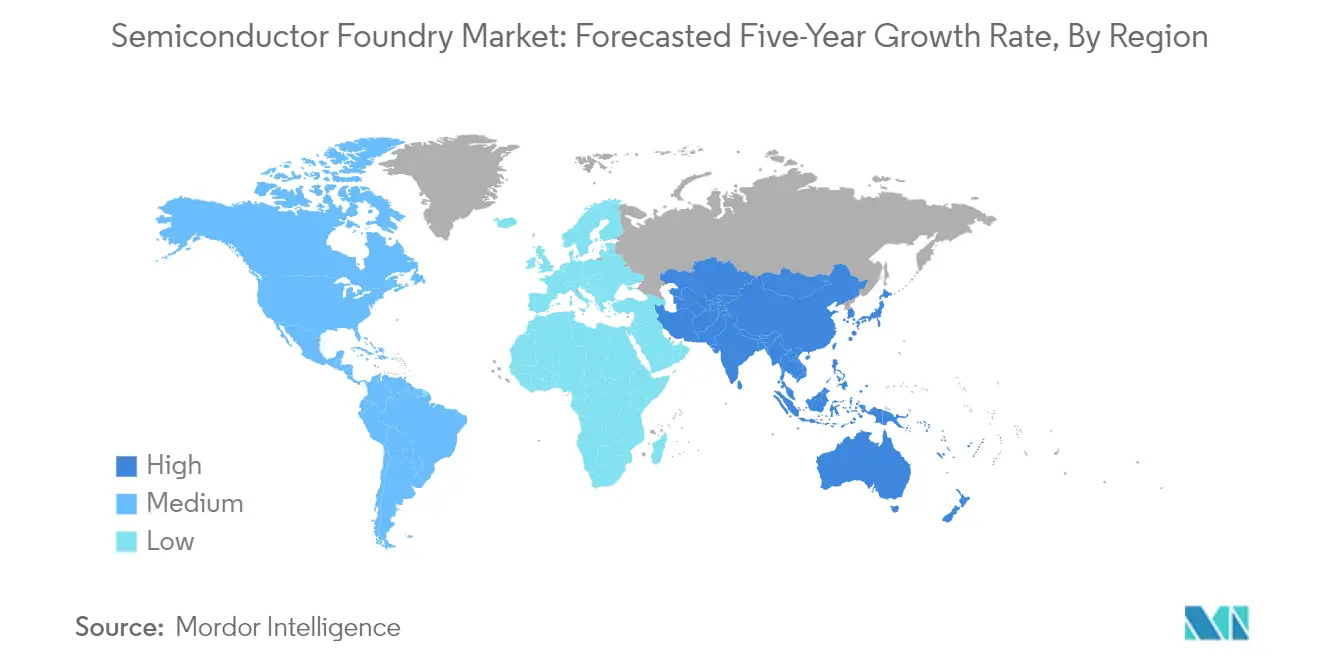

Semiconductor Foundry Market in North America

North America represents the largest market for semiconductor fabs and semiconductor fabrication globally, commanding approximately 58% of the global market share in 2024. The region's dominance is primarily driven by substantial government initiatives and private sector investments in domestic semiconductor manufacturing capabilities. The United States leads the regional market with its robust technological infrastructure and the presence of major semiconductor companies. The region's strength lies in its advanced research capabilities, skilled workforce, and strong intellectual property protection framework. The market is characterized by increasing investments in cutting-edge manufacturing facilities, particularly focusing on advanced nodes for applications in artificial intelligence, 5G technology, and high-performance computing. The presence of major technology companies and their growing demand for custom semiconductor solutions further strengthens the region's position. Additionally, the emphasis on reducing dependency on foreign semiconductor manufacturing and strengthening domestic supply chains continues to shape the market dynamics in North America.

Semiconductor Foundry Market in Europe, Middle East & Africa

The Europe, Middle East & Africa (EMEA) region has demonstrated steady growth in the semiconductor foundry market, with an approximate growth rate of 6% during 2019-2024. The region's semiconductor ecosystem is characterized by a strong focus on automotive, industrial, and power electronics applications. European countries are actively developing their semiconductor manufacturing capabilities through various initiatives and partnerships with global players. The region's strength lies in its robust automotive industry, which drives significant demand for specialized semiconductor solutions. The market is witnessing increased investments in research and development, particularly in areas such as power semiconductors and compound semiconductors. The Middle East is emerging as a potential hub for semiconductor manufacturing, with several countries showing interest in developing domestic capabilities. The African semiconductor market, while relatively smaller, is gradually developing with an increasing focus on digital transformation and technological advancement.

Semiconductor Foundry Market in Asia-Pacific

The Asia-Pacific semiconductor foundry market is poised for robust expansion, with a projected growth rate of approximately 8% during 2024-2029. The region represents a critical hub in the global semiconductor supply chain, with countries like Taiwan, South Korea, and Japan leading in advanced manufacturing capabilities. China's aggressive expansion in semiconductor manufacturing capabilities is reshaping the regional market dynamics. The region benefits from a well-established ecosystem of suppliers, manufacturers, and research institutions. The market is characterized by significant investments in advanced manufacturing facilities and continuous technological innovations. The presence of major foundries and their ongoing capacity expansions strengthens the region's position in the global semiconductor supply chain. The market is driven by growing demand from various sectors, including consumer electronics, automotive, and industrial applications. Additionally, the region's competitive advantage in terms of manufacturing costs and technical expertise continues to attract global semiconductor companies seeking foundry services.

Get Analysis on Important Geographic Markets

Download PDF

Semiconductor Foundry Industry Overview

Top Companies in Semiconductor Foundry Market

The semiconductor foundry market is dominated by major players, including TSMC, Samsung Electronics, GlobalFoundries, UMC, and SMIC. These semiconductor foundry companies are heavily investing in advanced manufacturing processes and innovative technologies such as extreme ultraviolet lithography (EUV) and advanced packaging solutions. The industry is witnessing significant expansion through new fabrication facilities across multiple geographies, particularly in response to growing demand and supply chain diversification needs. Companies are forming strategic partnerships with technology firms and automotive manufacturers while also focusing on specialized process nodes for different applications. Operational agility is being enhanced through analytics-driven manufacturing optimization, automation, and smart factory initiatives. The leading players are also making substantial investments in research and development to maintain technological leadership in areas such as 3nm and 2nm process nodes, silicon photonics, and advanced packaging technologies.

High Barriers Drive Market Consolidation Trends

The semiconductor foundry market exhibits a highly consolidated structure dominated by a few global players, particularly in advanced process nodes. The industry's high capital intensity and technological complexity create significant barriers to entry, with new fab construction requiring massive investments and extensive technical expertise. Market consolidation is further driven by the need for economies of scale and the increasing costs of research and development in advanced manufacturing processes. The industry has witnessed strategic mergers and acquisitions aimed at expanding technological capabilities and geographic presence, with established players acquiring smaller specialized foundries to enhance their service offerings.

The market is characterized by a mix of pure-play foundries and integrated device manufacturers (IDMs) offering foundry services. While pure-play foundries like TSMC and GlobalFoundries focus exclusively on manufacturing for other companies, IDMs like Samsung and Intel are expanding their foundry services to leverage their manufacturing expertise and capacity. Regional players are increasingly focusing on specialized process nodes and applications, creating a tiered market structure where different players serve distinct market segments based on technological capabilities and customer requirements.

Innovation and Specialization Drive Future Success

Success in the semiconductor manufacturing industry increasingly depends on technological leadership and specialized manufacturing capabilities. Incumbent players must continue investing in cutting-edge process technologies while also developing specialized solutions for emerging applications in automotive, IoT, and artificial intelligence. The ability to offer comprehensive design enablement platforms, intellectual property portfolios, and advanced packaging solutions is becoming crucial for maintaining market position. Companies must also focus on sustainability initiatives and energy-efficient manufacturing processes to meet evolving customer and regulatory requirements.

For contenders looking to gain market share, focusing on specialized market segments and developing expertise in specific applications or process nodes offers a viable strategy. Building strong relationships with key customers through long-term agreements and collaborative development programs helps ensure stable demand and revenue streams. Geographic diversification and government support through initiatives like the CHIPS Act provide opportunities for expansion and market entry. The industry's future success will also depend on managing supply chain risks, developing workforce capabilities, and maintaining flexibility to adapt to rapidly evolving technology requirements and market demands.

Semiconductor Foundry Market Leaders

-

Taiwan Semiconductor Manufacturing Company (TSMC) Limited

-

Globalfoundries Inc.

-

United Microelectronics Corporation (UMC)

-

Semiconductor Manufacturing International Corporation

-

Samsung Electronics Co. Ltd (Samsung Foundry)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Semiconductor Foundry Market News

- December 2022 - EPC and Vanguard International Semiconductor Corporation (VIS) announced a multi-year production agreement for gallium nitride-based power semiconductors in December 2022. EPC will take advantage of VIS' 8-inch (200 mm) wafer fabrication capabilities, which is expected to significantly increase manufacturing capacity for EPC's high-performance GaN transistors and integrated circuits. Production will begin in early 2023.

- November 2022 - Hua Hong Semiconductor Ltd received regulatory approval for a USD 2.5 billion IPO in Shanghai. The planned initial public offering (IPO) comes as China's chip companies gear up for steeper competition with the United States due to geopolitical tensions. Due to this, Hua Hong intends to use the money to invest in a new fabrication plant - or fab - in the eastern city of Wuxi, with construction set to begin in 2023 and an eventual production capacity of 83,000 wafers per month.

Semiconductor Foundry Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Foundry Capacity Utilization Trends

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Optimization of Semiconductor Processes through Analytics

- 5.1.2 Automotive, IoT, and AI Sectors are Driving the Market

-

5.2 Market Challenges

- 5.2.1 Moores Law is about Reaching its Physical Limitation

- 5.3 Major Industry Partnerships

- 5.4 Foundry Trends Related to Semiconductor Products

6. MARKET SEGMENTATION

-

6.1 By Technology Node

- 6.1.1 10/7/5 nm

- 6.1.2 16/14 nm

- 6.1.3 20 nm

- 6.1.4 28 nm

- 6.1.5 45/40 nm

- 6.1.6 65 nm

- 6.1.7 Other Technology Nodes

-

6.2 By Application

- 6.2.1 Consumer Electronics and Communication

- 6.2.2 Automotive

- 6.2.3 Industrial

- 6.2.4 HPC

- 6.2.5 Other Applications

-

6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe, Middle East and Africa

- 6.3.3 Asia Pacific

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 TSMC Limited

- 7.1.2 Globalfoundries Inc.

- 7.1.3 United Microelectronics Corporation (UMC)

- 7.1.4 Semiconductor Manufacturing International Corporation (SMIC)

- 7.1.5 Samsung Electronics Co. Ltd (Samsung Foundry)

- 7.1.6 Dongbu Hitek Co. Ltd

- 7.1.7 Intel Corporation

- 7.1.8 Hua Hong Semiconductor Limited

- 7.1.9 Powerchip Technology Corporation

- 7.1.10 STMicroelectronics NV

- 7.1.11 Tower Semiconductor Ltd.

- 7.1.12 Vanguard International Semiconductor Corporation

- 7.1.13 X-FAB Silicon Foundries

- 7.1.14 NXP Semiconductors NV

- 7.1.15 Renesas Electronics Corporation

- 7.1.16 Microchip Technologies Inc.

- 7.1.17 Texas Instruments Inc.

8. OVERALL SEMICONDUCTOR (O-S-D AND IC) SALES BY IDMS DURING THE STUDY PERIOD AND KEY TRENDS AND DYNAMICS INFLUENCING THE GROWTH

9. FOUNDRY SALES BY IDMS DURING THE STUDY PERIOD

10. VENDOR MARKET SHARES BY TOP 5 IDMS BASED ON SEMICONDUCTOR SALES AND AN INDICATION OF THE PERCENTAGE SHARES BY CATEGORY (O-S-D VS IC) DURING THE STUDY PERIOD

11. VENDOR MARKET SHARE ANALYSIS - PUREPLAY COMPANIES

12. INVESTMENT ANALYSIS

13. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Semiconductor Foundry Industry Segmentation

A semiconductor foundry, also called a fab and fabrication plant, refers to a factory where devices, like integrated circuits (ICs), are manufactured. Both pure-play foundries (foundries that do not offer products of their own) and IDMs (players that design and produce their own products) are considered a part of the study.

The study tracks the revenue accrued from the semiconductor foundries used across applications. Also, the revenue accrued from the semiconductor foundry vendors has been considered along with the COVID-19 impact on market projection.

The Semiconductor Foundry Market is segmented by Technology Node (10/7/5 nm, 16/14 nm, 20 nm, 28 nm, 45/40 nm, 65 nm, and other technology nodes), by Application (Consumer Electronics and communication, Automotive, Industrial, HPC, and other applications), and by Geography (North America, Europe, Middle East & Africa, and Asia Pacific). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Technology Node | 10/7/5 nm |

| 16/14 nm | |

| 20 nm | |

| 28 nm | |

| 45/40 nm | |

| 65 nm | |

| Other Technology Nodes | |

| By Application | Consumer Electronics and Communication |

| Automotive | |

| Industrial | |

| HPC | |

| Other Applications | |

| By Geography | North America |

| Europe, Middle East and Africa | |

| Asia Pacific |

Need A Different Region or Segment?

Customize Now

Semiconductor Foundry Market Research FAQs

What is the current Semiconductor Foundry Market size?

The Semiconductor Foundry Market is projected to register a CAGR of 7.67% during the forecast period (2025-2030)

Who are the key players in Semiconductor Foundry Market?

Taiwan Semiconductor Manufacturing Company (TSMC) Limited, Globalfoundries Inc., United Microelectronics Corporation (UMC), Semiconductor Manufacturing International Corporation and Samsung Electronics Co. Ltd (Samsung Foundry) are the major companies operating in the Semiconductor Foundry Market.

Which is the fastest growing region in Semiconductor Foundry Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Semiconductor Foundry Market?

In 2025, the North America accounts for the largest market share in Semiconductor Foundry Market.

What years does this Semiconductor Foundry Market cover?

The report covers the Semiconductor Foundry Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Semiconductor Foundry Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Semiconductor Foundry Market Research

Mordor Intelligence offers extensive expertise in analyzing the semiconductor foundry and semiconductor manufacturing industry. We provide comprehensive insights into global chip manufacturing and semiconductor production trends. Our research thoroughly examines the evolving landscape of wafer fabrication and foundry services. This includes a detailed analysis of leading semiconductor fabrication companies and their technological capabilities. The report covers various segments in depth, such as digital foundry, analog foundry, and specialty foundry operations. We pay particular attention to advanced foundry developments and IC foundry innovations.

Stakeholders across the semiconductor manufacturing value chain can access our detailed report PDF, available for download. It covers crucial aspects of wafer foundry operations and silicon foundry developments. The analysis encompasses key areas like logic foundry and memory foundry segments. We examine how semiconductor fab companies are adapting to market demands. Our comprehensive research delivers valuable insights into chip production trends, foundry services evolution, and the broader semiconductor fabrication landscape. This enables informed decision-making for industry participants, from semiconductor foundry companies to end-users.