Saudi Arabia Architectural Paints Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

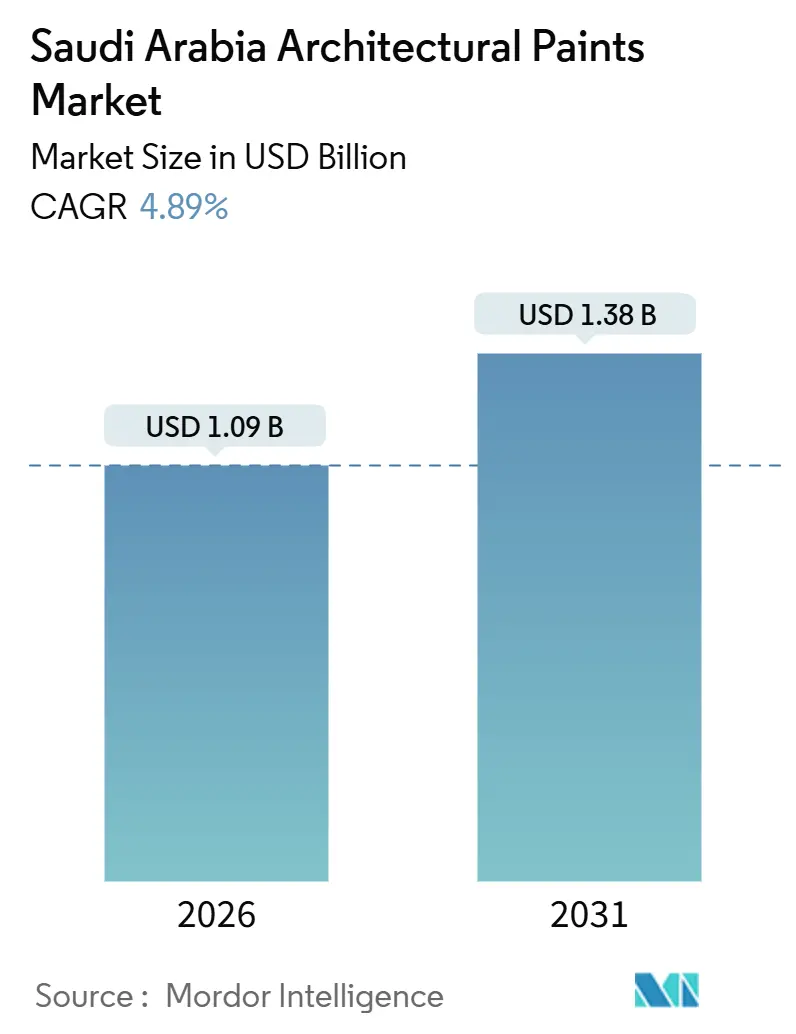

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Architectural Paints Market Analysis by Mordor Intelligence

The Saudi Arabia Architectural Paints Market size is estimated at USD 1.09 billion in 2026, and is expected to reach USD 1.38 billion by 2030, at a CAGR of 4.89% during the forecast period (2026-2031). This headline expansion is rooted less in sheer volumes and more in a pivot toward premium, low-VOC and polyurethane systems specified for Vision 2030 giga-projects. Water-borne technology already constitutes more than half of sales, professional applicators control two-thirds of demand, and vertical integration is emerging as the surest hedge against crude-linked feedstock swings. Forthcoming Saudi Building Code revisions, an accelerating tourism pipeline exceeding 55,000 hotel rooms, and anti-dumping duties on titanium dioxide imports combine to reshape cost structures and supplier strategies. While aluminum composite panel cladding is shrinking repaint cycles in high-rise projects, the surge of luxury resorts and heritage restorations keeps the Saudi Arabia architectural coatings market moving steadily upward.

