| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 31.08 Billion |

| Market Size (2030) | USD 56.75 Billion |

| CAGR (2025 - 2030) | 12.80 % |

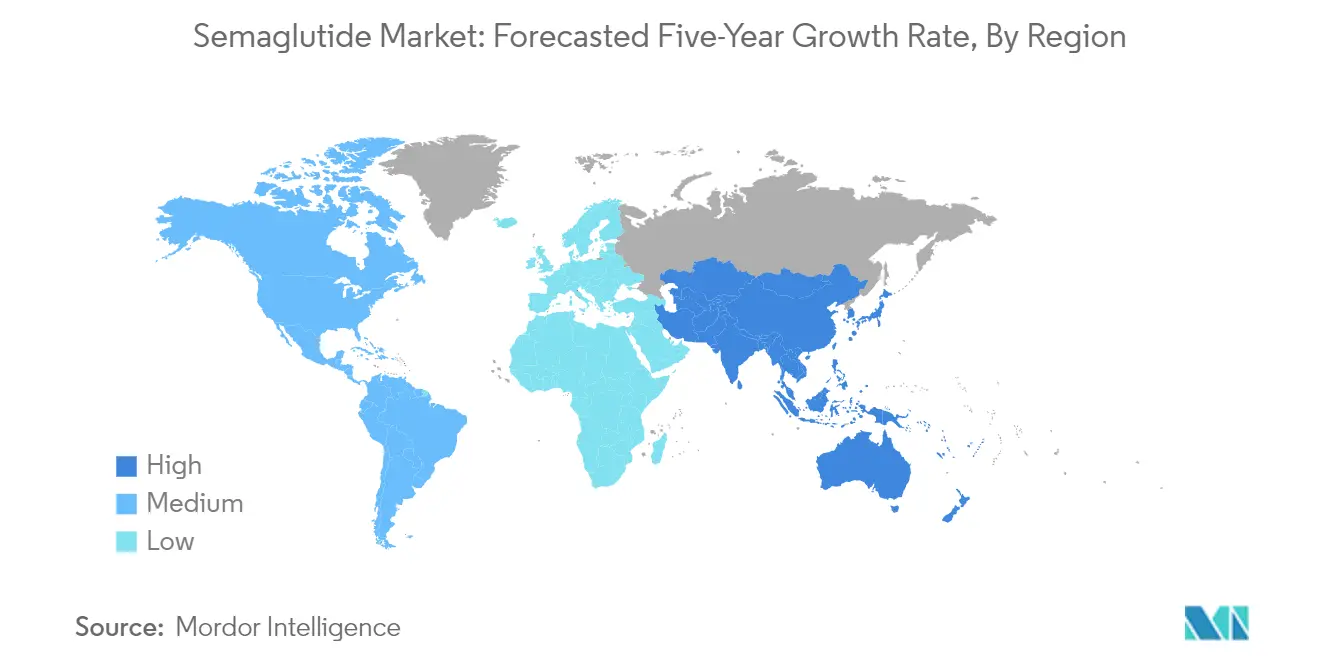

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

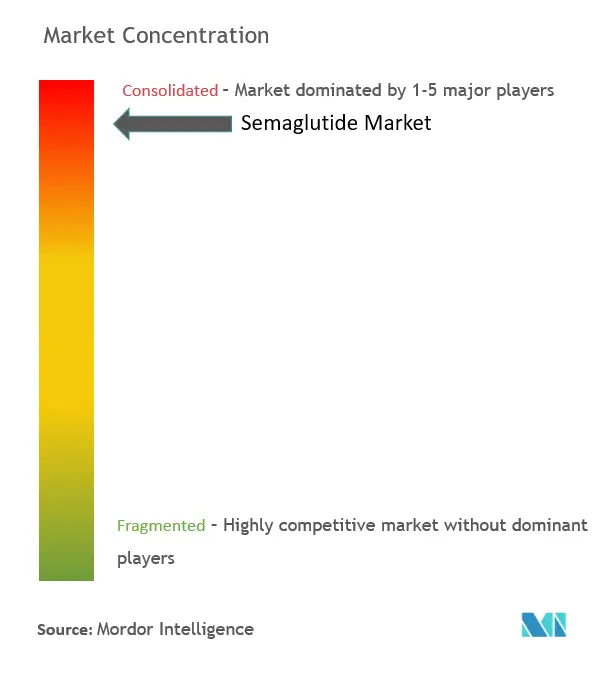

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Semaglutide Market Analysis

The Semaglutide Market size is estimated at USD 31.08 billion in 2025, and is expected to reach USD 56.75 billion by 2030, at a CAGR of 12.8% during the forecast period (2025-2030).

Beyond Weight Loss: Semaglutide's Expanding Therapeutic Horizon

The therapeutic landscape for semaglutide extends far beyond its initial positioning as a diabetes medication. While Ozempic and Rybelsus gained prominence in managing type 2 diabetes, and Wegovy revolutionized weight management, the clinical utility of this GLP-1 receptor agonist continues to evolve. Healthcare providers now recognize semaglutide's potential impacts across multiple body systems - from cardioprotective effects and kidney function preservation to possible cognitive benefits currently under investigation. This multifaceted therapeutic profile is reshaping treatment protocols, with endocrinologists, cardiologists, and primary care physicians developing collaborative approaches to patient care. The medication's effectiveness in addressing various components of metabolic syndrome simultaneously represents a paradigm shift from the traditional siloed approach to chronic disease management. For healthcare systems, this necessitates a fundamental rethinking of disease management programs that have historically separated diabetes care from obesity treatment and cardiovascular risk reduction. Forward-thinking providers are now implementing comprehensive metabolic health programs that leverage semaglutide's broad mechanism of action while addressing potential side effects through proactive management. The clinical implication is clear: healthcare organizations that develop integrated treatment pathways recognizing semaglutide's multisystem effects will deliver superior outcomes compared to those maintaining fragmented specialty-based approaches.

The Patient Journey Reimagined: New Delivery Models Shaping Market Access

The unprecedented patient demand for semaglutide has catalyzed significant transformation in healthcare delivery models. Traditional prescription pathways have given way to innovative access channels, with digital health platforms becoming instrumental in connecting patients to semaglutide therapies. Telehealth services specialized in weight management and diabetes care have experienced dramatic growth, creating streamlined patient journeys from initial consultation through ongoing medication management. This evolution extends to pharmacy services, where specialized fulfillment models help patients navigate insurance coverage challenges and manufacturer savings programs. Patient support has similarly evolved, with specialized coaching programs designed to maximize therapeutic outcomes by addressing the lifestyle modifications needed alongside medication therapy. These emerging care models reflect a market adapting to both clinical needs and consumer preferences, with convenience and continuity becoming differentiating factors in provider selection. Insurance coverage remains variable across markets, creating opportunity for subscription-based models that offer predictable monthly costs for patients paying out-of-pocket. The strategic implication for market stakeholders is clear: success in the semaglutide space increasingly depends on creating ecosystem-based approaches that extend beyond medication provision to encompass the entire therapeutic journey. Companies and providers that master this integrated service delivery will capture greater market share than those focused solely on medication access.

Manufacturing Excellence: The Unsung Hero Behind Market Expansion

Behind the headlines about clinical benefits and market demand, the story of semaglutide companies and their manufacturing capabilities represents a critical market dynamic often overlooked in analysis. The complex production process for this peptide-based medication requires sophisticated biopharmaceutical manufacturing expertise, creating significant barriers to entry for potential competitors. Capacity expansion has become a strategic priority for manufacturers as demand continues to grow across both diabetes and weight management indications. These production investments require long-term planning, with new facilities taking years to validate and bring online - timing that impacts competitive positioning as patents eventually expire. The geographic distribution of manufacturing capacity reveals interesting strategic choices, with companies balancing production costs against supply chain security and intellectual property protection. Regional manufacturing hubs allow for tailored distribution strategies that address varying regulatory requirements and patient needs across markets. The intricate cold chain logistics required for injectable semaglutide formulations adds another layer of complexity that manufacturers must master. Quality control takes on heightened importance given the medication's growing use in otherwise healthy populations seeking weight management solutions. The manufacturing implications are significant: as demand continues to exceed supply in many markets, companies that achieve manufacturing excellence - optimizing production efficiency while maintaining rigorous quality standards - will capture disproportionate market value compared to those struggling with supply consistency.

Semaglutide Market Trends

Diabetes Surge: The Silent Catalyst Behind Semaglutide's Ascent

The relentless increase in diabetes prevalence worldwide serves as a powerful undercurrent propelling the semaglutide market forward. With millions of new diagnoses each year, particularly Type 2 diabetes in both developed and emerging economies, healthcare systems are seeking more effective glucose management solutions. The clinical profile of semaglutide—with its demonstrated ability to effectively lower HbA1c levels while offering weight reduction benefits—has positioned it as a preferred option for healthcare providers managing increasingly complex diabetic patients. Medical practices are adapting their treatment algorithms to incorporate these benefits earlier in the disease progression, recognizing that earlier intervention with effective agents can significantly improve long-term outcomes.The changing demographics of diabetes are reshaping treatment paradigms and the market landscape for GLP-1 receptor agonists like semaglutide.

Younger patient populations, earlier onset of Type 2 diabetes, and longer treatment durations collectively increase the importance of medications with proven long-term safety profiles. Healthcare systems adopting value-based care models find medications like Ozempic and Rybelsus particularly attractive for their potential to reduce costly complications and hospitalizations. Companies that develop patient support programs and digital monitoring tools alongside their semaglutide offerings are seeing better adherence rates and patient outcomes, creating a competitive advantage in this growing therapeutic area.

Beyond the Scale: How Obesity's Global Footprint Expands Semaglutide's Reach

The worldwide obesity crisis has evolved from a public health concern into a powerful market force for weight management medications, with semaglutide emerging as a frontrunner in this expanded arena. Unlike previous generations of weight loss drugs that offered modest benefits with significant side effects, semaglutide's ability to deliver substantial, sustained weight reduction has redefined expectations. This shift is particularly evident in markets where obesity-related comorbidities drive healthcare costs—creating economic incentives for insurers and health systems to embrace pharmaceutical interventions that address the root cause rather than merely managing symptoms.

Medical practices specializing in weight management are developing new protocols that combine semaglutide with lifestyle interventions for optimal results. The strategic positioning of semaglutide formulations specifically for weight management—exemplified by Wegovy—represents a significant development in pharmaceutical market strategy. By creating distinct branding, dosing protocols, and clinical evidence pathways for obesity indications, manufacturers have effectively expanded their addressable market without cannibalizing their diabetes franchise.

Employers and insurance providers, traditionally hesitant to cover weight loss medications, are increasingly recognizing the economic benefits of semaglutide coverage as evidence emerges on reduced workplace absenteeism and decreased healthcare utilization among users. Organizations that develop comprehensive weight management programs incorporating both pharmaceutical and lifestyle components will likely achieve better patient outcomes while securing preferred formulary positions.

Beyond Blood Sugar: Semaglutide's Expanding Therapeutic Horizons

The clinical versatility of semaglutide is opening doors beyond its original diabetes indication, creating multiple growth vectors for market participants. Emerging evidence suggesting cardiovascular benefits, renal protection, and potential applications in non-alcoholic steatohepatitis (NASH) has pharmaceutical strategists envisioning a multi-purpose therapy rather than a single-indication product. This expanded therapeutic profile changes the value proposition significantly—potentially transforming semaglutide from a specialized diabetes medication into a cornerstone therapy with applications across multiple specialties and care pathways.

Medical centers are increasingly establishing dedicated clinics that specialize in metabolic health rather than single-disease management, recognizing the interconnected nature of these conditions. The sequential expansion strategy employed with semaglutide offers valuable lessons about maximizing molecular value through methodical indication expansion. Rather than pursuing all potential applications simultaneously, the measured approach of establishing a strong market presence in diabetes before targeting obesity has allowed for optimal pricing strategies and the development of specialized commercial infrastructure.

Healthcare systems and payers are increasingly evaluating semaglutide through a wider lens—considering its potential impact across multiple disease states when making coverage decisions. Companies that develop comprehensive evidence-generation plans spanning multiple indications will more effectively capture the full value potential of next-generation GLP-1 receptor agonists and position themselves as leaders in metabolic health.

From Injection to Ingestion: How Delivery Innovation Propels Semaglutide's Market Evolution

The innovation landscape in the semaglutide market has shifted decisively toward drug delivery systems, with oral formulations like Rybelsus representing a potential tipping point in patient acceptance and market penetration. This technological leap addresses one of the most significant barriers to GLP-1 receptor agonist adoption—injection aversion—opening the door to earlier therapy initiation and expanded patient populations.

Primary care physicians, who have historically shown reluctance to prescribe injectable therapies due to patient resistance and office workflow challenges, are now incorporating oral semaglutide into their treatment algorithms at increasing rates, expanding the prescriber base beyond endocrinology specialists. Medical practices report that patients previously hesitant about injection therapy are now proactively discussing oral options during consultations.

The development of varied delivery mechanisms has triggered an industry-wide race to improve convenience and reduce administration frequency. Weekly injectable formulations have already demonstrated substantial advantages over daily options, and research into longer-acting preparations represents the next competitive frontier for semaglutide companies. Healthcare providers increasingly factor patient preferences and adherence probability into prescribing decisions, giving delivery innovations significant influence on market dynamics. Organizations that combine innovative delivery systems with practical support infrastructure—including adherence tools, side effect management resources, and reimbursement navigation—are establishing advantages in this evolving therapeutic category, particularly with patients who prioritize convenience in their treatment decisions.

Patient Power: How Consumer Preference is Reshaping the Semaglutide Landscape

The unprecedented patient demand for semaglutide products represents a case of consumer-driven pharmaceutical market dynamics fueled by visible results, celebrity endorsements, and social media discourse. Unlike most prescription medications, where physicians remain the primary decision drivers, GLP-1 receptor agonists like Ozempic have generated a level of patient awareness and proactive requests that more closely resemble consumer product patterns. This shift in influence has significant implications for pharmaceutical marketing strategies as direct-to-consumer communication channels gain importance relative to traditional physician engagement efforts.

Healthcare practices that are unprepared for the volume of patient inquiries about semaglutide have developed standardized assessment protocols and educational materials to manage this demand efficiently. The patient preference phenomenon extends beyond awareness to sophisticated benefit-risk calculations that impact persistence and adherence patterns for semaglutide therapy. Users who experience meaningful weight reduction alongside glycemic control demonstrate higher persistence rates, creating a cycle of visible results, positive word-of-mouth, and sustained treatment engagement. Manufacturers who understand the patient journey—including early expectations, side effect management, and achievement milestones—can design support programs that improve real-world outcomes.

Forward-thinking healthcare systems are responding by creating specialized metabolic health clinics that combine pharmaceutical intervention with lifestyle modification programs, recognizing that optimization of these highly sought therapies requires dedicated support rather than integration into standard care models without additional resources.

Segment Analysis: By Brand

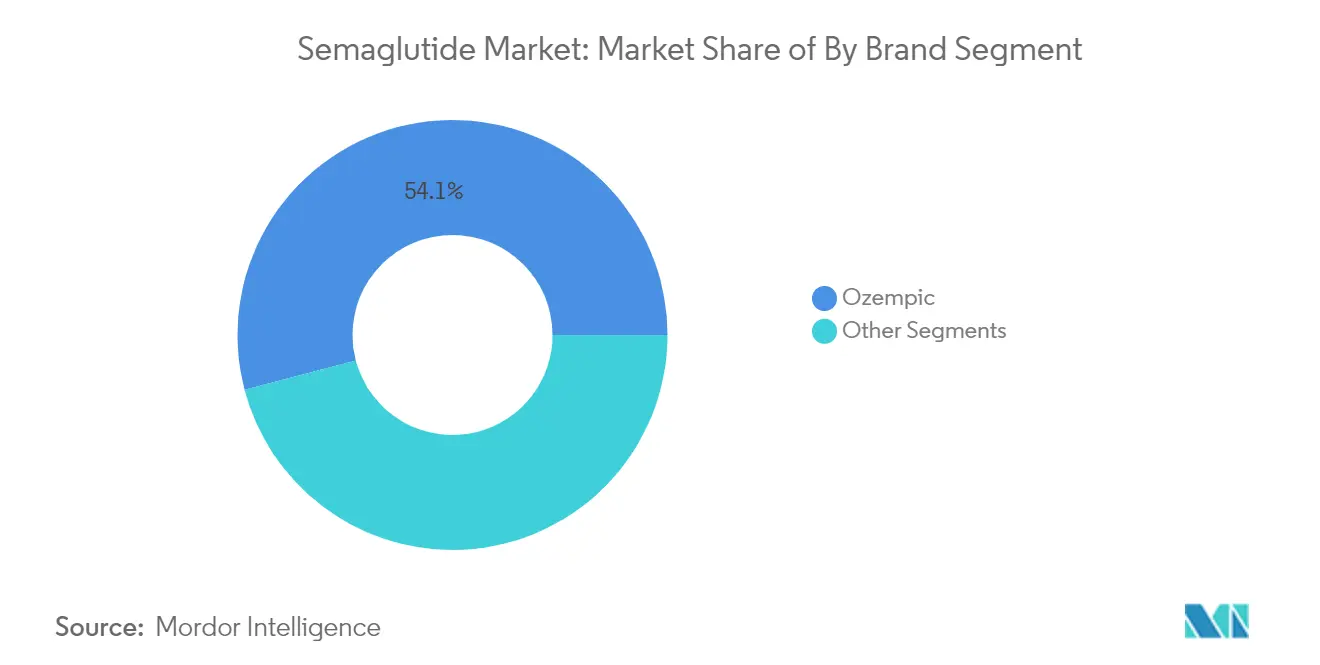

Ozempic: Commanding the Semaglutide Market

Ozempic has reshaped diabetes management in 2025, capturing a dominant 54.1% of the global semaglutide market. This success stems from its proven effectiveness as both a diabetes treatment and weight management solution. Novo Nordisk has positioned Ozempic as the preferred choice for healthcare providers seeking complete metabolic control for their patients, driving substantial Ozempic market share across all healthcare settings. This market leadership reveals an important strategic insight: diabetes and weight management markets are merging, with both patients and doctors preferring treatments that tackle both conditions. Companies in this field must adapt to a new reality where single-purpose products struggle against versatile treatments like Ozempic that deliver wider health benefits. To compete effectively, pharmaceutical companies need to forge partnerships with metabolic research organizations and healthcare systems that can enhance their market position in this transformed landscape.

Rybelsus: Oral Innovation Driving Unprecedented Growth

Rybelsus is setting new growth standards in the semaglutide market with an impressive 18.7% CAGR, outpacing all competitors through its innovative oral delivery format. As the first oral GLP-1 receptor agonist, Rybelsus has tapped into a large segment of patients who avoided injectable therapies but wanted semaglutide benefits. This growth comes from the product's perfect balance of effectiveness and convenience—a combination particularly appealing to primary care physicians treating various diabetes patients. The strong Rybelsus sales forecast highlights a key market lesson: innovation in how drugs are delivered can be as valuable as creating new molecules. This insight should reshape pharmaceutical strategy, suggesting companies should invest in developing alternative delivery systems for existing effective drugs rather than focusing only on new compounds. This approach offers a faster, more reliable path to market growth by addressing patient preferences and expanding treatment access across different population groups.

Wegovy: Strategic Positioning in Weight Management

Between Ozempic's market dominance and Rybelsus's rapid growth, Wegovy has created its distinct position by targeting obesity treatment rather than diabetes care. Novo Nordisk's careful semaglutide market approach has allowed this brand to avoid competing directly with its sister products while leveraging the same effective semaglutide molecule. This strategy shows how pharmaceutical companies can maximize value from a single compound by customizing branding, dosing, and target uses for different patient groups. Recent Wegovy market share developments reveal complex market dynamics where doctors increasingly view these treatments as complementary options to match individual patient needs, insurance coverage, and clinical situations. This sophisticated approach to brand management offers valuable lessons for pharmaceutical executives: instead of pursuing winner-takes-all strategies, carefully differentiated brands within a therapeutic class can expand the overall semaglutide market size while meeting diverse patient needs—creating more sustainable growth than any single product could achieve alone.

Geography Analysis

North America: The Powerhouse Behind Semaglutide's Global Success

North America dominates the semaglutide market, capturing 73.8% of global market share in 2025. This leadership position stems from several key advantages: strong healthcare infrastructure, high obesity and diabetes rates, good physician acceptance, and broad insurance coverage for GLP-1 medications. The region has benefited significantly from Novo Nordisk's strategic focus, including extensive educational campaigns and consumer advertising that have normalized weight management medications. For industry players, this dominance carries an important lesson: North America will continue to receive priority during supply constraints, making it essential for any serious market entry strategy to include strong plans for this region to secure meaningful revenue opportunities.

United States: Where Semaglutide Found Its First Home and Greatest Champions

The United States represents the core of the global semaglutide market, controlling majority of worldwide sales. What makes the U.S. market unique isn't just its size but its distinctive healthcare environment that has accelerated adoption. American patients have become powerful advocates, with social media amplifying success stories and celebrities openly discussing their Ozempic experiences. This public acceptance, combined with medical professionals increasingly treating obesity as a chronic disease rather than a lifestyle issue, has created strong ongoing demand. The strategic takeaway is clear: the U.S. market serves as both a testing ground and primary revenue source for semaglutide producers, making U.S.-focused clinical data and real-world evidence critical competitive advantages.

Canada: The Quiet Revolution in Semaglutide Adoption

While less prominent than the U.S., Canada represents an important part of the North American semaglutide market, with steady growth. The Canadian approach to Ozempic and Wegovy adoption differs noticeably from the American model—it's less driven by consumer marketing and more by systematic integration into clinical guidelines for diabetes and obesity treatment. Canadian healthcare providers show particular interest in semaglutide's heart benefits beyond blood sugar control, creating distinct prescription patterns. For companies in this space, the key insight is recognizing that Canada's public health system creates different requirements for market access—success here requires evidence focused on long-term health economic outcomes rather than just short-term weight loss results, offering valuable strategic diversity for companies too heavily focused on the American market.

Europe: The Strategic Counterbalance in the Global Semaglutide Landscape

Europe represents the second most important market in the global semaglutide market, offering unique strategic value through its diverse healthcare systems. The European approach to GLP-1 medications reflects a more cautious regulatory environment, with thorough health technology assessments determining both approval and reimbursement. This creates a market where clinical evidence requirements often exceed those in North America, particularly regarding long-term heart and mortality outcomes. European health authorities typically negotiate aggressively on Ozempic and Wegovy pricing, creating challenges but potentially valuable precedents for market access strategies. The key insight for stakeholders is seeing Europe not merely as a secondary revenue source but as a critical validation region—success here often predicts global acceptance and provides essential real-world evidence for expansion into other regions.

Germany: The European Stronghold of Semaglutide Innovation

Germany stands as the cornerstone of European semaglutide market adoption, serving as the regional leader for GLP-1 acceptance. The German market's importance comes from its unique combination of physician independence, strong diabetes specialization, and relatively flexible reimbursement pathways compared to other European countries. German medical communities have been particularly receptive to Rybelsus as the first oral GLP-1 option, creating distinct prescription patterns that prioritize patient convenience. The country's robust health economic assessment system has also generated valuable real-world evidence supporting semaglutide's long-term value. For companies in this market, the strategic priority lies in recognizing Germany's dual role as both a commercial powerhouse and a reference market—successful strategies here often spread throughout European territories, making German key opinion leader engagement and market access excellence especially valuable.

Spain: The Unexpected Growth Engine in Europe's Semaglutide Story

Spain has emerged as Europe's surprise growth leader in the semaglutide market, achieving an impressive CAGR that outpaces all other European countries. This accelerated adoption stems from several converging factors: Spain's diabetes management guidelines underwent major revision in 2023, moving GLP-1 medications to earlier-line therapy; Spanish endocrinologists have shown strong interest in the dual indications for both diabetes and weight management; and the national health system implemented innovative outcomes-based payment models for Ozempic that enabled broader access. The key insight for market participants focuses on Spain's role as a testing ground for new commercial approaches—the country's regional autonomy in healthcare decision-making has allowed for natural experiments in market access strategy, providing valuable lessons that can be applied to other European markets facing similar pricing pressures and value demonstration requirements.

The European Mosaic: Navigating Diverse Healthcare Systems in the Semaglutide Era

Beyond Germany and Spain, Europe's remaining territories form a complex landscape of opportunity in the semaglutide market, each with distinct adoption drivers and barriers. The United Kingdom has focused semaglutide access through specialized weight management centers rather than primary care, creating concentrated areas of expertise. France has shown particular interest in Rybelsus as an oral option, with its pharmacy-centered healthcare model supporting patient education initiatives. Italy shows uneven adoption patterns, with northern regions prescribing at rates closer to Germany while southern areas lag behind. Switzerland, despite its smaller population, has outsized influence through its early adoption trends and willingness to integrate GLP-1 medications into comprehensive care pathways. The unifying strategic requirement across these diverse markets centers on localization excellence—success demands adapting global evidence packages to address the specific economic, cultural, and clinical priorities of each healthcare system rather than applying one-size-fits-all European strategies.

Asia-Pacific: The Future Frontier of Semaglutide Expansion

The Asia-Pacific region represents both the current challenge and future promise of the global semaglutide market, positioning itself as tomorrow's growth engine. This region presents striking contrasts—containing both highly developed healthcare systems with established GLP-1 adoption patterns and emerging markets where awareness and accessibility remain major barriers. The region's diabetes epidemic, particularly evident in countries like China and India, creates an underlying demand driver that promises sustained growth as access barriers are addressed. Pricing strategies across Asia-Pacific show interesting adaptations, with tiered approaches and market-specific presentations helping balance affordability with commercial viability. The strategic priority lies in recognizing the region's future importance—those that invest now in physician education, patient awareness, and flexible pricing models will likely capture greater value as these markets mature and healthcare spending increases in the coming decade.

Rest of the World: Emerging Opportunities Beyond Major Markets

The remaining global territories represent a growing semaglutide market, with growth trajectories pointing to untapped potential, particularly in select South American and Middle Eastern countries. Brazil leads the region in volume, though with distinct pricing pressures that require creative market access approaches. Middle Eastern Gulf states present a different picture, with high per-capita wealth allowing premium pricing but requiring investment in physician education about obesity as a medical rather than lifestyle condition. The African continent remains underpenetrated mainly, though South Africa and select North African countries show promising early indicators. For manufacturers and distributors, the key strategy involves identifying and developing "lighthouse markets" within each region—countries whose healthcare systems and economic foundations can support early adoption and potentially create reference models for neighboring territories, maximizing resource efficiency while building foundations for future expansion.

Semaglutide Industry Overview

Dominance Amid Disruption: The Novo Nordisk Factor

The semaglutide market is largely controlled by Novo Nordisk, which owns the patents for major brands like Ozempic, Rybelsus, and Wegovy. With Ozempic market share at approximately 54.1%, Novo Nordisk has built a significant lead that makes it difficult for new players to enter the market. This forces other semaglutide companies to find unique selling points such as new delivery methods or improved side effect profiles. The key takeaway for industry players is simple: to succeed in this market, companies need to solve problems that Novo Nordisk's products don't address rather than competing directly. We're seeing this play out as pharmaceutical companies team up with tech firms to create digital tools that help patients stick to their medication schedules and achieve better weight management results - a strategy that could help smaller players find their place without directly challenging Novo Nordisk's dominant position.

Beyond the Molecule: The Innovation Battleground

While the basic semaglutide compounds are patent-protected, smart companies are finding competitive advantages through innovations in how the drug is formulated, delivered, and experienced by patients. Rybelsus stands out as the first oral GLP-1 medication, showing how delivery innovation can create a distinct market position even when using the same active ingredient as injectable versions. Companies are increasingly focusing on improving drug formulations to extend patent life and develop technologies that enhance absorption, reduce side effects, or allow less frequent dosing. The market is shifting toward comprehensive treatment solutions rather than standalone medications. Several medium-sized pharmaceutical companies are now developing diagnostic tools to identify which patients will respond best to GLP-1 therapy, potentially saving costs by avoiding treatment for those unlikely to benefit. This more holistic approach is becoming essential for companies wanting to compete effectively beyond just manufacturing the molecule.

Market Access as Competitive Currency: Navigating Reimbursement Landscapes

As demand for GLP-1 therapies exceeds supply, competitive advantage now belongs to companies that secure favorable insurance coverage and maintain reliable supply chains. The growth in wegovy market share across key regions shows how important relationships with insurance companies and healthcare systems have become. Companies now compete not just on clinical benefits but on their ability to navigate complex insurance and reimbursement systems in different countries. This means developing strong market access capabilities is now a core competitive necessity. Several companies are forming strategic manufacturing partnerships to ensure consistent supply in high-growth regions like Asia-Pacific, where the market is growing at about 15.6% annually. Companies that can balance pricing pressures from insurers while maintaining manufacturing capacity to meet growing demand will gain the edge in this market. These business capabilities, rather than just product features, increasingly determine which companies gain or lose market share in both established and emerging markets.

Semaglutide Market Leaders

-

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Semaglutide Market News

- November 2023: Novo Nordisk announced that Wegovy was shown to reduce the risk in people with cardiovascular disease or another cardiovascular event by 20%. The results were confirmed in a presentation of the entire dataset at the American Heart Association conference in Philadelphia.

- September 2023: Novo Nordisk advised the Ozempic Medicine Shortage Action Group and Therapeutic Goods Administration that the supply of weight loss drugs throughout FY 2023 and FY 2024 will be limited. The company stated that the demand for this drug has surged in recent months, particularly for the low-dose (0.25/0.5 mg) version, and additional demand is created by a rapid increase in prescription for ‘off-label’ use.

Semaglutide Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Brand

- 5.1.1 Wegovy

- 5.1.2 Rybelsus

- 5.1.3 Ozempic

-

5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Rest of the World

6. MARKET INDICATORS

- 6.1 Type 1 Diabetes Population

- 6.2 Type 2 Diabetes Population

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Novo Nordisk A/S

- *List Not Exhaustive

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Semaglutide Industry Segmentation

Semaglutide is an antidiabetic medication used for the treatment of type 2 diabetes and an anti-obesity medication used for long-term weight management. The semaglutide market is segmented by brands and geography. By brands, the market is segmented into Ozempic, Wegovy, and Rybelsus. The report also covers the market sizes and forecast for the semaglutide market in major countries across different regions. For each segment, the market size is provided in terms of value (USD) and volume (units).

| By Brand | Wegovy | ||

| Rybelsus | |||

| Ozempic | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | |||

Need A Different Region or Segment?

Customize Now

Semaglutide Market Research Faqs

How big is the Semaglutide Market?

The Semaglutide Market size is expected to reach USD 31.08 billion in 2025 and grow at a CAGR of 12.80% to reach USD 56.75 billion by 2030.

What is the current Semaglutide Market size?

In 2025, the Semaglutide Market size is expected to reach USD 31.08 billion.

Which is the fastest growing region in Semaglutide Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Semaglutide Market?

In 2025, the North America accounts for the largest market share in Semaglutide Market.

What years does this Semaglutide Market cover, and what was the market size in 2024?

In 2024, the Semaglutide Market size was estimated at USD 27.10 billion. The report covers the Semaglutide Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Semaglutide Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Semaglutide Industry Report

Statistics for the 2025 Semaglutide market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Semaglutide analysis includes a market forecast outlook for 2025 to 2030 and historical overview. Get a sample of this industry analysis as a free report PDF download.