Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

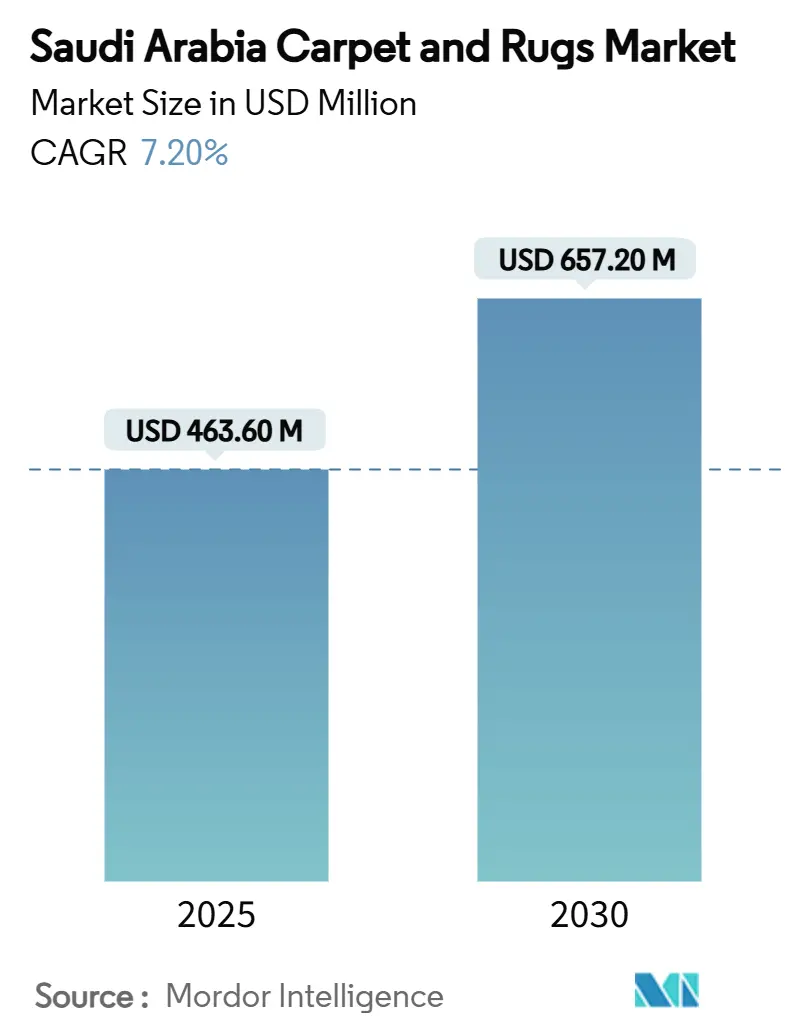

| Market Size (2025) | USD 463.60 Million |

| Market Size (2030) | USD 657.20 Million |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

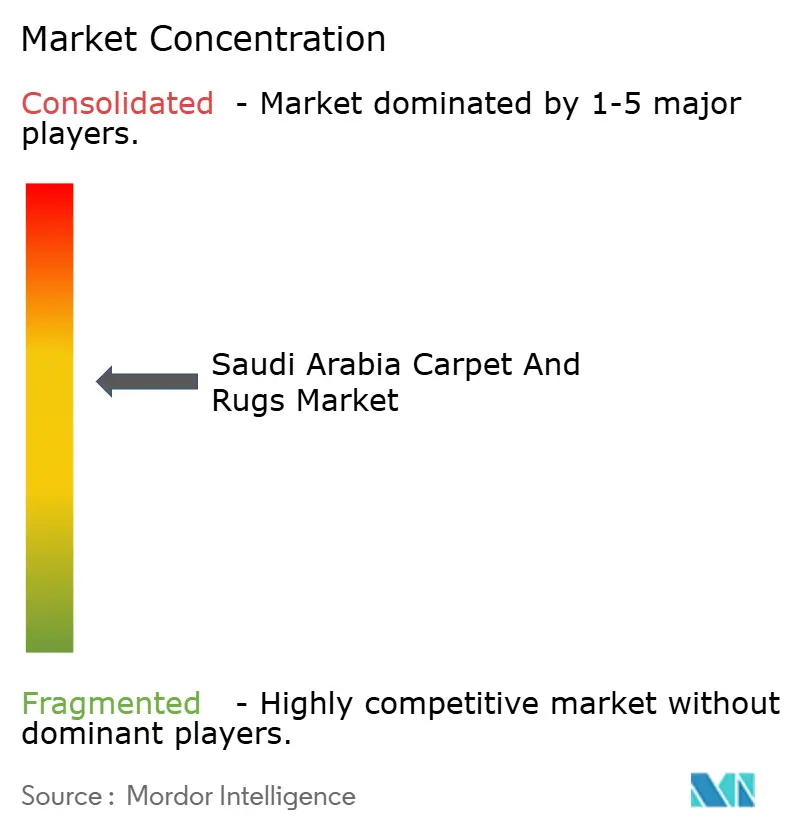

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Carpet And Rugs Market Analysis by Mordor Intelligence

The Saudi Arabia carpet and rugs market size stood at USD 463.6 million in 2025 and is on track to reach USD 657.2 million by 2030 at a 7.20% CAGR, supported by Vision 2030 construction spending, rapid hotel development, and steady housing completions. Accelerated infrastructure activity around NEOM, Jeddah, Mecca, and Riyadh is translating into large‐volume orders for commercial-grade floor coverings, while the Sakani program’s success in lifting homeownership to 63.74% sustains robust residential demand[1] Source: Ministry of Municipal and Rural Affairs and Housing, “Sakani Program Progress Update,” momrah.gov.sa. Product innovation in solution-dyed polyester, growth in stain-resistant nylon collections, and the rising adoption of antimicrobial backing technologies position suppliers to appeal to both value-conscious homeowners and specification-driven commercial buyers. Intensifying import competition from China and Turkey is applying margin pressure, yet it is also stimulating local manufacturers to automate production, broaden sustainable offerings, and expand B2B relationships with hotel developers. Digitalization, including social-commerce channels and direct manufacturer portals, is improving product discovery and shortening procurement cycles across the Saudi Arabia carpet and rugs market.

Key Report Takeaways

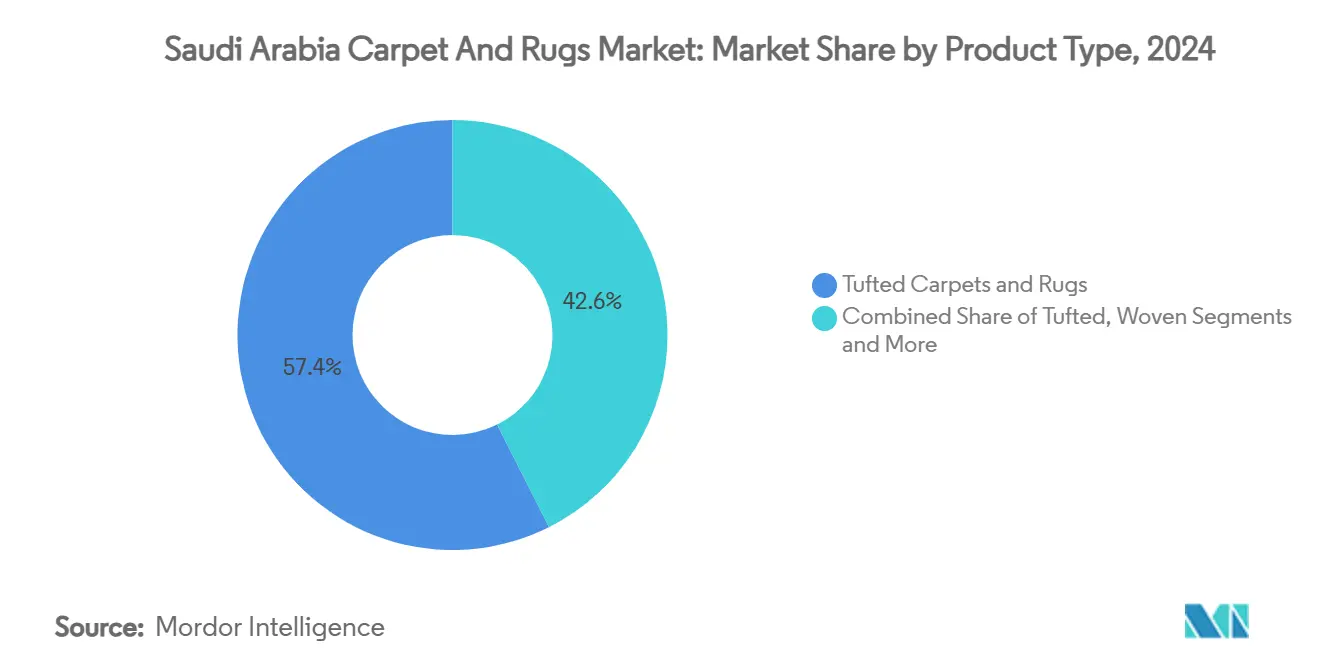

- By product type, tufted carpets held 57.4% of the Saudi Arabia carpet and rugs market share in 2024, while needle-punched formats are set to post the fastest 8.52% CAGR through 2030.