Key Report Takeaways

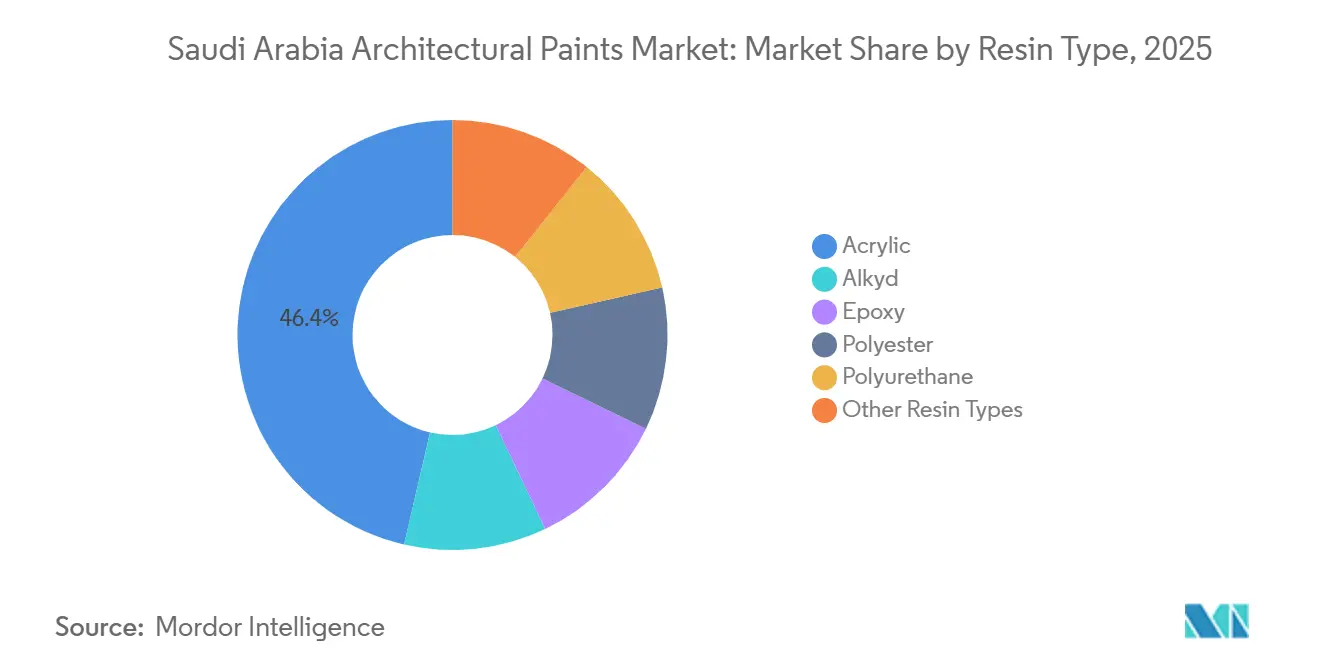

- By resin type, acrylics commanded 46.38% of the Saudi Arabia architectural coatings market size in 2025, while polyurethane recorded the fastest 5.48% CAGR to 2031.

- By technology, water-borne systems captured 52.47% of the Saudi Arabia architectural coatings market share in 2025 and are expanding at a 5.51% CAGR through 2031.

