| Study Period | 2024 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 0.77 Billion |

| Market Size (2030) | USD 1.53 Billion |

| CAGR (2025 - 2030) | 14.70 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Scandium Market Analysis

The Scandium Market size is estimated at USD 0.77 billion in 2025, and is expected to reach USD 1.53 billion by 2030, at a CAGR of 14.7% during the forecast period (2025-2030).

The global scandium industry is experiencing significant transformation driven by the rapid evolution of the electric vehicle (EV) sector and emerging technological applications. Global EV sales demonstrated remarkable growth in 2022, with sales figures more than tripling compared to 2021, reaching 997,909 units from 310,982 units. This surge in EV adoption has created new opportunities for scandium applications, particularly in lightweight components and battery technologies. Industry forecasts from Delta Electronics project global EV penetration to reach 40% by 2030, with anticipated sales of 26 million units by 2026, indicating sustained long-term demand for scandium-based materials.

The production landscape of scandium has undergone notable changes with significant investments in new production facilities and extraction technologies. A milestone development occurred in 2022 when Rio Tinto established North America's first scandium oxide production facility, marking a crucial step toward diversifying the global supply chain. This development has been accompanied by innovations in extraction methods, particularly from secondary sources such as red mud and titanium dioxide waste streams, which are helping to address traditional supply constraints and sustainability concerns in the scandium market.

The aerospace manufacturing sector is witnessing substantial restructuring, with several countries implementing strategic initiatives to enhance domestic production capabilities. China's aerospace industry has announced ambitious plans to manufacture 1,000 aircraft before 2030, while various other nations are investing in modernizing their aerospace manufacturing infrastructure. These developments are driving innovations in materials engineering, particularly in the development of advanced alloys and manufacturing processes that utilize rare earth metals like scandium for their unique properties.

Technological advancements in energy storage systems and materials science are opening new avenues for scandium applications. Researchers at leading institutions have made breakthrough discoveries in solid-state battery technology utilizing scandium-based compounds, potentially revolutionizing energy storage solutions. The integration of scandium in advanced materials has expanded beyond traditional applications, with emerging uses in 3D printing, electronics, and next-generation semiconductor technologies. These developments are fostering collaborations between material scientists, manufacturers, and end-users, creating a more dynamic and innovation-driven scandium market environment.

Scandium Market Trends

Increasing Usage in Solid Oxide Fuel Cells (SOFC)

The growing adoption of solid oxide fuel cells is driving significant demand for scandium, primarily due to its crucial role in improving SOFC efficiency and performance. SOFCs utilize scandium oxide in their solid oxide electrolyte material, which facilitates the movement of negative oxygen ions from cathode to anode without requiring precious metals, corrosive acids, or molten materials. The incorporation of scandium in solid electrolytes has revolutionized SOFC technology by enabling operation at much lower temperatures compared to conventional systems, substantially reducing capital and maintenance costs while extending operational life. This technological advancement is particularly significant given that SOFCs can achieve electrical efficiency of up to 60%, far surpassing the efficiency of traditional coal power plants.

Recent developments in the SOFC sector demonstrate strong market momentum and increasing scandium demand. In October 2023, HD Hyundai made a strategic investment of EUR 45 million in Elcogen, focusing on marine propulsion systems and stationary power generation using SOFC technology. Additionally, Bloom Energy's implementation of a groundbreaking 10-megawatt solid oxide fuel cell contract with Unimicron Technology Corp. in August 2023 highlights the growing industrial adoption. The sector's growth is further supported by substantial clean energy investments, with USD 2.8 trillion invested in energy in 2023, of which USD 1.7 trillion was allocated to clean energy initiatives including renewable power, nuclear, grids, and storage solutions. The U.S. Department of Energy's projection of 80% electricity generation from clean sources by 2030 further underscores the potential for SOFC technology and, consequently, scandium demand.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand for Aluminum-Scandium Alloys in the Aerospace and Defense Industry

The aerospace and defense industry's growing demand for aluminum-scandium alloy is emerging as a crucial driver for the scandium industry, driven by the unique properties these alloys offer. When scandium is added to aluminum alloys, it significantly enhances their strength, corrosion resistance, and heat tolerance while improving weldability and weld strength. These characteristics make aluminum-scandium alloy particularly valuable in aircraft manufacturing, where they enable weight reduction of 15-20% compared to traditional materials, leading to improved fuel efficiency and enhanced performance. The material's superior properties, including its ability to prevent embrittlement at high temperatures, make it ideal for critical applications in aerospace, aviation, and defense components.

The expansion of aerospace manufacturing capabilities, particularly in emerging markets, is creating new opportunities for aerospace alloys. China's aerospace sector exemplifies this trend, with over 200 small aircraft parts manufacturers actively contributing to the industry's growth. The Chinese government's substantial investments in domestic manufacturing capacities and the rapid expansion of the aircraft parts and assembly manufacturing sector indicate growing demand for high-performance materials like aerospace alloys. This trend is further reinforced by the increasing focus on developing domestic aerospace capabilities and reducing dependence on traditional aerospace manufacturing hubs. The alloys' applications extend beyond commercial aviation to military aircraft, defense equipment, and space exploration vehicles, where their unique combination of lightweight properties and structural integrity provides significant advantages.

Segment Analysis: Product Type

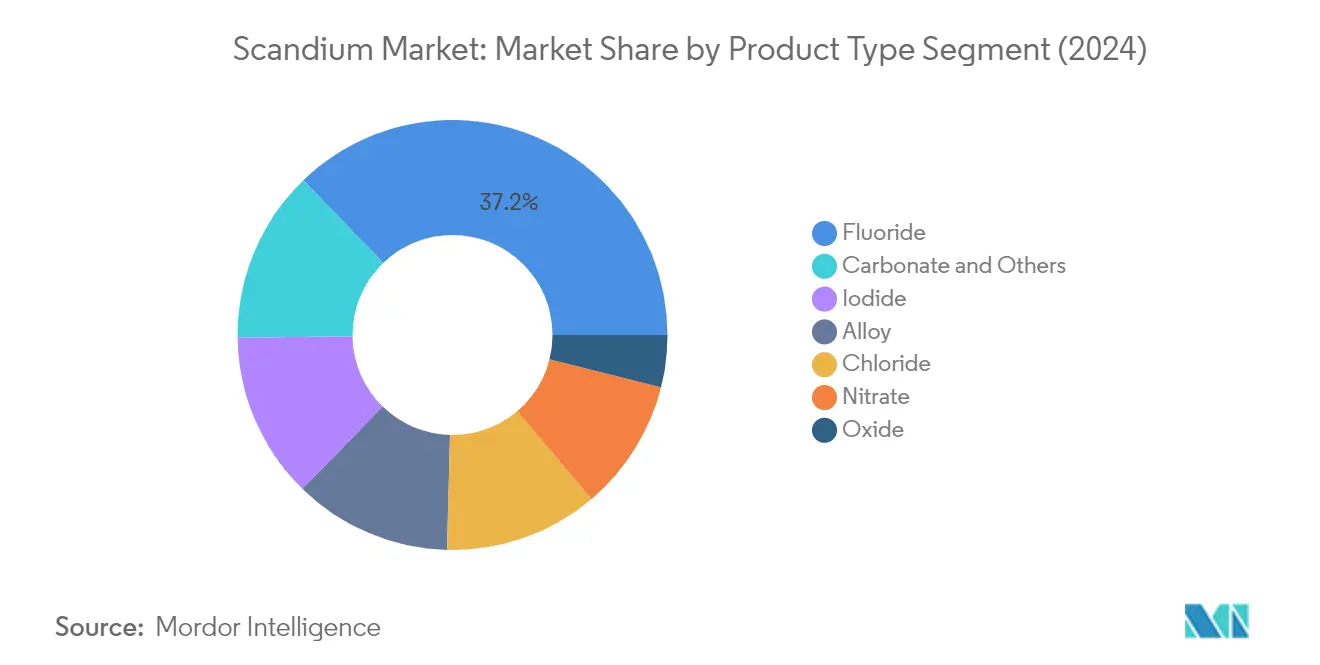

Fluoride Segment in Global Scandium Market

The fluoride segment continues to dominate the global scandium market, holding approximately 37% market share in 2024. This significant market position is attributed to its extensive usage in manufacturing aluminum alloys, particularly for the automobile industry, due to its low impurity levels. Scandium fluoride's unique properties, including its high melting point of around 1,552ºC and negative thermal expansion capabilities over a wide temperature range from 10K to 1100K, make it invaluable for industrial applications. The segment's dominance is further strengthened by its crucial role in optical coatings, catalysts, electronic ceramics, and the laser industry, where its exceptional performance characteristics are essential for high-precision applications.

Chloride Segment in Global Scandium Market

The chloride segment is emerging as the fastest-growing segment in the scandium market, projected to grow at approximately 13% during 2024-2029. This remarkable growth is driven by its increasing adoption in research laboratories and the production of optical fibers, halide lamps, electronic ceramics, and lasers. The segment's expansion is further supported by its critical role in electrolyte procedures for producing metallic scandium. The water-soluble crystalline nature of scandium chloride makes it particularly valuable for forming intermetallic nickel-scandium compound films through potentiostatic cathodic reduction from molten salt mixtures, contributing to its accelerating market growth.

Remaining Segments in Product Type Segmentation

The other significant segments in the scandium market include scandium oxide, nitrate, iodide, alloy, and carbonate products, each serving unique industrial applications. The scandium oxide segment is crucial for high-temperature systems and electronic ceramics, while nitrate compounds are essential in organic synthesis and petrochemical applications. Iodide products are particularly valuable in high-intensity lighting applications, especially in television and film industries. The alloy segment serves critical applications in aerospace and defense, while carbonate and other products contribute to specialized applications such as research and development in various industries. These segments collectively form a comprehensive product portfolio that caters to diverse industrial needs and technological applications.

Segment Analysis: End-User Industry

Solid Oxide Fuel Cells (SOFCs) Segment in Scandium Market

The Solid Oxide Fuel Cells (SOFCs) segment dominates the global scandium market, commanding approximately 36% of the total market share in 2024. This significant market position is primarily driven by the increasing adoption of scandium-stabilized zirconium in SOFCs, which has emerged as the preferred material for oxide-conductive electrolytes. The segment's dominance is further strengthened by scandium's ability to deliver high power outputs at lower temperatures compared to traditional materials, making it particularly valuable for SOFC applications. Major companies like Bloom Energy have been instrumental in driving this segment's growth through their innovative products such as the "Bloom Box," which utilizes scandium in fuel cell ink coating. The segment's strong performance is also supported by various government initiatives and increasing investments in fuel cell technology across major economies, particularly in regions like North America, Europe, and Asia-Pacific.

Electronics Segment in Scandium Market

The Electronics segment is demonstrating remarkable growth potential in the scandium market, with a projected growth rate of approximately 9% during the forecast period 2024-2029. This impressive growth trajectory is driven by the increasing application of scandium in various electronic components, particularly in the manufacturing of high-performance displays, computer switches, and advanced semiconductor devices. The segment's growth is further accelerated by the rising demand for scandium-based materials in emerging technologies such as 5G infrastructure, where scandium's unique properties enhance the performance of electronic components. The expansion of consumer electronics manufacturing in key markets like China, South Korea, and the United States, coupled with ongoing technological advancements in the electronics industry, continues to create new opportunities for scandium applications.

Remaining Segments in End-User Industry

The remaining segments in the scandium market include Aerospace and Defense, Ceramics, Sporting Goods, Lighting, and 3D Printing, each contributing uniquely to the market's dynamics. The Aerospace and Defense segment maintains a strong presence due to the increasing use of scandium-aluminum alloys in aircraft manufacturing and defense applications. The Ceramics segment leverages scandium's properties for high-performance ceramic materials, while the Sporting Goods sector utilizes scandium alloys in manufacturing lightweight, high-strength equipment. The Lighting segment incorporates scandium in high-intensity discharge lamps and stadium lighting systems, while the emerging 3D Printing segment showcases promising applications in additive manufacturing technologies. These segments collectively demonstrate the versatility of scandium across various industrial applications, contributing to the overall market growth.

Scandium Market Geography Segment Analysis

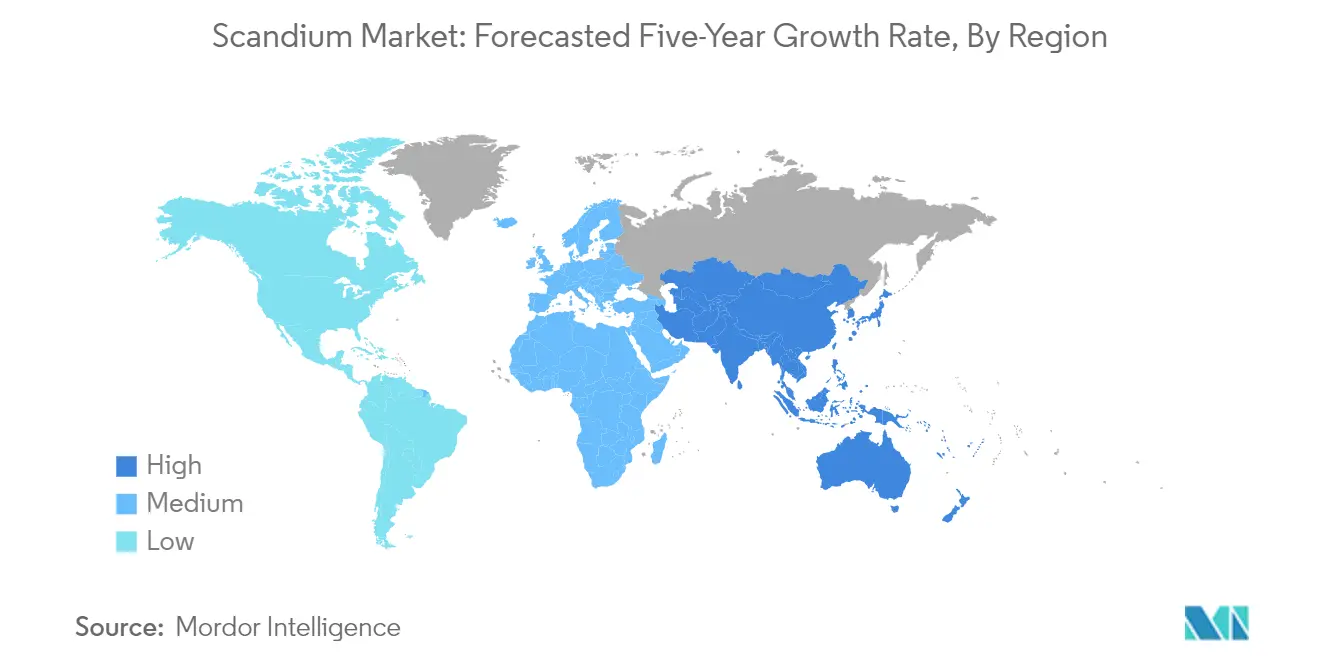

Scandium Market in the United States

The United States dominates the global scandium market, commanding approximately 37% of the total market share. The country's leadership position is primarily driven by its robust aerospace and defense sector, where scandium-aluminum alloys are extensively used in aircraft manufacturing and military applications. The presence of major players like Bloom Energy, a leading manufacturer of solid oxide fuel cells (SOFCs), has significantly contributed to the market's growth, as the company's "Bloom Box" technology utilizes substantial amounts of scandium oxide in fuel cell ink coating. The country's strong focus on research and development, particularly in advanced materials and clean energy technologies, continues to drive innovation in scandium applications. The expanding electric vehicle sector, coupled with the government's push towards sustainable transportation solutions, has created new opportunities for scandium-based materials in lightweight vehicle components and battery technologies. Additionally, the country's well-established electronics and semiconductor industries provide a steady demand for scandium in various high-tech applications.

Scandium Market in Japan

Japan's scandium market is projected to experience remarkable growth with an anticipated CAGR of approximately 11% during 2024-2029. The country's market dynamics are heavily influenced by its leadership in fuel cell technology development, particularly through the Ene-farm program, which provides subsidies for residential fuel cell systems. Japan's commitment to establishing itself as a global leader in fuel cell technology is evident through its ambitious target of deploying 1 GW of larger fuel cell-based systems by 2030. The country's aerospace industry maintains a strong international reputation, particularly in research and development of dual-use technology. Japanese companies are actively involved in the development of several aircraft families, including the B777, B777X, and B787, driving demand for scandium-based alloys. The nation's robust electronics manufacturing sector, which accounts for one-third of its economic output, creates substantial demand for scandium in various applications. The country's focus on technological innovation and advancement in producing new aircraft, coupled with its strong position in consumer electronics manufacturing, continues to drive market growth.

Scandium Market in China

China's scandium market is characterized by its strong integration with the country's massive manufacturing base and growing clean energy sector. The nation's commitment to fuel cell technology development is evident through its government's emphasis on clean energy technology adoption for transitioning to a low-carbon economy. The Chinese government's initiative to support around 50,000 zero-emissions fuel cell vehicles by 2025 has created significant opportunities for scandium applications in SOFCs. The country's aircraft parts and assembly manufacturing sector has been expanding rapidly, with over 200 small aircraft parts manufacturers contributing to the ecosystem. China's position as the world's largest base for electronics production further strengthens its scandium market, with the country actively engaged in manufacturing products ranging from smartphones to gaming systems. The government's push towards electric vehicle adoption and the development of domestic manufacturing capabilities has created additional demand for scandium-based materials in various applications.

Scandium Market in Russia

Russia's scandium market benefits from the country's significant domestic production capabilities and growing industrial base. The nation's aerospace industry, comprising around 250 companies and employing 400,000 people, represents a key demand driver for scandium-based materials. The government's ambitious plan to produce 1,000 domestic aircraft before 2030 demonstrates its commitment to reducing dependence on foreign manufacturers. The country's electronics sector, primarily driven by Ruselectronics, which accounts for 80% of domestic electronics production, provides a steady demand for scandium in various applications. The development of new scandium extraction technologies from uranium mining by-products has strengthened Russia's position in the global supply chain. The country's focus on developing domestic manufacturing capabilities across various sectors, including aerospace, defense, and electronics, continues to drive the demand for scandium-based materials and alloys.

Scandium Market in Other Countries

The scandium market in other countries shows diverse growth patterns influenced by regional industrial development and technological advancement. Countries like Brazil, Canada, and South Korea are experiencing increased demand driven by their growing aerospace and electronics sectors. India's emerging electric vehicle market and expanding electronics manufacturing base are creating new opportunities for scandium applications. The Middle Eastern countries, particularly Saudi Arabia, are showing interest in scandium applications for their developing aerospace and defense sectors. European nations outside the major markets are witnessing growth in scandium demand, particularly in countries with strong manufacturing bases like Poland and Belgium. South American countries are gradually increasing their scandium consumption as their industrial bases expand and modernize. These emerging markets collectively contribute to the global scandium ecosystem, though their individual market shares remain relatively smaller compared to the leading countries.

Get Analysis on Important Geographic Markets

Download PDF

Scandium Industry Overview

Top Companies in Scandium Market

The scandium market is characterized by continuous product innovation and strategic expansion initiatives by key players. Companies are focusing on developing advanced scandium-based materials, particularly aluminum-scandium alloys, to meet growing demand from the aerospace and automotive sectors. Operational agility is demonstrated through vertical integration strategies, with many players expanding their capabilities across the value chain from mining to end-product manufacturing. Strategic moves include significant investments in research and development of separation and purification technologies, while geographical expansion is primarily centered on establishing production facilities in regions with abundant scandium resources. Companies are also pursuing collaborations and partnerships to strengthen their technological capabilities and market presence, particularly in emerging applications like solid oxide fuel cells and 3D printing.

Consolidated Market with Strong Regional Players

The global scandium market exhibits a partially consolidated structure dominated by both established conglomerates and specialized producers. Major players include state-owned enterprises, particularly from China, alongside international mining corporations and specialized rare earth elements processors. The market shows a distinct pattern of regional concentration, with Chinese companies holding significant production capacity, while companies from Russia, Australia, and the Philippines maintain strategic positions in specific product segments and geographical markets. The industry structure is characterized by high entry barriers due to technical expertise requirements and capital-intensive operations.

Merger and acquisition activity in the scandium market is primarily driven by vertical integration objectives and technological capability enhancement. Companies are increasingly pursuing strategic alliances and joint ventures to secure raw material supply and expand their product portfolios. The trend of consolidation is particularly evident in the development of primary scandium mining projects, where established players are partnering with exploration companies to develop new sources of supply. These strategic moves are reshaping the competitive landscape as companies seek to strengthen their market positions and achieve economies of scale.

Innovation and Supply Chain Control Drive Success

For incumbent players to maintain and expand their market share, focus on technological innovation and supply chain optimization is crucial. Companies need to invest in developing more efficient extraction and processing methods while expanding their product portfolios to serve emerging applications. Success factors include establishing long-term supply contracts with end-users, particularly in the aerospace and automotive sectors, and maintaining strong research and development capabilities. The ability to provide consistent product quality and reliable supply is becoming increasingly important as end-user industries demand higher performance standards.

New entrants and contenders in the scandium market must focus on developing niche applications and establishing strategic partnerships to gain market presence. The key to success lies in securing reliable raw material sources and developing cost-effective processing technologies. Companies need to consider regulatory compliance, particularly in environmental protection and resource conservation, as governments worldwide implement stricter regulations on rare earth elements mining and processing. The risk of substitution remains relatively low due to scandium's unique properties, but companies must continue to demonstrate the value proposition of scandium-based products to maintain market growth.

Scandium Market Leaders

-

Hunan Institute of Rare Earth Metal Materials

-

MCC Grop

-

Sunrise Energy Metals

-

Hunan Oriental Scandium Co., Ltd.

-

Henan Rongjia scandium vanadium Technology Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Scandium Market News

- January 2024: NioCorp Developments Ltd agreed with London-based Brunel University London, a leading research university focused on the global application of cast aluminum alloys, to develop innovative aluminum-scandium alloys and applications for use in the automotive sector.

- April 2023: Rio Tinto entered a binding agreement to acquire the Platina Scandium Project, a high-grade scandium resource in New South Wales, from Platina Resources Limited for USD 14 million. The project, near Condobolin in central New South Wales, comprises a long-life, high-grade scalable resource that could produce up to 40 tons per annum of scandium oxide for an estimated period of 30 years.

Scandium Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Usage in Solid Oxide Fuel Cells (SOFCS)

- 4.1.2 Increasing Demand for Aluminum-Scandium Alloys in the Aerospace and Defense Industry

-

4.2 Restraints

- 4.2.1 High Cost of Scandium

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Analysis

- 4.6 Environmental Impact Analysis

5. MARKET SEGMENTATION

-

5.1 Product Type

- 5.1.1 Oxide

- 5.1.2 Fluoride

- 5.1.3 Chloride

- 5.1.4 Nitrate

- 5.1.5 Iodide

- 5.1.6 Alloy

- 5.1.7 Carbonate and Other Product Types

-

5.2 End-user Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Solid Oxide Fuel Cells

- 5.2.3 Ceramics

- 5.2.4 Lighting

- 5.2.5 Electronics

- 5.2.6 3D Printing

- 5.2.7 Sporting Goods

- 5.2.8 Other End-user Industries

-

5.3 Geography

- 5.3.1 Production Analysis

- 5.3.1.1 China

- 5.3.1.2 Russia

- 5.3.1.3 Philippines

- 5.3.1.4 Rest of the World

- 5.3.2 Consumption Analysis

- 5.3.2.1 United States

- 5.3.2.2 China

- 5.3.2.3 Russia

- 5.3.2.4 Japan

- 5.3.2.5 Brazil

- 5.3.2.6 European Union

- 5.3.2.7 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Guangxi Maoxin Technology Co. Ltd

- 6.4.2 Henan Rongjia Scandium Vanadium Technology Co. Ltd

- 6.4.3 Huizhou Top Metal Materials Co. Ltd

- 6.4.4 Hunan Rare Earth Metal Materials Research Institute Co. Ltd

- 6.4.5 Hunan Oriental Scandium Co. Ltd

- 6.4.6 JSC Dalur

- 6.4.7 MCC Group

- 6.4.8 NioCorp Development Ltd

- 6.4.9 Rio Tinto

- 6.4.10 Rusal

- 6.4.11 Scandium International Mining Corporation

- 6.4.12 Stanford Advanced Materials

- 6.4.13 Sumitomo Metal Mining Co. Ltd (Taganito HPAL nickel Corp.)

- 6.4.14 Sunrise Energy Metals Limited

- 6.4.15 Treibacher Industrie AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential Applications in the Automotive industry

- 7.2 Growing Technology for Storing Energy

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Scandium Industry Segmentation

Scandium, with the chemical symbol Sc and atomic number 21, is a silver-white transitional metal categorized as a rare-earth element. It possesses distinctive traits such as lightness, a high melting point, and a small ionic radius. Due to its small ion size, it seldom forms concentrations exceeding 100 ppm naturally, as it doesn't readily bond with common ore-forming anions. Notably, its main applications include solid oxide fuel cells (SOFCs) and aluminum-scandium alloys, enhancing strength and performance, particularly due to its fine grain refinement, which reduces hot cracking in welds and improves fatigue behavior.

The scandium market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into oxide, fluoride, chloride, nitrate, iodide, alloy, carbonate, and other product types. By end-user industry, the market is segmented into aerospace and defense, solid oxide fuel cells, ceramics, lighting, electronics, 3D printing, sporting goods, and other end-user industries. The report also covers the market size and forecasts for scandium in 6 countries across major regions. For each segment, market sizing and forecasts were made based on revenue (USD million).

| Product Type | Oxide | ||

| Fluoride | |||

| Chloride | |||

| Nitrate | |||

| Iodide | |||

| Alloy | |||

| Carbonate and Other Product Types | |||

| End-user Industry | Aerospace and Defense | ||

| Solid Oxide Fuel Cells | |||

| Ceramics | |||

| Lighting | |||

| Electronics | |||

| 3D Printing | |||

| Sporting Goods | |||

| Other End-user Industries | |||

| Geography | Production Analysis | China | |

| Russia | |||

| Philippines | |||

| Rest of the World | |||

| Consumption Analysis | United States | ||

| China | |||

| Russia | |||

| Japan | |||

| Brazil | |||

| European Union | |||

| Rest of the World | |||

Need A Different Region or Segment?

Customize Now

Scandium Market Research FAQs

How big is the Scandium Market?

The Scandium Market size is expected to reach USD 0.77 billion in 2025 and grow at a CAGR of 14.70% to reach USD 1.53 billion by 2030.

What is the current Scandium Market size?

In 2025, the Scandium Market size is expected to reach USD 0.77 billion.

Who are the key players in Scandium Market?

Hunan Institute of Rare Earth Metal Materials, MCC Grop, Sunrise Energy Metals, Hunan Oriental Scandium Co., Ltd. and Henan Rongjia scandium vanadium Technology Co., Ltd are the major companies operating in the Scandium Market.

What years does this Scandium Market cover, and what was the market size in 2024?

In 2024, the Scandium Market size was estimated at USD 0.66 billion. The report covers the Scandium Market historical market size for years: 2024. The report also forecasts the Scandium Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Scandium Market Research

Mordor Intelligence offers a comprehensive analysis of the scandium and rare earth elements markets. We leverage decades of expertise in researching critical minerals and strategic metals. Our extensive coverage includes the entire SC industry ecosystem. This ranges from scandium mining operations to the production of scandium oxide and scandium compounds. The report provides detailed insights into the evolving landscape of transition metals and their industrial applications. We particularly focus on the growing market value of rare earth metals.

Stakeholders across the value chain can access our detailed analysis through an easy-to-download report PDF. This report offers strategic insights into aluminum scandium alloy applications in aerospace alloy manufacturing and scandium lighting technologies. The comprehensive SC market report examines emerging opportunities in the rare metals market. It also provides actionable intelligence on scandium products and their industrial applications. Our SC annual report delivers valuable data on scandium minerals and market dynamics. This supports informed decision-making for industry participants and investors interested in the transition metals market.