- By material, nylon led with 33.6% revenue share in 2024; polyester is forecast to expand at a 7.15% CAGR between 2025-2030.

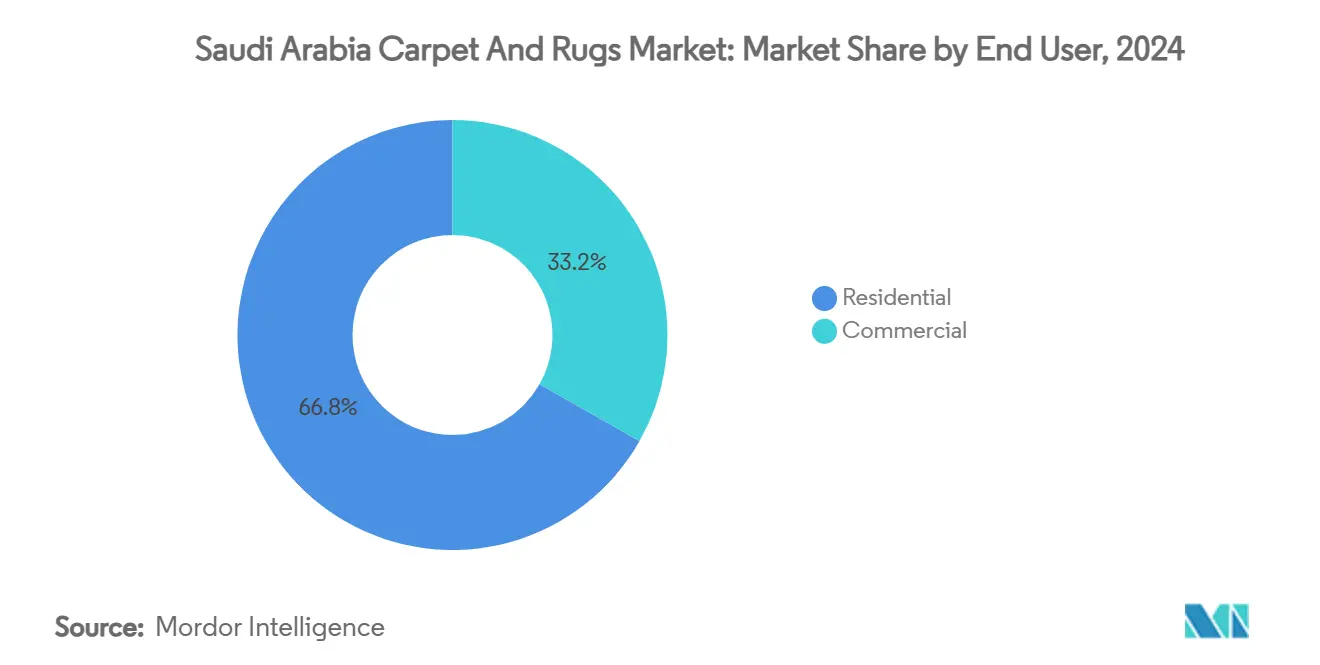

- By end user, residential applications accounted for 66.8% of the Saudi Arabia carpet and rugs market size in 2024, whereas commercial installations are projected to grow at an 8.12% CAGR to 2030.

- By distribution channel, the B2C retail route commanded 74.5% share in 2024, and B2B direct sales are advancing at a 7.31% CAGR through 2030.

- By geography, the Central region captured 36.8% share in 2024; the Western region is forecast to lead growth with a 7.54% CAGR during 2025-2030.

- The market exhibits moderate concentration, with Al Sorayai Group, Al Abdullatif Industrial Investment Co., Oriental Weavers, Shaw Industries Group, and Mohawk Industries holds major market share in 2024.

Saudi Arabia Carpet And Rugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 infrastructure boom lifts floor-covering demand | +2.1% | National focus on NEOM, Riyadh, Jeddah | Long term (≥ 4 years) |

| Hotel pipeline surge fuels hospitality carpeting spend | +1.8% | Western and Central regions | Medium term (2-4 years) |

| Higher disposable income drives premium home décor upgrades | +1.3% | Urban centers | Medium term (2-4 years) |

| Government Sakani housing program accelerates new-home fit-outs | +1.0% | Nationwide suburbs | Short term (≤ 2 years) |

| Demand for antimicrobial, stain-resistant carpets in healthcare & public venues | +0.6% | Major cities | Long term (≥ 4 years) |

| Social-commerce adoption expands online carpet sales | +0.4% | Urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Infrastructure Boom Lifts Floor-Covering Demand

Mega-projects such as NEOM, The Red Sea Project, and Qiddiya require millions of square meters of floor coverings meeting stringent energy, emissions, and performance criteria. Contractors now specify carpets with recycled content and low-VOC backings to align with the Kingdom’s 2060 net-zero pledge[2]Source: Saudi Vision 2030, “Net-Zero Emissions Commitment,” vision2030.gov.sa. Beyond flagship sites, more than 20 new airports, dozens of universities, and hundreds of healthcare facilities are in various stages of design and construction, each demanding durable products with life-cycle warranties and standardized maintenance protocols. Continuous refurbishment requirements across this infrastructure base anchor predictable replacement cycles, extending growth momentum across the Saudi Arabia carpet and rugs market for decades.

Hotel Pipeline Surge Fuels Hospitality Carpeting Spend

Saudi Arabia is on course to host 58% of MENA hotel keys by 2028, supported by 317 active projects totaling 79,984 rooms as of Q3 2024. Luxury and upscale properties represent nearly four out of every five rooms under development, triggering demand for custom-patterned Axminster-quality and tufted constructions with 36-ounce face weights capable of enduring heavy foot traffic. International operators such as Accor, Hilton, and Radisson stipulate global brand standards that elevate acoustic ratings, flammability compliance, and design uniformity across multiple properties [3]Source: Accor Group, “Middle East Development Pipeline Overview,” accor.com. Mecca’s role in religious tourism and Jeddah’s emergence as a Red Sea leisure hub, suppliers capable of delivering region-specific aesthetic palettes, rapid lead times, and onsite technical support are poised to deepen penetration in the Saudi Arabia carpet and rugs market.

Higher Disposable Income Drives Premium Home Décor Upgrades

Non-oil GDP growth of 4.3% projected for 2025 is boosting household spending power in Riyadh, Jeddah, and Dammam. Consumers increasingly orchestrate home makeovers that prioritize tactile comfort, noise damping, and visual warmth, motivating purchases of multi-level cut-pile carpets and wool-blend area rugs. Social-commerce platforms allow direct engagement with international brands and artisans, shrinking discovery barriers for premium designs. As urban professionals seek investment-grade furnishings, manufacturers emphasizing extended warranties, colorfast technologies, and personal design consultations gain mindshare throughout the Saudi Arabia carpet and rugs market.

Government Sakani Housing Program Accelerates New-Home Fit-Outs

The Sakani platform has facilitated 4.5 million lease contracts and assisted more than 96,000 families, pushing national homeownership above 63% by 2025. Most beneficiaries schedule flooring upgrades within the first twelve months of occupancy, creating reliable pull-through demand for mid-range tufted polypropylene and polyester offerings. Developers bundle turnkey flooring packages into mortgage financing, reducing upfront cash outlays and promoting brand-standardized carpet selections. Concentrated suburban clusters around Riyadh and Jeddah enable local installers to leverage route density, reducing service costs and enhancing the total value proposition for the Saudi Arabia carpet and rugs market.

Restraints Impact Analysis

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward hard-surface flooring | -1.4% | Urban districts | Medium term (2-4 years) |

| Raw-material price volatility (polypropylene, wool) | -0.8% | Nationwide | Short term (≤ 2 years) |

| Green-building certification raises compliance costs | -0.3% | Major metros | Long term (≥ 4 years) |

| Import influx from Turkey & China squeezes local margins | -0.6% | National mid-market | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Shift Toward Hard-Surface Flooring

Modern architectural preferences highlight large-format porcelain tiles, luxury vinyl planks, and polished concrete that complement minimalist interiors and simplify cleaning protocols. These surfaces demonstrate superior thermal comfort in hot climates and align with hospital-grade hygiene standards adopted during the pandemic. Retail showrooms increasingly display coordinated tile and LVP collections next to carpets, visually steering buyers toward hard options. While carpets retain advantages in acoustics and comfort, the share loss in new-build condominiums and corporate lobbies introduces growth headwinds for the Saudi Arabia carpet and rugs market.

