Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

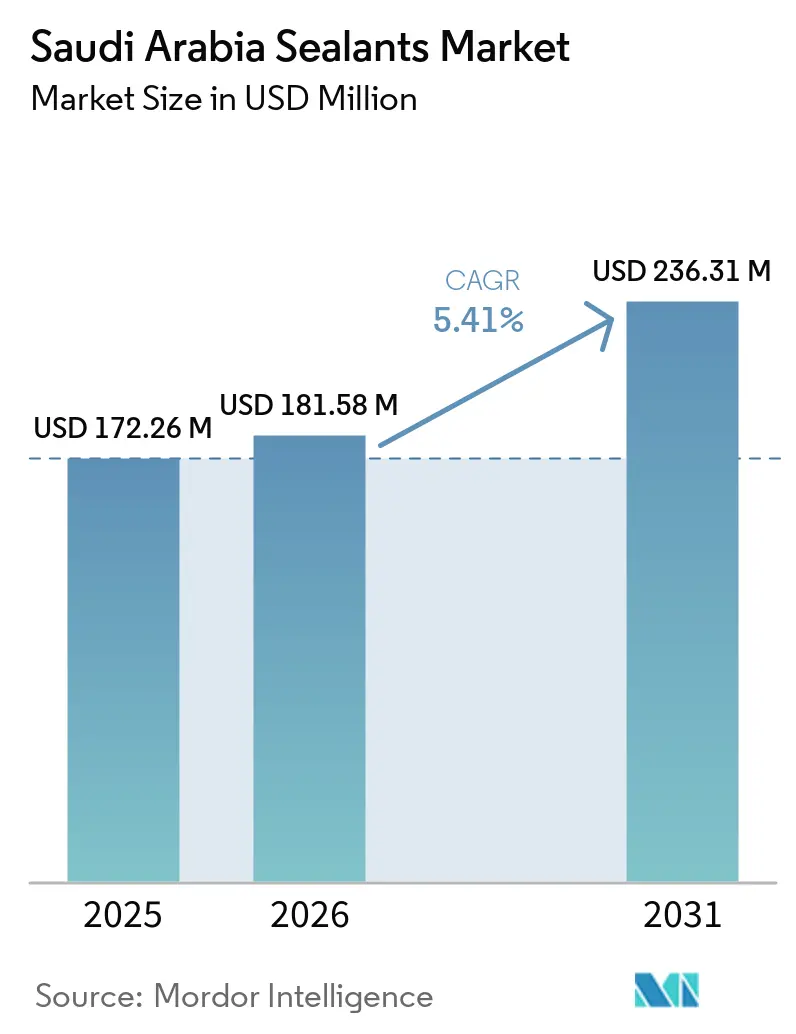

| Base Year Market Size (2025) | USD 172.26 Million |

| Market Size (2026) | USD 181.58 Million |

| Market Size (2031) | USD 236.31 Million |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Sealants Market Analysis by Mordor Intelligence

The Saudi Arabia Sealants Market size was valued at USD 172.26 million in 2025 and is estimated to grow from USD 181.58 million in 2026 to reach USD 236.31 million by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). Uninterrupted tender releases under Vision 2030 continue to channel giga-project demand toward locally produced, low-VOC chemistries that comply with Saudi Standards, Metrology and Quality Organization (SASO) rules, and the Saudi Green Building Code. Global suppliers have responded by buying Saudi production assets, speeding up approval cycles, and embedding technical-service teams next to project sites. The Saudi Arabia sealants market is also benefiting from accelerated hospital construction, rising automotive localization, and pilot use of 3D robotic extrusion that cuts material waste. Competition is shifting from pure price to a mix of in-Kingdom total value add (IKTVA) credits, reformulation speed, and on-site training capability, giving vertically integrated multinationals a measurable edge.

Key Report Takeaways

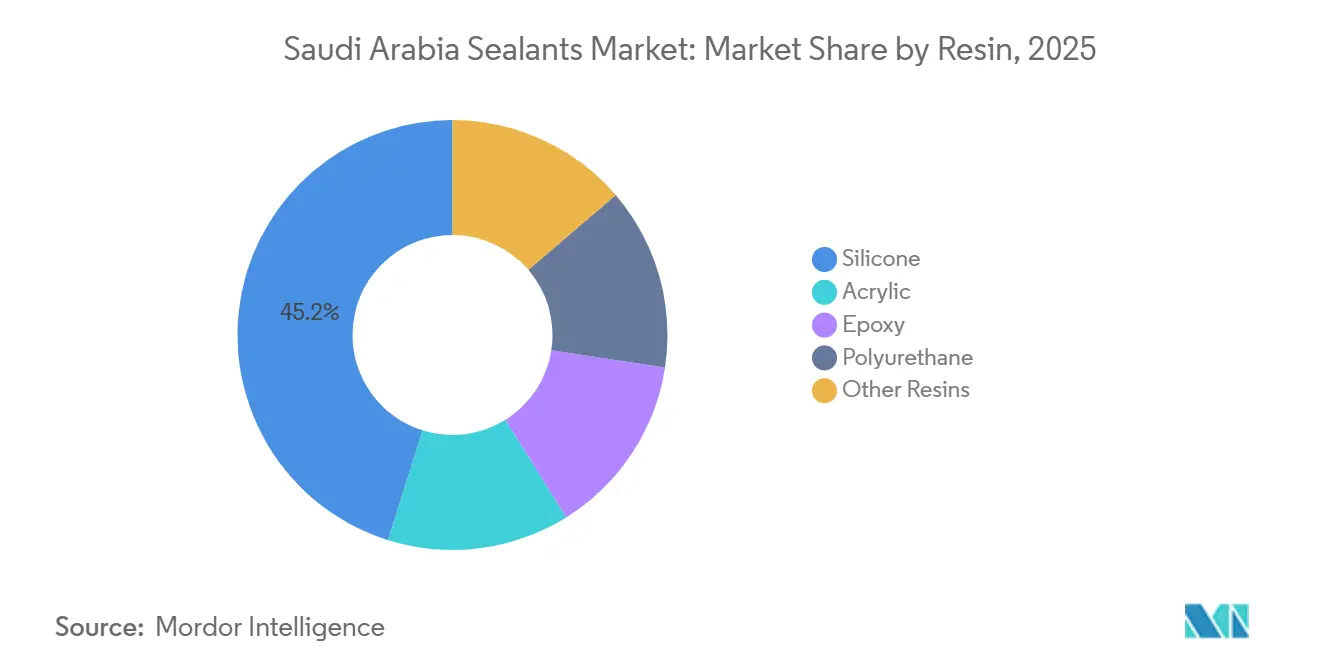

- By resin, silicone captured 45.16% of the Saudi Arabia Sealants market share in 2025, while acrylic resins are projected to expand at a 5.83% CAGR during the forecast period (2026-2031).

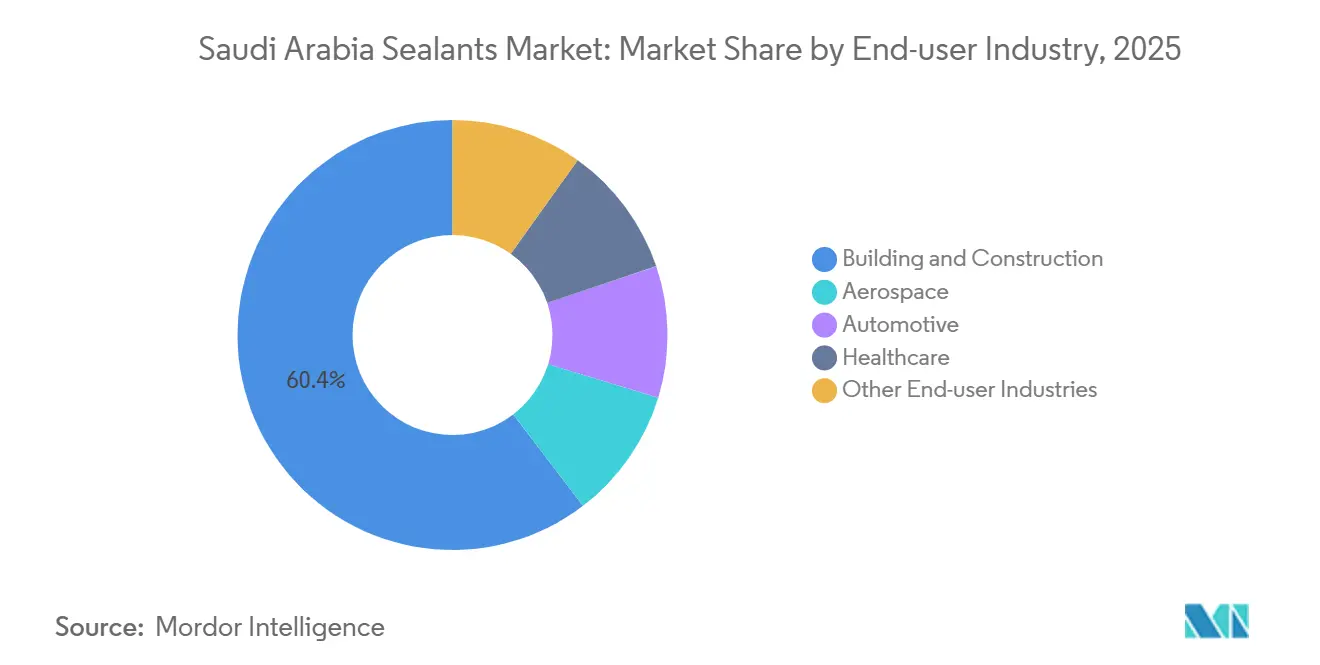

- By end-user industry, building and construction held 60.38% share of the Saudi Arabia Sealants market size in 2025; healthcare is advancing at a 6.12% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising automotive aftermarket demand for silicone gasket sealants | +0.8% | National, concentrated in Eastern Province industrial clusters and Riyadh | Medium term (2-4 years) |

| Growth in domestic aerospace MRO segment | +0.6% | Western Province (Jeddah MRO village), Riyadh King Khalid International Airport | Long term (≥ 4 years) |

| Healthcare-facility expansion spurring medical-grade sealant use | +1.1% | National, with early gains in Jeddah, Riyadh, Dammam | Short term (≤ 2 years) |

| Mandated low-VOC sealants in public projects (2027 onwards) | +1.2% | National, enforced via SASO and SBC 1001 compliance | Medium term (2-4 years) |

| On-site 3D-printed sealing solutions reduce material waste | +0.5% | Pilot deployments in NEOM, Red Sea Project modular construction zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Automotive Aftermarket Demand for Silicone Gasket Sealants

Extreme operating temperatures in Saudi Arabia shorten service intervals for traditional gaskets, so independent workshops have pivoted to high-temperature silicone that withstands more than 150°C and resists synthetic oils[1]Henkel, “Polybit Polycrete 3D Datasheet,” henkel.com. Dongfeng Motor’s 2025 agreement with Universal Motors Agencies to assemble 10,000 vehicles locally multiplies Original Equipment Manufacturer (OEM)-grade sealant demand that must now be sourced inside the Kingdom. Electric-vehicle adoption, although nascent, creates a secondary pull for thermally conductive silicones essential for battery-pack safety. Yet the fragmented aftermarket lacks standardized applicator certification, leaving joint quality inconsistent and elevating warranty risk for brands selling in the Saudi Arabia Sealants market.

Healthcare-Facility Expansion Spurring Medical-Grade Sealant Use

Planned hospital capacity additions necessitate medical-grade silicone and silane-modified hybrids that survive repeated autoclave cycles at 134°C and meet ISO 10993 standards. Turnkey public-private partnerships transfer material selection to international design-build firms that default to pre-qualified global brands, narrowing the supplier field in the Saudi Arabia sealants market. Smart-hospital blueprints specify non-outgassing sealants so that volatile emissions do not interfere with air-quality sensors, adding a new compliance layer that favors companies with in-Kingdom R&D.

Mandated Low-VOC Sealants in Public Projects

Saudi Standards, Metrology and Quality Organization (SASO) and SBC 1001 are converging on a 2027 VOC (Volatile Organic Compound) ceiling similar to California Rule 1168, and submittals must be uploaded to the SABER digital platform[2]SASO, “Saudi Green Building Code SBC 1001,” saso.gov.sa. BASF and Sika are first movers, having launched Baxxodur EC 151, an epoxy hardener that cuts VOCs (Volatile Organic Compounds) by 90% relative to legacy systems. Contractors adopting water-based acrylics avoid solvent-handling risks, but dusty substrates common on fast-track Saudi sites still require primers, demanding extra training for installers in the Saudi Arabia sealants market.

On-Site 3D-Printed Sealing Solutions Reduce Material Waste

Henkel’s Polybit Polycrete 3D and Sika’s Sikacrete-752 3D robots deposit continuous beads onto prefab panels, eliminating cartridges and shrinking material waste by 25%. Early pilots at NEOM’s modular housing yards recorded 40% shorter installation cycles, alleviating the skilled-labor bottleneck. Adoption hurdles center on climate-controlled staging and the absence of SASO print-joint test standards, but suppliers that integrate BIM data into mobile printers are poised to reshape the Saudi Arabia sealants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from mechanical fastening alternatives | -0.6% | National, particularly in industrial and infrastructure segments | Medium term (2-4 years) |

| Lengthy SASO certification for novel bio-based sealants | -0.9% | National, affecting all suppliers seeking to introduce sustainable formulations | Short term (≤ 2 years) |

| Skilled-applicator shortage affecting joint integrity | -1.3% | National, acute in mega-project zones (NEOM, Red Sea, Qiddiya) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy SASO Certification for Novel Bio-Based Sealants

Proving equivalence to petrochemical benchmarks across 15 performance criteria can take up to 24 months and cost USD 200,000 per formulation. That pace conflicts with Vision 2030 circular-economy milestones and discourages international suppliers from deploying plant-derived polyurethanes, slowing the greening of the Saudi Arabia sealants market. Early engagement in Gulf Standardization Organization working groups remains the lone fast-track option.

Skilled-Applicator Shortage Affecting Joint Integrity

Only 8% of Technical and Vocational Training Corporation graduates enter craft roles, leaving contractors dependent on a shrinking expatriate labor pool. Poor bead tooling and surface preparation drive 40% of premature joint failures, yet warranty claims still fall on manufacturers, inflating their after-sales costs within the Saudi Arabia sealants market. Training pacts such as Nesma & Partners’ 2025 agreement to certify 500 applicators per year are positive but insufficient against giga-project needs that exceed 2,000 applicators for NEOM alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Silicone Stability Underpins Acrylic Momentum

Silicone resins led the Saudi Arabia sealants market with a 45.16% share in 2025, owing to elasticity retention after day-night temperature swings that can top 70°C on façade surfaces. Acrylics, though smaller, are rising at a 5.83% CAGR during the forecast period (2026-2031) on the back of water-based, low-odor benefits that align with the 2027 low-VOC mandate. Hybrid polyurethane-acrylic launches such as MC-FLEX PU 22 shorten SASO approval by leveraging existing polyurethane data, encouraging mid-tier entrants. Geography shapes mix: Jeddah’s marine climate skews toward silicones, whereas Riyadh’s green-building drive tilts projects to acrylics. Suppliers that align product portfolios with regional differences are improving bid-win ratios on mega-project tenders.

Epoxies occupy a niche for structural anchoring because of their high compressive strength, but UV brittleness limits façade use. Polyurethanes dominate railway and fuel-exposed infrastructure, validated by the 176 km Riyadh Metro. Legacy polysulfide and butyl specifications persist in certain waterproofing applications but are ceding ground to silicone-polyurethane hybrids that combine weatherability and adhesion. The evolving mix confirms that the Saudi Arabia sealants market size expansion includes not only volume growth but also an upgrade toward higher-margin chemistries.

By End-User Industry: Construction Still Commands, Healthcare Surges

Building and construction absorbed 60.38% of 2025 demand as Vision 2030 pumped contracts into NEOM, Red Sea, and Qiddiya. Healthcare is the fastest-growing end-user, clocking a 6.12% CAGR during the forecast period (2026-2031) as hospital bed targets and turnkey PPP models funnel medical-grade demand to certified suppliers. Automotive assembly benefits from localization mandates that specify OEM-grade silicones, while the aerospace Maintenance, Repair, and Overhaul (MRO) corridor around Jeddah’s Saudi Aerospace Engineering Industries (SAEI) village needs fuel-resistant, fire-retardant sealants certified under Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) rules.

Developers are bundling sealant warranties with installation in a shift that privileges suppliers offering on-site technical service, reshaping share capture in the Saudi Arabia sealants market. Aerospace demand, although lower in volume, commands premium pricing because of regulatory overhead. Electric-vehicle battery packs introduce high-value thermally conductive silicones, but volumes remain constrained until the EV penetration curve steepens. Suppliers diversifying into healthcare and aerospace today lay a defensive moat against post-2030 construction tapering.

Geography Analysis

The Western Province, driven by port expansion, Red Sea luxury resorts, and the SAEI MRO complex, contributes most of the national sealant volume, favoring salt-fog-resistant silicone chemistries. The Central Region around Riyadh supplies the second most of the demand through mixed-use mega-projects, Riyadh Metro, and heritage revitalization that increasingly specify low-VOC acrylics for green-building awards. Eastern Province industrial clusters consume high-temperature silicones and chemical-resistant polyurethanes across petrochemical and desalination plants.

NEOM’s Tabuk zone is the fastest-growing micro-market as suppliers like MAPEI establish local plants, trimming delivery times from ten days to same day. Sustainability rules at Red Sea Project drive adoption of bulk-dispensed systems, while Qiddiya’s entertainment hub necessitates color-stable silicone-hybrids that survive 50°C swings. Smaller, specialized pockets exist: phosphate mines along the Northern Border need acid-resistant sealants, and the Southern cold-chain build-out specifies food-grade silicones. Suppliers fielding mobile technical teams to these remote projects are winning long-term service bundles, helping to tilt the Saudi Arabia sealants market share their way.

Competitive Landscape

The Saudi Arabia Sealants market is moderately consolidated. Regulatory engagement is a new moat: companies embedded in SASO working groups can shape bio-based test standards, whereas laggards face 24-month approvals. By 2030, the landscape will likely split into a premium, R&D-rich tier serving mega-projects and a commoditized tier filling low-spec residential demand.

Saudi Arabia Sealants Industry Leaders

Dow

Henkel AG & Co. KGaA

Sika AG

3M

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Silstar, the exclusive agent and distributor for Elkem's silicone products across Central Europe, the Middle East, and Africa, teamed up with Saudi Multichem to create the inaugural locally integrated specialty silicone supply chain in Saudi Arabia. This move is poised to boost the country's silicone sealant market.

- October 2025: Siway introduced its SV-888 weatherproof sealant at Big 5 Construct Saudi. It is designed for high-performance and durable glass-aluminum curtain walls in harsh, high-movement environments, offering a joint displacement capacity of ±50%.

Saudi Arabia Sealants Market Report Scope

Sealants, flexible and paste-like, fill gaps, joints, and cracks between surfaces, effectively blocking air, water, moisture, and dust. Widely utilized in aerospace, construction, automotive, and healthcare, sealants protect joints. Unlike adhesives, sealants focus on providing water resistance and sealing, rather than structural bonding.

The Saudi Arabia Sealants market report is segmented by resin (acrylic, epoxy, polyurethane, silicone, and other resins) and end-user industry (aerospace, automotive, building and construction, healthcare, and other end-user industries). The market size and forecasts are provided in terms of value (USD).

By Resin

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms