Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

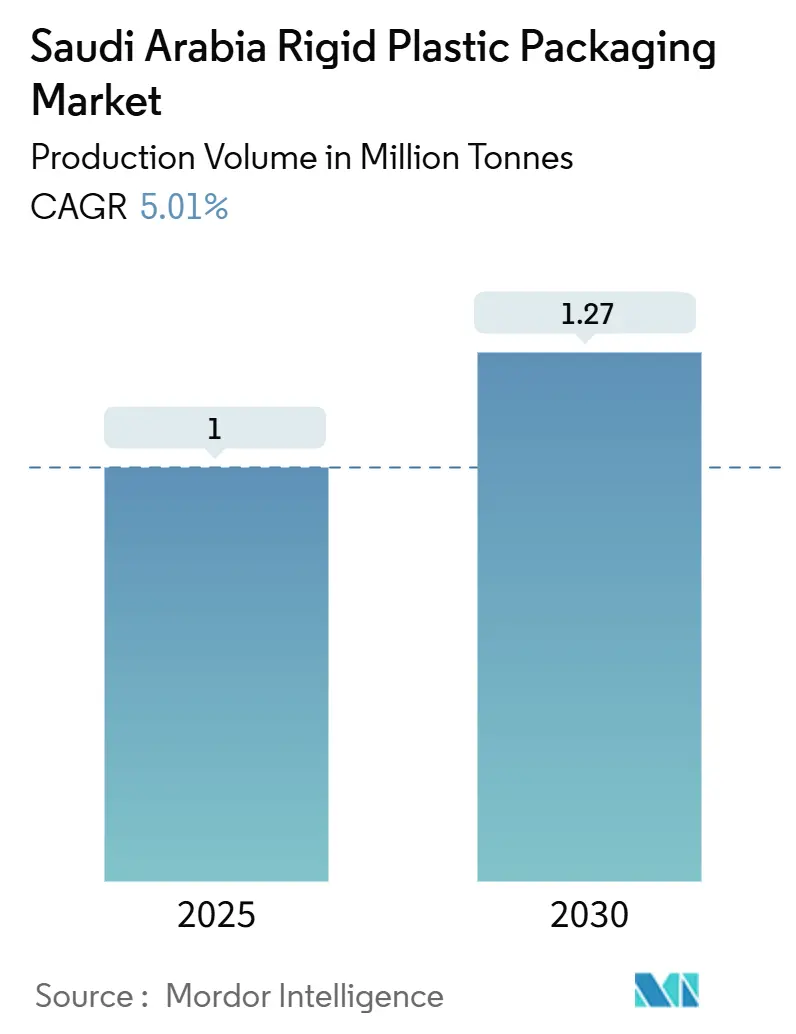

| Market Volume (2025) | 1 Million tonnes |

| Market Volume (2030) | 1.27 Million tonnes |

| Growth Rate (2025 - 2030) | 5.01% CAGR |

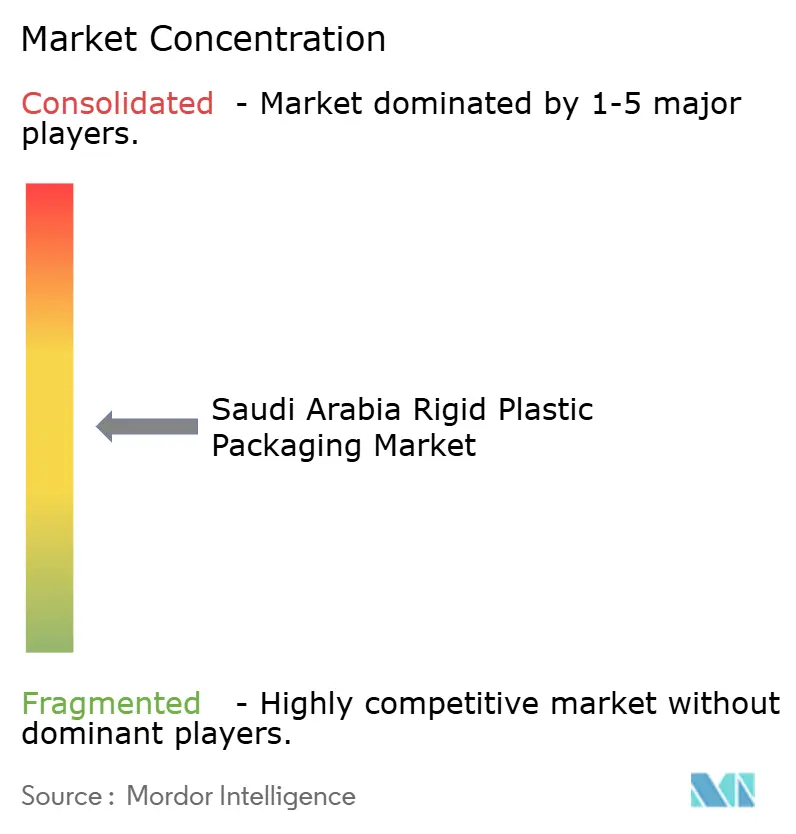

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Rigid Plastic Packaging Market Analysis by Mordor Intelligence

Saudi Arabia rigid plastic packaging market size stands at 1.0 million tonnes in 2025, and it is forecast to reach 1.27 million tonnes by 2030, registering a 5.01% CAGR during 2025-2030. This upward trajectory reflects the Kingdom’s strong feedstock position, broad polymer conversion capacity, and policy support under Vision 2030. Expansions such as SEPC’s Al-Jubail olefins project and the Aramco-Sinopec Yasref cracker reinforce domestic resin availability at globally competitive cost, ensuring dependable supply for converters. Robust bottled-water demand in the desert climate continues to anchor baseline volumes, while downstream industrialization programs diversify consumption into pharmaceuticals, food service, and construction. Circular-economy mandates are accelerating technology upgrades in recycling and traceability, giving first movers a strategic edge. Competitive intensity remains moderate, with established petrochemical affiliates and fast-scaling local converters both investing in automation, smart manufacturing, and compliance capabilities.

Key Report Takeaways

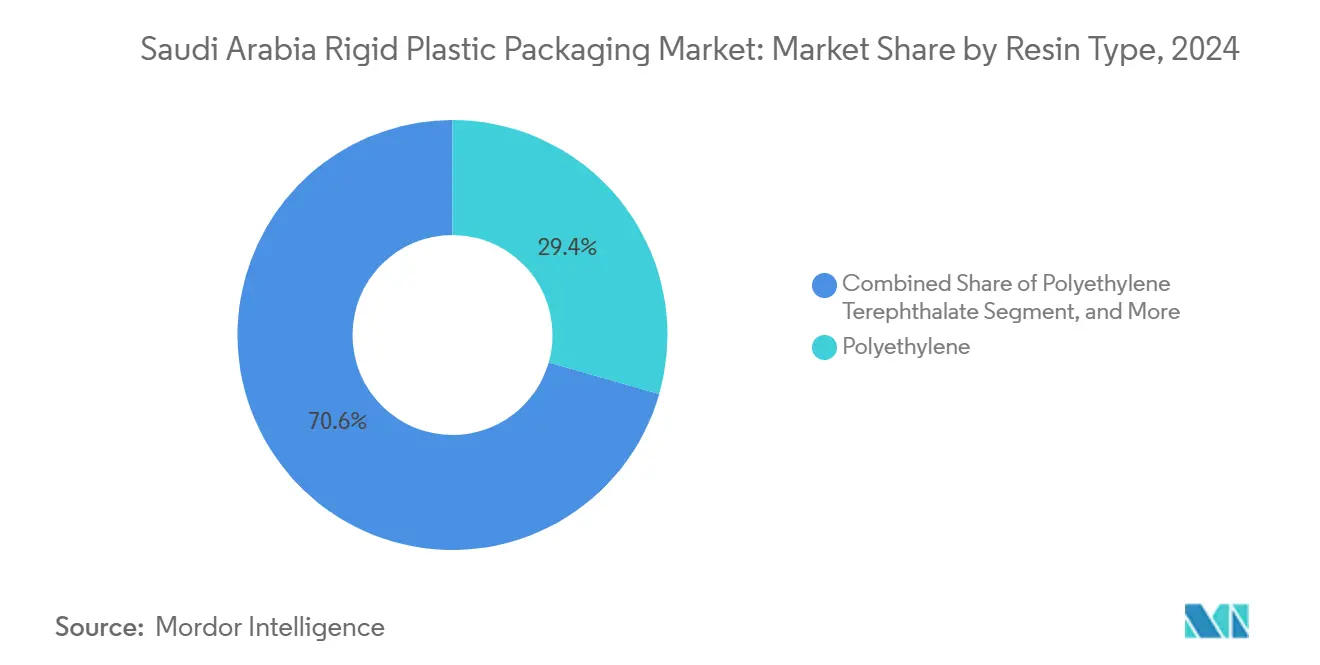

- By resin type, polyethylene led with 29.43% of the Saudi Arabia rigid plastic packaging market share in 2024, while polyethylene terephthalate is advancing at a 6.82% CAGR through 2030.

- By product type, bottles and jars accounted for 45.65% of the Saudi Arabia rigid plastic packaging market size in 2024; caps and closures are forecast to expand at a 7.22% CAGR to 2030.

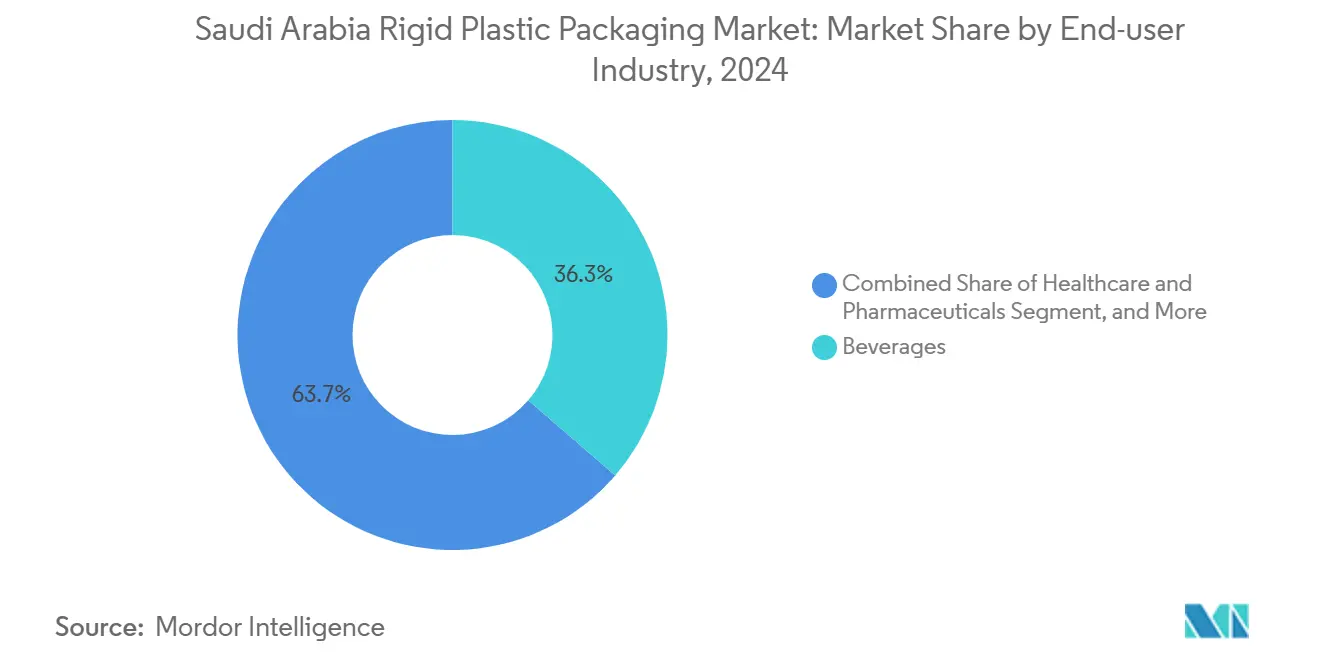

- By end-user industry, beverages captured 36.34% revenue share in 2024, whereas healthcare and pharmaceuticals is the fastest-growing segment at a 7.40% CAGR through 2030.

- By manufacturing process, injection moulding held 25.77% of the Saudi Arabia rigid plastic packaging market share in 2024, while thermoforming is projected to rise at a 6.38% CAGR up to 2030.

- SABIC, Obeikan Investment Group, and Zamil Plastic Industries together represented an estimated mid-teen share of national sales in 2024.

Saudi Arabia Rigid Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in bottled-water consumption amid desert climate | +1.8% | National, with concentration in Riyadh, Jeddah, Dammam metropolitan areas | Short term (≤ 2 years) |

| Saudi Vision 2030 investment in downstream plastics | +0.6% | National, with industrial clusters in Al-Jubail, Yanbu, Ras Al-Khair | Long term (≥ 4 years) |

| Food-service boom with quick-commerce and cloud kitchens | +0.8% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Mandate for pharma track-and-trace rigid packs | +0.4% | National, with regulatory compliance requirements | Medium term (2-4 years) |

| Rapid expansion of petrochemical recycling capacity | +0.6% | Industrial zones with integrated petrochemical complexes | Long term (≥ 4 years) |

| Carbon-border-tax preparedness driving local sourcing | +0.5% | Export-oriented manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Bottled-Water Consumption Amid Desert Climate

Extreme heat and low rainfall make safe packaged water a daily necessity for most households. Roughly 77% of residents rely on bottled water, lifting annual per-capita intake to nearly 120 liters and generating roughly 5 billion discarded PET bottles each year. Converter investment in bottle-grade PET lines, UV-resistant additives, and lightweight preforms therefore remains a priority. Retail pricing elasticity is limited, allowing premium packages with barrier enhancements to gain ground despite a government surcharge on large formats. As bottlers improve labeling and tamper security, closure makers benefit from demand for precision-molded caps that ensure shelf stability during long-distance transport in 40 °C ambient temperatures.

Saudi Vision 2030 Investment in Downstream Plastics

The state program targets conversion of up to 4 million barrels per day of crude into petrochemicals by 2030, realigning the upstream-to-downstream value chain. Projects such as the 1.8 million tonne Yasref cracker and the 18% capacity hike at Al-Jubail will lift domestic olefins output, narrowing resin import dependence and stabilizing local pricing. Cheaper feedstock under long-term supply contracts lets converters price more competitively in export tenders across the Gulf and Africa. International majors are responding: LyondellBasell’s 35% stake in polypropylene producer NATPET deepens global integration and introduces advanced catalyst technologies tailored for rigid packaging grades.

Food-Service Boom with Quick-Commerce and Cloud Kitchens

Half of the Kingdom’s population is under 30, and app-driven ordering habits are reshaping meal-consumption patterns. On-demand delivery and ghost-kitchen models require rigid containers that survive stacking, reheating, and last-mile vibration without leakage. Injection-molded polypropylene bowls with in-mold labels enable brand differentiation, while multi-compartment trays address portion-control preferences. Urban operators also favor tamper-evident lids to reassure customers about safety during transit a specification that rigid formats fulfill more reliably than flexible pouches. As platforms expand into Tier-2 cities, volume growth cascades to regional converters equipped with high-cavitation molds and automation.

Rapid Expansion of Petrochemical Recycling Capacity

The government aims to process 100 million tonnes of waste annually and achieve a 95% recycling rate, prompting joint ventures between polymer producers and recyclers.[1]Saudi Investment Recycling Company, “Circular Economy Initiatives and Recycling Statistics,” sirc.com.sa Chemical recycling units under development in Al-Jubail will output food-contact-grade rPET and rPP, giving brand owners access to certified recycled content without importing pellets. Converters participating in SABIC’s TRUCIRCLE program lock in feedstock at preferential terms and gain early compliance with future recycled-content mandates. Over the long term, access to consistent r-resin streams mitigates virgin-resin cost swings and enables closed-loop supply contracts with major beverage and pharmaceutical customers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-based resin prices | -0.7% | National, affecting all manufacturing regions | Short term (≤ 2 years) |

| Stringent single-use-plastic regulations and oxo-bio logos | -0.9% | National, with enforcement through SASO certification | Medium term (2-4 years) |

| Water-scarcity surcharge on high-volume bottle lines | -0.5% | National, with concentration in water-stressed regions | Medium term (2-4 years) |

| Glass and metal "premium" shift in FandB gifting culture | -0.4% | Urban centers, particularly Riyadh, Jeddah, and Eastern Province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Based Resin Prices

Polypropylene quotations at FOB Al-Jubail swung from USD 933 per tonne in Q3 2024 to the high USD 900s in early-2025 as global demand weakened and new capacity came online. Resin costs account for roughly two-thirds of converter operating expenses, so even modest shifts erode margins, especially for small firms lacking hedging tools. Domestic players do enjoy proximity to feedstock, but their export contracts are still benchmarked to international indices. The uncertainty discourages long-cycle capital spending on new molds or high cavitation presses, delaying capacity upgrades that could otherwise enhance competitiveness.

Stringent Single-Use-Plastic Regulations and Oxo-Bio Logos

From January 2025, all locally sold plastic products below 250 microns must carry SASO’s oxo-biodegradable logo, verified through laboratory testing at customs. Converters face 2-3% cost increases covering masterbatch additives and certification, plus potential shipment delays if paperwork is incomplete. Firms serving both domestic and export customers often need dual inventories one oxo-compliant and one conventional complicating production planning. The rule particularly affects disposable cutlery, trays, and thin-wall containers, though it has triggered R&D collaborations on enzyme-free degradation catalysts that may unlock cost savings over time.

Segment Analysis

By Resin Type : Polyethylene Retains Scale Despite Emerging PET Upside

Polyethylene captured 29.43% share of the Saudi Arabia rigid plastic packaging market in 2024, underscoring its versatility across bottles, drums, and closures. High-density grades dominate industrial pails and lubricant containers, while low-density and linear-low variants underpin squeeze bottles and thin-wall lids. Polyethylene’s all-purpose nature maintains strong customer loyalty, yet bottle-grade PET is advancing briskly at 6.82% CAGR as converters chase the superior clarity, barrier performance, and recycling profile valued by premium beverage and pharma buyers. The Saudi Arabia rigid plastic packaging market size for PET bottles is set to rise sharply as water bottlers retrofit lines for ultra-light preforms and boost rPET content targets. Strategic feedstock alliances for instance, between SABIC and local recyclers are aligning virgin and recycled resin supply, reducing exposure to volatile import prices and reinforcing domestic converter economics. Polypropylene sits in a strong third position, favored for closures, hot-fill food jars, and medical devices where chemical resistance and autoclavability offset slightly higher density. Engineering polymers remain niche but profitable, servicing healthcare, electrical, and automotive under-the-hood components.

Market participants increasingly differentiate via resin innovations. SABIC’s metallocene PE grades combine downgauging potential with stiffness, letting converters shave material usage without compromising top-load. Parallel moves in reactive compounding allow specialty masterbatch houses to incorporate UV stabilizers and oxygen scavengers tailored for desert logistics. Collectively, these advances protect polyethylene’s large installed base, even as rPET growth reshapes the beverage niche.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type : Bottles Remain Mainstay as Caps and Closures Outpace

Bottles and jars commanded 45.65% of 2024 volume, making them the anchor of the Saudi Arabia rigid plastic packaging market. Large PET formats meet everyday water needs, while smaller HDPE and PP jars serve condiments, nutraceuticals, and cosmetics. Multilayer barrier bottles for dairy drinks use EVOH tie layers to extend shelf life in a high-temperature retail environment. At the same time, caps and closures are projected to clock a 7.22% CAGR through 2030, reflecting demand for precision, tamper evidence, and child resistance. Pharma regulations stipulate serialized caps, and beverage brands require torque-optimized lightweight designs compatible with high-speed filling lines. The Saudi Arabia rigid plastic packaging market size for closures is expanding as converters deploy 64-cavity injection molds and in-mold slitting to supply both carbonated soft drink lines and aseptic bottling halls.

Trays, containers, and IBCs together form a growing diversified stream. Thermoformed PP trays support the boom in cloud kitchens, while drum and IBC use climbs in chemicals distribution, underpinned by Vision 2030 forward-integration projects. Niche segments such as trigger sprayers and dosing caps leverage local mold-making capability, adding functional sophistication that reduces reliance on imports.

By End-User Industry : Beverage Holds the Lead, Healthcare Accelerates

Beverages maintained the top 36.34% slice of Saudi Arabia rigid plastic packaging market share in 2024. Year-round heat and lifestyle habits keep water coolers and convenience stores restocking PET bottles daily. Soft drinks, flavored milk, and functional beverages add to baseline demand, pushing converters to develop light-and-oxygen-barrier structures that safeguard flavor in 45 °C truck trailers. In parallel, healthcare and pharmaceuticals is the quickest climber, forecast at 7.40% CAGR through 2030 as the Local Content and Government Procurement Authority pushes for 40% local drug output. Rigid HDPE bottles with humidity-barrier liners and serialized labels meet Saudi Food and Drug Authority track-and-trace rules, while prefilled syringe and vial trays emerge as ancillary opportunities.

Food packaging remains a solid third pillar, spanning dairy, frozen protein, and on-the-go snacks. Regulatory clarity around oxo-biodegradables nudges some operators toward thicker reusable tubs that sidestep thin-film mandates. Cosmetics and personal-care users lean on elegant acrylic jars and airless pumps to position premium brands. Industrial chemicals and construction materials employ heavy-duty drums, pails, and corrugated PP sheets, taking advantage of integrated polymer-to-package supply chains.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Manufacturing Process : Injection Moulding Dominant, Thermoforming Closes the Gap

Injection moulding held 25.77% of 2024 output, underscoring its unrivaled flexibility in producing closures, capsules, and high-precision components. The process benefits from steady investments in servo-hydraulic presses, high-speed take-out robots, and cavity-specific hot-runner monitoring. Lightweighting initiatives are lowering part weights by 10-15%, increasing throughput and trimming resin costs. Thermoforming, meanwhile, is on track for a 6.38% CAGR as it gains favor in food service trays and pharmaceutical blister packs. Converters value its short tooling lead times and inherent material-saving potential for shallow cavities.

Blow moulding remains the workhorse for large water bottles, leveraging multilayer parison technology for CO₂ retention and light blocking. Compression moulding addresses specialty closures where dimensional stability is paramount. Extrusion forms sheets and profiles later shaped in secondary operations, while rotational moulding maintains a niche in oversized tanks and road barriers vital for mega-projects like NEOM.

Geography Analysis

Eastern Province dominates supply because Al-Jubail and Dammam host world-scale crackers and polymerization plants, letting converters secure resin just a few kilometers from their molding halls. The Saudi Arabia rigid plastic packaging market size in this corridor benefits from integrated logistics dedicated port berths, rail spurs, and common-user tank farms that shrink shipping times and working capital. Riyadh, the country’s political and healthcare nerve center, drives demand for pharmaceutical and diagnostic packaging. Vision-aligned public tender frameworks increasingly stipulate local procurement, catalyzing greenfield plants in Riyadh’s industrial zones with proximity to research hospitals and distribution hubs.

Jeddah’s port on the Red Sea is the principal gateway for consumer goods moving to and from East Africa and the Suez Canal. Packaging converters in Jeddah tap that flow, offering co-packing and labeling services that align with Halal certification and Arabic labeling rules, then backhauling resin to Africa to build scale. Western Province demand also swells from the USD 613 billion NEOM project, whose workforce needs daily meal kits, construction-chemical drums, and modular building components. NEOM’s circular-construction commitment stipulates high recycled-content targets, sharpening the appeal of rPE and rPP rigid formats.

The central agricultural belt spanning Qassim and Hail uses rigid containers for dates, dairy, and poultry, where temperature-controlled logistics demand robust insulation and shock resistance. The northern and southern regions, historically underserved, are now on the radar as Vision 2030’s local-content calculators reward investments that spread industrialization. State-owned Saudi Investment Recycling Company plans satellite MRFs in these areas, ensuring that collected bottles loop back into rPET pellets feeding regional converters.

Competitive Landscape

The Saudi Arabia rigid plastic packaging industry is moderately fragmented. National champion SABIC leverages integrated upstream units and the TRUCIRCLE circular program to supply specialty polyolefins and r-resins that command brand premiums.[2]SABIC, “NPE2024: SABIC showcasing progress in plastic innovation,” sabic.com Obeikan Investment Group operates across PET preforms, corrugated board, and digital printing, cross-selling full packaging suites to multinational beverage and dairy clients. Zamil Plastic Industries showcases high-cavitation cap lines and ISO-class cleanrooms that qualify them for pharmaceutical contracts.

Entry barriers rise in 2025 as SASO’s updated import-certification scheme mandates facility registration, periodic audits, and biodegradability verification. Local firms that adopted SAP-based quality systems and traceability in advance now secure faster customs clearance, tilting tender outcomes in their favor. Automation and Industry 4.0 adoption remain decisive: players deploying cavity-pressure sensors and predictive maintenance reduce downtime by up to 15%, enabling aggressive price points without sacrificing margin. Today’s white spaces cluster around smart packaging, for example, NFC-tagged medicine bottles that simplify patient adherence, and reusable quick-commerce meal trays where embedded QR codes manage cleaning cycles. Recycling joint ventures also matter WASCO processes about half of the Kingdom’s recyclables and supplies rPET flakes that converters pelletize in-house.[3]Waste Collection and Recycling Company, “Waste Management and Recycling Services,” wasco.com.

Sustainability narratives influence market share as government buyers adopt green-procurement scorecards. Early adopters of chemical recycling and mass-balance accounting already see uplift in high-margin segments like infant-formula scoops and travel-electronics casings. International entrants often seek joint ventures to navigate localization quotas and raw-material allocations, mirroring LyondellBasell’s NATPET investment. Overall competition revolves less around sheer tonnage and more around agility, compliance, and design-for-circularity expertise.

Saudi Arabia Rigid Plastic Packaging Industry Leaders

-

Obeikan Investment Group

-

OCTAL Holding SAOC

-

Takween Advanced Industries Company

-

Arabian Plastic Industrial Company Ltd.

-

Zamil Plastic Industries Company Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Aramco and Sinopec agreed to expand the Yasref complex with a 1.8 million tonne cracker and 1.5 million tonne aromatics section, boosting domestic feedstocks for converters.

- April 2025: LyondellBasell signed to acquire a 35% stake in NATPET, adding 400,000 tonnes of PP capacity oriented toward rigid-packaging grades.

- April 2025: Borouge launched projects to lift olefins and polyolefins capacity to 6.6 million tonnes by 2028, awarding FEED to Linde and EPC to Target Engineering.

- November 2024: SABIC, iyris, and Napco teamed to develop greenhouse-roofing polymers emphasizing UV durability and recyclability.

Saudi Arabia Rigid Plastic Packaging Market Report Scope

The study on the Saudi Arabian rigid plastic packaging market tracks demand for significant packaging format types such as bottles and jars, trays and containers, caps and closures, and cups and lids, among other products, along with corresponding end-user industry verticals of these rigid plastic packaging products.

The Saudi Arabian rigid plastic packaging market is segmented by product (bottles and jars, trays and containers, caps and closures, intermediate bulk containers (IBCs), drums, pallets, and other products), material type (polyethylene (PE (LDPE and LLDPE and HDPE)), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), and other rigid plastic packaging materials), and end-use industry (food, beverage, healthcare, cosmetics and personal care, industrial, building and construction, automotive, and other end-use industries (household products and logistics)). The market sizes and forecasts are provided in terms of volume (tons) for all the above segments.

By Resin Type

| Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Polyethylene Terephthalate | |

| Polypropylene | |

| Polystyrene and EPS | |

| Other Resin Types |

By Product Type

| Bottles and Jars |

| Trays and Containers |

| Caps and Closures |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Other Product Types |

By End-user Industry

| Food | Candy and Confectionery |

| Dairy and Frozen | |

| Meat, Poultry and Seafood | |

| Other Food Types | |

| Beverage | |

| Healthcare and Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Industrial Chemicals | |

| Building and Construction | |

| Other End-user Industries |

By Manufacturing Process

| Injection Moulding |

| Blow Moulding |

| Thermoforming |

| Compression Moulding |

| Extrusion |

| Other Manufacturing Process |

| By Resin Type | Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | ||

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polyethylene Terephthalate | ||

| Polypropylene | ||

| Polystyrene and EPS | ||

| Other Resin Types | ||

| By Product Type | Bottles and Jars | |

| Trays and Containers | ||

| Caps and Closures | ||

| Intermediate Bulk Containers (IBCs) | ||

| Drums | ||

| Other Product Types | ||

| By End-user Industry | Food | Candy and Confectionery |

| Dairy and Frozen | ||

| Meat, Poultry and Seafood | ||

| Other Food Types | ||

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Industrial Chemicals | ||

| Building and Construction | ||

| Other End-user Industries | ||

| By Manufacturing Process | Injection Moulding | |

| Blow Moulding | ||

| Thermoforming | ||

| Compression Moulding | ||

| Extrusion | ||

| Other Manufacturing Process | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Saudi Arabia rigid plastic packaging market?

The market measures 1.0 million tonnes in 2025 and is projected to grow to 1.27 million tonnes by 2030.

How fast is the sector growing?

The market is set to advance at a 5.01% CAGR during 2025-2030, fueled by Vision 2030 industrial programs and rising bottled-water demand.

Which product type leads demand?

Bottles and jars hold the largest 45.65% share, supported by water and beverage consumption.

Which end-user industry shows the highest growth potential?

Healthcare and pharmaceuticals are forecast to expand at a 7.40% CAGR through 2030 as local drug production scales up.

How do new SASO regulations affect packaging producers?

Mandatory oxo-biodegradable logos add 2-3% to material costs and require dual inventories for domestic and export lines.

What factors influence resin price volatility in Saudi packaging?

Global crude-oil swings and new GCC polymer capacity drive frequent shifts in PP and PE pricing, impacting converter margins.

Page last updated on: