Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

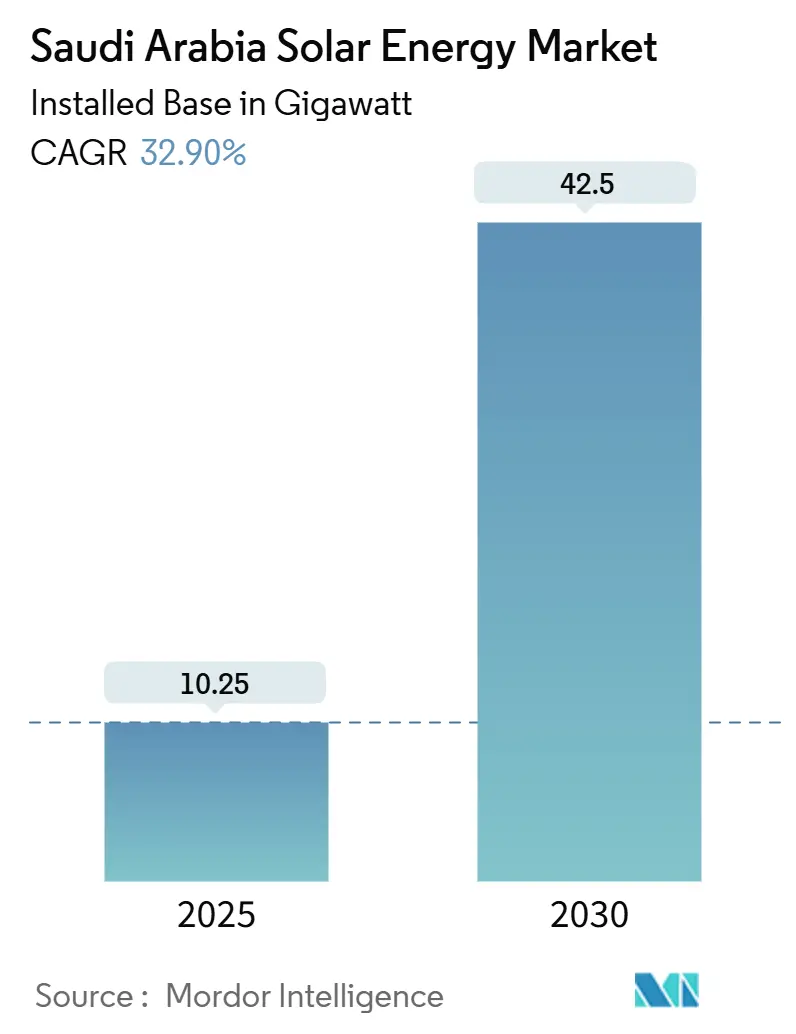

| Market Volume (2025) | 10.25 gigawatt |

| Market Volume (2030) | 42.5 gigawatt |

| Growth Rate (2025 - 2030) | 32.90% CAGR |

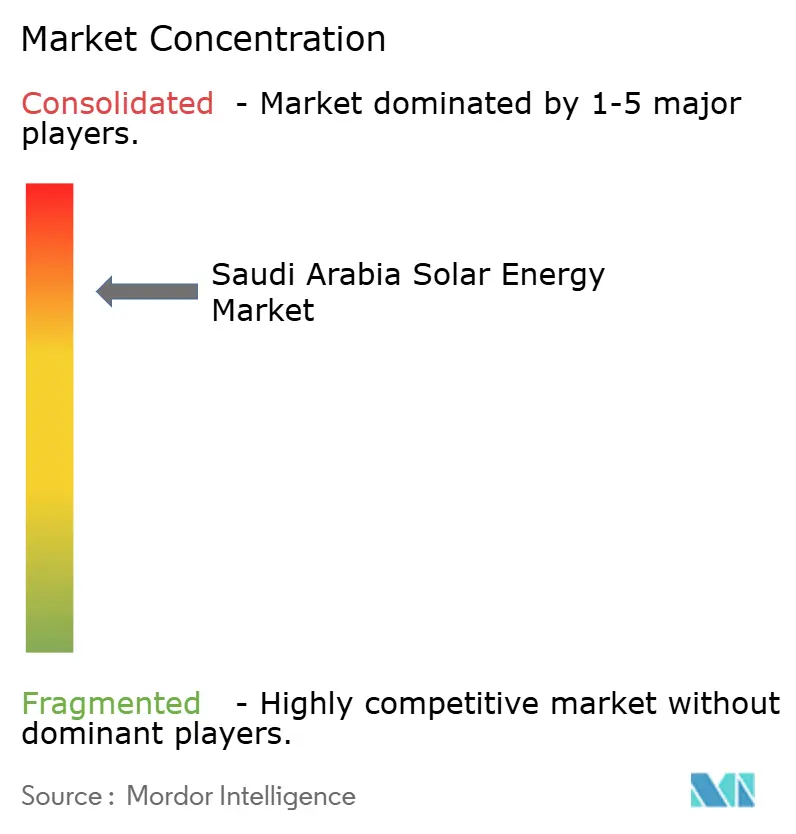

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Solar Energy Market Analysis by Mordor Intelligence

The Saudi Arabia Solar Energy Market size in terms of installed base is expected to grow from 10.25 gigawatt in 2025 to 42.5 gigawatt by 2030, at a CAGR of 32.90% during the forecast period (2025-2030).

Demand for clean electricity, Vision 2030 mandates, and record-low auction tariffs keep investor momentum high, while streamlined REPDO tenders slash development risk and financing costs. Utility procurements now embed battery storage and local-content thresholds, aligning climate goals with industrial policy and driving domestic manufacturing. Abundant solar irradiance and available desert land sustain world-leading capacity factors that anchor competitive pricing. At the same time, rising commercial and industrial uptake signals a pivot from purely utility-scale builds toward diverse distributed applications, reinforcing a dynamic, multisegment market framework.

Key Report Takeaways

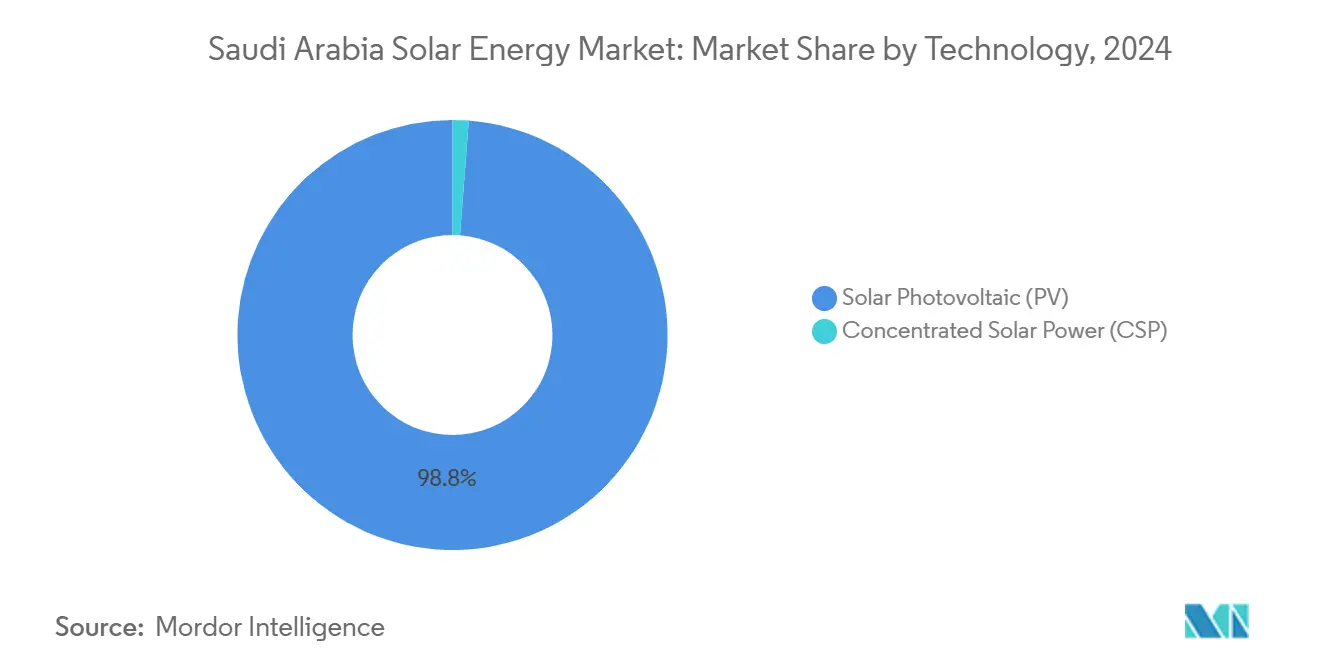

- By technology, solar photovoltaics (PV) led with 98.8% of the Saudi arabia solar energy market share in 2024, while concentrated solar power (CSP) is projected to expand at a 46.5% CAGR to 2030, the fastest among all segments.

- By grid type, on-grid installations held a 90.2% share of the Saudi arabia solar energy market in 2024, and off-grid systems are advancing at a 37.8% CAGR through 2030.

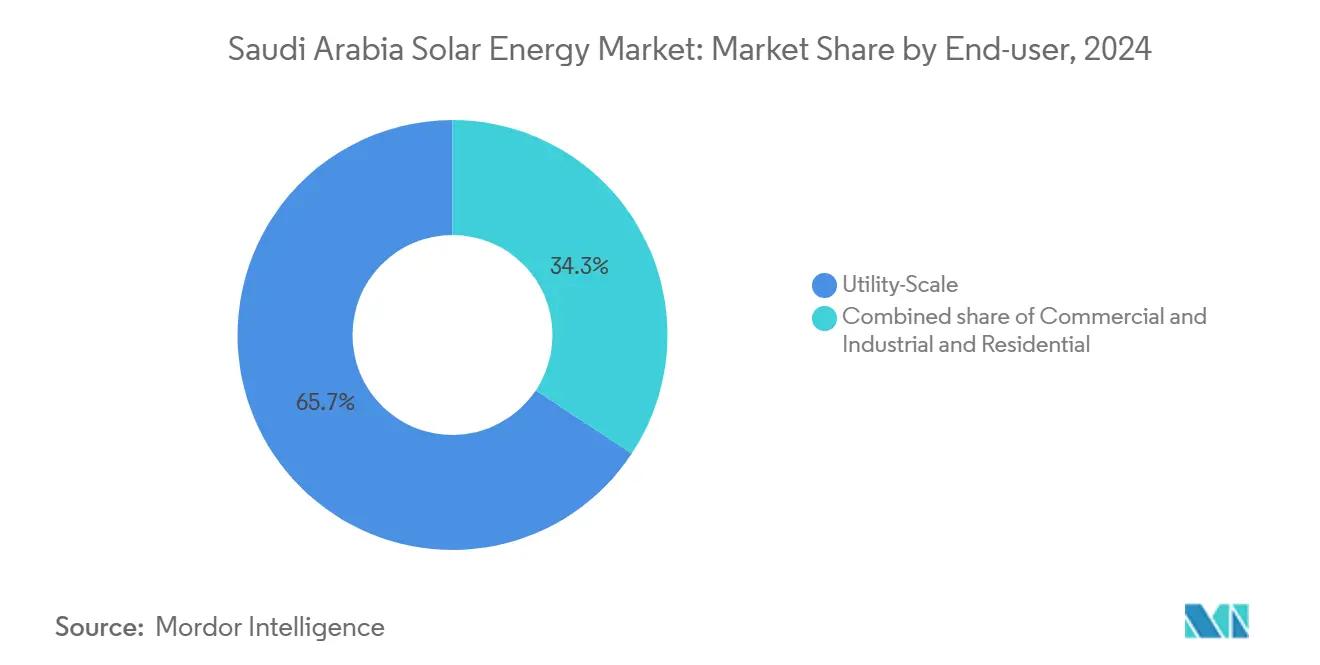

- By end-user, utility-scale projects accounted for 65.7% of the Saudi arabia solar energy market size in 2024, while commercial and industrial installations are forecast to expand at a 41.1% CAGR to 2030.

Saudi Arabia Solar Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 National Renewable Energy Program targets | +8.50% | Northern and Eastern provinces | Long term (≥ 4 years) |

| Declining levelized cost of solar PV | +6.20% | High-irradiance zones nationwide | Medium term (2-4 years) |

| REPDO utility-scale tender pipeline | +7.10% | Grid-connected areas nationwide | Medium term (2-4 years) |

| Abundant irradiance and land availability | +4.80% | Northern Border and Eastern provinces | Long term (≥ 4 years) |

| Localization incentives for PV manufacturing | +3.40% | Riyadh and Eastern manufacturing hubs | Long term (≥ 4 years) |

| Green-hydrogen export ambitions | +2.80% | NEOM and Red Sea corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Vision 2030 National Renewable Energy Program Targets Drive Systematic Deployment

The government targets 58.7 GW of renewables by 2030, equal to roughly half of expected installed capacity, which reshapes the country's generation portfolio from hydrocarbons to clean power. REPDO's multi-round auctions provide developers with predictable timelines, uniform contract structures, and escalating local-content rules, which increased from 15% to 35% between Round 1 and Round 6. Over 3.3 GW was awarded in the latest rounds at an average tariff of 1.97¢/kWh, underscoring the program's credibility. The tender cadence signals to investors that additional land banks, transmission upgrades, and financing windows will remain in sync. Predictability reduces capital costs and underpins a bankable project pipeline, ensuring that the Saudi Arabia solar energy market continues attracting global and regional developers.

Declining Levelized Cost Creates Grid Parity Advantage

Recent winning bids dipped to 1.67 c/kWh, surpassing natural gas estimates by more than 50% once LNG export opportunity costs are factored in. Module pricing benefits from local fabrication agreements with JinkoSolar and TCL Zhonghuan that eliminate import duties and freight charges. Superior average irradiation of 2,200 kWh/m²/year delivers capacity factors above 28%, enabling fewer panels to deliver more energy and improving project economics.(1) King Abdullah University of Science and Technology, “Solar Atlas for the Kingdom,” kaust.edu.sa Bifacial modules and single-axis trackers extract incremental yield, while risk-based O&M contracts keep downtime low. Combined, these factors lock in grid-parity or better economics, helping the Saudi Arabia solar energy market outcompete conventional assets.

REPDO Tender Pipeline Ensures Market Predictability

Announced tenders cover more than 20 GW through 2030, offering transparency unmatched in many emerging markets. Standardized PPAs, indexed escalation clauses, and new performance-based incentives for grid services make revenue streams highly forecastable. Hybrid solar-storage obligations in upcoming rounds build a procurement bridge between merchant renewables and dispatchable capacity. Local-content uplifts embedded in bid scoring further stimulate supply-chain formation, securing module, tracker, and inverter plants in Riyadh and Eastern Province. These design choices create a virtuous cycle where each auction round tightens pricing while boosting domestic value addition, cementing the Saudi Arabia solar energy market as a regional benchmark for structured renewables growth.

Abundant Solar Resources Enable Competitive Advantage

Northern desert zones post direct normal irradiance of 2,500 kWh/m²/year, surpassing California and Spain by up to 30%. Low land-lease rates and minimal competing land uses limit acquisition friction. Dense networks of pyranometers and satellite-based forecasting reduce interannual yield uncertainty, improving bankability. Multi-gigawatt clusters enable shared infrastructure, such as 380 kV substations and operations centers, thereby reducing per-megawatt balance-of-plant costs. High irradiation also supports emerging CSP designs with longer thermal storage, adding firm capacity without fossil back-up. Together, these resource advantages keep levelized costs trending downward, reinforcing the competitive edge of the Saudi Arabia solar energy market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid connection bottlenecks in remote areas | −2.1% | Northern Border and Empty Quarter | Medium term (2-4 years) |

| High upfront cost of CSP versus PV | −1.8% | Nationwide | Short term (≤ 2 years) |

| Water scarcity for panel cleaning | −1.3% | Central and northern deserts | Short term (≤ 2 years) |

| Import dependence for key components | −1.5% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Connection Bottlenecks Constrain Remote Development

Legacy transmission grids radiate from coastal gas-fired hubs toward load centers, leaving northern deserts underserved.(2)Saudi Electricity Company, “Annual Report 2024,” sec.com.sa High-capacity 380 kV lines and flexible AC/DC converters are budgeted, yet construction timelines extend up to five years, outpacing PV build schedules. Interim battery tenders totaling 8 GWh mitigate imbalance risk but cannot substitute for bulk transmission. Developers front-load interconnection studies, sometimes relocating projects nearer to substations, which shifts optimal irradiation trade-offs. Until grid corridors catch up, the Saudi Arabia solar energy market must juggle resource quality against infrastructure readiness.

High Upfront Capital Requirements Limit CSP Deployment

While CSP delivers 12-15 h of stored energy, costs remain USD 3,500–5,000/kW, quadruple utility PV levels. Complex molten-salt loops and specialized turbines need bespoke engineering and higher contingency reserves. Lenders demand stricter technical due diligence, elongating the financial close. Hybrid PV-CSP configurations have slightly lower weighted costs but do not fully bridge the gap. Consequently, CSP is restricted to projects with premium revenues for firm power, capping near-term volume and curbing its share of the Saudi Arabia solar energy market.

Segment Analysis

By Technology: PV Commands Volume While CSP Gains Strategic Footholds

Solar photovoltaic installations held 98.8% of the Saudi Arabian solar energy market share in 2024, reflecting unmatched cost advantages and modular scalability.(3) International Renewable Energy Agency, “Renewable Capacity Statistics 2024,” irena.org Large desert tracts enable gigawatt-scale PV clusters, and single-axis trackers plus bifacial modules push capacity factors past 28%. Falling module prices and standardized EPC contracts drive levelized costs below 2 c/kWh, entrenching PV as the workhorse of new renewable capacity. As more local factories ramp up, project developers anticipate steadier pricing and shorter lead times, deepening PV’s dominance within the Saudi Arabia solar energy market.

Concentrated solar power, though small in absolute volume, is projected to book a 46.5% CAGR during 2025–2030. Storage-equipped CSPs fill late-evening demand and provide inertia, an attribute prized as variable PV penetrates deeper into the grid.(4)SolarPower Europe, “CSP Cost Outlook 2025,” solarpowereurope.org Thermal storage up to 15 h allows dispatch beyond sunset, reducing reliance on gas peakers. NEOM, industrial clusters, and remote desalination plants value this dispatchable green heat. As molten-salt technologies and heliostat automation reduce capital expenditures (capex), CSP’s addressable niche widens, ensuring it remains a strategic complement within the Saudi Arabia solar energy market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grid Type: On-Grid Dominates Yet Off-Grid Surges for Remote Demand

On-grid assets comprised 90.2% of installed capacity in 2024, underpinning the centralized generation strategy and benefiting from the Saudi Electricity Company’s bankable PPAs. Gigawatt-sized parks plug into 380 kV backbone lines and benefit from economies of scale in operations and maintenance (O&M), land use, and financing. Robust regulatory oversight enhances certainty, reinforcing the on-grid segment’s central role within the Saudi Arabia solar energy market.

Off-grid systems, although starting from a small base, are projected to register a 37.8% CAGR to 2030, driven by giga-projects such as NEOM and large mines located outside main grid corridors. Microgrids combine PV with batteries and sometimes small wind turbines, slashing diesel costs and curbing emissions. Modular storage containers, fast-tracking EPC, and simplified land permitting make off-grid attractive for time-sensitive developments. As the logistics and remote tourism economies grow, the off-grid share of the Saudi Arabia solar energy market is expected to accelerate, despite its current minor footprint.

By End-User: Utility-Scale Leads While C&I Demand Gains Momentum

Utility-scale projects accounted for 65.7% of the Saudi Arabia solar energy market size in 2024, secured through centrally procured bids ranging from 50 MW to 2 GW. Streamlined environmental reviews and competitive auction designs keep build costs down, anchoring national decarbonization plans. These installations directly connect to high-voltage networks, supplying bulk power that supports peak summer loads.

Commercial and industrial users are forecast to posta 41.1% CAGR, reflecting corporate cost-saving drives and sustainability pledges. Steel, cement, and petrochemical operators benefit from on-site PV arrays linked through net-metering or virtual PPAs. Recent policy tweaks offering bankable contracts and faster interconnection approvals unlock rooftop and carport deployment. While residential uptake remains modest due to subsidized tariffs, pilot programs in smart cities indicate latent potential, adding diversity to the Saudi Arabia solar energy market over time.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Northern Border and Eastern provinces capture the bulk of large-scale awards as their irradiance surpasses 2,500 kWh/m²/year and land acquisition is straightforward. Mega-parks, such as the 2 GW Al-Sadawi cluster, co-locate shared substations, cutting grid-tie expenses and boosting overall capacity factors. These regions anchor the national push toward 58.7 GW of renewables, reinforcing the primacy of resource-rich desert corridors within the broader Saudi Arabia solar energy market.

Western provinces are leveraging solar energy to power tourism and desalination. The Red Sea Development Company commissioned a 400 MW solar microgrid paired with 1.3 GWh batteries, supplying 100% renewable power to resorts and airports.(5)Red Sea Development Company, “Solar Microgrid Commissioning News,” redseadevelopmentcompany.com NEOM’s northwest location will stack more than 4 GW of PV for hydrogen export, adding strategic depth to the Saudi Arabia solar energy market by coupling electricity with commodity exports.

Distributed solar atop factories and logistics hubs combine energy savings with ESG branding. As electricity demand increases with the development of new data centers and advanced industries, central provinces will integrate rooftop, carport, and ground-mount systems, completing a diversified geographic tapestry for the Saudi Arabia solar energy market.

Competitive Landscape

ACWA Power leads with 17.8 GW of contracted capacity across 14 projects, leveraging backing from the Public Investment Fund and its deep project-finance expertise to maintain a first-mover edge. The developer’s portfolio spans PV, CSP, and hybrid configurations, underpinning technology diversification. Partnerships with Saudi Aramco on integrated solar-hydrogen complexes extend its influence beyond power sales, anchoring new value chains inside the Saudi Arabian solar energy market.

Foreign IPPs, such as Masdar, EDF Renewables, and TotalEnergies, secure positions through joint ventures that combine global engineering expertise with local execution networks. Chinese OEMs JinkoSolar, LONGi, and Trina Solar establish factories in Riyadh and the Eastern Province, meeting rising local-content thresholds while seeding after-sales service centers. These moves intensify competition, driving hardware costs lower and accelerating technology transfer across the Saudi Arabia solar energy market.

Technology innovation now defines differentiation. Developers deploy AI-enabled performance monitoring, drone-based inspections, and high-efficiency bifacial modules to squeeze additional yield. As bids inch below 2 c/kWh, O&M optimization and ancillary service offerings around batteries and grid support become new revenue levers. This push for operational excellence underscores a maturing phase for the Saudi Arabian solar energy market, where cost leadership must coexist with technical sophistication.

Saudi Arabia Solar Energy Industry Leaders

-

Alfanar Group

-

Abu Dhabi Future Energy Company (Masdar)

-

EDF Renewables

-

Saudi Electricity Company

-

ACWA Power Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: In a historic move for the Middle East, ACWA Power clinched a USD 3.2 billion financing deal from a consortium of international banks. The funds are earmarked for three ambitious utility-scale solar projects: Haden (1.5 GW), Muwayh (2 GW), and Al Khushaybi (2 GW).

- December 2024: JinkoSolar, in collaboration with the Public Investment Fund, has unveiled a USD 1.2 billion joint venture. The duo aims to establish a 10 GW solar cell and module manufacturing facility in Riyadh, with production scheduled to commence in 2026. Notably, the facility is poised to channel 70% of its output to regional markets.

- November 2024: TCL Zhonghuan has commenced construction of a USD 2.8 billion integrated solar manufacturing complex in the Eastern Province, featuring 20 GW of ingot and wafer production capacity with advanced monocrystalline silicon technology.

- October 2024: The Red Sea Development Company commissioned a 400 MW solar microgrid with 1.3 GWh of battery storage, achieving a 100% renewable energy supply for Phase 1 of its tourism infrastructure and establishing a blueprint for sustainable destination development.

- September 2024: Saudi Electricity Company has awarded a USD 1.5 billion contract for eight 8 GWh battery energy storage systems across six locations, supporting the grid integration of renewable energy and enhancing system stability.

Saudi Arabia Solar Energy Market Report Scope

Solar energy is a type of renewable energy where solar panels are used to generate electricity. Solar panels deployed on rooftops or mounted on the grounds are utilized effectively by energy consumers.

Saudi Arabia's solar energy market is segmented by type into solar photovoltaic (PV) and concentrated solar energy (CSP). For each segment, the market sizing and forecasts have been done based on the installed capacity (MW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is solar capacity growing in Saudi Arabia?

Installed capacity is forecast to expand from 10.25 GW in 2025 to 42.50 GW by 2030, reflecting a 32.9% CAGR.

What share of installations use photovoltaic versus CSP technology?

Solar photovoltaic accounts for 98.8% of total capacity, while concentrated solar power holds a niche share but posts the fastest-growing CAGR at 46.5%.

Which regions attract the largest utility-scale solar parks?

Northern Border and Eastern provinces host most large parks due to superior irradiance and available land, supported by 380 kV grid corridors.

Why are off-grid solar systems gaining traction?

Remote giga-projects and industrial sites value off-grid microgrids for cost savings and fast deployment, driving a 37.8% CAGR for the segment.

Who is the leading developer in the country?

ACWA Power leads with 17.8 GW contracted across 14 projects, backed by the Public Investment Fund and strategic ties with Saudi Aramco.

What role does local manufacturing play in cost reduction?

New module and wafer plants in Riyadh and Eastern Province shorten supply chains and meet local-content rules, contributing to record-low auction tariffs under 2 c/kWh.

Page last updated on: