| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 18.03 Billion |

| Market Size (2030) | USD 24.07 Billion |

| CAGR (2025 - 2030) | 5.95 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Semiconductor CVD Market Analysis

The Semiconductor CVD Equipment Market size is estimated at USD 18.03 billion in 2025, and is expected to reach USD 24.07 billion by 2030, at a CAGR of 5.95% during the forecast period (2025-2030).

The semiconductor industry is undergoing a profound transformation driven by technological advancements in chip manufacturing processes and increasing demand for advanced computing capabilities. The evolution of chip technology has reached new milestones, as demonstrated by IBM's breakthrough in 2nm chip technology, achieving 45% higher performance or 75% lower energy use compared to advanced 7nm node chips. This technological progression is reshaping the industry landscape, particularly in areas such as artificial intelligence, hybrid cloud computing, and Internet of Things applications, where the demand for more sophisticated and energy-efficient chips continues to grow exponentially.

The industry's manufacturing landscape is characterized by substantial capital requirements and complex infrastructure development. Setting up a new semiconductor foundry requires an investment ranging from USD 15 billion to USD 20 billion, while back-end assembly, packaging, and testing facilities demand between USD 5 billion to USD 7 billion. These significant capital requirements have led to increased collaboration between manufacturers, research institutions, and government entities to share resources and expertise. The industry's focus has shifted towards developing more efficient and cost-effective manufacturing processes while maintaining high-quality standards.

The global semiconductor ecosystem has witnessed significant developments in supply chain optimization and manufacturing capabilities. According to the Semiconductor Equipment and Materials International (SEMI), the industry achieved record-breaking equipment sales, reaching USD 103 billion, highlighting the robust investment in manufacturing infrastructure. This expansion in manufacturing capabilities is accompanied by innovations in semiconductor process equipment and wafer fabrication equipment, enabling the production of more complex and sophisticated semiconductor devices with enhanced performance characteristics.

The industry's commitment to research and development remains strong, with over 100 domestic and international semiconductor companies actively engaged in microchip research and development across various regions. These R&D initiatives focus on advancing semiconductor CVD equipment technologies for producing both inorganic thin films of 2D materials and high-purity polymeric thin films. The memory category in global semiconductor sales demonstrated particularly strong performance, with a 27.4% growth rate and total sales reaching USD 158 billion, indicating robust demand for advanced semiconductor solutions across various applications.

Semiconductor CVD Market Trends

Increase in Demand for Microelectronics and Semiconductor Devices

The semiconductor industry is experiencing unprecedented demand growth driven by the rapid evolution of technology across multiple sectors. Semiconductor deposition equipment, such as chemical vapor deposition (CVD), has emerged as the most widely adopted industrial technique for producing semiconducting thin films and complex layered micro- and nano-structures, essential for manufacturing high-quality and high-performance solid materials. The industry's transformation is evident in the continuous advancement of manufacturing processes, with companies pursuing node scaling beyond 10nm to 5nm and even 3nm, while simultaneously developing sophisticated three-dimensional structures for logic and memory applications. This technological progression is supported by the rising demand for semiconductors in critical applications, including artificial intelligence, hybrid cloud computing, and Internet of Things (IoT) devices, which require increasingly complex and efficient semiconductor components.

The expanding scope of semiconductor applications has created a robust ecosystem for CVD equipment manufacturers. Common semiconducting thin films produced through CVD processes include silicon carbide (SiC), gallium nitride (GaN), and gallium arsenide (GaAs), which are fundamental to developing next-generation electronic devices. The market is witnessing significant momentum in the development of power electronics, particularly in the automotive sector, where the transition to electric vehicles is driving demand for advanced semiconductor components. Additionally, the integration of semiconductors in healthcare devices, wearables, and 3D printing of medical devices is creating new avenues for CVD technology implementation. The industry's growth is further amplified by the increasing adoption of web-integrated wireless healthcare devices and the rising demand for high-performance computing applications that require sophisticated chip manufacturing processes.

Understand The Key Trends Shaping This Market

Download PDF

Rise in Application of the Technology for Several End-Users

Chemical vapor deposition technology has evolved to become a cornerstone in various industrial applications, extending far beyond traditional semiconductor manufacturing. The technology's versatility is demonstrated through its critical role in producing high-quality thin films for multiple end-user applications, including aerospace engine components, medical implants, solar cells, smart glass, carbon nanotubes, nanowires, LEDs, and MEMS devices. The growing demand for nanotechnology materials, including carbon nanotubes (CNTs), carbon nanofibers (CNFs), and silicon nanowires (Si-NWs), particularly in electric vehicle battery manufacturing, has created new opportunities for physical vapor deposition equipment manufacturers. These materials enable increased energy density and charge speed while contributing to reduced cost per kWh in battery applications.

The expansion of CVD applications is particularly evident in the development of advanced packaging solutions and emerging technologies. The technology has become instrumental in producing complex structures such as multi-layer stacks, nanowires/nanorods, and quantum dots, which are essential for next-generation electronic devices. The industry is witnessing increased adoption in research and development activities, with facilities like the Canadian Photonics Fabrication Centre (CPFC) utilizing metal-organic chemical vapor deposition (MOCVD) reactors for the research and fabrication of gallium arsenide (GaAs) and indium phosphide (InP)-based devices. Furthermore, the technology's application in producing high-performance thin films for optical data transmission and advanced power electronics demonstrates its crucial role in enabling future technological advancements across various industries, from telecommunications to renewable energy systems. The use of atomic layer deposition equipment is also gaining traction, particularly in the production of high-precision thin films required for these advanced applications.

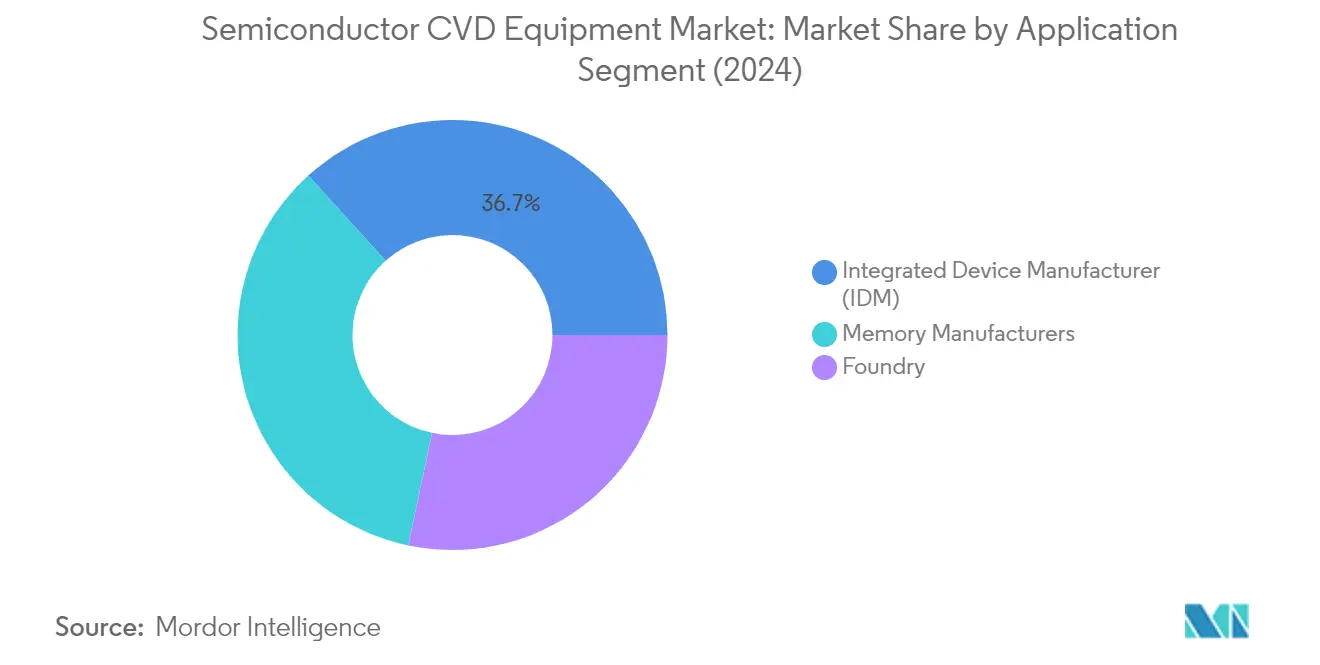

Segment Analysis: By Application

Integrated Device Manufacturer (IDM) Segment in Semiconductor CVD Equipment Market

The Integrated Device Manufacturer (IDM) segment holds the dominant position in the semiconductor process equipment market, accounting for approximately 37% market share in 2024. This segment encompasses the manufacturing of logic components, optoelectronics, sensors, and discrete components, excluding memory manufacturers. The segment's leadership is driven by the increasing demand for sophisticated three-dimensional structures for logic and advanced packaging applications. IDMs are actively pursuing node scaling beyond 10 nm to 5 nm and even 3 nm, while other manufacturers are moving away from planar architectures in favor of advanced 3D structures. The growth in this segment is particularly supported by the rising sales of microelectronics and consumer electronics, which has led to increased demand for semiconductor ICs and subsequently boosted the production capacity requirements of semiconductor device manufacturers.

Memory Manufacturers Segment in Semiconductor CVD Equipment Market

The Memory Manufacturers segment is emerging as the fastest-growing segment in the semiconductor deposition equipment market for the period 2024-2029. This remarkable growth is driven by the exponential increase in data consumption globally and the subsequent demand for memory products. The segment's growth is particularly fueled by the rising adoption of high-performance memory solutions in data centers, 5G smartphones, and artificial intelligence applications. Various vendors are expanding their memory businesses to meet the growing demand from consumer electronics and data centers. The advancement in plasma-enhanced chemical vapor deposition technologies and the development of new process technologies for memory manufacturing are further accelerating this segment's growth. The increasing focus on developing high-density memory solutions and the integration of advanced packaging technologies are also contributing factors to this segment's rapid expansion.

Remaining Segments in Application Market Segmentation

The Foundry segment plays a crucial role in the semiconductor CVD equipment market by focusing on the manufacturing of logic components, including microcontrollers and microprocessors. This segment has shown significant advancement in anti-wear cutting tool coating and microprocessor manufacturing processes. The segment's growth is supported by the increasing adoption of advanced packaging technologies and the rising demand for specialized semiconductor components. Foundries are particularly focusing on developing innovative solutions for emerging technologies such as artificial intelligence, edge computing, and 5G applications, while also advancing their capabilities in LPCVD equipment and rapid thermal processing technologies.

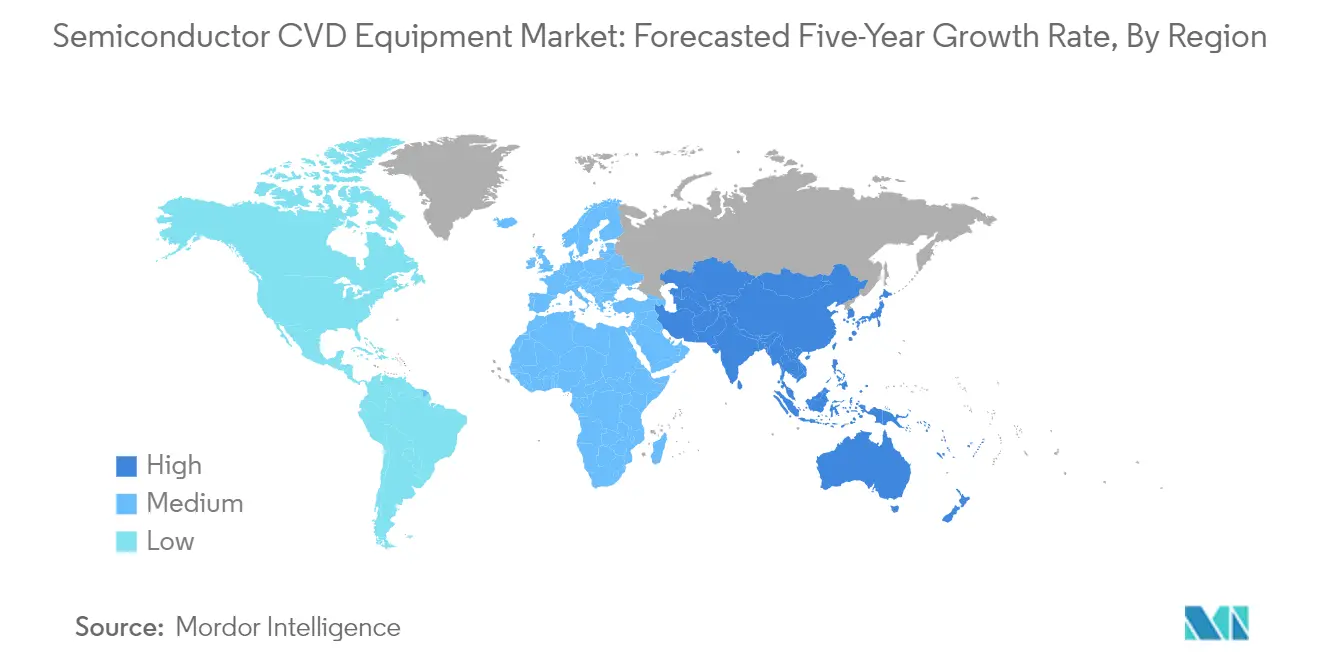

Semiconductor CVD Equipment Market Geography Segment Analysis

Semiconductor CVD Equipment Market in North America

The North American semiconductor CVD equipment market maintains a significant presence, holding approximately 11% of the global market share in 2024. The region's market is primarily driven by substantial investments in semiconductor manufacturing equipment and advanced research facilities. The United States continues to develop new strategies to strengthen its position in semiconductor manufacturing, particularly focusing on reducing dependence on Asian manufacturers. The region's market growth is supported by robust demand from various sectors, including automotive electronics, data centers, and advanced computing applications. The presence of major semiconductor companies and research institutions further strengthens the market ecosystem. Additionally, government initiatives to boost domestic semiconductor production capacity and technological innovation are creating favorable conditions for market expansion. The region's focus on developing cutting-edge technologies such as artificial intelligence, quantum computing, and advanced wireless networks is also contributing to increased demand for sophisticated semiconductor CVD equipment.

Semiconductor CVD Equipment Market in Europe

The European semiconductor CVD equipment market has demonstrated robust growth, achieving approximately an 18% annual growth rate from 2019 to 2024. The region's market is characterized by a strong presence of established semiconductor manufacturers and research institutions. European semiconductor manufacturers are increasingly focusing on developing advanced manufacturing capabilities for power electronics, automotive semiconductors, and specialized electronic components. The market benefits from substantial research and development activities in countries like Germany, France, and the Netherlands. The presence of major automotive manufacturers and their increasing demand for semiconductor components is driving market growth. Furthermore, the European Union's initiatives to enhance semiconductor manufacturing capabilities and reduce dependency on external suppliers are creating new opportunities. The region's strong focus on sustainable manufacturing practices and energy-efficient semiconductor production is also influencing the adoption of advanced semiconductor manufacturing equipment technologies.

Semiconductor CVD Equipment Market in Asia Pacific

The Asia Pacific region continues to dominate the global semiconductor CVD equipment market, with projections indicating approximately 9% growth annually from 2024 to 2029. The region serves as the global hub for semiconductor manufacturing, with countries like Taiwan, South Korea, Japan, and China leading the market. The market is characterized by extensive manufacturing capabilities, continuous technological advancements, and significant investments in production capacity expansion. The presence of major foundries and integrated device manufacturers (IDMs) drives the demand for advanced semiconductor manufacturing equipment. The region's strong electronics manufacturing ecosystem, coupled with growing domestic demand for semiconductor devices, creates a robust market environment. The increasing focus on developing advanced packaging technologies and compound semiconductors is further driving market growth. Additionally, government initiatives to boost domestic semiconductor capabilities and the rising adoption of advanced technologies across various industries continue to fuel market expansion.

Semiconductor CVD Equipment Market in Rest of World

The Rest of World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for semiconductor CVD equipment. These regions are witnessing growing interest in developing domestic semiconductor capabilities, particularly in countries with strong industrial bases. The market is driven by increasing investments in electronics manufacturing facilities and rising demand for consumer electronics. Government initiatives to attract semiconductor investments and develop local manufacturing capabilities are creating new opportunities. The automotive sector's growth in these regions, particularly in Latin America, is contributing to increased demand for semiconductor components. Additionally, the growing focus on digitalization and technological advancement in Middle Eastern countries is creating new avenues for market growth. The region's market is also benefiting from increasing investments in research and development facilities and the gradual development of the semiconductor ecosystem.

Get Analysis on Important Geographic Markets

Download PDF

Semiconductor CVD Industry Overview

Top Companies in Semiconductor Chemical Vapor Deposition Equipment Market

The semiconductor CVD equipment market features several established global players, including Applied Materials, Lam Research, ASM International, Tokyo Electron, AIXTRON, and Veeco Instruments. These companies are heavily focused on product innovation, particularly in developing advanced deposition technologies for next-generation semiconductors and specialized applications like power electronics and photonics. Operational agility is demonstrated through their emphasis on automated solutions and integrated process technologies that enable faster production cycles and improved yield management. Strategic initiatives commonly involve expanding manufacturing footprints in key semiconductor hubs and strengthening local presence through service networks. Companies are also pursuing collaborative partnerships with research institutions and semiconductor manufacturers to accelerate technology development and maintain competitive advantages. The market witnesses continuous investment in R&D facilities and demonstration centers to showcase new capabilities and support customer process development needs.

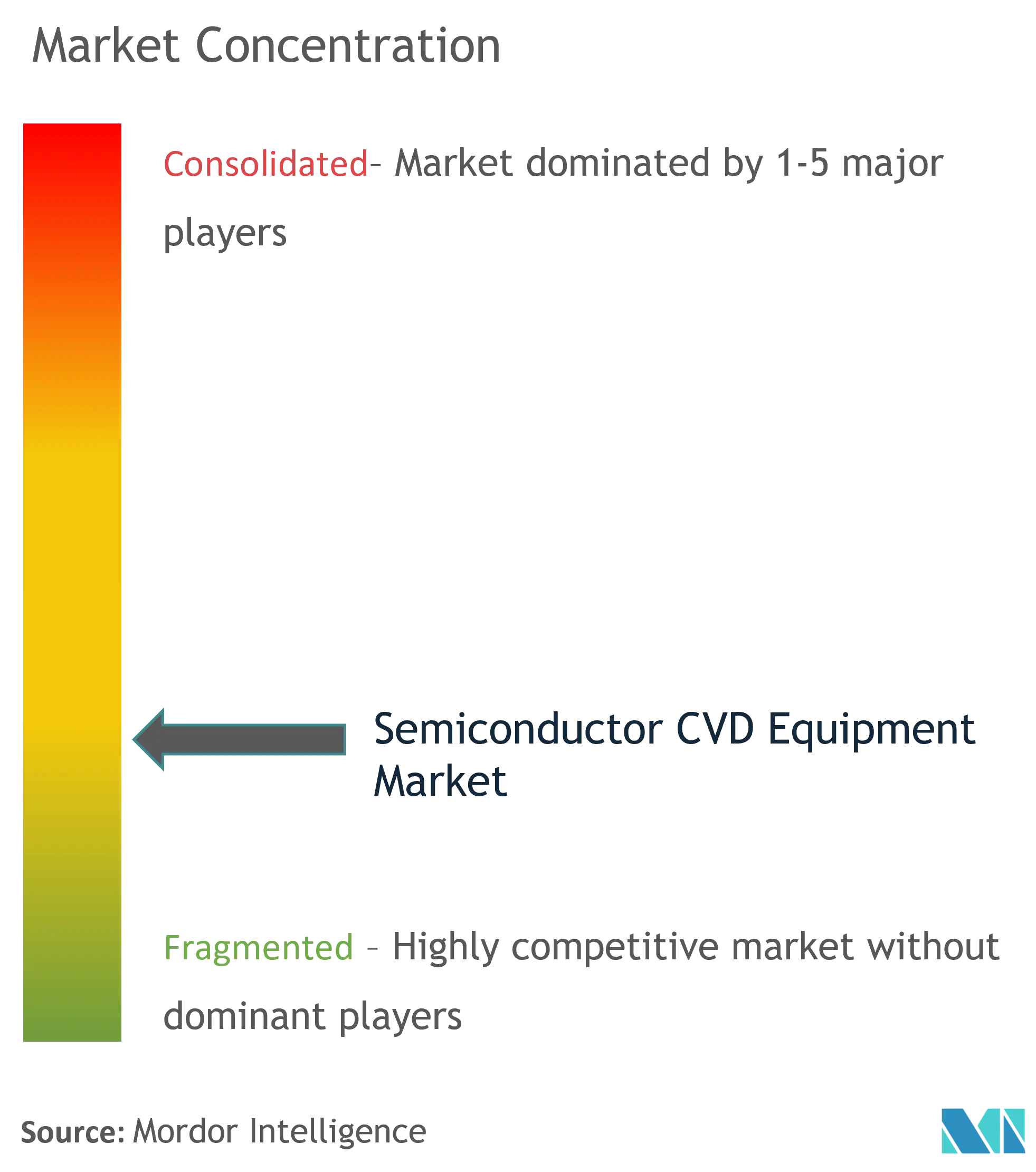

Global Leaders Dominate Consolidated Market Structure

The semiconductor manufacturing equipment market exhibits a highly consolidated structure dominated by large multinational corporations with comprehensive technology portfolios and an established global presence. These market leaders possess significant advantages through their extensive intellectual property holdings, long-standing customer relationships, and ability to provide integrated solutions across multiple process steps. The competitive landscape is characterized by high barriers to entry due to the complex nature of technology development, substantial capital requirements, and the need for extensive process expertise and customer support capabilities. Regional players typically focus on specific market niches or serve as suppliers to larger equipment manufacturers.

The market has witnessed strategic consolidation through mergers and acquisitions, primarily aimed at expanding technology capabilities and strengthening market presence in high-growth regions. Companies are particularly focused on acquiring specialized technology providers to enhance their offerings in emerging applications such as advanced packaging, compound semiconductors, and memory devices. The trend toward consolidation is further driven by the increasing complexity of semiconductor manufacturing processes and the need for comprehensive solution providers who can support multiple technology nodes and applications.

Innovation and Customer Relations Drive Success

Success in the semiconductor process equipment market increasingly depends on maintaining technological leadership while building strong customer relationships through comprehensive support services. Equipment manufacturers must continuously invest in developing new deposition technologies that address emerging challenges in semiconductor manufacturing, particularly for advanced nodes and novel device architectures. The ability to provide integrated solutions that optimize process performance, reduce operating costs, and improve yield is becoming increasingly critical. Companies must also maintain strong financial positions to support ongoing R&D investments and respond to cyclical market demands.

Market participants need to focus on developing flexible manufacturing capabilities and robust supply chains to address growing customer demands for customization and rapid delivery. Building strong partnerships with key semiconductor manufacturers and research institutions helps companies stay ahead of technology trends and maintain competitive positions. The regulatory environment, particularly regarding export controls and environmental regulations, continues to influence market dynamics and requires companies to maintain robust compliance programs. Success also depends on the ability to provide comprehensive training and technical support services to help customers optimize equipment performance and maximize return on investment.

Semiconductor CVD Market Leaders

-

AIXTRON SE

-

ASM International

-

CVD Equipment Corporation

-

Applied Materials, Inc

-

Oxford Instruments

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Semiconductor CVD Market News

- September 2021 - Lam Research announced the expansion of its manufacturing footprint in Oregon with a new 45,000 square foot facility in Sherwood. The new facility is Lam's fifth manufacturing site in the United States. It will further enhance its resilience and ability to meet increasing customer demand as chip suppliers seek to scale up production.

- February 2021 - Oxford Instruments Plasma Technology announced that it would relocate to a state-of-the-art manufacturing facility in Bristol, United Kingdom. Customers, who include the world's leading semiconductor device manufacturers and materials research organizations, are driving the migration. The new facility will feature 1,000m2 of ISO 5 and 6 class application laboratories with a full array of wafer processing options and advanced characterization/metrology technology.

Semiconductor CVD Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3. EXECUTIVE SUMMARY

4. MARKET INSIGHT

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Assessment of Impact of Covid-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increase In Demand For Microelectronics And Semiconductor Devices

- 5.1.2 Rise In Application Of The Technology For Several End-users

-

5.2 Market Restraint

- 5.2.1 High Investment For The Technology

-

5.3 Cvd Processes Technology Snapshot

- 5.3.1 Atmospheric-pressure Chemical Vapor Deposition (apcvd)

- 5.3.2 Density-plasma Chemical Vapor Deposition (dpcvd)

- 5.3.3 Low-pressure Chemical Vapor Deposition (lpcvd)

- 5.3.4 Metal-organic Chemical Vapor Phase Deposition (mocvd)

6. MARKET SEGMENTATION

-

6.1 By Application

- 6.1.1 Foundry

- 6.1.2 Integrated Device Manufacturer (idm)

- 6.1.3 Memory Manufacturers

-

6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Rest of The World

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Aixtron Se

- 7.1.2 Applied Materials, Inc.

- 7.1.3 Asm International

- 7.1.4 Cvd Equipment Corporation

- 7.1.5 Oxford Instruments Plc

- 7.1.6 Lam Research Corporation

- 7.1.7 Tokyo Electron Limited

- 7.1.8 Ulvac Inc.

- 7.1.9 Veeco Instruments Inc.

- *List Not Exhaustive

8. MARKET INVESTMENTS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Semiconductor CVD Industry Segmentation

Chemical vapor deposition (CVD) is a technique where a solid material is deposited from vapor by the chemical reaction occurring on or near a substrate surface. CVD Equipment facilitates the performance of the CVD technique in semiconductor manufacturing processes. The Semiconductor Chemical Vapor Deposition (CVD) Equipment Market is segmented by Application (Foundry, Integrated Device Manufacturer (IDM), Memory Manufacturers), and Geography. The scope of the study also incorporates the impact of covid-19 on the studied market.

| By Application | Foundry |

| Integrated Device Manufacturer (idm) | |

| Memory Manufacturers | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of The World |

Need A Different Region or Segment?

Customize Now

Semiconductor CVD Market Research FAQs

How big is the Semiconductor CVD Equipment Market?

The Semiconductor CVD Equipment Market size is expected to reach USD 18.03 billion in 2025 and grow at a CAGR of 5.95% to reach USD 24.07 billion by 2030.

What is the current Semiconductor CVD Equipment Market size?

In 2025, the Semiconductor CVD Equipment Market size is expected to reach USD 18.03 billion.

Who are the key players in Semiconductor CVD Equipment Market?

AIXTRON SE, ASM International, CVD Equipment Corporation, Applied Materials, Inc and Oxford Instruments are the major companies operating in the Semiconductor CVD Equipment Market.

Which is the fastest growing region in Semiconductor CVD Equipment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Semiconductor CVD Equipment Market?

In 2025, the Asia Pacific accounts for the largest market share in Semiconductor CVD Equipment Market.

What years does this Semiconductor CVD Equipment Market cover, and what was the market size in 2024?

In 2024, the Semiconductor CVD Equipment Market size was estimated at USD 16.96 billion. The report covers the Semiconductor CVD Equipment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Semiconductor CVD Equipment Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Semiconductor CVD Equipment Market Research

Mordor Intelligence provides a comprehensive analysis of the semiconductor CVD equipment industry. We leverage our extensive expertise in semiconductor manufacturing equipment research to offer valuable insights. Our detailed report examines the complete spectrum of semiconductor process equipment. This includes physical vapor deposition equipment and various deposition technologies. The analysis covers developments in wafer fabrication equipment, innovations in atomic layer deposition equipment, and advancements in thin film coating equipment technologies. These insights offer stakeholders crucial information on market dynamics and technological advancements.

Our in-depth research report is available as an easy-to-download PDF. It offers valuable insights into semiconductor deposition equipment trends, including a detailed analysis of PECVD equipment, MOCVD equipment, and LPCVD equipment technologies. The report examines key developments in semiconductor thin film deposition processes. It provides comprehensive coverage of the atomic layer deposition equipment market. Stakeholders across the wafer fabrication equipment market benefit from our detailed analysis of emerging technologies, competitive landscapes, and growth opportunities in the physical vapor deposition equipment market. This enables informed decision-making and strategic planning.