| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 31.02 Billion |

| Market Size (2030) | USD 55.85 Billion |

| CAGR (2025 - 2030) | 12.48 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Saudi Arabia Facility Management Market Analysis

The Saudi Arabia Facility Management Market size is estimated at USD 31.02 billion in 2025, and is expected to reach USD 55.85 billion by 2030, at a CAGR of 12.48% during the forecast period (2025-2030).

The Saudi Arabian facility management industry is experiencing significant transformation driven by technological advancement and economic diversification. According to the International Monetary Fund (IMF), Saudi Arabia's GDP is projected to exceed USD 1,072.44 billion by 2027, indicating robust economic growth that directly influences the facility management sector. The integration of the Internet of Things (IoT) and artificial intelligence has revolutionized facility operations, as evidenced by SIERRA's launch of eFACiLiTY Enterprise FM Software in March 2024, which introduces advanced multilingual AI/ML solutions for streamlined maintenance operations. This technological evolution has enabled facility managers to monitor equipment performance, generate automated work orders, and maintain real-time operational oversight remotely.

The market is witnessing a significant shift toward professional and specialized facility services across various sectors. The Saudi employment-to-population ratio increased to 55.70% in 2022, reflecting growing workforce participation and increasing demand for well-maintained commercial spaces. In August 2023, the Public Investment Fund (PIF) established the Saudi Facility Management Company (FMTECH) to provide comprehensive services including utility management, energy management, waste management, maintenance, housekeeping, security, and landscaping services, demonstrating the government's commitment to professionalizing the sector.

The tourism sector's remarkable expansion has created new opportunities for integrated facility management services. Saudi Arabia recorded a 58% growth in tourist arrivals during the first seven months of 2023 compared to 2019, necessitating enhanced facility management solutions for hospitality infrastructure. The tourism sector's development pipeline includes 23 projects currently under development with a total investment value of SAR 16 billion (USD 4.26 billion), indicating substantial growth potential for facility management services in the hospitality sector.

Regulatory developments are reshaping the facility management landscape in Saudi Arabia. In October 2023, the Real Estate General Authority announced plans to implement the country's first facility management regulation in 2024, under the initiative "Facility Management in the Digital Age – Towards Adopting a Smart Future." This regulatory framework aims to standardize facility management operations and promote the adoption of smart technologies. The integration of advanced security technologies, including biometrics, facial recognition, and access control systems, along with energy-efficient solutions and waste management strategies, is becoming increasingly prevalent across various sectors, reflecting the industry's evolution toward more sophisticated and sustainable facility management practices.

Saudi Arabia Facility Management Market Trends

Infrastructure Development and Growing Real Estate Sector

Saudi Arabia's robust infrastructure development is primarily driven by significant government investments and ambitious development projects across various sectors. The Ministry of Finance's substantial budget allocation of SAR 34 billion (USD 9.06 billion) for housing, infrastructure, and transportation sectors in FY 2023 demonstrates the government's commitment to infrastructure development. This investment surge has created extensive opportunities for facility management services across new commercial buildings, residential complexes, and mega-projects like NEOM, which represents a USD 500 billion industrial zone development powered by renewable energy and focused on sectors including energy, water, biotechnology, food, and advanced manufacturing.

The real estate sector's growth is further evidenced by the rapid expansion of hospitality infrastructure and commercial developments. According to Tophotelprojects.com, Saudi Arabia had 167 planned hotel development projects in 2022, with 24% scheduled for completion by 2025. The tourism sector's increasing contribution, reaching 4.45% of GDP as of June 2023, has catalyzed substantial investments in hospitality infrastructure. This growth is supported by the government's commitment to invest over USD 800 million in the tourism sector over the upcoming decade, creating additional demand for comprehensive facility management services across new developments and existing properties.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Outsourcing Trend and Supporting Government Initiatives

The Saudi Arabian market is experiencing a significant shift toward outsourcing facility management services, supported by government initiatives and Vision 2030's economic diversification goals. This trend is exemplified by recent major industrial developments, such as the October 2023 partnership between Hyundai and Saudi Arabia's Public Investment Fund (PIF) to establish an automobile manufacturing facility with an annual production capacity of 50,000 vehicles. Such large-scale industrial projects require specialized facility services, driving the trend toward outsourcing these critical functions to experienced service providers.

The government's proactive approach in supporting industrial development is further demonstrated by recent initiatives in various sectors. In November 2023, the establishment of Vedanta Copper International (VCI) Business Limited through a SAR 1 million investment showcases the growing industrial base requiring professional facility management services. Additionally, the tourism sector's development, with 23 projects currently under development worth SAR 16 billion (USD 4.26 billion), reflects the government's commitment to creating opportunities for facility services providers across diverse sectors.

Emphasis on Green and Sustainable Building Practices

Saudi Arabia's commitment to sustainable development and green building practices has become a significant driver in the facility management market, particularly through initiatives aligned with Vision 2030's environmental goals. The development of NEOM, powered entirely by renewable energy, represents a landmark shift toward sustainable infrastructure development in the country. This mega-project, along with other sustainable development initiatives, has created increased demand for building services that can implement and maintain environmentally conscious building practices.

The industrial sector's transformation toward sustainability is evidenced by the integration of advanced control systems and automation in infrastructure development, particularly in manufacturing facilities embracing Industry 4.0 principles. This shift requires building maintenance services to adapt to new environmental standards and implement energy-efficient solutions across industrial, commercial, and residential properties. The focus on sustainable practices is further reinforced by the government's support for projects that incorporate renewable energy sources and environmentally friendly building materials, creating a new paradigm in facility management services that prioritizes environmental stewardship alongside operational efficiency.

Segment Analysis: By Type of Facility Management

Outsourced Facility Management Segment in Saudi Arabia FM Market

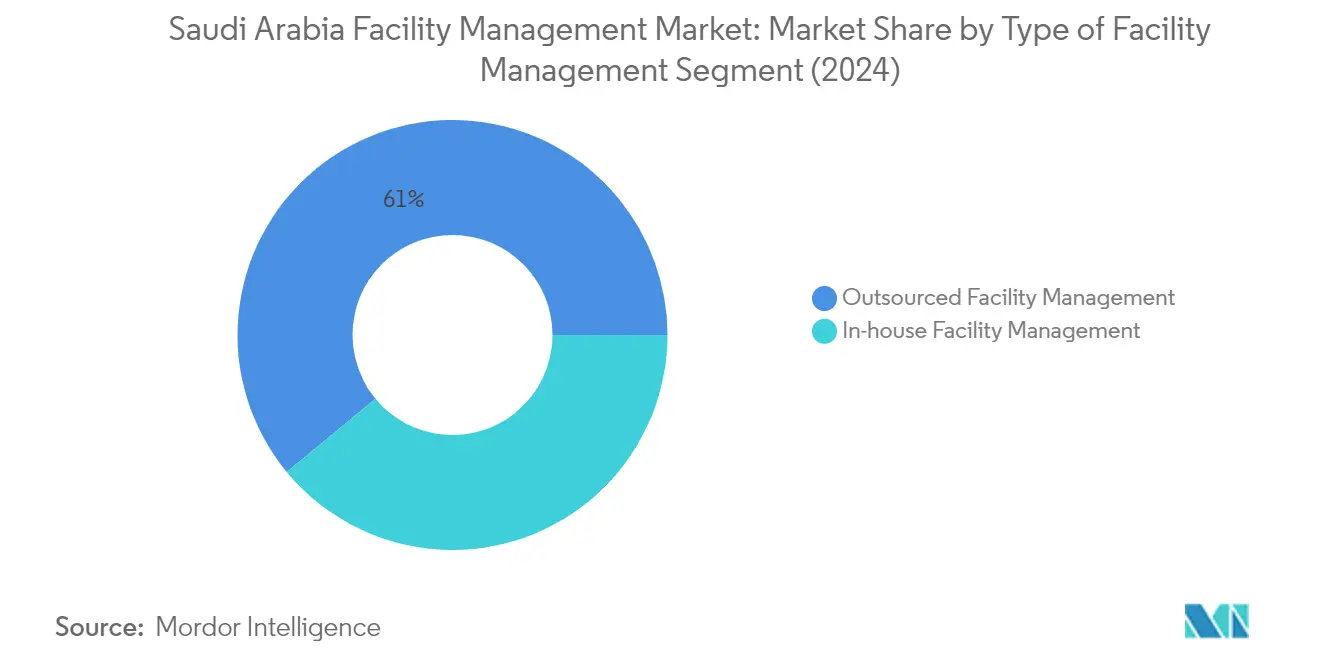

The outsourced facility management segment dominates the Saudi Arabia facility management market, holding approximately 61% of the market share in 2024. This significant market position is driven by the increasing trend of businesses outsourcing their non-core activities to specialized service providers. The segment encompasses various service delivery models, including single FM, bundled FM, and integrated FM solutions, catering to diverse industry needs across commercial, retail, industrial, and government sectors. The growth in this segment is particularly notable in major cities like Riyadh, Jeddah, Makkah, and the Dammam Metropolitan Area, where organizations are increasingly recognizing the benefits of outsourcing facility management services to improve operational efficiency and reduce costs.

In-house Facility Management Segment in Saudi Arabia FM Market

The in-house facility management segment is emerging as the fastest-growing segment in the Saudi Arabia facility management market, projected to grow at approximately 12% during the forecast period 2024-2029. This robust growth is primarily attributed to the increasing focus on maintaining direct control over critical facility operations, particularly in sectors where security and compliance are paramount. The segment's growth is further supported by government initiatives such as Saudi Vision 2030, which emphasizes infrastructure development and the modernization of facilities across various sectors. Organizations are increasingly investing in developing their internal facility management capabilities, incorporating advanced technologies and sustainable practices to enhance operational efficiency and maintain better control over their facilities.

Segment Analysis: By Offering Type

Hard Facility Management Segment in Saudi Arabia Facility Management Market

The hard facility management segment dominates the Saudi Arabia facility management market, holding approximately 55% market share in 2024. This segment encompasses critical services such as mechanical, electrical, plumbing, preventive maintenance, structural maintenance, HVAC, and asset management services that directly impact the physical infrastructure of buildings. The segment's prominence is driven by the increasing demand for on-site electrical and mechanical solutions in both commercial and industrial sectors, making electromechanical and operational maintenance a significant revenue contributor. The implementation of fire and security systems, which are mandatory in every structure, has further strengthened this segment's position. The rise in construction activities across Saudi Arabia and the growing adoption of sustainable energy consumption practices have also contributed to the segment's market leadership, as organizations increasingly focus on optimizing their building systems and building maintenance.

Soft Facility Management Segment in Saudi Arabia Facility Management Market

The soft facility management segment is emerging as the fastest-growing segment in the Saudi Arabia facility management market, projected to grow at approximately 11% CAGR from 2024 to 2029. This remarkable growth is primarily driven by the expanding healthcare and education sectors in Saudi Arabia, where maintaining strict safety and cleanliness regulations is paramount. The segment's growth is further accelerated by the Saudi Arabian government's significant investment in healthcare, which accounted for USD 36.8 billion of its 2022 budget. The education sector's transformation, with the development of new facilities and infrastructure, has created additional demand for soft facility management services. The increasing focus on consumer experience in commercial spaces and the growing importance of sustainable practices have also contributed to the segment's rapid expansion, as evidenced by recent partnerships like Motakamila's collaboration with Cool Inc. to deliver professional services to Via Riyadh venues, offices, and restaurants.

Segment Analysis: By End-User Industry

Commercial and Retail Segment in Saudi Arabia Facility Management Market

The commercial facility management segment dominates the Saudi Arabia facility management market, commanding approximately 43% market share in 2024. This segment's prominence is primarily driven by Saudi Arabia's Vision 2030 initiatives aimed at transforming the country's economy through diversification and promoting non-oil-based sectors. The segment encompasses various facilities, including office buildings occupied by business services, corporate offices of manufacturers, IT and telecommunication companies, finance and insurance firms, convenience stores, and multichannel retail establishments. The retail industry in Saudi Arabia is witnessing an ever-growing demand for facility management as key industry players and manufacturers increasingly look at innovative products, with most retailers making considerable strides to embrace technology for enhancing retail experiences. Commercial spaces require comprehensive facility services, including property accounting, renting, contract management, procurement management, and several other specialized services, making professional facility management essential for optimal operations.

Manufacturing and Industrial Segment in Saudi Arabia Facility Management Market

The industrial facility management segment is projected to be the fastest-growing segment in the Saudi Arabia facility management market, with an expected growth rate of approximately 11% during 2024-2029. This robust growth is attributed to Saudi Arabia's position as one of the fastest-growing manufacturing industries in the region, supported by anchor projects by the government, low taxes, and business-friendly regulations favoring automation and advancement of the manufacturing sector. The segment covers major applications across various industries, including food and beverage, electronics, automotive, mining, and oil and gas industries. The focus on Industry 4.0 indicates the sector's readiness to adopt new technologies to boost production output at better quality, further augmenting the growth of facility management services. The manufacturing sector's emphasis on workplace safety, environmental regulations compliance, and efficient facility management is driving increased demand for both hard facility management and soft facility management services.

Remaining Segments in End-User Industry

The other significant segments in the Saudi Arabia facility management market include Government, Infrastructure, and Public Entities, Institutional, and Other End-User Industries. The Government segment is particularly notable due to its strategic importance in Saudi Arabia's development plans and mega-projects. The Institutional segment, comprising healthcare and education sectors, plays a crucial role in supporting the country's social infrastructure development. These segments are benefiting from various government initiatives, including smart city developments, healthcare sector expansion, and educational facility improvements. The implementation of advanced technologies, increasing focus on sustainability, and the growing trend toward outsourcing facility management services are common drivers across these segments, contributing to the overall market growth and development of the facility management industry in Saudi Arabia.

Saudi Arabia Facility Management Industry Overview

Top Companies in Saudi Arabia Facility Management Market

The facility management market in Saudi Arabia is characterized by established players demonstrating strong innovation capabilities and strategic growth initiatives. Companies are increasingly investing in digital transformation and automation technologies, including IoT platforms, smart building solutions, and predictive maintenance systems to enhance service delivery and operational efficiency. The competitive landscape shows a clear trend toward developing integrated facility management solutions that combine both hard and soft facility services under single contracts. Market leaders are expanding their geographical presence across major cities while simultaneously diversifying their service portfolios to include specialized offerings like energy management and sustainability solutions. Strategic partnerships and collaborations with international players are becoming increasingly common as companies seek to enhance their technical capabilities and service quality. Additionally, firms are placing greater emphasis on developing local talent and implementing Saudization initiatives in alignment with Vision 2030 objectives.

Market Structure Shows Dynamic Competitive Environment

The Saudi facility management market exhibits a mix of well-established international corporations and strong local players, with both types of companies wielding significant market influence. Local conglomerates have leveraged their deep understanding of regional requirements and established relationships with government entities to maintain strong market positions, while international players bring advanced technological capabilities and global best practices to the market. The industry is experiencing gradual consolidation through strategic acquisitions and joint ventures, particularly as larger players seek to expand their service offerings and geographical coverage. The establishment of the Saudi Facility Management Company (FMTECH) by the Public Investment Fund represents a significant development in market structure, indicating increased government focus on developing the sector.

The competitive dynamics are further shaped by the presence of specialized service providers focusing on specific segments such as cleaning, security, or technical maintenance, alongside integrated facility management providers offering comprehensive solutions. Market participants are increasingly pursuing vertical integration strategies to enhance control over service delivery and improve operational efficiency. The industry has witnessed several notable mergers and acquisitions, with larger players acquiring specialized service providers to expand their capabilities and market reach. This consolidation trend is expected to continue as companies seek to achieve economies of scale and enhance their competitive positioning in the market.

Innovation and Integration Drive Future Success

Success in the Saudi facility management market increasingly depends on companies' ability to embrace technological innovation and deliver integrated solutions that address evolving customer needs. Incumbent players must focus on developing sophisticated service offerings that incorporate smart building technologies, energy management solutions, and sustainable practices to maintain their market positions. The ability to provide data-driven insights through advanced analytics and reporting capabilities is becoming crucial for competitive advantage. Companies need to invest in workforce development and training programs to ensure service quality while maintaining compliance with Saudization requirements. Additionally, establishing strong relationships with key stakeholders across various sectors, particularly in government and commercial segments, remains vital for sustained growth.

Market contenders can gain ground by focusing on specialized service niches or developing innovative solutions that address specific customer pain points. The increasing emphasis on environmental sustainability and energy efficiency presents opportunities for companies to differentiate themselves through green building solutions and sustainable facility management practices. Success also depends on the ability to navigate regulatory requirements and adapt to changing market conditions, particularly as Saudi Arabia continues to implement economic reforms under Vision 2030. Companies must carefully consider end-user concentration risks by diversifying their client base across multiple sectors and geographical regions. The development of strong vendor management capabilities and efficient supply chain processes will become increasingly important as the market continues to evolve.

Saudi Arabia Facility Management Market Leaders

-

Initial Saudi Group (Alesayi Holding)

-

Almajal G4S (Atlas Ontario LP)

-

Emcor Saudi Company Limited

-

SETE Energy Saudia for Industrial Projects Ltd (SETE Saudia)

-

ZOMCO (Zamil Operations & Maintenance) (Zamil Group)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Saudi Arabia Facility Management Market News

- May 2024: Diriyah Square is set to welcome a premium office development as The Diriyah Company breaks ground, further diversifying its infrastructure portfolio for the business community. Emphasizing sustainability, the five low-rise office buildings will collectively offer close to 39,000 square meters of gross leasable area (GLA) and an expansive gross floor area (GFA) nearing 47,000 square meters.

- March 2024: SIERRA launched its eFACiLiTY Enterprise Facility Management Software, claiming it to be the world's most comprehensive Computer-Aided Facilities Management (CAFM) and Integrated Workplace Management System (IWMS). Operating on a Software as a Service (SaaS) subscription model, the software is hosted on Microsoft Azure. Additionally, it features the eFACiLiTY Virtual Assistant, a sophisticated multilingual AI/ML solution powered by the Maintenance Guru. This smart tool identifies issues by sifting through the knowledge base and simplifies the generation of accurate work orders with just one click.

- February 2024: Saudi Arabia's Real Estate General Authority (REGA) has launched its inaugural Facility Management (FM) service, aiming to revolutionize the country's housing sector. This initiative is designed to enhance the quality of life for residents through the effective management of residential communities.

Saudi Arabia Facility Management Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

-

4.4 Base Indicator Analysis

- 4.4.1 Construction Activities in Saudi Arabia

- 4.4.2 Expansion of Key International FM Services

- 4.4.3 Commercial Real Estate Sector in the Region

- 4.4.4 Office Supply Uptake and Occupancy Rates

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Demand For IFM and Outsourcing of Non-core Operations From Emerging Verticals

- 5.1.2 Emphasis on Green and Sustainable Building Practices

- 5.1.3 Renewed Emphasis on Workplace Optimization and Productivity

- 5.1.4 Giga and Megaprojects in KSA Driving the Demand For Fm Services

-

5.2 Market Challenges

- 5.2.1 Cost Optimization Problems

- 5.2.2 Lack of Specialized Talents

- 5.2.3 Growing Competition Expected to Impact Profit Margins of Existing Vendors

6. MARKET SEGMENTATION

-

6.1 Service Type

- 6.1.1 Hard Service

- 6.1.1.1 Asset Management

- 6.1.1.2 MEP and HVAC Services

- 6.1.1.3 Fire Systems and Safety

- 6.1.1.4 Other Hard FM Services

- 6.1.2 Soft Service

- 6.1.2.1 Office Support and Security

- 6.1.2.2 Cleaning Services

- 6.1.2.3 Catering Services

- 6.1.2.4 Other Soft FM Services

-

6.2 Offering Type

- 6.2.1 In-House

- 6.2.2 Outsourced

- 6.2.2.1 Single FM

- 6.2.2.2 Bundled FM

- 6.2.2.3 Integrated FM

-

6.3 End-user Industry

- 6.3.1 Commercial, Retail, and Restaurants

- 6.3.2 Manufacturing And Industrial

- 6.3.3 Government, Infrastructure, And Public Entities

- 6.3.4 Institutional

- 6.3.5 Other End-user Industries

-

6.4 Region

- 6.4.1 Riyadh

- 6.4.2 Makkah

- 6.4.3 Eastern Province

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Initial Saudi Group (Alesayi Holding)

- 7.1.2 Emcor Saudi Company Limited

- 7.1.3 Almajal G4S (Allied Universal)

- 7.1.4 SETE Energy Saudia for Industrial Projects Ltd (SETE Saudia)

- 7.1.5 ZOMCO (Zamil Operations & Maintenance) (Zamil Group)

- 7.1.6 SAMAMA Holding Group

- 7.1.7 Khidmah Sole Proprietorship LLC (Aldar Properties PJSC)

- 7.1.8 ENGIE Solutions (Engie Group)

- 7.1.9 Nesma United Industries Co. Ltd

- 7.1.10 AL-YAMAMA Group

- 7.1.11 Olive Arabia Co. Ltd

- 7.1.12 Tamimi Group

- 7.1.13 Facilities Management Company (FMCO)

- 7.1.14 Al Suwaidi Holding Company KSA

- 7.1.15 Enova Facilities Management Services LLC

- 7.1.16 Saudi Binladin Group - Operation and Maintenance

- 7.1.17 Musanadah Facilities Management Company (Alturki Holding)

- 7.1.18 Seder Group

- 7.1.19 Jash Holding LLC

- 7.1.20 El Seif Operation and Maintenance (ESOM)

- *List Not Exhaustive

8. VENDOR POSITIONING ANALYSIS

9. FUTURE OUTLOOK OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Saudi Arabia Facility Management Industry Segmentation

Facility management services involve building upkeep, utilities, maintenance operations, waste services, and security. These services are divided into hard and soft facility management services. Hard services comprise mechanical and electrical maintenance, fire safety and emergency services, building management system controls, elevator and lift maintenance, and conveyor maintenance. Soft services include cleaning, recycling, security, pest control, handyperson services, ground maintenance, and waste disposal.

The Saudi Arabia facility management market is segmented by service type (hard service (asset management, MEP and HVAC services, fire systems and safety, and other hard FM services), soft services (office support and security, cleaning services, catering services, and other soft FM services)), offering type (in-house, outsourced [single FM, bundled FM, integrated FM]), and end-user industry (commercial and retail and restaurants, manufacturing and industrial, government, infrastructure and public entities, institutional, and other end-user industries), region (Riyadh, Makkah, Eastern Province, Rest of Saudi Arabia). The Report Offers the Market Size in Value Terms in USD for all the Abovementioned Segments.

| Service Type | Hard Service | Asset Management | |

| MEP and HVAC Services | |||

| Fire Systems and Safety | |||

| Other Hard FM Services | |||

| Soft Service | Office Support and Security | ||

| Cleaning Services | |||

| Catering Services | |||

| Other Soft FM Services | |||

| Offering Type | In-House | ||

| Outsourced | Single FM | ||

| Bundled FM | |||

| Integrated FM | |||

| End-user Industry | Commercial, Retail, and Restaurants | ||

| Manufacturing And Industrial | |||

| Government, Infrastructure, And Public Entities | |||

| Institutional | |||

| Other End-user Industries | |||

| Region | Riyadh | ||

| Makkah | |||

| Eastern Province | |||

Need A Different Region or Segment?

Customize Now

Saudi Arabia Facility Management Market Research FAQs

How big is the Saudi Arabia Facility Management Market?

The Saudi Arabia Facility Management Market size is expected to reach USD 31.02 billion in 2025 and grow at a CAGR of 12.48% to reach USD 55.85 billion by 2030.

What is the current Saudi Arabia Facility Management Market size?

In 2025, the Saudi Arabia Facility Management Market size is expected to reach USD 31.02 billion.

Who are the key players in Saudi Arabia Facility Management Market?

Initial Saudi Group (Alesayi Holding), Almajal G4S (Atlas Ontario LP), Emcor Saudi Company Limited, SETE Energy Saudia for Industrial Projects Ltd (SETE Saudia) and ZOMCO (Zamil Operations & Maintenance) (Zamil Group) are the major companies operating in the Saudi Arabia Facility Management Market.

What years does this Saudi Arabia Facility Management Market cover, and what was the market size in 2024?

In 2024, the Saudi Arabia Facility Management Market size was estimated at USD 27.15 billion. The report covers the Saudi Arabia Facility Management Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Saudi Arabia Facility Management Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Saudi Arabia Facility Management Market Research

Mordor Intelligence provides comprehensive insights into the FM and facility management industry. Our detailed analysis and consulting expertise cover the complete spectrum of facility services. This includes building maintenance, workplace management, and space management solutions. The report offers in-depth coverage of both soft facility management and hard facility management segments. It also addresses crucial aspects of building operations and facility operations. Our analysis spans industrial facility management, commercial facility management, and residential facility management sectors. This offers stakeholders a complete view of the Saudi Arabian market landscape.

The report, available as an easy-to-download PDF, equips decision-makers with actionable insights into integrated facility management trends and opportunities. Stakeholders gain valuable understanding of property management and asset management dynamics. Detailed sections on facility maintenance, building services, facility cleaning, and facility security provide operational guidance. The research supports strategic planning across total facility management and corporate facility management initiatives. This enables organizations to optimize their facility management approaches and enhance operational efficiency in the Saudi Arabian market.