Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

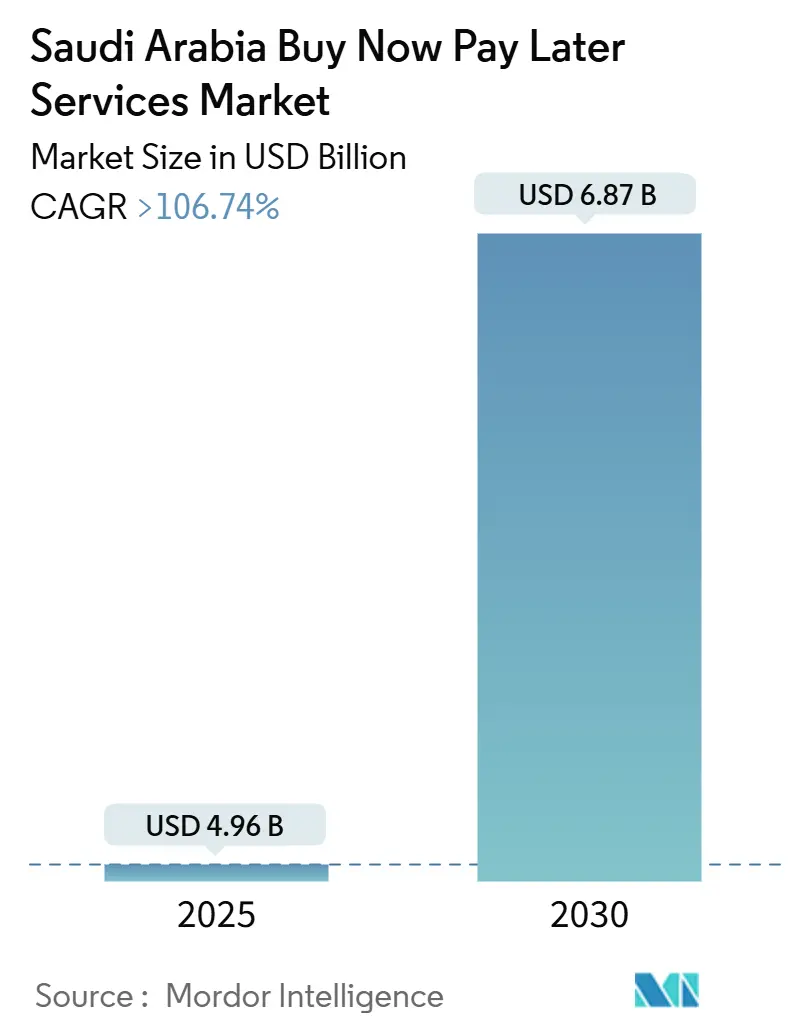

| Market Size (2025) | USD 4.96 Billion |

| Market Size (2030) | USD 6.87 Billion |

| Growth Rate (2025 - 2030) | 106.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Buy Now Pay Later Services Market Analysis by Mordor Intelligence

The Saudi Arabia buy now pay later services market size is currently valued at USD 4.96 billion and is projected to reach USD 6.87 billion by 2030, reflecting a 6.74% CAGR over the forecast period. The measured growth trajectory underscores a mature phase in which strictly enforced regulations, ambitious Vision 2030 cashless targets, and deep merchant integration shape expansion. SAMA’s 2023 licensing framework now governs 67 finance companies, ensuring disciplined underwriting and consumer protection [1]Source: Saudi Central Bank, “BNPL Licensing Framework and Regulatory Guidelines,” SAMA.GOV.SA. Vision 2030’s focus on 70% non-cash transactions was surpassed in 2024, with electronic payments already accounting for 79% of all transactions, a milestone that directly expands the Saudi Arabia buy now pay later services market. E-commerce GMV rose to USD 9.87 billion in 2024, fueling demand for installment options at checkout. Meanwhile, smartphone penetration tops 98%, allowing app-based providers to deliver instant credit decisions that resonate with young, credit-averse consumers. Competitive intensity is mounting as traditional banks enter the Saudi Arabia BNPL market with Sharia-compliant products that align with local financial norms.

Key Report Takeaways

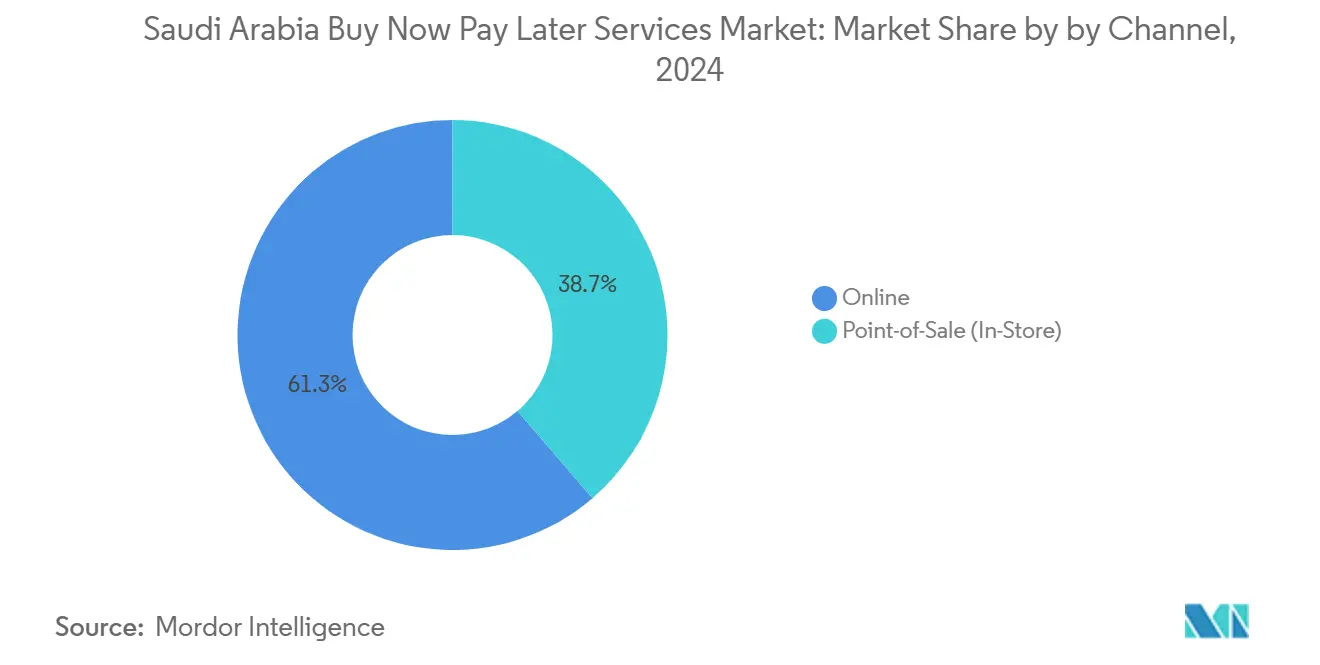

- By channel, online platforms accounted for 61.28% of the Saudi Arabia BNPL market share in 2024, while point-of-sale installations are advancing at a 24.65% CAGR through 2030.

- By end-user type, fashion & personal care held 37.73% of the Saudi Arabia BNPL market size in 2024; healthcare financing is forecast to expand at 35.39% CAGR to 2030.

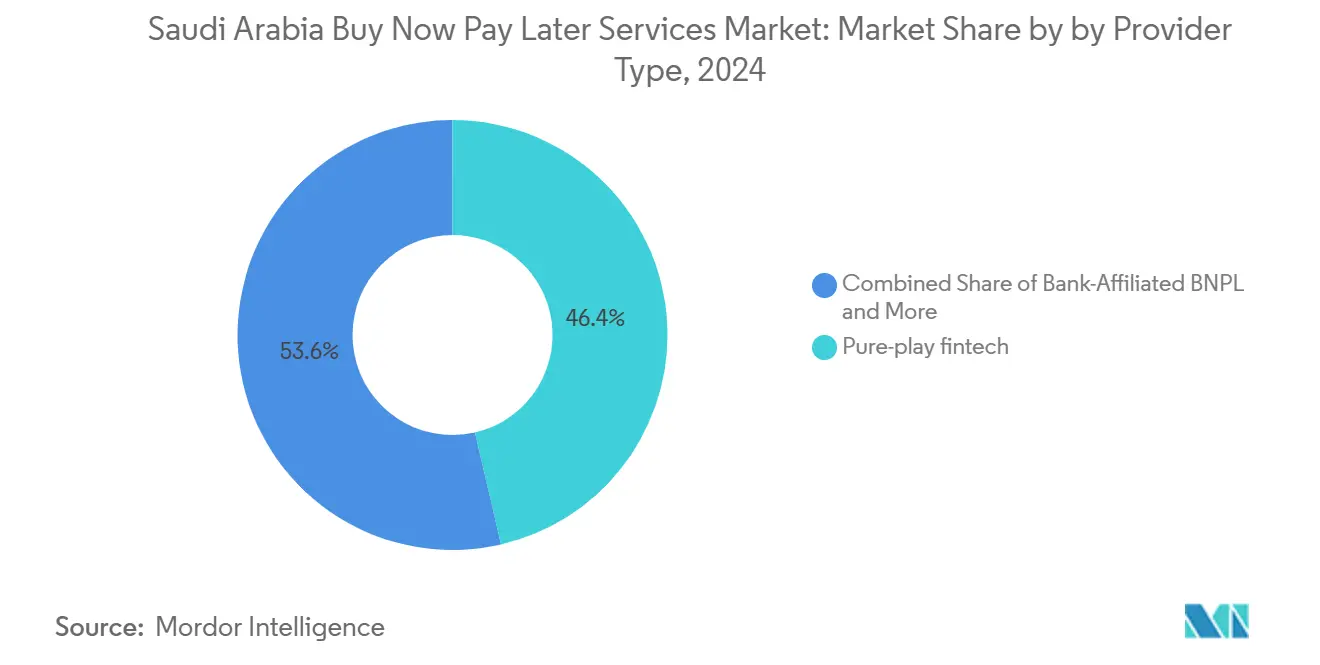

- By provider type, pure-play fintechs controlled 46.37% of the Saudi Arabia BNPL market share in 2024, yet bank-affiliated BNPL services record the highest projected CAGR at 29.74% through 2030.

- By region, central province led with 31.64% revenue share in 2024, while northern province is poised for a 30.33% CAGR owing to NEOM and Red Sea megaprojects.

Saudi Arabia Buy Now Pay Later Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of e-commerce platforms | +0.8% | National, strongest in Riyadh & Jeddah | Short term (≤ 2 years) |

| Millennial & Gen-Z credit aversion | +0.9% | Urban centers nationwide | Medium term (2-4 years) |

| Vision 2030 payment infrastructure upgrades | +0.7% | Nationwide, fast-tracked in NEOM & Red Sea | Long term (≥ 4 years) |

| High smartphone penetration | +0.6% | National, 98% internet access | Short term (≤ 2 years) |

| Merchant demand for higher average order value and customer retention | +0.7% | Nationwide, especially in retail and electronics | Medium term (2–4 years) |

| Entry of Sharia-compliant BNPL products expanding addressable market | +0.6% | Predominantly in conservative regions and Tier 2 cities | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Proliferation of E-commerce Platforms

Saudi online retail sales jumped 78.3% to SAR 37.02 billion (USD 9.87 billion) in 2024, turning installment payments from an alternative into a default choice at checkout [2]Source: Saudi E-commerce Council, “2024 Online Retail Statistics,” SEC.GOV.SA. Noon, Amazon.sa, and other leading marketplaces embed BNPL buttons that lift merchant conversion rates by 20-30% according to Checkout.com. Increased GMV ensures that the Saudi Arabia buy now pay later services market scales in tandem with e-commerce logistics networks, including last-mile delivery hubs that offer pay-in-four at the doorstep. Smaller merchants adopt white-label solutions from Tamara and Tabby, extending reach to tier-2 cities. As consumer expectations normalize around split payments, providers differentiate on approval speed and loyalty perks rather than mere availability.

Millennial & Gen-Z Credit Aversion

Two-thirds of Saudi residents are under 35, and this cohort shows a pronounced preference for transparent, fee-free installment products over revolving credit cards. Visa reports that 75% of Saudis are familiar with BNPL services and 33% had transacted through them by 2024 [3]Source: Visa, “Consumer Payment Attitudes Study 2024,” VISA.COM. Peer-to-peer social influence accelerates uptake, especially for fashion drops and electronics launches. The generational tilt widens the addressable base for the Saudi Arabia buy now pay later services market, as young shoppers view split payments as budgeting tools rather than debt. Merchants respond by marketing “0% profit-rate” banners during sales seasons, confident that BNPL boosts average order value by more than 35%.

Vision 2030 Payment Infrastructure Upgrades

Contactless adoption rose from 4% in 2017 to 94% in 2020 on the national mada network [4]Source: Saudi Payments, “Contactless Adoption Report 2025,” SAUDIPAYMENTS.COM. SAMA’s Phase 2 Open Banking rollout in 2025 allows BNPL providers to access consumer payment data subject to consent thus reducing fraud and improving credit assessment. The centralized SADAD platform and fast payments system (Sarie) shorten settlement cycles to minutes, lowering liquidity costs for BNPL operators. These rails position the Saudi Arabia buy now pay later services market for long-run scalability as megaprojects in NEOM and the Red Sea rely on cashless visitor experiences. These advancements align with Saudi Arabia’s Vision 2030 goal of creating a digitally-driven, cashless economy. As fintech adoption grows, BNPL services are expected to play a critical role in supporting tourism, retail, and e-commerce sectors by offering seamless and inclusive payment options.

High Smartphone Penetration

Saudi Arabia's 98% internet penetration and 109 Mbps average connection speeds create optimal conditions for mobile-first BNPL applications, enabling instant credit decisions and seamless user experiences. Smartphone-native BNPL apps leverage biometric authentication and AI-driven risk assessment to approve transactions within seconds, removing traditional barriers to installment payment adoption. The mobile-first approach particularly benefits younger consumers who prefer app-based financial services over traditional banking interfaces, with BNPL providers reporting 80% of transactions originating from mobile applications. This technological foundation enables innovative features like QR code payments at physical stores and integration with digital wallets, expanding BNPL utility beyond e-commerce into everyday retail transactions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of unified credit bureau | -0.4% | National, acute in smaller cities | Medium term (2-4 years) |

| Rising over-indebtedness concerns | -0.3% | National, policy focus in urban hubs | Short term (≤ 2 years) |

| Persistent cash-on-delivery culture in smaller cities | -0.5% | Tier 2 and Tier 3 cities | Medium term (2–4 years) |

| Profit-pressure from interchange-fee caps and MDR negotiations | -0.6% | National, acute in digital payment hotspots | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Lack of Unified Credit Bureau Creating Data Asymmetry

The absence of comprehensive credit bureau coverage creates significant information asymmetries that limit BNPL providers' ability to assess consumer creditworthiness accurately, forcing reliance on alternative data sources and conservative underwriting models. SAMA's credit bureau initiatives remain fragmented across multiple institutions, preventing holistic view of consumer debt obligations and increasing default risk for BNPL operators. This data gap particularly affects consumers with limited formal banking relationships, creating barriers to financial inclusion despite BNPL's potential to serve underbanked segments. The information asymmetry forces BNPL providers to implement stricter approval criteria and lower credit limits, constraining market expansion and limiting transaction values compared to markets with mature credit infrastructure.

Rising Concern Over Consumer Over-Indebtedness Prompting Stricter Rules

Growing awareness of consumer debt accumulation risks is driving regulatory scrutiny of BNPL practices, with SAMA implementing comprehensive licensing requirements and operational guidelines in December 2023 to prevent irresponsible lending. Consumer protection concerns are mounting as multiple BNPL providers compete for the same customer base, potentially enabling consumers to accumulate excessive installment obligations across platforms without centralized monitoring. The regulatory response includes mandatory affordability assessments, cooling-off periods, and enhanced disclosure requirements that increase operational costs for BNPL providers while potentially limiting customer acquisition rates. International precedents from Australia and the UK, where regulators imposed strict BNPL oversight following consumer debt concerns, suggest Saudi authorities may implement additional restrictions if over-indebtedness indicators emerge.

Segment Analysis

By Channel: Digital-Physical Convergence Accelerates

Online transactions retained 61.28% of the Saudi Arabia buy now pay later services market in 2024, yet the point-of-sale segment is forecast to grow at 24.65% CAGR as merchants embed QR-based installments at cash registers. Electronics chains such as Jarir and Extra report 40-50% gains in average ticket size after integrating BNPL apps. In turn, omnichannel retailers push for unified platforms that allow consumers to start a transaction online and finish it in-store, blurring channel boundaries. The Saudi Arabia buy now pay later services market size attributed to POS channels is projected to exceed USD 14 billion by 2030, reflecting rising physical retail integration. To accelerate brick-and-mortar uptake, providers deploy lightweight APIs that link to legacy POS systems without expensive hardware upgrades. As consumer journeys oscillate between browsing on a phone and purchasing at a mall, providers that synchronize limits, rewards, and repayment calendars across channels capture higher stickiness. Flynas’s integration of Tabby for ticket purchases exemplifies BNPL’s traction in non-retail services, while super-apps such as ToYou incorporate pay-in-four for food delivery. These cross-vertical moves deepen consumer familiarity, bringing steady repeat usage that anchors volume growth.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Type: Healthcare Emerges as Growth Engine

Fashion & personal care commanded 37.73% of the Saudi Arabia buy now pay later services market size in 2024, buoyed by frequent seasonal drops. However, healthcare is projected to clock the fastest 35.39% CAGR as clinics and pharmacies adopt installment plans for dental, optical, and elective procedures. Average household health outlays exceed USD 51 (SAR 191) per month, and 50% of consumers still rely on current income, signaling room for financing solutions. The Saudi Arabia buy now pay later services market share captured by healthcare is expected to rise markedly once insurance co-payments and cosmetic surgeries migrate to pay-in-six plans. Durable segments such as kitchen appliances also maintain momentum: spread-out payments enable mid-income households to upgrade white goods without depleting savings. Providers tailor tenures to product life cycles; for instance, a refrigerator purchase may qualify for 12-month plans, balancing ticket size and default risk. Across all end-user types, loyalty programs that bundle discounts for on-time payments nudge repeat purchases and lengthen customer lifetime value.

By Provider Type: Banks Challenge Fintech Dominance

Pure-play fintechs accounted for 46.37% of the Saudi Arabia buy now pay later services market share in 2024, yet bank-affiliated offerings are scaling rapidly at 29.74% CAGR on the back of established customer bases. Al Rajhi Bank’s Sahlha program caps fees at 0.90% per month and validates Sharia compliance via cost-plus contracts, winning conservative consumers. Riyad Bank’s DAFA’AT waives profit entirely for salary-transfer clients, undercutting fintech pricing. Lower funding costs allow banks to offer longer tenors without volume surcharges, challenging fintech margins. Retailer-embedded platforms remain nascent but strategically pivotal. Large merchants view proprietary BNPL as a route to own checkout data and avoid interchange fees. Carrefour’s pilot pay-in-four illustrates this trend, though scale depends on securing SAMA licenses. For fintechs, partnerships with acquirers such as Checkout.com extend reach across thousands of SMEs, offsetting bank competition.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Central Province, anchored by Riyadh, accounted for 31.64% of Saudi Arabia’s buy now pay later (BNPL) market in 2024. This dominance stems from Riyadh’s dense concentration of mega malls, retail clusters, and tech-savvy consumers. The city’s progressive regulatory stance toward fintech innovation has fostered partnerships between digital lenders and major retail chains. Such an enabling environment allows BNPL providers to scale rapidly across diverse consumer categories, from electronics to fashion. Riyadh’s growing population of young professionals and expatriates continues to reinforce sustained transaction volumes and long-term digital payment adoption.

The Western Province closely follows, driven primarily by the spending surge associated with religious tourism in Mecca and Medina. Pilgrims increasingly use installment options for booking hotels, transport, and pilgrimage packages through Sharia-compliant BNPL platforms. The integration of fintech payment systems into tourism infrastructure enhances both accessibility and transaction transparency. Seasonal peaks during Umrah and Hajj seasons translate into higher BNPL usage across hospitality and mobility sectors. Consequently, the Western Province remains a key anchor for expanding consumer finance solutions tailored to short-duration travel spending.

The Northern Province is poised for the fastest growth, with a forecasted 30.33% CAGR as futuristic projects like NEOM institutionalize cashless ecosystems. Large-scale infrastructure and residential developments in this region create fertile ground for fintech adoption. In the Eastern Province, affluent oil sector employees are increasingly using BNPL for luxury retail and automotive purchases. Expanding port infrastructure in Dammam supports international retail inflows, enhancing BNPL cross-border acceptance. Meanwhile, the Southern Province shows emerging potential in agricultural and equipment financing as modernization initiatives demand flexible payment solutions. Together, these regional dynamics are expected to give Saudi Arabia’s BNPL market a broad and inclusive national footprint by 2030.

Healthcare Segment in Saudi Arabia BNPL Services Market

The Healthcare segment has emerged as the fastest-growing segment in Saudi Arabia's BNPL services market, with a projected growth rate of approximately 31% during 2024-2029. This remarkable growth trajectory is being fueled by innovative partnerships between BNPL providers and healthcare institutions, offering patients flexible payment options for various medical services including diagnostics, blood tests, and wellness programs. The segment's rapid expansion is particularly notable as healthcare providers increasingly recognize the value of offering installment-based payment facilities to make medical services more accessible and affordable. The integration of zero-interest financing solutions in healthcare is transforming the traditional payment landscape, with providers offering zero-interest installment plans ranging from 6 to 60 months, making premium healthcare services more attainable for a broader segment of the population.

Remaining Segments in Saudi Arabia BNPL Services Market

The other significant segments in the Saudi Arabia BNPL market include Other Products, Other Electronic Appliances, and Kitchen Appliances, each playing a vital role in the market's development. The Other Products segment encompasses travel, hospitality, and various retail categories, demonstrating the versatility of consumer payment solutions across different sectors. The Other Electronic Appliances segment has gained substantial traction through partnerships with major electronics retailers and e-commerce platforms, while the Kitchen Appliances segment has benefited from the increasing adoption of online shopping for home appliances. These segments collectively reflect the broader integration of BNPL services across Saudi Arabia's retail landscape, with each category contributing to the overall market expansion through specialized offerings and targeted consumer solutions.

Competitive Landscape

The Saudi Arabia buy now pay later services market is moderately concentrated but highly dynamic, with the top five players driving the majority of transaction value. Tamara leads the space by focusing on omni-channel merchant coverage and offering Sharia-compliant financing solutions. Tabby, another key player, targets fashion and electronics segments and moved its headquarters to Saudi Arabia in 2024 to strengthen its local presence. Both companies secured significant funding rounds in 2025 to enhance credit analytics capabilities and support regional expansion. Their growth reflects a strategic blend of product specialization and market localization. These dominant players continue to shape consumer expectations and merchant adoption in the evolving BNPL landscape.

Traditional banks are stepping into the BNPL space, intensifying competition. Saudi National Bank now offers a “Split in 4” installment plan at 0% APR for cardholders, leveraging its access to credit bureau data to offer higher spending limits. Al Rajhi Bank taps into its physical branch network to reach older customers who may be unfamiliar with digital finance apps. Meanwhile, new fintech entrants like Jeel Pay and Barq are expanding the market’s reach by offering micro-installments starting at USD 13.33 (SAR 50), targeting underbanked segments. This growing diversity of players is expanding financial inclusion while pushing innovation across pricing models. The entry of banks and new startups is reshaping the competitive landscape and challenging early market leaders to differentiate further.

The current wave of competition hinges on technological capabilities and regulatory compliance. Players are racing to develop advanced AI-driven risk engines and fraud detection systems to manage growing transaction volumes. Investments in instant push notifications and Arabic-first user experiences aim to increase approval rates and customer retention. Merchant adoption is supported through seamless SDK integrations, ensuring frictionless point-of-sale implementation. Partnerships with Visa and mada help guarantee widespread acceptance across retail channels. With the Saudi Central Bank (SAMA) enforcing strict oversight, compliance has become a key differentiator and a barrier to entry. As regulatory costs rise, market consolidation is likely, with smaller providers seeking acquisitions to survive and scale.

Saudi Arabia Buy Now Pay Later Services Industry Leaders

Spotti

Tabby

Tamara

Postpay

Cashew Payments

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: SAMA licensed "Madafuou Alarabia" as the 67th finance company authorized for BNPL activity, demonstrating continued regulatory support for market expansion while maintaining strict licensing standards. The approval reflects SAMA's balanced approach to fostering fintech innovation while ensuring consumer protection and financial stability.

- March 2025: Checkout.com partnered with Tabby to expand BNPL adoption across Saudi merchants, with research indicating 42% of Saudi consumers have used BNPL services. The partnership enables Checkout.com's merchant network to offer Tabby's installment solutions, significantly expanding distribution reach and transaction volume potential.

- March 2025: Tamara Finance received preliminary approval from SAMA for consumer finance licensing, enabling expanded credit services beyond traditional BNPL offerings. The license approval positions Tamara to compete directly with traditional banks in personal lending while leveraging existing merchant relationships and customer data.

- September 2024: Tabby relocated its headquarters to Saudi Arabia and acquired digital wallet Tweeq, demonstrating strategic commitment to the Saudi market while expanding payment capabilities. The acquisition provides Tabby with additional financial services capabilities and local market expertise to compete with domestic providers.

Saudi Arabia Buy Now Pay Later Services Market Report Scope

Buy now, pay later (BNPL) is a short-term financing that allows customers to make purchases and pay for them later, generally without incurring interest. BNPL arrangements, sometimes known as "point of sale installment loans," are becoming a more popular payment alternative, especially in online shopping.

The Saudi Arabian buy now, pay later services market is segmented into channel and end-user types. By channel, the market is segmented into online and POS (point of sale). The market is segmented by end-users into kitchen appliances, consumer electronics, fashion and personal care, and healthcare. The report offers market size and forecasts for the market in terms of revenue (USD) for all the above segments.

By Channel

| Online |

| Point-of-Sale (In-Store) |

By End-User Type

| Kitchen Appliances |

| Other Consumer Electronics |

| Fashion & Personal Care |

| Healthcare |

| Other End-User Types |

By Provider Type

| Bank-Affiliated BNPL |

| Pure-Play Fintech |

| Retailer-Embedded Platforms |

By Region

| Central Province |

| Western Province |

| Eastern Province |

| Northern Province |

| Southern Province |

| By Channel | Online |

| Point-of-Sale (In-Store) | |

| By End-User Type | Kitchen Appliances |

| Other Consumer Electronics | |

| Fashion & Personal Care | |

| Healthcare | |

| Other End-User Types | |

| By Provider Type | Bank-Affiliated BNPL |

| Pure-Play Fintech | |

| Retailer-Embedded Platforms | |

| By Region | Central Province |

| Western Province | |

| Eastern Province | |

| Northern Province | |

| Southern Province |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Saudi Arabia BNPL market in 2025?

It stands at USD XX billion with a XX% CAGR forecast to 2030.

Which channel leads BNPL volume in Saudi Arabia?

Online platforms hold 61.28% share, though point-of-sale solutions are the fastest-growing.

What segment is the fastest-growing in BNPL end-use?

Healthcare financing leads with a projected 35.39% CAGR through 2030.

How are banks competing with fintech BNPL providers?

Banks leverage low funding costs and Sharia-compliant structures to offer fee-free or low-fee installments.

Which region shows the highest BNPL growth potential?

Northern province, supported by NEOM and Red Sea megaprojects, is forecast to grow at 30.33% CAGR.