Market Size of Semiconductor Equipment Industry

| Study Period | 2019 - 2029 |

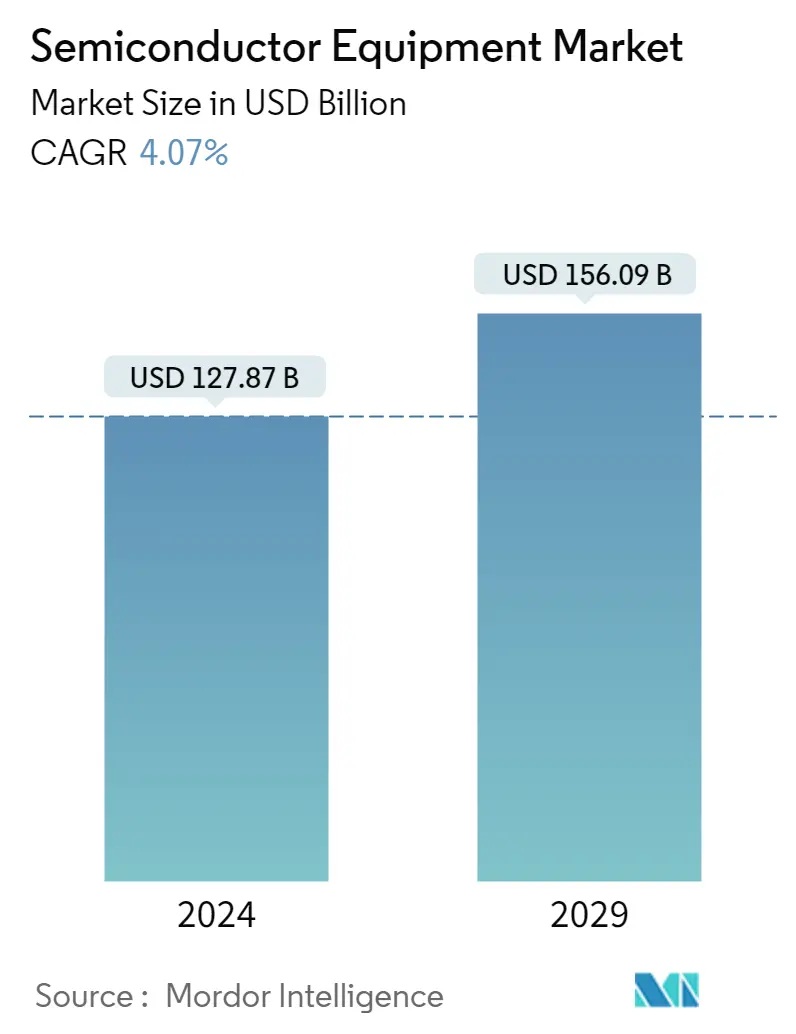

| Market Size (2024) | USD 127.87 Billion |

| Market Size (2029) | USD 156.09 Billion |

| CAGR (2024 - 2029) | 4.07 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Semiconductor Equipment Market Analysis

The Semiconductor Equipment Market size is estimated at USD 127.87 billion in 2024, and is expected to reach USD 156.09 billion by 2029, growing at a CAGR of 4.07% during the forecast period (2024-2029).

The global semiconductor industry is driven by the simultaneous growth of smartphones and other devices, such as advanced consumer electronics, and the growth of the automotive industry.

- These industries are driven by technology transitions such as wireless technologies (5G) and artificial intelligence. Several factors, including a steady rise in the demand for high-performance and low-cost semiconductors, drive the market with varying impacts over the short, medium, and long term.

- The deployment of 5G is expected to be one of the key factors driving the market. This is because the expansion of 5G would lead to the expansion of the wireless industry and enable innovations like augmented reality, mission-critical services, fixed wireless access, and the Internet of Things.

- Furthermore, with the gradual transitions in the semiconductor industry, such as the miniaturization of nodes and wafer sizes, the demand for increasing the wafer sizes for ultra-large-scale integration technologies has fostered the growth of semiconductor equipment. Moreover, fab manufacturers are shifting process monitors from bare wafers to production wafers due to the higher cost and inspection challenges faced by wafer miniaturization.

- The global demand for 300 mm silicon wafers is strong, and the demand for 200 mm has also seen a surge in recent years. According to SEMI, 200 mm fabs are gearing up to add over 600,000 wafers per month across the world during 2017-2022. Such trends are further expected to act as catalysts for the growth of the market studied.

- The COVID-19 pandemic disrupted the supply chains and production processes of semiconductors worldwide, especially in China, during the first half of 2020. The primary reason was a labor shortage, during which several semiconductor companies suspended operations. This created a crunch for end-product companies that depend on semiconductors.

Semiconductor Equipment Industry Segmentation

A semiconductor is an essential electronic equipment component, enabling advances in telecommunications, computing, biotechnology, weapon technology, aviation, renewable energy, and various other industries. Semiconductors, also known as integrated circuits (ICs) or microchips, are made from pure materials, such as silicon and germanium, and composite materials, such as gallium arsenide.

The scope of the study for the semiconductor equipment market is structured to track the spending on equipment types, i.e., front-end and back-end equipment. The market is further segmented into supply chain participants, i.e., IDM, OSAT, and foundry. The market is also segmented by geography. All the data presented in this study is as per recent information. All the market projections are adjusted to reflect the impact of COVID-19 on the semiconductor equipment market. The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| By Equipment Type | |||||||||

| |||||||||

|

| By Supply Chain Participants | |

| IDM | |

| OSAT | |

| Foundry |

| By Geography | ||||||

| North America | ||||||

| Europe | ||||||

| ||||||

| Rest of the World |

Semiconductor Equipment Market Size Summary

The semiconductor equipment market is poised for steady growth, driven by the expanding global demand for advanced consumer electronics and the automotive industry's technological advancements. The market's expansion is significantly influenced by the transition to wireless technologies like 5G and the integration of artificial intelligence, which are reshaping the landscape of consumer electronics and automotive applications. The demand for high-performance, cost-effective semiconductors is a key driver, with the deployment of 5G expected to catalyze further innovations in areas such as augmented reality and the Internet of Things. The industry's shift towards larger wafer sizes for ultra-large-scale integration technologies and the transition from bare to production wafers are also contributing to the market's growth trajectory.

The semiconductor equipment market is characterized by a high concentration of activity in a few key countries, with China, Taiwan, South Korea, and Japan playing pivotal roles. China's significant investment in mature semiconductor technologies and its government's focus on the semiconductor industry as a driver of economic growth are noteworthy. Taiwan's robust demand for chips in vehicles and high-performance computing is expected to make it a leading spender on front-end chip manufacturing equipment. South Korea's efforts to build a "K-Semiconductor belt" and its ambitious plans to double chip exports underscore the country's commitment to enhancing its global semiconductor industry presence. The competitive landscape is moderately intense, with major players like Applied Materials Inc., ASML Holding Semiconductor Company, and KLA Corporation leading the market. Recent developments, such as SCREEN Holdings' environmental initiatives and United Microelectronics Corporation's new facility in Singapore, highlight the industry's focus on sustainability and capacity expansion.

Semiconductor Equipment Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Intensity of Competitive Rivalry

-

1.2.5 Threat of Substitutes Products

-

-

1.3 Assessment of Impact of COVID-19 on the Industry

-

-

2. MARKET SEGMENTATION

-

2.1 By Equipment Type

-

2.1.1 Front-end Equipment

-

2.1.1.1 Lithography Equipment

-

2.1.1.2 Etch Equipment

-

2.1.1.3 Deposition Equipment

-

2.1.1.4 Metrology/Inspection Equipment

-

2.1.1.5 Material Removal/Cleaning Equipment

-

2.1.1.6 Photoresist Processing Equipment

-

2.1.1.7 Other Equipment Types

-

-

2.1.2 Back-end Equipment

-

2.1.2.1 Test Equipment

-

2.1.2.2 Assembly and Packaging Equipment

-

-

-

2.2 By Supply Chain Participants

-

2.2.1 IDM

-

2.2.2 OSAT

-

2.2.3 Foundry

-

-

2.3 By Geography

-

2.3.1 North America

-

2.3.2 Europe

-

2.3.3 Asia Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 Taiwan

-

2.3.3.4 Korea

-

-

2.3.4 Rest of the World

-

-

Semiconductor Equipment Market Size FAQs

How big is the Semiconductor Equipment Market?

The Semiconductor Equipment Market size is expected to reach USD 127.87 billion in 2024 and grow at a CAGR of 4.07% to reach USD 156.09 billion by 2029.

What is the current Semiconductor Equipment Market size?

In 2024, the Semiconductor Equipment Market size is expected to reach USD 127.87 billion.