Raw-Material Price Volatility

Polypropylene costs fluctuate in line with Brent crude swings, while global wool prices vary with pasture yields in New Zealand and Australia. Local producers hedging with quarterly contracts still face margin compression when spot rates spike. Currency exposure emerges as polypropylene imports are denominated in USD, yet retail transactions occur in Saudi Riyals. Manufacturers unable to pass through raw-material surcharges risk ceding shelf space to vertically integrated global suppliers within the Saudi Arabia carpet and rugs market. The volatility particularly impacts mid-market segments where price sensitivity limits manufacturers' ability to pass through cost increases, forcing margin compression or market share losses to competitors with more flexible cost structures and diversified supply chains.

Segment Analysis

By Product Type: Tufted Dominance Faces Needle-Punched Innovation

In 2024, due to cost-effective mass production and design versatility. Housing developers specify broadloom tufted rolls in standard neutral palettes that complement inclusive interior schemes, while commercial fit-outs choose solution-dyed tufted tiles for ease of replacement and sound attenuation. The Saudi Arabia carpet and rugs market size for tufted products reached USD 266 million in 2025 and continues to expand in tandem with residential mortgage uptake.

Needle-punched formats, though holding a smaller base, are forecast at an 8.52% CAGR through 2030, supported by the expansion of airports, exhibition halls, and temporary event venues that value rapid installation and exceptional wear resistance. Manufacturers introduce multi-layer needling and fused fiber enhancements, improving dimensional stability and extending service life, which resonates with facility managers targeting lower total ownership costs. As premium tourism projects move toward large-scale opening phases, demand for high-density needle-punched tiles capable of sustaining rolling-load traffic will accelerate, narrowing the performance perception gap between tufted and needle-punched solutions within the Saudi Arabia carpet and rugs market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Nylon Leadership Challenged by Polyester Innovation

Nylon maintained a 33.6% revenue share in 2024 on account of its resilience against crushing and superior color retention, key attributes for hotel corridors and office spaces under 24-hour HVAC cycles. Many global brands specify solution-dyed Type 6,6 nylon to achieve bleach cleanability and permanent stain resistance across their Saudi portfolios. The Saudi Arabia carpet and rugs market size for nylon categories is projected to cross USD 230 million by 2030, benefiting from higher star-rated hotel deliveries.

Polyester is gaining traction at a 7.15% CAGR due to advances in solution-dyed PET fibers harvested from recycled bottles. Improved bulk, softness, and color variation, combined with lower price points, make polyester products attractive to first-time homeowners and mid-scale hospitality operators. Mills installs trifocal spinnerets enabling deeper dye penetration, satisfying designers seeking vibrant hues without sacrificing colorfastness. As LEED projects prefer recyclability credentials, polyester’s closed-loop potential further lifts its relevance in the Saudi Arabia carpet and rugs market.

By End User: Residential Dominance Faces Commercial Acceleration

Residential projects represented 66.8% of total revenue in 2024 owing to the volume of new housing builds and ongoing renovations of early-2000s villas. Consumer perceptions favor plush cut-pile textures for bedrooms and family rooms where thermal comfort and child safety remain paramount. Promotional financing and store credit plans make multiyear upgrades attainable for mid-income households, keeping residential replacement cycles near seven years.

Commercial applications, led by hospitality and mixed-use developments, are advancing faster at an 8.12% CAGR as 362,000 hotel keys move through various construction phases. High-traffic lobbies, ballrooms, and prayer halls require 40-ounce tufted or woven Axminster carpets with custom motifs reflecting regional heritage, pushing average selling prices above residential equivalents. Government office consolidations into new administrative districts further increase specification opportunities, propelling the Saudi Arabia carpet and rugs market toward a more balanced residential-commercial mix by 2030.

By Distribution Channel: B2C Retail Dominance Challenged by B2B Direct Sales

Brick-and-mortar B2C outlets accounted for 74.5% of sales in 2024, fueled by consumer reliance on tactile evaluation and installer referrals for large floor areas. Branded galleries, hypermarkets, and DIY chains curate in-store vignettes that simplify pattern matching and accessories selection, strengthening walk-in conversion rates. The advent of augmented reality mobile apps enriches on-floor experiences, blending digital visualization with immediate product handling.

B2B direct sales to developers and facility management firms are growing at a 7.31% CAGR as project owners negotiate large-lot pricing, bespoke dimensions, and synchronized delivery schedules without intermediary margins. Manufacturers are embedding project configurators into extranets, enabling architects to upload CAD files and receive stitch-count optimized layouts within hours. This responsiveness reduces waste, cuts installation downtime, and heightens switching costs, consolidating supplier relationships across the Saudi Arabia carpet and rugs market.

Geography Analysis

The Central region commands 36.8% market share in 2024, anchored by Riyadh's role as the administrative and business epicenter where government installations, corporate headquarters, and residential developments generate sustained carpet demand across multiple segments. The region's dominance reflects its concentration of economic activity, including the King Abdullah Financial District and numerous government complexes that require premium commercial carpeting meeting international standards. Riyadh's position as the primary destination for domestic migration and expatriate professionals creates continuous residential demand, while the city's central role in Vision 2030 implementation ensures sustained infrastructure investment that drives commercial carpet procurement. The region benefits from established distribution networks and proximity to major manufacturers, creating cost advantages that reinforce its market leadership position.

The Western region, encompassing Jeddah, Mecca, and Medina, is projected to grow at a 7.54% CAGR through 2030, benefitting from religious tourism inflows exceeding 25 million pilgrims annually and Red Sea coastal development that integrates luxury resorts, branded residences, and entertainment venues[3]Source: JLL, “Saudi Arabia Hotel Market Intelligence 2025,” jll.com. Large hospitality footprints necessitate layered carpet specifications—from durable corridor runners to opulent wool-blend ballroom pieces, diversifying product mix in the Saudi Arabia carpet and rugs market. The Red Sea Project's luxury tourism focus creates opportunities for premium carpet specifications that align with international hospitality standards, while Jeddah's role as the commercial capital drives office and retail carpet demand. Cultural heritage preservation projects in AlUla and traditional design preferences in religious tourism venues favor carpets that incorporate regional aesthetic elements while meeting modern performance standards.

The Eastern, Northern, and Southern regions collectively represent emerging growth opportunities as Vision 2030's regional development initiatives extend infrastructure investment beyond traditional economic centers. The Eastern region, anchored by Dammam and the petrochemical industrial complex, demonstrates steady growth driven by industrial expansion and expatriate residential demand that favors international design preferences and premium specifications. The Northern and Southern regions benefit from government initiatives to diversify economic activity away from oil-dependent centers, creating new institutional and commercial carpet demand as regional universities, healthcare facilities, and government complexes expand their operations. These emerging regions present opportunities for manufacturers to establish early market presence before competition intensifies, particularly in segments requiring specialized products for extreme climate conditions

Competitive Landscape

The Saudi Arabia carpet and rugs market exhibits moderate concentration with five key players commanding significant market share: Al Sorayai Group, Al Abdullatif Industrial Investment Co., Oriental Weavers, Shaw Industries Group, and Mohawk Industries, creating a competitive structure that balances local market knowledge with global manufacturing capabilities. This configuration reflects the market's dual nature, where established local manufacturers leverage cultural understanding and government relationships against international players who compete through advanced manufacturing technologies, broader product portfolios, and supply chain efficiencies.

Strategic differentiation increasingly centers on sustainability credentials and technological innovation, as manufacturers respond to green building certification requirements and evolving consumer preferences for environmentally responsible products that meet LEED and other international standards. Oriental Weavers exemplifies this approach through their USD 1.5 million investment in solar power generation, targeting 4,000 tons of annual carbon emission reductions while maintaining production efficiency, demonstrating how environmental initiatives can create competitive advantages. Mohawk Industries' circular economy initiatives, achieving 36% reduction in greenhouse gas emissions intensity since 2010 while developing products incorporating recycled materials, illustrate how sustainability investments translate into market positioning advantages

Strategic partnerships with hospitality giants multiply reach: Hilton’s pipeline of 77 future properties and Radisson’s goal of 150 hotels by 2030 translate into multi-year carpet supply contracts covering guestrooms, conference centers, and branded residences [4]Source: Hilton Worldwide, “Hilton Expands Footprint in Saudi Arabia,” hilton.com. White-space opportunities emerge in specialized applications including antimicrobial carpets for healthcare facilities expanding under Vision 2030, luxury handwoven rugs for cultural tourism venues that celebrate Saudi heritage, and smart carpets incorporating IoT sensors for commercial building management systems that optimize maintenance schedules and indoor environmental conditions. The market's growth trajectory creates room for emerging players, particularly those focusing on niche segments such as outdoor carpets for extreme climate conditions, modular systems for temporary installations, and custom designs for religious and cultural facilities.

Saudi Arabia Carpet And Rugs Industry Leaders

Al Sorayai Group

Al Abdullatif Industrial Investment Co

Oriental Weavers

Shaw Industries Group

Mohawk Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hilton signed Diyar Ajwa, Tapestry Collection by Hilton, a 221-room debut property featuring locally inspired décor elements.

- May 2025: Hilton signed Diyar Ajwa, Tapestry Collection by Hilton, a 221-room debut property featuring locally inspired décor elements.

- March 2025: Government confirmed delivery of 362,000 new hotel rooms by 2030 under a USD 110 billion tourism expansion plan.

- August 2024: AVANA Companies invested SAR 22 million in fintech startup Ezdaher.sa to unlock Shariah-compliant hotel project funding.

Saudi Arabia Carpet And Rugs Market Report Scope

A carpet is a textile floor covering typically consisting of an upper layer of pile attached to a backing. The report covers a complete background analysis of the Saudi Arabian carpet and rugs market, which includes an assessment of the parental market, emerging trends in the segments and regional market, and significant changes in market dynamics and market overview. The report also offers qualitative and quantitative assessments, by analyzing the data gathered from industry analysts and market participants across various key points in the value chain. The Saudi Arabia Carpet and Rugs Market is segmented by Type (Wall to Wall Tufted Carpet, Wall to Wall Woven Carpet, and Rugs), Distribution Channel (Contractors, Retail, and Other Distribution Channels), and Application (Residential and Commercial). The report offers market size and forecasts for the market in value (USD million) for all the above segments.

By Product Type

| Tufted |

| Woven |

| Needle-Punched |

| Knotted / Hand-Knotted |

| Others (Flat-weave, Hooked, Braided) |

By Material

| Nylon |

| Polyester (PET & PTT) |

| Polypropylene |

| Wool |

| Other Natural Fibres (Jute, Sisal, Cotton, Silk) |

| Recycled & Bio-based Fibres |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Corporate Offices | |

| Retail | |

| Healthcare & Educational Institutions | |

| Other Commercial Facilities |

By Distribution Channel

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores |

| Specialty Flooring Stores (includes exclusive brand outlets) | |

| Furniture & Furnishing Stores | |

| Online | |

| Other Distribution Channels |

By Geography

| Western |

| Central |

| Northern |

| Eastern |

| Southern |

| By Product Type | Tufted | |

| Woven | ||

| Needle-Punched | ||

| Knotted / Hand-Knotted | ||

| Others (Flat-weave, Hooked, Braided) | ||

| By Material | Nylon | |

| Polyester (PET & PTT) | ||

| Polypropylene | ||

| Wool | ||

| Other Natural Fibres (Jute, Sisal, Cotton, Silk) | ||

| Recycled & Bio-based Fibres | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Corporate Offices | ||

| Retail | ||

| Healthcare & Educational Institutions | ||

| Other Commercial Facilities | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores | |

| Specialty Flooring Stores (includes exclusive brand outlets) | ||

| Furniture & Furnishing Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Western | |

| Central | ||

| Northern | ||

| Eastern | ||

| Southern | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia carpet and rugs market?

The market stands at USD 463.6 million in 2025 and is projected to reach USD 657.2 million by 2030.

How fast is the commercial segment growing?

Commercial installations are forecast to grow at an 8.12% CAGR through 2030, outpacing the overall market.

Which product type leads sales in Saudi Arabia?

Tufted carpets held 57.4% revenue share in 2024, dominating both residential and commercial applications.

Why are polyester carpets gaining popularity?

Advances in solution-dyed PET technology, improved stain resistance, and strong sustainability credentials are driving a 7.15% CAGR for polyester products.

Which region will record the highest growth in carpet demand?

The Western region, led by Jeddah, Mecca, and Medina, is expected to post a 7.54% CAGR between 2025-2030 due to tourism and megaproject activity.

Page last updated on: