Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

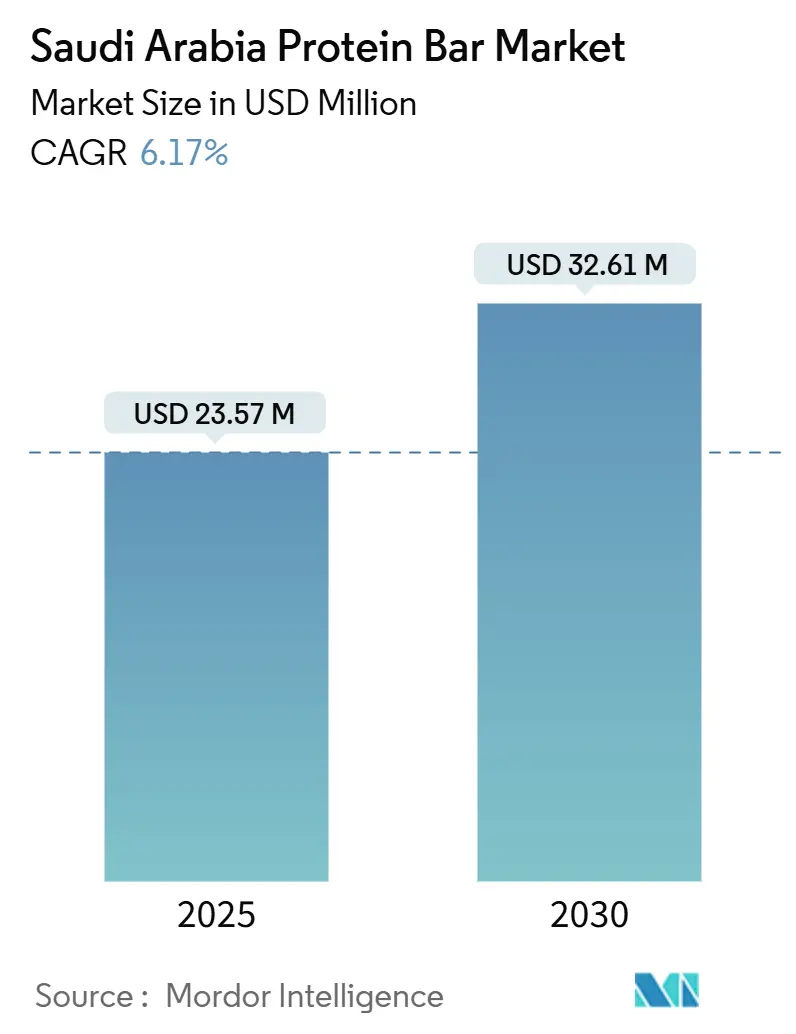

| Market Size (2025) | USD 23.57 Million |

| Market Size (2030) | USD 32.61 Million |

| Growth Rate (2025 - 2030) | 6.17% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Protein Bar Market Analysis by Mordor Intelligence

The Saudi Arabia protein bar market size stands at USD 23.57 million in 2025 and is forecast to reach USD 32.61 million by 2030, expanding at a 6.71% CAGR. This steady climb mirrors the Kingdom’s Vision 2030 focus on healthier living, the mainstreaming of fitness culture, and the widening availability of convenient on-the-go nutrition. Structural reform has opened new female-only fitness centers, e-commerce platforms have shortened the path to purchase, and major retailers now dedicate premium shelf space to functional snacks. International brands continue to introduce differentiated formulations, while local firms experiment with date-based protein bars that align with cultural tastes and could benefit from subsidy programs aimed at stimulating domestic food manufacture. Competitive intensity is moderate, giving both entrenched multinational leaders and agile Saudi innovators room to defend or grow share through localization, ingredient sourcing shifts, and digital marketing that targets the nation’s youthful consumer base.

Key Report Takeaways

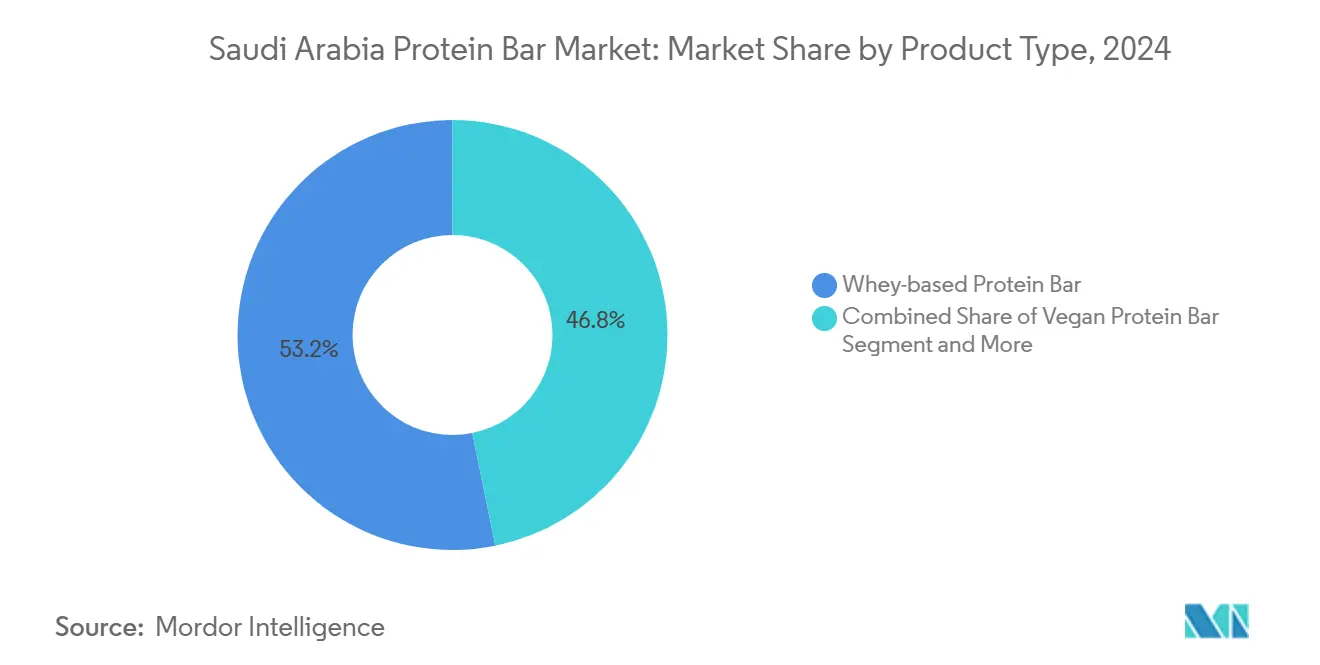

By type, whey-based protein bars led with 53.18% of the Saudi Arabia protein bar market share in 2024, while vegan protein bar tends to be the fastest type, registering a CAGR of 11.28%, through 2030.

By function, post-workout recovery accounted for 32.75% share of the Saudi Arabia protein bar market size in 2024 and sports nutrition lead, registering a CAGR of 9.86%, through 2030.

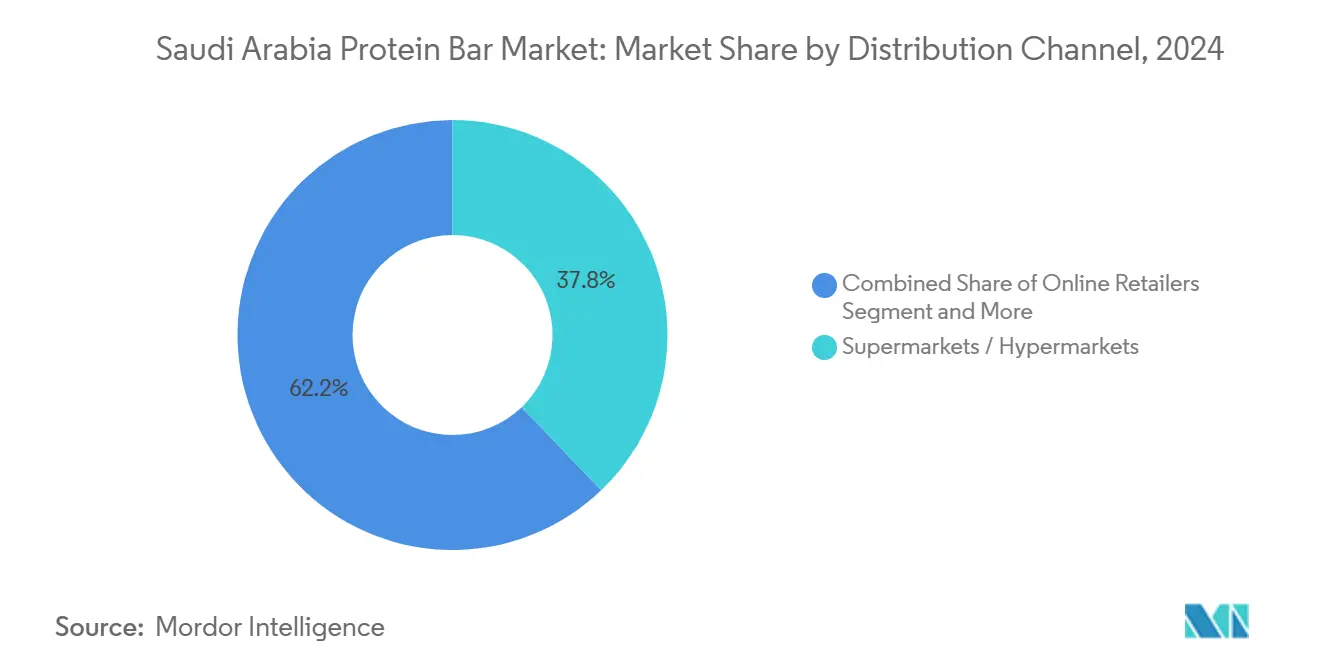

By distribution channel, supermarkets and hypermarkets captured 37.84% share of the Saudi Arabia protein bar market size in 2024, while online retailers are advancing at a 12.69% CAGR through 2030.

Saudi Arabia Protein Bar Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health & fitness culture among youth | +1.5% | National, concentrated in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Increasing demand for convenient on-the-go nutrition | +1.8% | National, urban concentration | Short term (≤ 2 years) |

| Expansion of modern retail & e-commerce penetration | +2.1% | National, led by major cities | Short term (≤ 2 years) |

| Government healthy-living initiatives (Vision 2030) | +0.9% | National | Long term (≥ 4 years) |

| Surge in female gym memberships post-reform | +1.2% | National, particularly urban centers | Medium term (2-4 years) |

| Localization of date-based protein bars & subsidy support | +0.8% | National, manufacturing hub focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Health & Fitness Culture Among Youth

Saudi Arabia counts 63% of its residents under 30, creating a demographic powerhouse that expects fitness facilities to be as accessible as coffee shops. Gyms such as GymNation are partnering with local investors to roll out spacious, low-priced clubs in Riyadh, Jeddah, and Dammam, normalizing structured exercise across socioeconomic tiers. Government-led “Sports for All” campaigns channel Vision 2030 budgets into community events, university leagues, and workplace wellness competitions, all of which integrate protein bars into post-activity routines. Social media magnifies these shifts: Saudi influencers post workout videos and “snack hauls” that feature the newest flavors, while global athletes visiting for high-profile boxing or Formula E events endorse portable protein. The Saudi Arabia protein bar market therefore enjoys a pipeline of first-time buyers who quickly graduate to habitual use once they associate bars with performance gains.

Increasing Demand for Convenient On-the-Go Nutrition

The pace of urban employment, particularly on Vision 2030 mega-projects such as NEOM, leaves little room for seated meals. Busy professionals reach for individually wrapped bars that deliver 15–20 g of protein in seconds, sidestepping time and refrigeration constraints. Portable nutrition spikes during Ramadan: consumers rely on bars to supply protein between sunset iftar and the pre-dawn suhoor, smoothing energy levels during daylight fasting hours. Foodservice operators now place branded bar displays near cashier zones, encouraging impulse purchases at gyms, petrol stations, and co-working cafés. To sustain demand, manufacturers promote multi-bar “office pack” formats, aligning with employers’ wellness programs and bulk-ordering platforms. All these factors keep the Saudi Arabia protein bar market in view of professionals striving to balance dietary quality with demanding schedules.

Expansion of Modern Retail & E-Commerce Penetration

Panda operates 198 hypermarkets and four distribution centers, Tamimi Markets plans to double its 90-store footprint, and Al Othaim runs 256 branches nationwide. Each chain devotes end-caps and eye-level shelves to functional snacks, backed by point-of-sale education that demystifies protein content and flavors. Simultaneously, grocery apps supported by government digitalization policies deliver nationwide, offering same-day or next-day drop across the Kingdom. With year-round temperatures exceeding 40 °C, producers rely on cold-chain logistics specialists such as Abbar Foods to preserve bar texture and prevent fat bloom during transit. E-commerce sites allow consumers to filter by protein grams, allergen status, and halal certification, increasing the chance of first-time trials. Subscription models further embed buying habits, translating retail infrastructure improvements directly into Saudi Arabia protein bar market value.

Government Healthy-Living Initiatives (Vision 2030)

Vision 2030’s Quality of Life Program stipulates the construction of sports facilities, cycling paths, and public parks in every major city. The National Center for Health Promotion now funds awareness campaigns on balanced diets, with televised segments that feature protein bars as post-exercise refueling tools. The Saudi Food and Drug Authority revised nutrition-labeling regulations in 2024, forcing brands to disclose complete amino-acid profiles and sugar-alcohol content. Transparent labels reward premium formulations and nudge consumer choice toward bars with cleaner ingredient lists. Complementing demand-side signals, the National Industrial Development and Logistics Program extends duty exemptions on imported machinery for local bar production lines, encouraging manufacturers to shift assembly and wrapping to Saudi plants over the long term. Policy coherence therefore underpins both the supply and the demand for protein bars.

Restraints Impact Analysis

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High landed cost due to import dependency | –0.7% | National, stronger in price-sensitive segments | Short term (≤ 2 years) |

| Competition from alternative snack formats | –0.5% | National, modern retail channels | Medium term (2-4 years) |

| Impending sugar-content tax extension to bars | –0.4% | National | Medium term (2-4 years) |

| Shelf-life & cold-chain hurdles in desert climate | –0.3% | National, rural distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Landed Cost Due to Import Dependency

Specialty ingredients such as whey isolate and chicory-root fiber arrive through Jeddah Islamic Port, incurring freight surcharges and currency-related volatility. Post-COVID freight prices have stabilized yet remain 18–22% above 2019 baselines, pushing up ex-factory prices. The imposition of 15% VAT in 2020 and selective excise duties on sugary foods further compress retail margins. PepsiCo’s USD 300 million expansion in Dammam underscores industry commitment to curbing import reliance, but local procurement still cannot supply micronized leucine or certain heat-stable enzymes at commercial scale. Brands must choose between absorbing extra costs, downsizing bar weight, or passing rises to consumers—each option risking volume softness in the Saudi Arabia protein bar market’s value segment.

Competition from Alternative Snack Formats

Protein-fortified yogurts from Almarai, sugar-free protein cookies from Nestlé’s FITNESS line, and high-protein camel-milk shakes all encroach on occasions historically owned by bars. The reformulation of traditional Saudi ma'amoul with added pea protein offers familiar taste at competitive price points, seducing consumers who would otherwise experiment with imported bars. Nestlé’s FITNESS No Sugar Protein Bar leverages a household brand identity that eases shopper hesitation in front of crowded snack aisles. As cross-category protein options proliferate, companies must invest in flavor innovation, portion versatility, and experiential marketing to keep the Saudi Arabia protein bar market from ceding share to wider snack alternatives.

Segment Analysis

By Type: Whey Dominance Meets Vegan Acceleration

The whey-based segment represented 53.18% of the Saudi Arabia protein bar market share in 2024, underpinning overall category leadership through brands such as Quest, Atkins, and Optimum Nutrition. Whey’s superior amino-acid spectrum and rapid absorption resonate with gym-centric consumers seeking proven performance benefits. Larger players secure price advantages by leveraging global whey procurement contracts, while domestic importers maintain chilled facilities to protect protein integrity during sea transit. The segment also profits from medical endorsement: sports-science clinics embedded in Riyadh’s King Abdullah Sports City often recommend 20 g whey snacks post-session. Consequently, the Saudi Arabia protein bar market size attributable to whey formulations is expected to expand in line with new gym buildouts and personal-trainer adoption of protein tracking apps that link directly to bar purchase reminders.

Vegan bars, forecast to grow at an 11.28% CAGR through 2030, ride a wave of plant-based curiosity among millennials and Gen Z Muslims who see ethical and environmental value in alt-protein sources. Simply Good Foods’ acquisition of OWYN extends a ready-to-drink loyalist pool into bar formats, giving cross-channel leverage. Domestically, SMEs blend Saudi dates with chickpea or fava-bean protein to achieve 12–15 g protein targets without soy or dairy allergens. Retailers allocate “plant powered” shelves to differentiate these SKUs from legacy whey, and e-commerce algorithms surface vegan bundles during Eco-Friendly Week promotions. Should import tariffs on pea protein isolate taper under prospective GCC agreements, vegan bars could approach price parity with whey, pushing the Saudi Arabia protein bar market size for plant-based lines beyond current projections.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Function: Recovery Focus Drives Sports Nutrition Expansion

Post-workout recovery bars captured 32.75% of the Saudi Arabia protein bar market share in 2024. Their positioning, centered on muscle repair within the anabolic window, fits narratives promoted by gym influencers and physiotherapists. Formulations typically pair 20 g protein with 2 g creatine and electrolytes, marketing a “one-pack solution” for post-training needs. These SKUs enjoy distribution privileges at gym reception counters, where impulse grabbing is common after exhausting sessions. Packaging frequently includes QR codes linking to body-composition tracking apps, embedding bars in holistic self-improvement journeys that reinforce brand loyalty across urban fitness clusters.

Sports-nutrition-specific bars, while only nascent, are advancing at a 9.86% CAGR, signaling a transition from generic recovery to sport-tailored macronutrient ratios. Marathon-oriented bars fine-tune maltodextrin-to-fructose matrices for endurance fuel, whereas strength-athlete bars emphasize higher leucine for muscle protein synthesis. The Ministry of Sport’s increased funding for federations—fencing, climbing, triathlon—creates discipline-specific academies that stock such bars in onsite vending machines. Manufacturers co-sponsor race events, providing sample kits inside registration packs and capturing CRM data for targeted remarketing. This deep vertical integration positions performance-centric SKUs as premium extensions within the Saudi Arabia protein bar market.

By Distribution Channel: Traditional Retail Strength Faces Digital Disruption

Supermarkets and hypermarkets commanded a 37.84% slice of the Saudi Arabia protein bar market size in 2024, benefitting from weekly grocery habits and trust in well-lit aisles. End-cap displays featuring clear calorie counts encourage trial among family shoppers seeking better-for-you snacks for school lunchboxes. Retailers allocate loyalty-program points multipliers to protein-bar purchases during White Friday sales, lifting volumes without permanent price erosion. Instore dieticians conduct weekend demos, explaining amino-acid profiles and steering consumers toward multi-flavor variety packs that increase average basket value. While foot traffic remains robust, supermarkets face mounting pressure to differentiate as online platforms erode convenience advantages once exclusive to brick-and-mortar.

Online retailers, scaling at 12.69% CAGR, exploit frictionless checkout, nationwide reach, and algorithm-driven personalization that suggests bars based on previous searches for whey protein powder or calorie-tracking apps. E-pharmacies such as Nahdi Online add credibility by vetting ingredient lists and offering pharmacist chat support. Subscription models deliver 12-bar monthly boxes with rotating flavors, locking households into recurring revenue streams and generating predictive demand curves that optimize factory scheduling. Flash-sales timed around sunset during Ramadan create surge orders, addressed by expanded fulfillment centers near Jeddah and Riyadh airports. With rising smartphone penetration already above 93%, the Saudi Arabia protein bar market sees digital as both the fastest-growing end-point and a data goldmine for micro-targeted product development.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Riyadh accounts for the single-largest share of the Saudi Arabia protein bar market, reflecting the city’s 7.8 million population, highest gym density per capita, and concentration of corporate headquarters that purchase wellness packages for employees. Disposable incomes support premium bars priced 15–28% above national averages, and café-adjacent fitness studios feed steady demand for grab-and-go post-workout snacks. Jeddah follows as a commercial hub with strong expatriate presence, whose familiarity with international fitness products accelerates brand trial and pushes flavor diversification beyond date and chocolate toward peanut butter crunch and blueberry muffin variants. The Eastern Province, buoyed by Aramco employment clusters, exhibits high weekday morning sales as shift workers buy bars en route to industrial sites.

Secondary urban centers—Medina, Taif, Khobar—are poised for catch-up, driven by government mandates for balanced regional development. As malls open in these cities, anchor hypermarkets replicate health aisles seen in Riyadh and Jeddah, ensuring consistent product set. Yet distribution still contends with hot-chain breaches along long desert highways, pressing suppliers to equip trucks with real-time temperature telemetry and contingency stopovers at refrigerated depots. Rural penetration remains lowest; however, the Ministry of Municipal and Rural Affairs funds 18 new logistics hubs that could shorten lead times and mitigate melt risks. For the Saudi Arabia protein bar market, geography thus dictates iterative network investment, flavor adaptation to conservative palates, and phased marketing spend calibrated to urban income strata.

Competitive Landscape

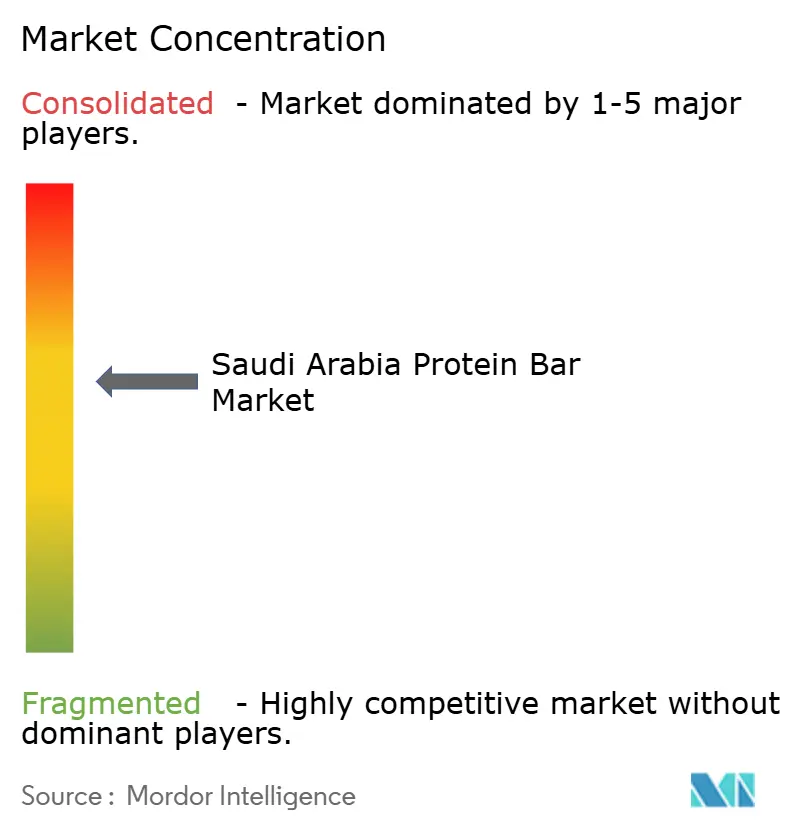

Global multinationals PepsiCo, Simply Good Foods, and Nestlé command shelf visibility through aggressive trade-marketing budgets, but local powerhouse Almarai leverages cold-chain prowess and brand familiarity to defend share in dairy-adjacent snack bars. Moderate concentration (6/10) reflects this tussle between scale and local insight. PepsiCo’s Dammam expansion adds extruded bar lines capable of running both whey and plant-based matrices, shortening replenishment cycles, and reducing the forex exposure attached to finished-goods imports. Simply Good Foods cross-sells Atkins snack bars in pharmacies where OWYN vegan shakes sit, broadening health baskets at complementary price points. Nestlé capitalizes on its first Saudi factory to roll out FITNESS-branded bars that pair naturally with the company’s breakfast-cereal franchise, tapping household trust established over decades.

Local innovators exploit cultural white space. SMEs package date-caramel flavors in gold foil, signaling premium gifting potential during Eid and National Day. Niche players experiment with camel-milk whey, seeking functional differentiation and story-telling resonance. Female-led startups craft bars sized for women’s caloric needs, marketing them through Instagram Live workouts hosted by certified trainers. To increase barriers to entry, incumbents sign long-term exclusives with Tamimi and Panda for prime shelf real estate, while digital natives secure top-of-search positions via keyword bidding wars on noon.com and Amazon.sa. The Saudi Arabia protein bar market therefore balances global heft with grassroots ingenuity, forging a dynamic yet disciplined playing field where localization and supply-chain agility are decisive.

Saudi Arabia Protein Bar Industry Leaders

-

PepsiCo

-

The Simply Good Foods Co.

-

General Mills

-

Barebells Functional Foods

-

Almarai Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2023: think!, a part of Glanbia Performance Nutrition, offers high-protein snacks. The company announced the launch of two new dessert-inspired flavors for its best-selling line of High Protein Bars, including Boston Crème Pie and Chocolate Mint.

- April 2023: Divine Chocolates expanded its market in Saudi Arabia. The company's product portfolio includes For Fit, a healthy chocolate bar that is halal certified, contains whey protein and no added sugar, and is gluten-free.

- March 2023: OptiBiotix Health PLC, a supplier of microbiome-health ingredients, launched its GoFigure consumer line of nutritional shakes and bars in Saudi Arabia. GoFigure products feature OptiBiotix’s trademark weight-management ingredient, SlimBiome.

Saudi Arabia Protein Bar Market Report Scope

Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats.

The report is segmented by type and distribution channel. Based on type, the market is segmented into vegan protein bars and regular protein bars. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online stores, and other distribution channels. The market sizing has been done in value terms (USD) for all the above-mentioned segments.

By Type

| Vegan Protein Bar |

| Whey-based Protein Bar |

| Mixed Type Protein Bars |

By Function

| Meal-Replacement |

| Post-Workout Recovery |

| Sports Nutrition |

| Others (Dietary Supplements, Energy Boost) |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience and Grocery Stores |

| Specialty Nutrition Stores |

| Online Retailers |

| Others |

| By Type | Vegan Protein Bar |

| Whey-based Protein Bar | |

| Mixed Type Protein Bars | |

| By Function | Meal-Replacement |

| Post-Workout Recovery | |

| Sports Nutrition | |

| Others (Dietary Supplements, Energy Boost) | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Convenience and Grocery Stores | |

| Specialty Nutrition Stores | |

| Online Retailers | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Saudi Arabia protein bar market in 2025?

The Saudi Arabia protein bar market size is USD 23.57 million in 2025.

What is the projected CAGR of protein bar sales in Saudi Arabia through 2030?

Sales are forecast to post a 6.71% CAGR over 2025–2030.

What is the projected CAGR of protein bar sales in Saudi Arabia through 2030?

Sales are forecast to post a 6.71% CAGR over 2025–2030.

Which protein source dominates bar formulations sold in Saudi Arabia?

Whey-based bars lead with 53.18% market share in 2024.

Why are vegan protein bars growing faster than other types?

Demand stems from rising plant-based diets and local innovations that blend Saudi dates with pea or rice protein, driving an 11.28% CAGR.

Page last updated on: