Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 2.04 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Hospital Supplies Market Analysis by Mordor Intelligence

The Saudi Arabia Hospital Supplies Market size is estimated at USD 1.53 billion in 2026, and is expected to reach USD 2.04 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031).

Rising health allocations under Vision 2030, an expanding chronic-disease patient pool, and a national goal to add 27,000 beds by 2030 are the primary growth engines for the Saudi Arabia hospital supplies market. Diabetes affects 18.5% of adults, cardio-metabolic disorders account for more than one-third of deaths, and an aging population intensifies per-capita consumption of disposables, wound-care kits, and monitoring devices. Operating-room equipment is set to be the fastest-growing product group as flagship institutions deploy robotic surgery and hybrid theatres. At the same time, NUPCO’s digital marketplace shortens tender cycles and squeezes inefficient distributors. Local-content incentives, environmental levies on single-use plastics, and AI-driven inventory platforms are reshaping supplier strategies as they navigate compliance costs and margin pressure within the Saudi Arabia hospital supplies market.

Key Report Takeaways

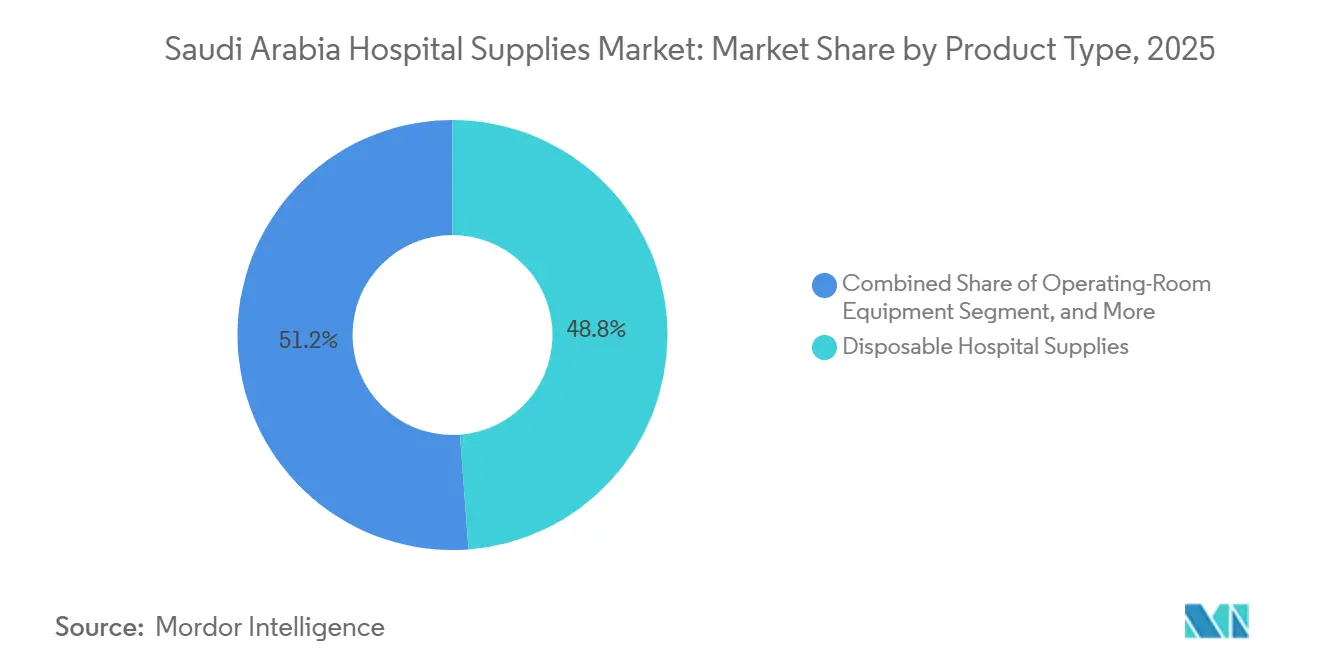

- By product type, disposable hospital supplies held 48.81% of the Saudi Arabia hospital supplies market share in 2025; operating-room equipment is projected to expand at a 7.73% CAGR through 2031.

- By application, surgical and trauma care led with a 37.73% revenue share in 2025, while wound management is forecast to post the highest 8.23% CAGR from 2025 to 203.

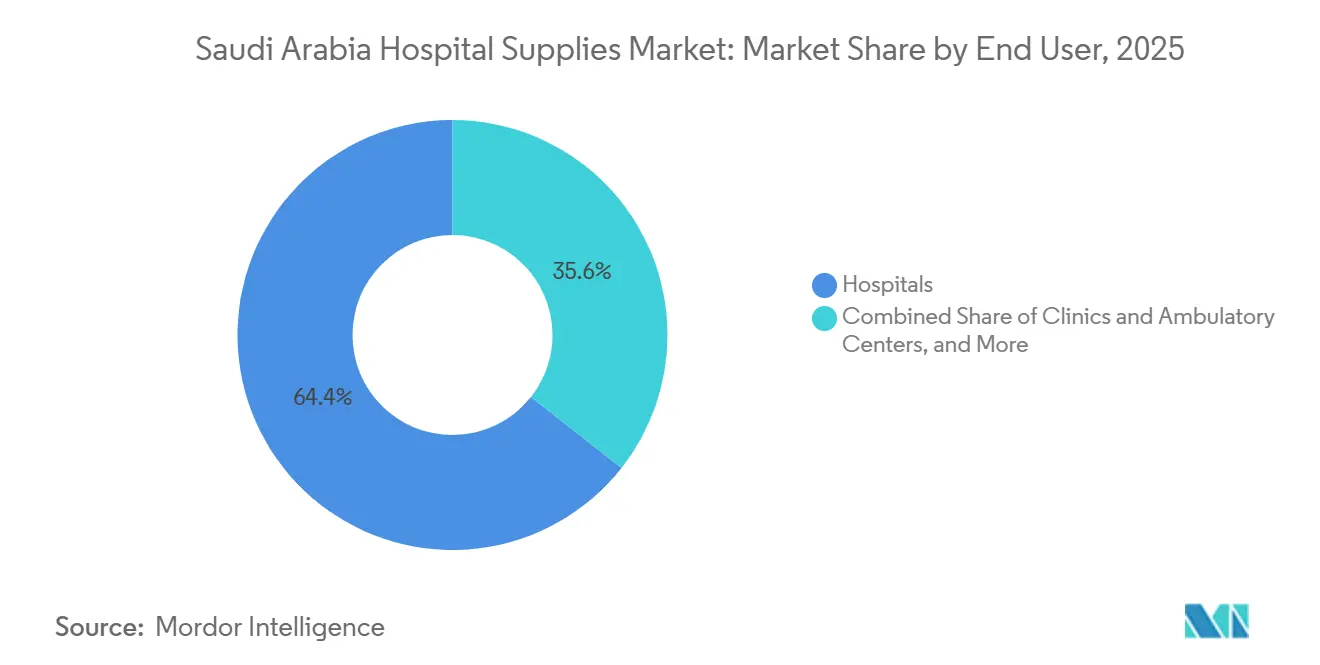

- By end user, hospitals captured 64.38% of spending in 2025; clinics and ambulatory centers are expected to grow at the fastest rate, with a 6.75% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Hospital Supplies Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Vision 2030 Healthcare Expenditure | +1.5% | National, with concentration in Riyadh, Jeddah, Dammam medical cities | Long term (≥ 4 years) |

| Rising Chronic-Disease Burden | +1.3% | National, highest incidence in urban centers and Eastern Province | Medium term (2-4 years) |

| Expansion of Hospital Bed Capacity & New Medical Cities | +1.2% | National, priority zones include Neom, Qiddiya, King Salman Medical City | Long term (≥ 4 years) |

| NUPCO E-Procurement Digitization Accelerates Purchasing | +0.8% | National, serving 300+ hospitals and 2,500 clinics | Short term (≤ 2 years) |

| Local-Content Incentives for Domestic Disposables Production | +0.6% | National, with manufacturing clusters in Riyadh, Jeddah, Dammam, Jazan | Medium term (2-4 years) |

| AI-Driven Inventory Optimisation Demanding Smart Consumables | +0.5% | National, early adoption in large hospital networks and NUPCO warehouses | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Vision 2030 Healthcare Expenditure

Vision 2030 allocates SAR 260 billion for health and social development in the 2025 budget, representing a 12% increase from the previous year, which underscores the state's commitment to diversifying beyond hydrocarbons.[1]Saudi Ministry of Finance, “Budget Statement 2025,” MOF.GOV.SA Funding supports the development of 12 new medical cities and upgrades to 150 existing facilities, each requiring multi-year contracts for disposables, sterilizers, and monitors. The privatization roadmap, covering 290 hospitals and 2,300 primary health centers, introduces pay-for-performance models that reward lower infection rates, spurring demand for advanced wound dressings and rapid sterilization systems. Public Investment Fund outlays of above USD 65 billion through 2030 provide suppliers with the visibility needed to justify in-country production partnerships. ISO 13485 compliance remains mandatory for all devices entering NUPCO tenders, ensuring adherence to quality systems and favoring well-capitalized vendors.

Rising Chronic-Disease Burden

Diabetes prevalence stands at 18.5% of adults, with 51% of citizens aged 65 and older managing the condition, which drives sustained demand for glucose strips, insulin pens, and advanced dressings.[2]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” IDF.ORG Cardiovascular ailments account for 37% of deaths, lifting catheterization-lab consumables and post-operative monitoring needs. The national screening launched in 2024 covers 5 million citizens annually, converting undiagnosed cases into active therapy cohorts that rely on steady supply flows. Wound-management revenue is projected to climb at an 8.23% CAGR as negative-pressure therapy and bioactive dressings become the standard of care. Obesity affects 23.1% of adults, extending hospital stays and raising per-patient use of PPE and infection-control products.

Expansion of Hospital Bed Capacity & New Medical Cities

Saudi Arabia operates 497 hospitals with 80,000 beds, equivalent to 2.3 beds per 1,000 population, which is below the OECD average of 4.7.[3]Saudi Ministry of Health, “Health Sector Transformation Program,” MOH.GOV.SA Vision 2030 mandates the addition of 27,000 beds by the end of the decade, concentrated in mega projects, including King Salman Medical City and the Neom Health District. Operating-room equipment leads product-level gains with a 7.73% CAGR as facilities install robotic systems and hybrid theatres that retain high-acuity procedures domestically. Public-private partnerships govern 60% of builds and embed penalties for stock-outs, favoring suppliers with in-Kingdom warehousing and real-time inventory platforms.

NUPCO E-Procurement Digitization Accelerates Purchasing

NUPCO’s digital marketplace, live since Q1 2025, automates tender issuance, bid scoring, and contract award across more than 300 hospitals and 2,500 clinics, delivering 18–22% cost savings on high-volume items. Two new distribution centers, scheduled to be operational in 2026, will reduce last-mile delivery times to under 24 hours for 85% of orders, thereby reducing safety stock and freeing up working capital. Predictive analytics models influenza seasons and Hajj surges, allowing suppliers to pre-position inventory and avoid emergency airfreight premiums that previously added 8–12% to costs. Smaller distributors that outperform on service can displace incumbents, intensifying market fragmentation in Saudi Arabia's hospital supplies market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import Dependency Exposes Supply Chains to FX & Logistics Shocks | -0.7% | National, acute impact on high-value capital equipment and specialty consumables | Short term (≤ 2 years) |

| Stringent SFDA Approvals & Tender Pre-Qualification Hurdles | -0.5% | National, disproportionately affects new entrants and innovative device categories | Medium term (2-4 years) |

| Environmental Levies on Single-Use Plastics to Lift Unit Costs | -0.4% | National, with stricter enforcement in Riyadh, Jeddah, and Neom zones | Medium term (2-4 years) |

| Nurse Shortage & Saudization Slow Uptake of High-Tech Devices | -0.3% | National, most acute in rural regions and secondary-tier hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Dependency Exposes Supply Chains to FX & Logistics Shocks

Saudi Arabia sources 85% of its devices from abroad, making the sector vulnerable to currency fluctuations and shipping delays. Red Sea disruptions in 2024 stretched container transit from 28 to 45 days, forcing hospitals to hold 60–90 days of stock and tying up SAR 1.2 billion in extra working capital. Cold-chain requirements add 12–15% to transport costs during peak summer temperatures above 45 °C. Local manufacturing remains skewed toward gauze and bandages, leaving specialty consumables vulnerable to external shocks and pressuring the Saudi Arabia hospital supplies market.

Stringent SFDA Approvals & Tender Pre-Qualification Hurdles

The Saudi Food and Drug Authority aligns with EU MDR standards, which require clinical evaluation reports, post-market surveillance plans, and ISO 13485 certification before market entry. Approval takes 3–6 months for Class IIa devices and up to 12 months for Class III devices, which delays innovative launches and allows incumbents to secure multi-year tenders. Pre-qualification requires audited financial statements and proof of a three-year GCC supply history, which can exclude start-ups and smaller foreign firms. Compliance adds USD 50,000–150,000 per SKU, discouraging broad portfolios in the Saudi Arabia hospital supplies market.

Segment Analysis

By Product Type: Robotics and AI Propel Operating-Room Equipment

Operating-room equipment posted the fastest segment growth, advancing at a 7.73% CAGR as 12 medical cities install robotic platforms, hybrid theatres, and AI anesthesia workstations. King Faisal Specialist Hospital expanded its robotic program to eight consoles in 2024, enabling minimally invasive procedures that cut length of stay by up to 40%. The segment secured long-term agreements with GE Healthcare and Siemens Healthineers, securing pipeline visibility for OEMs within the Saudi Arabia hospital supplies market. Disposable hospital supplies retained a 48.81% revenue share in 2025; however, growth is expected to moderate to a 5.2% CAGR as centralized procurement compresses pricing and environmental regulations drive a partial shift toward reusables.

Sterilization and disinfectant products benefit from waste-diversion targets that favor low-temperature hydrogen peroxide systems. However, capital costs are 20–25% higher than those of legacy ethylene oxide units, and there is slow uptake in budget-constrained facilities. Mobility aids and transportation equipment are expected to rise in tandem with the expansion of home care and an elderly cohort projected to reach 12% of the population by 2030. All categories must meet ISO 13485 requirements to qualify for tenders, ensuring sustained quality thresholds across the Saudi Arabia hospital supplies market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Diabetic Burden Accelerates Wound Management

Wound management is forecast to expand at an 8.23% CAGR through 2031 as diabetic foot ulcers and pressure injuries escalate with the 18.5% adult diabetes prevalence. Negative-pressure therapy became mainstream in tertiary hospitals by 2025, halving healing times for complex wounds and lowering readmissions. Bioactive dressings that reduce dressing-change frequency by 40% are gaining reimbursement, boosting revenue for suppliers with collagen and silver-based portfolios. A local Mölnlycke plant will shorten lead times and enhance price competitiveness, reinforcing supplier positions within the Saudi Arabia hospital supplies market.

Surgical and trauma care maintained a 37.73% share in 2025, driven by high volumes of cardiac, orthopedic, and neurosurgical procedures that require large quantities of sutures and drapes. Infection-control and PPE spending stabilized post-pandemic, with hospitals carrying 90-day reserves as a strategic buffer.

By End User: Privatization Fuels Ambulatory-Center Expansion

Clinics and ambulatory centers are projected to record a 6.75% CAGR, the fastest among end users, as Vision 2030 shifts low-acuity procedures into outpatient settings and private operators scale day-surgery units. Dr. Sulaiman Al-Habib Medical Group added 25% capacity in 2024–2025, performing same-day cataract and hernia repairs that cut per-case supply costs up to 35%. Alcon’s Jeddah experience center trains surgeons on phaco systems, accelerating the adoption of same-day discharge cataract protocols. These trends widen market scope for single-use kits and pre-sterilized packs in the Saudi Arabia hospital supplies market.

Hospitals still account for 64.38% of expenditure due to their dominance in tertiary care and high-acuity admissions. Home healthcare providers grew by 18% in 2025 as insurers funded remote monitoring and infusion therapy, driving demand for portable oxygen concentrators and telehealth-ready glucometers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Competitive Landscape

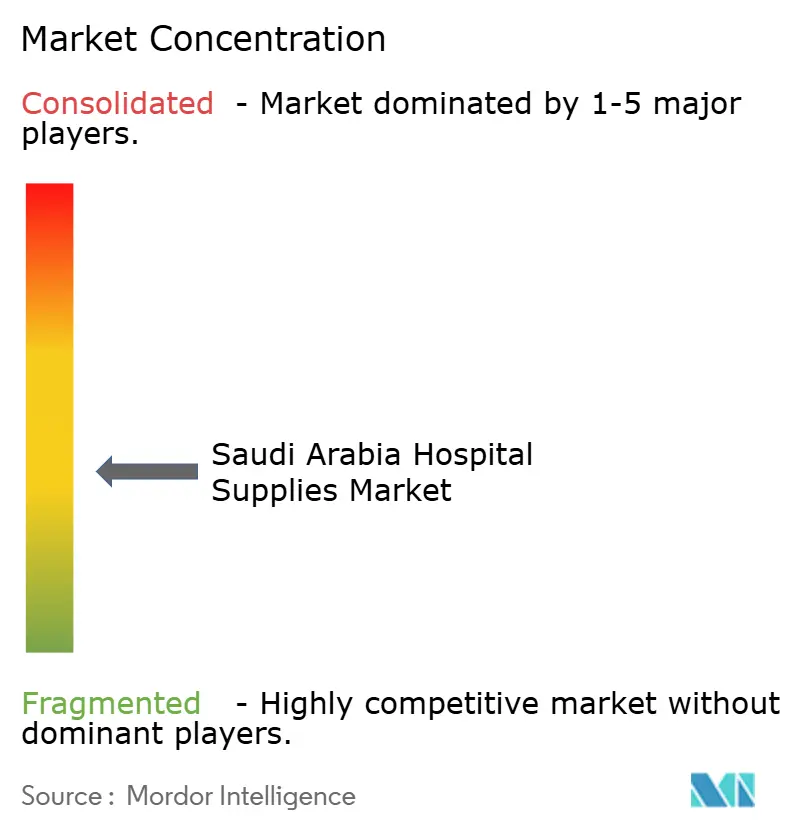

Competition is moderately fragmented. The top five suppliers, Becton Dickinson, 3M, B. Braun, Cardinal Health, and GE Healthcare, collectively hold the largest company share of the revenue. Siemens Healthineers’ SHIFT Innovation Center, inaugurated in 2025, embeds R&D with local clinicians and supports preferential access to tenders for AI-enabled imaging systems. Johnson & Johnson MedTech’s direct presence since 2024 accelerates SFDA approvals and facilitates navigation of pre-qualification hurdles for trauma implants.

Local distributors, such as SOMATCO and Al Ahmad Medical Co., leverage relationships with procurement committees but lack the necessary training infrastructure and IT integration required for long-term contracts. Emerging players like MiCo BioMed fill white spaces in rapid diagnostics with price points 30–40% below imports, aided by a new Jazan facility. Green-economy levies open niches for biodegradable supplies where companies such as Stryker pilot reusable surgical sets that align with waste-diversion targets. Technology adoption differentiates winners; GE Healthcare’s Portrait VSM reduces ICU stay by 1.2 days and cuts supply waste, advantages that translate into stickier contracts within the Saudi Arabia hospital supplies market.

Saudi Arabia Hospital Supplies Industry Leaders

3M

GE Healthcare

Stryker Corporation

B. Braun Melsungen AG

Beckton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Siemens Healthineers inaugurated the SHIFT Innovation Center in Riyadh, a SAR 150 million (USD 40 million) facility co-developing AI diagnostic algorithms with King Saud University and the Ministry of Health, positioning the company to capture preferential access to tenders for next-generation imaging systems.

- April 2025: Becton Dickinson opened a Training & Education Academy in Riyadh, investing SAR 30 million (USD 8 million) to certify 200 healthcare professionals annually on blood-collection systems, infusion pumps, and infection-prevention protocols, strengthening customer retention and supporting Saudization workforce targets.

- March 2025: Alcon launched the first Alcon Experience Center in the Middle East and Africa in Jeddah, a SAR 25 million (USD 6.7 million) training hub for ophthalmologists on phacoemulsification systems and premium intraocular lenses, accelerating adoption of same-day cataract surgery in ambulatory settings.

- February 2025: Sanofi, Sudair Pharma, and NUPCO inaugurated Saudi Arabia's first local insulin manufacturing facility in Riyadh, with annual capacity of 15 million insulin pens covering 70% of domestic demand and reducing import dependency by an estimated SAR 400 million (USD 107 million) annually.

Saudi Arabia Hospital Supplies Market Report Scope

As per the scope of the report, the hospital supplies market of Saudi Arabia encompasses the supply of devices essential to reduce medical errors and improve patient safety in hospitals. These devices are also associated with the protection against hospital-acquired infections (HAIs), including products to maintain proper management of hospital equipment.

The Saudi Arabian hospital supplies market is segmented by product type (operating room equipment, mobility aids and transportation equipment, sterilization and disinfectant products, disposable hospital supplies, syringes and needles, and other product types). The report offers the value (in USD million) for these segments.

By Product Type

| Disposable Hospital Supplies |

| Operating-Room Equipment |

| Sterilization & Disinfectants |

| Mobility Aids & Transportation |

| Other Product Types |

By Application

| Surgical & Trauma Care |

| Wound Management |

| Infection-Control & PPE |

| Other Applications |

By End User

| Hospitals |

| Clinics & Ambulatory Centers |

| Home-Healthcare Providers |

| Long-Term-Care Facilities |

| By Product Type | Disposable Hospital Supplies |

| Operating-Room Equipment | |

| Sterilization & Disinfectants | |

| Mobility Aids & Transportation | |

| Other Product Types | |

| By Application | Surgical & Trauma Care |

| Wound Management | |

| Infection-Control & PPE | |

| Other Applications | |

| By End User | Hospitals |

| Clinics & Ambulatory Centers | |

| Home-Healthcare Providers | |

| Long-Term-Care Facilities |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Saudi Arabia hospital supplies market?

The Saudi Arabia hospital supplies market size stands at USD 16.78 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 5.92% CAGR, reaching USD 22.08 billion by 2031.

Which product segment will grow the quickest?

Operating-room equipment is projected to post the fastest 7.73% CAGR through 2031.

Why is wound management attracting attention?

Diabetes prevalence of 18.5% fuels an 8.23% CAGR in wound-care demand, the highest among applications.

How does Vision 2030 influence procurement?

Vision 2030 funds 27,000 new beds and privatizes hospitals, driving multi-year contracts and performance-based purchasing.