Saudi Arabia Chocolate Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.23 Billion |

| Market Size (2030) | USD 1.53 Billion |

| Growth Rate (2025 - 2030) | 4.46% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Chocolate Market Analysis by Mordor Intelligence

The chocolate market in Saudi Arabia is projected to grow from USD 1.23 billion in 2025 to USD 1.53 billion by 2030, registering a CAGR of 4.46% during this period. The market's growth is driven by he rise in religious tourism, the strong cultural tradition of gifting, and the increasing adoption of Western snacking habits. Advancements in cold-chain infrastructure, improvements in premium packaging, and innovations such as date-based chocolate fillings are transforming the competitive landscape. By product type, dark chocolate is gaining popularity due to its perceived health benefits. In terms of form, pralines and truffles are gaining popularity as they align with the gifting culture. The premium price segment is growing faster than the mass-market segment, reflecting a shift in consumer preferences toward higher-quality products. Plant-based ingredients are also gaining traction as consumers seek healthier and more sustainable options. Online retail is emerging as a significant distribution channel, driven by the convenience it offers to consumers. The Saudi Arabian chocolate market is moderately consolidated, with a few key players dominating the competitive landscape.

Key Report Takeaways

- By product type, milk and white chocolate held 68.45% of the 2024 volume, while dark chocolate is projected to expand at a 5.73% CAGR through 2030.

- By form, tablets and bars led the Saudi Arabian chocolate market with a 64.36% share in 2024; pralines and truffles are forecast to grow at a 5.83% CAGR through 2030.

- By price range, mass-market offerings accounted for 72.84% of 2024 sales, while premium chocolate is projected to advance at a 6.48% CAGR between 2025 and 2030.

- By ingredient type, dairy-based formulations accounted for 65.92% of the 2024 volume, whereas plant-based chocolate is expected to grow at a 5.39% CAGR through 2030.

- By distribution channel, supermarkets/hypermarkets maintained 60.82% volume share in 2024; online retail is projected to expand at a 9.26% CAGR through 2030.

Saudi Arabia Chocolate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pilgrim tourism during Hajj and Umrah boost seasonal spikes | +0.6% | National, concentrated in Makkah, Madinah, and Jeddah travel corridors | Short term (≤ 2 years) |

| Innovations with date, saffron, pistachio-chocolate hybrids due to Saudi Arabia's cultural connection | +0.5% | National, with premium positioning in Riyadh, Jeddah, and Eastern Province urban centers | Medium term (2-4 years) |

| Strong gifting culture and festive occasions | +0.7% | National, peaking during Ramadan, Eid al-Fitr, Eid al-Adha, and National Day | Short term (≤ 2 years) |

| Strengthening demand for luxury packaging | +0.4% | National, skewed toward high-income districts in Riyadh, Jeddah, and Khobar | Medium term (2-4 years) |

| Increasing acceptance of Western snacking habits | +0.5% | National, led by youth demographics in major cities | Long term (≥ 4 years) |

| Celebrity and influencer endorsements shaping brand perception | +0.3% | National, amplified via social media platforms targeting Gen Z and millennials | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pilgrim tourism during Hajj and Umrah boost seasonal spikes

Pilgrim tourism creates significant seasonal spikes in Saudi Arabia’s chocolate demand, especially during the Hajj period. In 2025, the Kingdom welcomed 1,673,230 Hajj pilgrims, with 1,506,576 of them being international visitors, according to Data Saudi[1]Source: Data Saudi, "Overview", datasaudi.sa. This influx of pilgrims generates a short but intense period of high demand, as many visitors purchase locally made chocolates to take back as gifts and souvenirs. To capitalize on this opportunity, airports, hotels, and souvenir shops expand their offerings of halal-certified and premium-priced chocolate assortments. The Air Connectivity Program, which increases flight capacity, has further boosted the number of impulse buyers. Retailers prepare for this seasonal surge by stocking up on inventory in advance, even though it requires a higher level of working capital. This strategy enables them to maximize revenue during the Hajj season, a crucial period for chocolate sales in the country.

Increasing acceptance of Western snacking habits

Urbanization and increased exposure to global media are changing how people in Saudi Arabia consume chocolate. What was once primarily a ceremonial treat is now becoming a popular everyday snack. In 2023, Saudi Arabia imported USD 140 million worth of chocolate products, making it the 11th-largest chocolate importer globally, according to the Observatory of Economic Complexity[2]Source: Observatory of Economic Complexity, "Chocolate Products (Contains Cocoa, Over 2kg)", oec.world. This highlights the growing influence of Western snacking habits in the country. Products like Kinder Joy, with its portion-controlled and novelty design, have gained significant popularity, especially among younger consumers. Mars has adapted its well-known brands, such as Galaxy, Snickers, and M&M’s, to suit local tastes by producing them at its facility in King Abdullah Economic City. Over the past decade, vending machines, which were once rare in locations such as malls, universities, and offices, have become increasingly common.

Innovations with date, saffron, pistachio-chocolate hybrids due to Saudi Arabia’s cultural connection

Saudi Arabia’s confectionery market is evolving rapidly as brands combine traditional local ingredients, such as dates, saffron, and pistachios, with cocoa to create premium and innovative chocolate products. Dates, in particular, are gaining popularity due to their rich composition of natural sugars, minerals, vitamins, dietary fiber, protein, and antioxidants, including carotenoids and phenolics, as highlighted in a ScienceDirect publication from December 2024[3]Source: ScienceDirect, "Nutritional, Nutraceutical Attributes, Microbiological and Chemical Safety of Different Varieties of Dates—A review", sciencedirect.com. These qualities make dates an attractive ingredient for healthier chocolate options. Social media trends, such as the rise of pistachio-stuffed “Dubai chocolate", are influencing consumer preferences, allowing local chocolatiers to charge higher prices for unique creations. For instance, in August 2025, Petit Gourmet introduced a 470 g “Pistachio Kunafa Chocolate” in collaboration with Kreol Travel Retail and Lagardère Travel Retail at Riyadh’s King Khalid International Airport.

Strong gifting culture and festive occasions

Saudi Arabia’s gift-giving culture plays a significant role in driving seasonal demand for premium chocolates, especially during key occasions such as Ramadan, Eid al-Fitr, and Eid al-Adha. During these times, hypermarkets, specialty boutiques, and gifting stores offer beautifully designed chocolate gift boxes and customized hampers. These often feature intricate details such as gold-foil accents and personalized calligraphy, making them highly appealing for festive gifting. For example, the Bateel dates and chocolates gift box has become a popular choice, demonstrating how premium hampers have become a key part of celebrations. Ferrero Rocher also remains a top favorite during Ramadan due to its elegant packaging and luxurious feel. The market caters to a wide range of preferences, with mass-market promotions running alongside exclusive boutique offerings, creating diverse options in terms of price and presentation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for low-sugar and low-calorie diets | -0.5% | National, concentrated among health-conscious urban populations | Medium term (2-4 years) |

| Storage and logistics costs due to extremely high temperatures in Saudi Arabia | -0.4% | National, acute in inland regions with temperatures exceeding 50°C | Short term (≤ 2 years) |

| Competition from healthier snack alternatives | -0.3% | National, driven by availability of protein bars, nuts, and dried fruits | Medium term (2-4 years) |

| Cultural preferences for traditional sweets | -0.3% | National, strongest in rural areas and among older demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cultural preferences for traditional sweets

Traditional sweets, such as kunafa, maamoul, and baklava, remain deeply ingrained in Saudi Arabian culture, especially during Ramadan, which reduces the demand for chocolate during this period. In 2023, the designation of maqshush as the national dessert further highlighted the strong preference for local flavors. According to research from Qassim University, pastries made with dates continue to enjoy high consumer acceptance, making them a strong competitor to chocolate. Additionally, fusion desserts such as pistachio-chocolate baklava and Nutella-filled kunafa are gaining popularity. However, these products often replace pure chocolate consumption rather than increasing the overall demand for confectionery. This trend creates a challenge for the chocolate market, as it limits its growth potential in the region.

Growing consumer preference for low-sugar and low-calorie diets

Health awareness is increasingly affecting chocolate consumption in Saudi Arabia. According to the International Diabetes Federation, 23.1% of adults in the country have diabetes[4]Source: International Diabetes Federation, "Saudi Arabia", idf.org. The Ministry of Health’s “Healthy Food Strategy” has introduced front-of-pack labeling rules, encouraging consumers to reduce their sugar intake. In response, retailers have expanded their offerings of sugar-free and stevia-sweetened chocolates. Dark chocolate, often seen as a healthier option due to its lower sugar content and higher cocoa percentage, is also gaining popularity. However, many health-conscious consumers are shifting away from traditional chocolates altogether. Instead, they are opting for alternatives like nuts, protein bars, and date-based snacks, which are perceived as more natural and nutritious.

Segment Analysis

By Product Type: Dark Chocolate Gains on Health Halo

Milk and white chocolate are the most preferred types in the Saudi Arabia market, contributing to 68.45% of total sales in 2024. The local preference for sweeter flavors, combined with the easy availability of these chocolates in hypermarkets, convenience stores, and gift shops, drives this strong preference. Brands also play a key role by consistently introducing new flavors and enhancing packaging to attract consumers. Festive seasons like Ramadan and Eid significantly boost the demand for these chocolates, making them a major source of revenue for manufacturers.

Dark chocolate, although holding a smaller share of the market, is steadily gaining traction as more consumers opt for healthier alternatives. This segment is expected to grow at a 5.73% CAGR through 2030, fueled by increasing demand for chocolates with higher cocoa content, antioxidant benefits, and lower sugar levels. Government regulations, such as the Ministry of Health’s front-of-pack labeling, have made nutritional information more transparent, encouraging healthier choices. Retailers are expanding their dark chocolate selections to cater to urban, health-conscious consumers who view it as a more guilt-free indulgence.

By Form: Pralines and Truffles Ride Gifting Wave

Tablets and bars are the most popular chocolate types in Saudi Arabia, making up 64.36% of the total demand in 2024. Their widespread popularity is due to their affordability and easy availability in stores like hypermarkets and convenience outlets. These chocolates are suitable for both casual snacking and gifting, making them a versatile choice for consumers. Regular promotional offers and a steady supply further enhance their appeal. Their familiarity and accessibility ensure they remain a favorite among people of all age groups, securing their strong position in the market.

Pralines and truffles, while holding a smaller share of the market, are expected to grow at a faster rate with a projected CAGR of 5.83% through 2030. This growth is largely driven by the increasing demand for premium chocolates, especially for gifting occasions. Their elegant packaging and luxurious designs make them highly appealing to consumers looking for high-quality options. Additionally, their visually attractive presentation aligns with social media trends, such as unboxing videos, which adds to their popularity. As consumers continue to seek indulgent and premium chocolate experiences, pralines and truffles are well-positioned for significant growth in the coming years.

By Price Range: Premium Segment Outpaces Mass Market

In 2024, mass-market chocolate products made up 72.84% of the total market volume, highlighting their strong popularity in Saudi Arabia. These chocolates are widely available in supermarkets, hypermarkets, and convenience stores, making them easily accessible for everyday purchases. Their affordability and frequent discounts make them a practical choice for families and individuals looking for budget-friendly options. The familiarity of well-known brands and their consistent availability through a strong distribution network further reinforce their dominance in the market.

Premium chocolate, although a smaller segment, is expected to grow much faster, with a projected CAGR of 6.48% through 2030. This growth is driven by increasing demand for chocolates made with high-quality ingredients and presented in luxurious packaging. Premium chocolates are often chosen for gifting, as they align with the cultural tradition of giving thoughtful and elegant gifts. Social media trends showcasing luxury products have also influenced consumer preferences, encouraging more people to opt for premium chocolates. As a result, this segment is expected to capture a larger share of the market's value in the years to come.

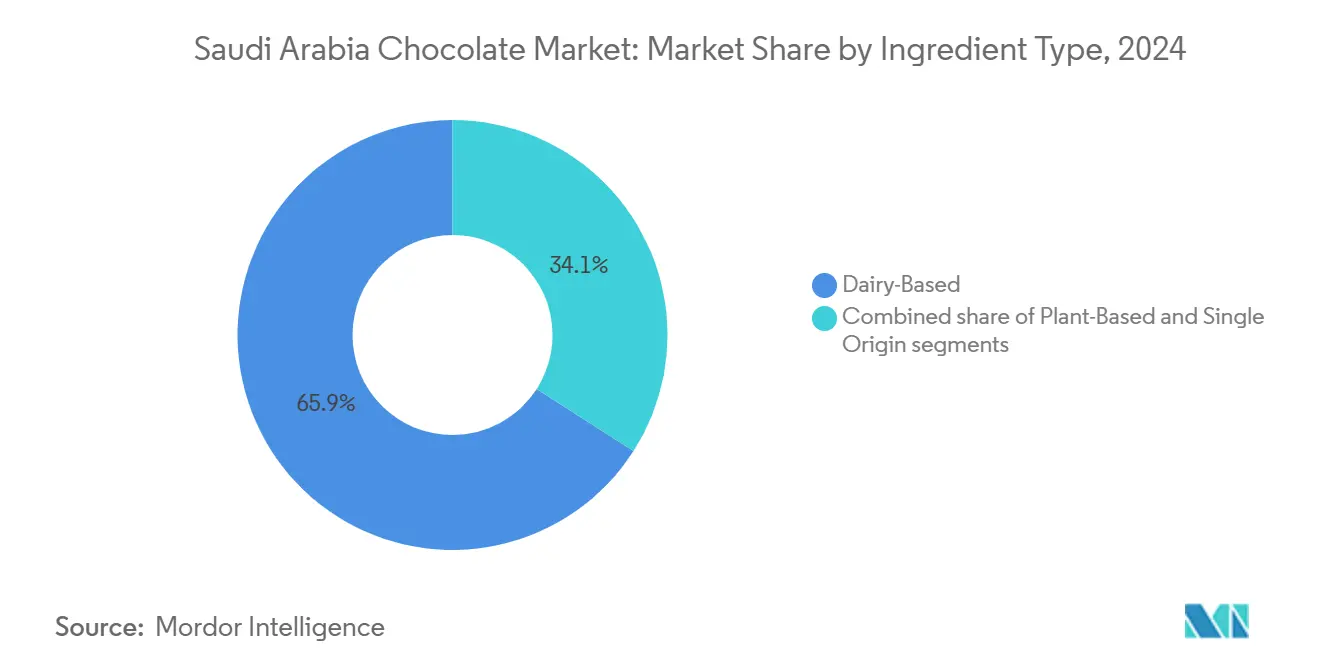

By Ingredient Type: Plant-Based Gains Traction

Dairy-based chocolate recipes accounted for 65.92% of the total market volume in 2024, making them the most popular choice among consumers in Saudi Arabia. This preference is largely due to the creamy and rich texture that dairy-based chocolates provide, which aligns well with local tastes. These products are widely available in retail outlets, including supermarkets and gift stores, ensuring easy access for consumers. Leading brands continue to focus on dairy-based chocolates to meet the strong demand and maintain their competitive edge in the market.

Meanwhile, plant-based chocolates, though currently a smaller segment, are expected to grow at a CAGR of 5.39% through 2030. This growth is being driven by increasing awareness of lactose intolerance and a gradual shift toward vegan or dairy-free diets. Consumers are showing interest in alternatives made from ingredients like oats, almonds, and coconuts, especially in premium product categories. While dairy-based chocolates are likely to remain dominant, the rising focus on health and wellness is creating opportunities for plant-based options to attract younger and more health-conscious buyers.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Retail Surges

In 2024, supermarkets/hypermarkets were the leading channels for chocolate sales in Saudi Arabia, accounting for 60.82% of the total market volume. These stores are highly preferred due to their convenient locations and the wide variety of chocolate products they offer. They attract customers with features like refrigerated displays that keep chocolates fresh, promotional discounts that make products more affordable, and dedicated sections for seasonal gifting. Placing chocolates near checkout counters encourages shoppers to make impulse purchases, further driving sales in these outlets.

Although online sales currently make up a smaller portion of the market, they are expected to grow significantly, with a projected CAGR of 9.26% through 2030. This growth is fueled by the increasing use of smartphones, which makes online shopping more accessible, as well as faster delivery options like same-day and next-day services. Subscription models for premium and specialty chocolates are also gaining popularity, offering consumers convenience and variety. As more people prioritize ease and flexibility, online platforms are likely to attract younger, tech-savvy shoppers who enjoy browsing and purchasing chocolates from the comfort of their homes.

Geography Analysis

The cities of Makkah, Madinah, and Jeddah experience a sharp rise in chocolate demand during the Ramadan and Hajj seasons, largely due to the large number of religious tourists. Retail kiosks in these areas often charge higher prices, and halal certification is essential for all products sold. In contrast, Riyadh and the Eastern Province dominate premium chocolate sales, driven by higher income levels and a significant expatriate population. Consumers in these regions prefer luxury items, such as single-origin chocolate bars and boutique truffles, which can cost up to SAR 150 per box. In 2024, Saudi Arabia imported over 123 million kilograms of chocolate, highlighting its reliance on imports despite efforts under Vision 2030 to boost local food production through investments of SAR 1 trillion in manufacturing.

To reduce dependency on imports, companies are investing in local production facilities. For instance, Nestlé is set to open a new factory in Jeddah’s Third Industrial City in 2025, with an initial production capacity of 15,000 tonnes. However, maintaining product quality in Saudi Arabia’s extreme heat remains a challenge, increasing the need for advanced cold-chain logistics. To address this, over USD 500 million has been invested in refrigerated logistics infrastructure by both the public and private sectors. The Saudi Food and Drug Authority (SFDA) has introduced digital systems like Food Import and Registration System (FIRS) and FASEH to speed up import clearance processes. While these systems improve efficiency and safety standards, they also require manufacturers to meet stricter compliance regulations.

Industrial parks across the country are attracting more confectionery projects, further supporting local production. Notable examples include IFFCO’s expansion in Dammam, KDD’s USD 100 million plant in Sudair, and AlBabtain Food’s planned chocolate factory. These initiatives reflect a growing focus on increasing domestic manufacturing capacity. However, the industry still heavily depends on imported cocoa from regions like West Africa and Latin America. This reliance on global suppliers makes the market vulnerable to price fluctuations, meaning that achieving full supply-chain independence remains a long-term objective for Saudi Arabia’s chocolate industry.

Competitive Landscape

The Saudi Arabian chocolate market is moderately consolidated, with a mix of global leaders and regional players competing for market share. Ferrero has expanded its operations in Saudi Arabia, increasing its workforce from 12 to 400 employees through a joint venture with Ismail Abudawood. This collaboration has enabled Ferrero to better understand local regulations and cultural preferences, giving it a competitive edge. Barry Callebaut, on the other hand, has adopted a cost-plus pricing model, transferring the rise in cocoa prices directly to customers. Despite global margin challenges, this approach has driven strong volume growth in the Middle East.

Regional brands like Aani & Dani and Patchi are making a mark by blending Arabic flavors with Swiss-style chocolate-making techniques, which resonate well with Saudi Arabia’s strong gifting culture. Pladis has also strengthened its presence by establishing a new hub in Jeddah, enhancing the supply chains for its brands, including Godiva and McVitie’s. This strategic move highlights Pladis’ ambition to compete in both the premium chocolate and biscuit segments. Private-label chocolates from hypermarkets are intensifying competition by offering products at lower prices than branded options, often using loyalty programs to attract customers.

Although technology adoption in the Saudi chocolate market is still in its early stages, companies are beginning to leverage data-driven strategies to improve efficiency. For example, Barry Callebaut has streamlined its product portfolio by removing low-performing stock-keeping units (SKUs). This optimization helps reduce costs and enhances service levels, ensuring a more efficient supply chain. As competition grows, both global and local players are focusing on innovation, operational improvements, and customer-centric strategies to strengthen their position in the Saudi Arabia chocolate market.

Saudi Arabia Chocolate Industry Leaders

-

Ferrero International SA

-

Mars Incorporated

-

Nestlé SA

-

Mondelēz International Inc.

-

Patchi LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2022: Nestlé announced plans to invest SAR 7 billion in the Kingdom of Saudi Arabia in the coming ten years in a strategic move to grow its longstanding business in the country, beginning with up to USD 99.6 million to establish a cutting-edge manufacturing plant – which is set to open in 2025.

- November 2022: Barry Callebaut launched 100% dairy-free and plant-based chocolate NXT in Saudi Arabia. NXT is the first-of-its-kind dairy-free, lactose-free, nut-free, allergen-free, 100% plant-based, and vegan dark and milk chocolate to respond to the growing demand for plant-based foods across the country.

Saudi Arabia Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Product Type. Tablets and Bars, Molded Blocks, Pralines and Truffles, and Other Forms are covered as segments by Form. Mass and Premium are covered as segments by Price Range. Convenience Stores, Online Retail Stores, Supermarkets/Hypermarkets, and Other Channels are covered as segments by Distribution Channel.

| Dark Chocolate |

| Milk and White Chocolate |

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

| Mass |

| Premium |

| Dairy-Based |

| Plant-Based |

| Single Origin |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Stores |

| Other Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-Based |

| Plant-Based | |

| Single Origin | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Convenience Stores | |

| Other Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms