| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 568.96 Million |

| Market Size (2030) | USD 722.70 Million |

| CAGR (2025 - 2030) | 4.90 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Semiconductor Bonding Equipment Market Analysis

The Semiconductor Bonding Equipment Market size is estimated at USD 568.96 million in 2025, and is expected to reach USD 722.70 million by 2030, at a CAGR of 4.9% during the forecast period (2025-2030).

The semiconductor industry is experiencing unprecedented transformation, with semiconductors now ranking as the world's fourth most traded product globally, following only crude oil, refined oil, and cars, according to recent Wall Street Journal reports. This positioning reflects the critical role of semiconductors in enabling high-computing applications across diverse sectors, including electronics, manufacturing, healthcare, telecommunications, and space exploration. The industry's strategic importance has prompted governments worldwide to implement supportive policies and establish public-private partnerships, particularly in advancing 5G technology development and deployment.

The integration of advanced technologies is reshaping the semiconductor landscape, with IoT devices driving significant market evolution. According to Ericsson's latest projections, global cellular IoT connections are expected to surge to 5.5 billion by 2027, while the total number of connected devices worldwide is anticipated to reach approximately 28.72 billion by 2028. This explosive growth in connectivity is driving demand for more sophisticated semiconductor solutions, particularly in power management and high-performance computing applications.

Major industry developments are reshaping the competitive landscape, exemplified by significant investments and strategic initiatives announced in early 2024. In February 2024, Taiwan Semiconductor Manufacturing Company (TSMC) marked a milestone by inaugurating its first chip factory in Japan, while in March 2024, Intel secured a preliminary memorandum for up to $8.5 billion in direct funding from the US Department of Commerce. These developments highlight the industry's shift toward geographical diversification and enhanced production capabilities.

The industry is witnessing a surge in strategic investments aimed at advancing manufacturing capabilities and technological innovation. China's launch of a $40 billion semiconductor fund in September 2023 represents one of the most significant initiatives to boost domestic semiconductor capabilities. Additionally, new manufacturing facilities are being designed with unprecedented capacity, with some new fabs planning to achieve production capabilities of up to 50,000 wafers per month, demonstrating the industry's commitment to meeting growing global demand through expanded production capabilities.

Semiconductor Bonding Equipment Market Trends

Increasing Investment by Semiconductor Manufacturers to Expand Their Manufacturing Capacity

The semiconductor industry is witnessing unprecedented levels of investment as manufacturers aim to expand their production capabilities and meet growing global demand. In February 2024, the US Department of Commerce announced $1.5 billion in planned direct funding for GlobalFoundries as part of the U.S. CHIPS and Science Act, enabling the company to expand and create new manufacturing capacity for automotive, IoT, aerospace, and defense applications. This investment will facilitate the immediate expansion of existing facilities and the construction of a new 358,000-square-foot semiconductor manufacturing facility in Malta.

In January 2024, South Korea announced ambitious plans to invest approximately $470 billion over the next 20 years to develop an extensive semiconductor cluster in Gyeonggi Province. This initiative involves collaboration with industry leaders like Samsung Electronics and SK Hynix, with the government proposing measures including tax incentives and competitiveness-boosting initiatives. The project aims to improve self-sufficiency in essential materials, parts, and equipment for chip production to 50% by 2030, while establishing 13 new chip plants, three research facilities, and expanding 21 existing fabs.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Semiconductor Chips Across Various Applications

The semiconductor industry is experiencing robust growth driven by increasing demand across multiple sectors, particularly in automotive, consumer electronics, and computation applications. The integration of semiconductor components in automobiles continues to accelerate, especially with the rising adoption of electric and autonomous vehicles. These vehicles require sophisticated microcontrollers, sensors, and radar chips, creating sustained demand for semiconductor manufacturing equipment and semiconductor packaging equipment solutions. The automotive sector's transformation is particularly evident in the growing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies, which rely heavily on sophisticated semiconductor devices.

The consumer electronics sector is witnessing unprecedented demand for semiconductor chips, driven by the proliferation of smartphones, tablets, and wearable devices. According to Ericsson's projections, smartphone mobile network subscriptions worldwide reached almost 6.4 billion in 2022 and are forecasted to exceed 7.7 billion by 2028. This growth is complemented by the rapid advancement of 5G technology, with GSMA predicting that 5G connections will represent over half (51%) of mobile connections by 2029, rising to 56% by the end of the decade. These technological advancements and increasing consumer demand are creating sustained pressure for semiconductor manufacturers to enhance their production capabilities and advance their bonding equipment technologies.

Segment Analysis: By Type

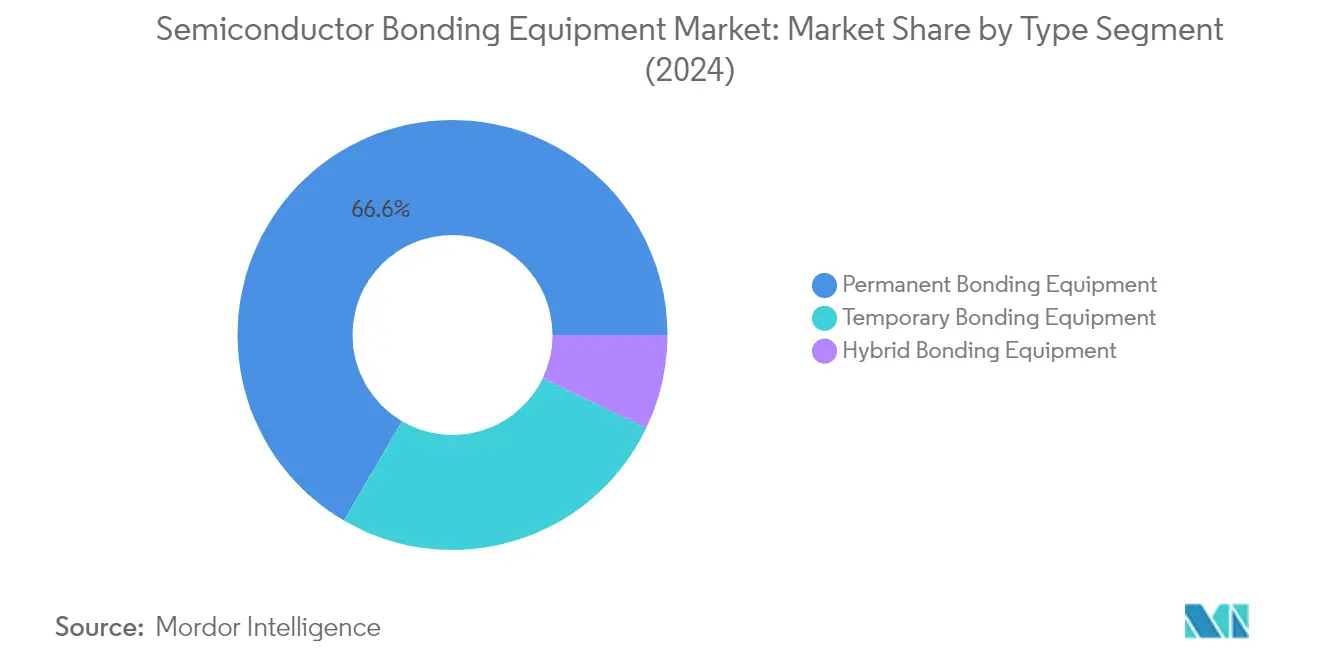

Permanent Bonding Equipment Segment in Semiconductor Bonding Equipment Market

The Permanent Bonding Equipment segment continues to dominate the semiconductor bonding equipment market, holding approximately 67% market share in 2024. This segment's prominence is driven by its crucial role in advanced packaging technologies, including 3D integration, wafer-level packaging, and system-in-package solutions. The increasing demand for permanent bonding equipment is primarily fueled by the need for improved device performance, reduced form factors, and enhanced functionality in semiconductor manufacturing. Major semiconductor manufacturers are increasingly adopting permanent bonding solutions for applications such as MEMS devices, CMOS image sensors, and power semiconductor devices, where secure electrical connections and efficient thermal regulation are essential.

Hybrid Bonding Equipment Segment in Semiconductor Bonding Equipment Market

The Hybrid Bonding Equipment segment is experiencing remarkable growth, projected to expand at approximately 14% CAGR from 2024 to 2029. This exceptional growth is driven by the increasing adoption of hybrid bonding technology in advanced semiconductor packaging, particularly in high-bandwidth memory stacking and chiplet-based CPUs. The segment's growth is further accelerated by major semiconductor manufacturers investing in hybrid bonding capabilities to enable precise and reliable bonding between dissimilar materials. The technology's advantages, including lower parasitic delay, high-density I/O, better thermal performance, and shorter height, make it particularly attractive for next-generation semiconductor devices and artificial intelligence applications. The integration of flip chip bonder and die bonding equipment technologies further enhances the capabilities of hybrid bonding solutions.

Remaining Segments in Semiconductor Bonding Equipment Market by Type

The Temporary Bonding Equipment segment plays a vital complementary role in the semiconductor bonding equipment market. This segment is essential for providing structural support during the processing of thin wafers, particularly in 3D IC manufacturing and fan-out wafer-level packaging applications. Temporary bonding solutions are crucial in handling delicate substrates like compound semiconductors and managing thin wafers during various processing steps. The segment's importance is particularly evident in applications requiring subsequent debonding processes, making it an integral part of advanced semiconductor manufacturing workflows. Additionally, the use of wafer bonding equipment is critical in ensuring the integrity and precision of these processes.

Segment Analysis: By Application

Power IC & Power Discrete Segment in Semiconductor Bonding Equipment Market

The Power IC and Power Discrete segment dominates the semiconductor bonding equipment market, commanding approximately 42% market share in 2024. This significant market position is driven by the rapid digitization of industries and the increasing number of connected devices that necessitate efficient power management and high-performance power semiconductor devices. The segment's growth is further fueled by the rising demand for high-energy and power-efficient devices, particularly in wireless and portable electronic products. The automotive industry's shift toward electrification has also contributed substantially to the segment's dominance, as power semiconductor devices are critical in facilitating efficient power management, conversion, and control across various applications. The industry has witnessed a rising inclination towards power modules and integrated solutions, with manufacturers creating compact, highly integrated modules that merge various power components like switches, diodes, and drivers to streamline system design and improve overall system efficiency.

Engineered Substrates Segment in Semiconductor Bonding Equipment Market

The Engineered Substrates segment is projected to exhibit the highest growth rate of approximately 10% during the forecast period 2024-2029. This remarkable growth trajectory is attributed to the increasing demand for compound-engineered substrate materials as the world seeks enhanced communication, sensing, and travel capabilities. Silicon carbide (SiC) is expected to gain a larger market share than silicon, especially in power applications, primarily driven by the electrification of vehicles and the need for high-voltage applications. Major industry players are actively working to secure or expand their substrate supply to meet this growing demand. The segment's growth is further supported by the introduction of various engineered substrates like Ga2O3, bulk GaN, diamond, and other materials that are paving the way for developing highly efficient devices and systems. The comprehensive bandgap materials will significantly benefit engineered substrates and bulk GaN in the coming years, with established players partnering to advance various engineered substrates. The integration of thermal compression bonding equipment and thermocompression bonding equipment is crucial in enhancing the performance of these substrates.

Remaining Segments in Semiconductor Bonding Equipment Market by Application

The market's other significant segments include Advanced Packaging, Photonic Devices, MEMS Sensors and Actuators, RF Devices, and CMOS Image Sensors, each serving crucial roles in different applications. Advanced Packaging continues to evolve with the increasing demand for 3D integration and heterogeneous integration. Photonic Devices are gaining importance in telecommunications and data transfer applications. MEMS Sensors and Actuators are crucial in automotive, medical, and industrial applications. RF Devices play a vital role in wireless infrastructure and communication systems. CMOS Image Sensors are becoming increasingly important in smartphone cameras, automotive cameras, and various imaging applications. These segments collectively contribute to the market's diverse application landscape, driven by technological advancements and increasing demand across various industries.

Semiconductor Bonding Equipment Market Geography Segment Analysis

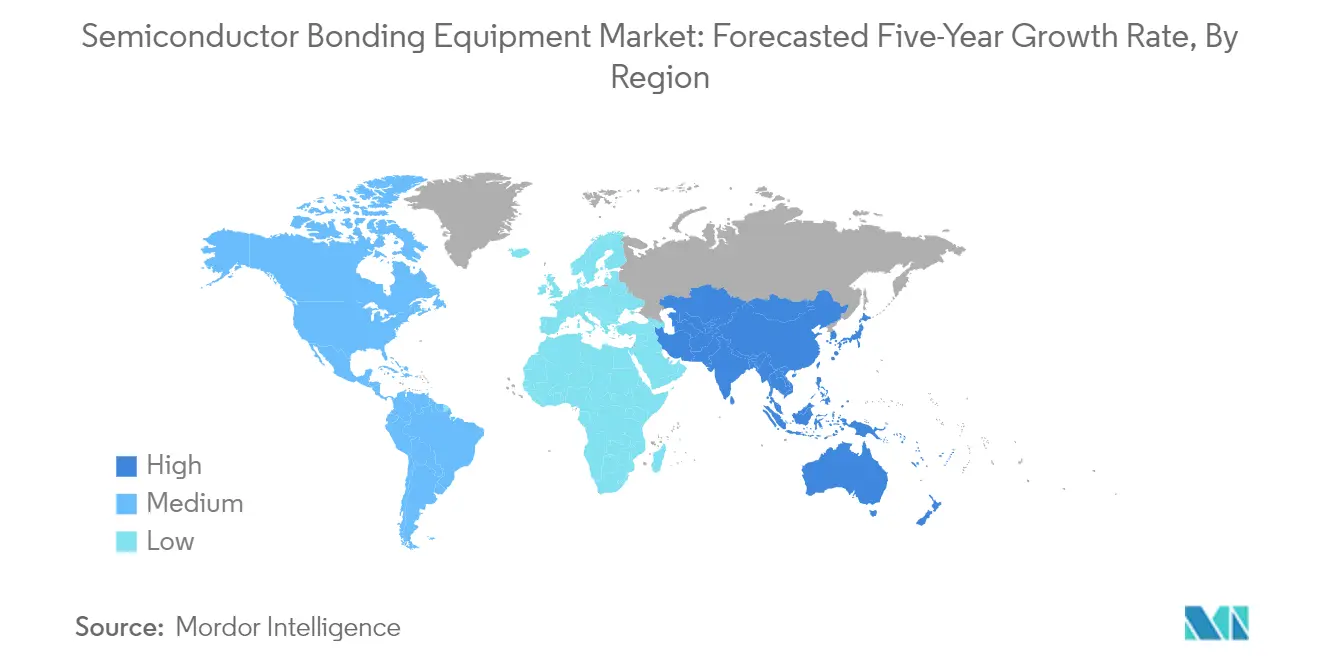

Semiconductor Bonding Equipment Market in North America

The North American semiconductor bonding equipment market holds approximately 11% of the global market share in 2024, driven primarily by substantial government initiatives and technological advancements in the region. The market is characterized by significant investments in research and development activities, particularly through programs like the CHIPS for America Act. The region's focus on advanced packaging techniques and stacked die technologies in connected systems has been a crucial growth driver. Major semiconductor manufacturers are actively expanding their production capabilities across the United States, with particular emphasis on advanced packaging equipment solutions. The presence of established players and emerging startups has created a highly competitive landscape, fostering innovation in bonding technologies. The region's strategic focus on reducing dependence on foreign semiconductor manufacturing equipment has led to increased investments in domestic production capabilities. Furthermore, the strong presence of end-user industries, particularly in automotive electronics, consumer electronics, and telecommunications, continues to drive demand for semiconductor bonding equipment.

Semiconductor Bonding Equipment Market in Asia-Pacific

The Asia-Pacific region has demonstrated remarkable growth in the semiconductor bonding equipment market from 2019 to 2024, establishing itself as the global manufacturing hub for semiconductor technologies. The region's dominance is particularly evident in countries like Taiwan, South Korea, Japan, and China, which host major semiconductor foundries and manufacturing facilities. The market's expansion is driven by substantial investments in semiconductor manufacturing capabilities, particularly in advanced packaging technologies and wafer fabrication. The presence of key market players and their continuous focus on technological advancement has strengthened the region's position in the global supply chain. The region's robust ecosystem of semiconductor manufacturers, coupled with supportive government policies and initiatives, has created a favorable environment for market growth. Additionally, the increasing adoption of advanced technologies such as 5G, artificial intelligence, and the Internet of Things (IoT) has further accelerated the demand for semiconductor bonding equipment in the region. The strong presence of consumer electronics manufacturers and the automotive industry has also contributed significantly to market expansion.

Semiconductor Bonding Equipment Market in Europe

The European semiconductor bonding equipment market is projected to grow at a CAGR of approximately 2% during 2024-2029, driven by strategic initiatives to enhance the region's semiconductor manufacturing capabilities. The market is witnessing significant transformation through various government-backed programs aimed at increasing Europe's global market share in semiconductor production. The region's focus on developing advanced chip manufacturing capabilities, particularly in countries like Germany and France, is creating new opportunities for bonding equipment manufacturers. The European Union's commitment to technological sovereignty in semiconductor production has led to increased investments in research and development activities. The market is particularly benefiting from the growing demand in automotive electronics, industrial automation, and renewable energy sectors. The presence of established research institutions and technological centers has fostered innovation in bonding technologies. Furthermore, the region's emphasis on sustainable manufacturing practices and energy-efficient solutions has influenced the development of next-generation semiconductor packaging equipment.

Semiconductor Bonding Equipment Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for semiconductor bonding equipment with growing potential. The market in these regions is primarily driven by increasing investments in manufacturing capabilities and rising demand for electronic devices. Countries in the Middle East, particularly the UAE and Saudi Arabia, are making strategic moves to establish themselves in the semiconductor industry as part of their economic diversification initiatives. Latin American countries, led by Brazil and Mexico, are witnessing growing demand for semiconductor components in the automotive and consumer electronics sectors. The region's market is characterized by increasing foreign direct investments and government initiatives to boost local manufacturing capabilities. The growing focus on digital transformation and technological advancement in these regions is creating new opportunities for wire bonding equipment manufacturers. Additionally, the establishment of new manufacturing facilities and research centers is expected to drive market growth in these regions.

Get Analysis on Important Geographic Markets

Download PDF

Semiconductor Bonding Equipment Market Overview

Top Companies in Semiconductor Bonding Equipment Market

The semiconductor bonding equipment market features prominent players like EV Group, ASMPT Semiconductor Solutions, MRSI Systems, WestBond Inc., Panasonic Industry Co. Ltd, and Tokyo Electron Limited, who are actively shaping industry dynamics through continuous innovation. These companies are increasingly focusing on developing advanced bonding solutions, particularly in areas like hybrid bonding technology, wafer-to-wafer bonding, and die-to-wafer bonding processes. The industry witnesses regular product launches and upgrades, with companies investing heavily in research and development to meet the evolving demands of semiconductor manufacturing. Strategic partnerships with research institutions, material suppliers, and end-users have become crucial for product development and market expansion. Companies are also expanding their global footprint through new manufacturing facilities and service centers, particularly in emerging semiconductor hubs across Asia-Pacific, while simultaneously strengthening their presence in established markets through enhanced distribution networks and customer support services.

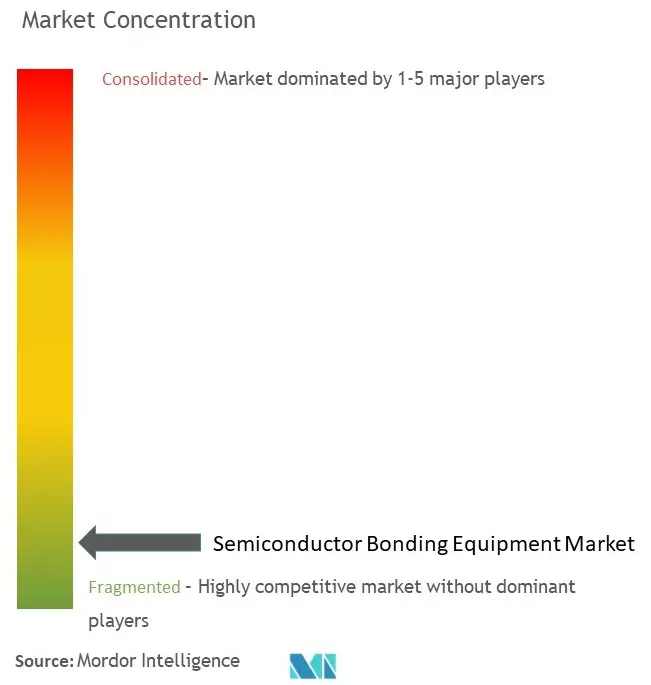

Market Dominated by Global Technology Conglomerates

The semiconductor bonding equipment market exhibits a relatively concentrated structure, dominated by established global technology conglomerates with extensive semiconductor industry experience. These major players leverage their comprehensive product portfolios, established distribution networks, and strong financial capabilities to maintain their market positions. The market demonstrates a mix of pure-play bonding equipment manufacturers and diversified semiconductor equipment providers, with the latter having advantages in offering integrated solutions. Regional players, particularly in Asia, are gaining prominence by specializing in specific bonding technologies and serving local semiconductor manufacturers, though their influence remains limited compared to global leaders.

The industry has witnessed strategic consolidation through mergers and acquisitions, primarily driven by the need to acquire new technologies and expand geographical presence. Companies are increasingly pursuing vertical integration strategies to enhance their control over the supply chain and improve operational efficiency. Joint ventures and strategic alliances have become common, particularly for developing next-generation bonding technologies and addressing the growing demand for advanced packaging solutions. The market's competitive dynamics are further influenced by the increasing focus on specialized applications like MEMS, photonic devices, and power semiconductors, leading to niche market opportunities for specialized semiconductor assembly equipment manufacturers.

Innovation and Adaptability Drive Market Success

Success in the semiconductor bonding equipment market increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological requirements. Market leaders are strengthening their positions by investing in advanced research facilities, developing proprietary technologies, and building comprehensive intellectual property portfolios. Companies are focusing on enhancing their equipment's precision, throughput, and reliability while simultaneously reducing the total cost of ownership for customers. The ability to provide customized solutions for specific applications, coupled with comprehensive after-sales support and training services, has become crucial for maintaining customer relationships and market share.

For emerging players and contenders, the path to market success lies in identifying and serving underserved market segments or developing innovative solutions for specific applications. The increasing complexity of semiconductor devices and the growing demand for advanced packaging solutions create opportunities for specialized IC packaging equipment providers. Companies must also consider the high concentration of customers in the semiconductor industry and develop strategies to manage the associated risks. Regulatory compliance, particularly regarding environmental standards and safety requirements, is becoming increasingly important as governments worldwide implement stricter controls on semiconductor manufacturing processes. The ability to navigate these regulatory requirements while maintaining operational efficiency will be crucial for long-term success in the market.

Semiconductor Bonding Equipment Market Leaders

-

EV Group

-

ASMPT Semiconductor Solutions

-

MRSI Systems. (Myronic AB)

-

WestBond Inc.

-

Panasonic Holding Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Semiconductor Bonding Equipment Market News

- December 2023 - Panasonic Industrial Automation and Mouser Electronics, the authorized global distributor of the latest electronic components and industrial automation products, entered a distribution agreement. According to the terms of the agreement, Panasonic Industrial Automation will provide customers with a wide range of integrated solutions for automation markets ranging from automotive to semiconductor, packaging to bio-medical.

- December 2023 - Tokyo Electron announced that it developed an Extreme Laser Lift Off (XLO) technology that contributes to innovations in the 3D integration of advanced semiconductor devices adopting permanent wafer bonding. This new technology for two permanently bonded silicon wafers uses a laser to separate the top silicon substrate from the bottom substrate with an integrated circuit layer.

Semiconductor Bonding Equipment Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Market Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5. Market Dynamics

-

5.1 Market Driver

- 5.1.1 Increasing Investment by Semiconductor Manufacturers to Expand their Manufacturing Capacity

- 5.1.2 Rising Demand for Semiconductor Chips across Various Application

-

5.2 Market Restraints

- 5.2.1 High Cost of Ownership

- 5.2.2 Increased Complexity Owing to Miniaturization of Circuits

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Permanent Bonding Equipment

- 6.1.2 Temporary Bonding Equipment

- 6.1.3 Hybrid Bonding Equipment

-

6.2 By Application

- 6.2.1 Advanced Packaging

- 6.2.2 Power IC and Power Discrete

- 6.2.3 Photonic Devices

- 6.2.4 MEMS Sensors and Actuators

- 6.2.5 Engineered Substrates

- 6.2.6 RF Devices

- 6.2.7 CMOS Image Sensors (CIS)

-

6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 EV Group

- 7.1.2 ASMPT Semiconductor Solutions

- 7.1.3 MRSI Systems. (Myronic AB)

- 7.1.4 WestBond Inc.

- 7.1.5 Panasonic Holding Corporation

- 7.1.6 Palomar Technologies

- 7.1.7 Dr. Tresky AG

- 7.1.8 BE Semiconductor Industries NV

- 7.1.9 Fasford Technology Co.Ltd (Fuji Group)

- 7.1.10 Kulicke and Soffa Industries Inc.

- 7.1.11 DIAS Automation (HK) Ltd

- 7.1.12 Shibaura Mechatronics Corporation

- 7.1.13 SUSS MicroTec SE

- 7.1.14 Tokyo Electron Limited

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Semiconductor Bonding Equipment Market Industry Segmentation

Wafer bonding is the process of adhering a thin substrate wafer to a support carrier disc using wafer substrate bonding units. Several bonding techniques are used to achieve this, requiring various equipment or machinery. Equipment types include permanent bonding, temporary bonding, and hybrid bonding. The scope of the bonding equipment market is limited to applications such as advanced packaging, power IC and power discrete, photonic devices, MEMS sensors and actuators, engineered substrates, RF devices, and CMOS image sensors (CIS).

The semiconductor bonding equipment market is segmented by type (permanent bonding equipment, temporary bonding equipment, hybrid bonding equipment), application (advanced packaging, power IC and power discrete, photonic devices, MEMS sensors and actuators, engineered substrates, RF devices, CMOS image sensors (CIS)), and geography (North America, Asia, Europe, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Type | Permanent Bonding Equipment |

| Temporary Bonding Equipment | |

| Hybrid Bonding Equipment | |

| By Application | Advanced Packaging |

| Power IC and Power Discrete | |

| Photonic Devices | |

| MEMS Sensors and Actuators | |

| Engineered Substrates | |

| RF Devices | |

| CMOS Image Sensors (CIS) | |

| By Geography | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Semiconductor Bonding Equipment Market Research FAQs

How big is the Semiconductor Bonding Equipment Market?

The Semiconductor Bonding Equipment Market size is expected to reach USD 568.96 million in 2025 and grow at a CAGR of 4.90% to reach USD 722.70 million by 2030.

What is the current Semiconductor Bonding Equipment Market size?

In 2025, the Semiconductor Bonding Equipment Market size is expected to reach USD 568.96 million.

Who are the key players in Semiconductor Bonding Equipment Market?

EV Group, ASMPT Semiconductor Solutions, MRSI Systems. (Myronic AB), WestBond Inc. and Panasonic Holding Corporation are the major companies operating in the Semiconductor Bonding Equipment Market.

Which is the fastest growing region in Semiconductor Bonding Equipment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Semiconductor Bonding Equipment Market?

In 2025, the Asia Pacific accounts for the largest market share in Semiconductor Bonding Equipment Market.

What years does this Semiconductor Bonding Equipment Market cover, and what was the market size in 2024?

In 2024, the Semiconductor Bonding Equipment Market size was estimated at USD 541.08 million. The report covers the Semiconductor Bonding Equipment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Semiconductor Bonding Equipment Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Semiconductor Bonding Equipment Market Research

Mordor Intelligence provides comprehensive industry analysis and market outlook for the semiconductor bonding equipment market, offering detailed insights into market size, growth trends, and competitive landscape. Our research covers the entire spectrum of semiconductor manufacturing equipment and semiconductor packaging equipment, including wire bonding equipment, flip chip bonders, and die attach equipment. The report pdf includes extensive market segmentation, forecasts, and analysis of key market leaders, helping stakeholders make informed decisions in this rapidly evolving industry.

Our consulting expertise extends beyond traditional market research to provide strategic insights for the semiconductor assembly equipment and semiconductor backend equipment sectors. We assist clients with technology scouting to identify emerging bonding technologies, conduct R&D and patent analysis for innovative thermal compression bonding equipment, and perform competition assessment to understand market positioning. Our services include detailed analysis of advanced packaging trends, project feasibility studies for new bonding equipment installations, and technology adoption roadmaps. Through B2B surveys and interviews with industry experts, we help clients understand evolving customer needs and market dynamics in the semiconductor packaging and assembly equipment market.