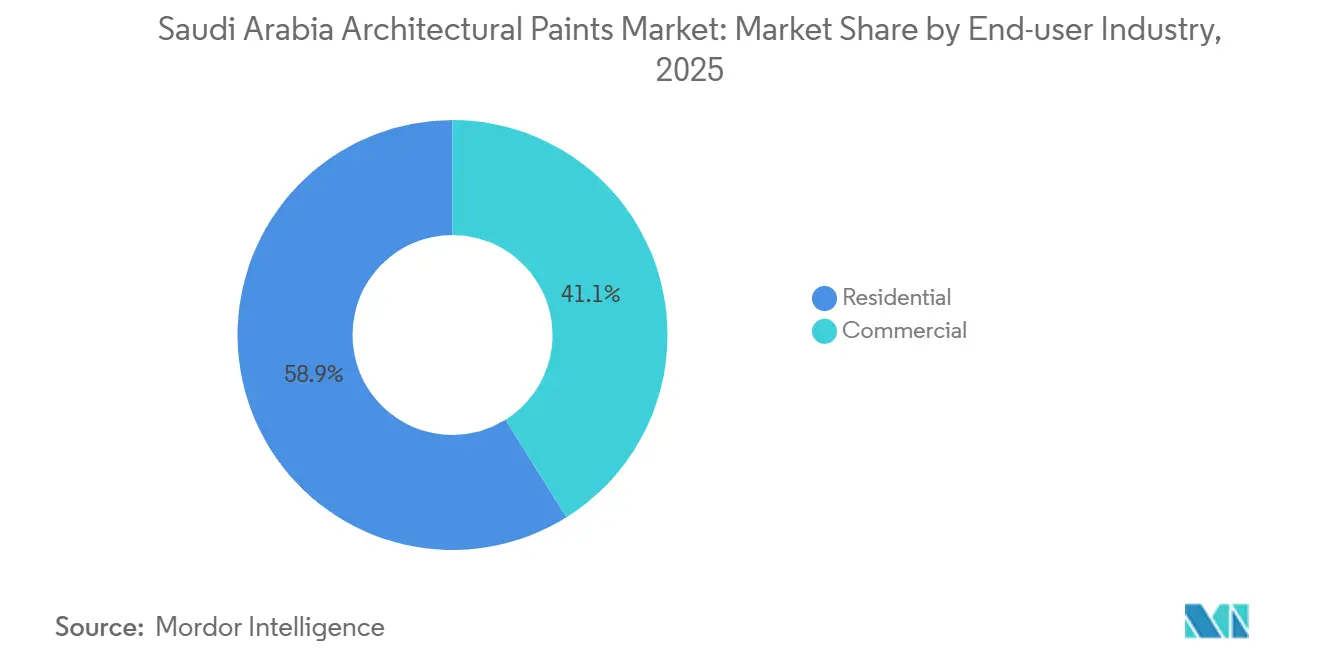

- By end-user industry, the residential segment held 58.89% of 2025 revenue; in contrast, commercial construction is advancing at a 5.32% CAGR through 2031.

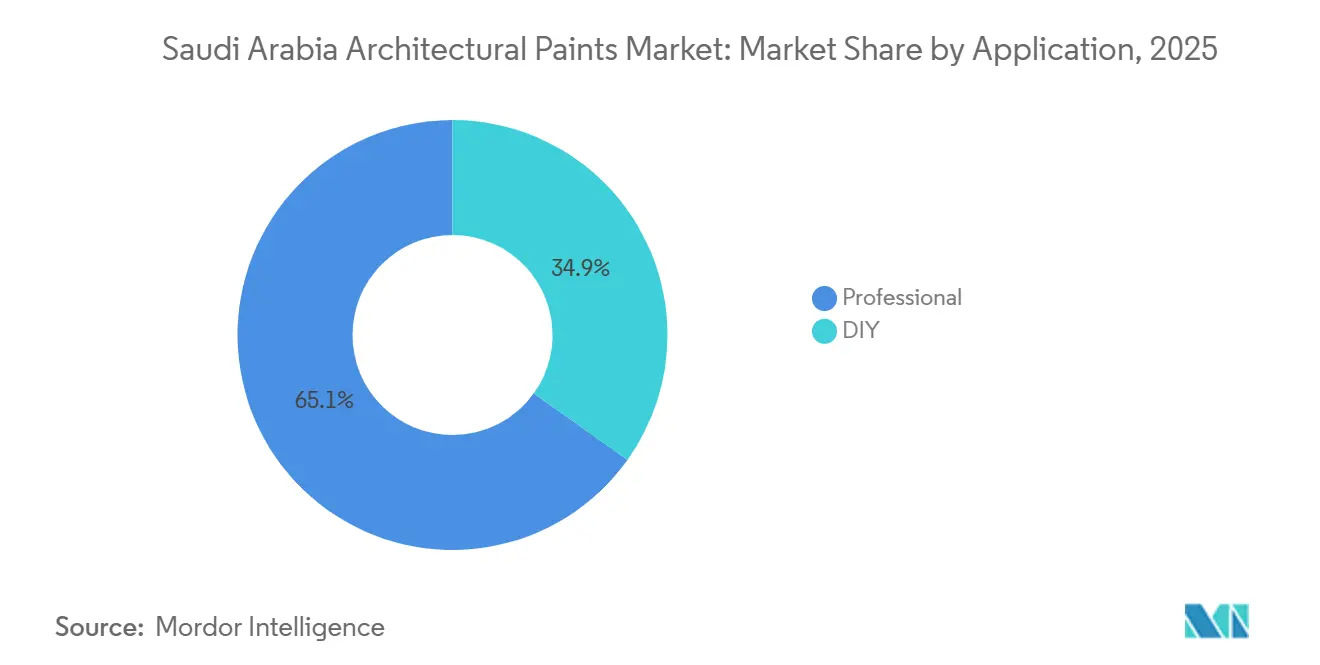

- By application channel, professional contractors controlled 65.12% of 2025 volume, whereas the DIY segment posts the briskest 5.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Architectural Paints Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of construction sector in Saudi Arabia | +1.2% | Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Increasing commercial construction backed by tourism boom | +0.9% | Makkah, Madinah, Red Sea coast | Short term (≤ 2 years) |

| Stricter energy-efficiency codes driving demand for high-performance coatings | +0.7% | Riyadh, NEOM | Long term (≥ 4 years) |

| Expansion of giga-projects (NEOM, The Line) creating premium paint demand | +1.1% | NEOM, Riyadh, Red Sea coast, Diriyah | Medium term (2-4 years) |

| Emerging preference for low-VOC and water-borne systems due to Green Saudi Initiative | +0.6% | Urban centers nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Construction Sector in Saudi Arabia

The Kingdom recorded 309,525 active building projects in 2024, sustaining baseline demand even though construction grew 4.6% year-on-year—slightly below the 4.89% CAGR expected for the Saudi Arabia architectural coatings market[1]General Authority for Statistics, “Quarterly Construction Indicators,” gastat.gov.sa. Rising real-estate lending, buoyant office occupancy of 89% in Riyadh, and mandated delivery of 300,000 housing units each year collectively reinforce residential dominance. Yet the faster tempo of commercial projects tied to tourism signals an emerging shift toward higher-margin epoxy and polyurethane finishes for lobbies, façades, and parking structures. Multinationals able to document ASTM performance are gaining specification advantages, while smaller local firms relying on generic alkyds risk exclusion from large tenders.

Increasing Commercial Construction Backed by Tourism Boom

Saudi Arabia greeted 109 million visitors in 2024, fueling over 150 hotel projects with 55,000 rooms and lifting the Saudi Arabia architectural coatings market through demand for LEED-compliant, low-VOC interiors. Red Sea Project resorts mandate pure acrylic and silicone-modified exteriors, Diriyah Gate’s USD 63.2 billion masterplan requires UV-stable earth-tone finishes, and Qiddiya’s entertainment hub stimulates textured decorative demand. Frequent refurbishment cycles in luxury hotels elevate recurring sales, reinforcing the commercial segment’s 5.32% CAGR through 2031.

Stricter Energy-Efficiency Codes Driving Demand for High-Performance Coatings

Saudi Building Code chapters 601-602 oblige thermal insulation, propelling uptake of cool-roof and heat-reflective systems that cut cooling loads by up to 30%. A 2024 KFUPM study confirmed a 13% energy saving from exterior insulation with acrylic plaster, bolstering specifications for high-performance water-borne products. LEED and Estidama frameworks supply the de facto VOC limits absent from SBC, and Greenguard-certified launches such as Jotun’s Fenomastic Wonderwall Lux illustrate how suppliers win premium project approvals.

Expansion of Giga-Projects (NEOM, The Line) Creating Premium Paint Demand

NEOM’s Sindalah island opened in December 2024 with marine-grade epoxy and polyurethane coatings that cost 40-60% more than standard emulsions. Although The Line was scaled back, its USD 100 billion budget still underwrites vertical infrastructure demanding antimicrobial, fire-rated coatings. Riyadh’s New Murabba alone is forecast to consume 50 million liters between 2026-2030, equating to 4.6% of annual national demand. Vertically integrated suppliers able to guarantee resin and pigment supply are positioned to capture these high-value tenders.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in crude-oil linked raw-material prices | -0.8% | Nationwide | Short term (≤ 2 years) |

| Rising popularity of exterior cladding systems reducing repaint cycles | -0.5% | Riyadh, Jeddah high-rises | Medium term (2-4 years) |

| Growing import of lower-priced Turkish and Asian paints in DIY channel | -0.3% | Nationwide retail | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Crude-Oil Linked Raw-Material Prices

Titanium dioxide spot prices surged from USD 2,024/t in December 2024 to above USD 2,200/t three months later, and impending anti-dumping duties of 18-34% on Chinese TiO₂ would further strain margins[2]General Authority of Foreign Trade, “Notice of Anti-Dumping Investigation on Titanium Dioxide,” gaft.gov.sa. Polypropylene costs continue to shadow Brent crude swings, challenging smaller manufacturers without long-term contracts. Aramco’s August 2024 move to lift its Petro Rabigh stake to roughly 60% aims to stabilize feedstock but underscores capital intensity in the value chain.

Rising Popularity of Exterior Cladding Systems Reducing Repaints

Aluminum composite panels accounted for 30-35% of new façade area in Riyadh and Jeddah in 2024, rising to 50-60% in towers over 20 stories. Ventilated cladding eliminates 5-7 year repaint cycles, trimming exterior demand in the Saudi Arabia architectural coatings market. Coil-coated PVDF panels with 20-25 year warranties shift expenditure away from liquid finishes, squeezing growth within the commercial high-rise envelope.

Segment Analysis

By Resin Type: Acrylic Dominance Anchored by UV Resistance

Acrylics held 46.38% of the Saudi Arabia architectural coatings market share in 2025 because of superior UV stability, forgiving application, and water-borne compatibility. Polyurethane’s 5.48% CAGR, however, signals mounting preference for abrasion-resistant coatings in mega-projects and industrial corridors. Vertically integrated leaders such as National Paints offset feedstock shocks through captive resin plants, while smaller players reliant on spot purchases face shrinking spreads. Acrylic will remain dominant in the Saudi Arabia architectural coatings market through 2031, yet its share could soften by two to three points as polyurethane and epoxy systems penetrate premium segments.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Water-Borne Gains Reflect Regulatory and Health Tailwinds

Water-borne systems captured 52.47% of the Saudi Arabia architectural coatings market in 2025, and their 5.51% CAGR eclipses overall industry growth. Solvent-borne finishes still command critical roles in marine, industrial, and fast-dry exterior jobs, but prolonged reliance on 300-400 g/L VOC alkyds is increasingly untenable on giga-project sites adopting LEED criteria. Hempel’s water-based Jeddah line and Jotun’s Greenguard launches typify the investment trajectory needed to serve this expanding niche.

By End-user Industry: Commercial Outpaces Residential on Tourism Catalyst

Residential projects generated 58.89% of revenue in 2025 under Ministry of Housing quotas, yet the commercial segment’s 5.32% CAGR is rewriting the mix as hotel, retail, and office renovations escalate. The Saudi Arabia architectural coatings market size allocated to residential builds may fall below 56% by 2031, whereas commercial refurbishments will keep water-borne and polyurethane grades in sustained demand.

By Application: Professional Channel Dominance Masks DIY Disruption

Professional contractors consumed 65.12% of the 2025 volume, controlling procurement for giga-projects and mass housing. Nevertheless, DIY demand is accelerating through online color tools, omnichannel retail, and Western chain entrants. Should e-commerce penetration hit 46% of retail by 2030, DIY share could approach 40%, challenging suppliers to adapt packaging, tinting logistics, and marketing.

Geography Analysis

Riyadh, Jeddah, and the Eastern Province collectively generated nearly 70% of 2025 demand, a dominance unlikely to fade as New Murabba, Diriyah Gate, King Salman Park, and multiple petrochemical expansions advance. NEOM and the northwestern Red Sea coast, while a smaller base, represent the fastest-growing pocket of the Saudi Arabia architectural coatings market, commanding premiums for marine-grade and low-VOC systems. Makkah and Madinah experience episodic surges tied to pilgrim seasons, while southern and border provinces lag, constrained by lower private investment. Trade flows reveal upside for backward integration: Saudi Arabia exported USD 286 million in acrylic polymers against USD 195 million in imports during 2022, yet the Kingdom still brings in significant finished coatings. Proposed duties on Chinese TiO₂ and painted aluminum sheets tilt the field toward domestic producers capable of capturing upstream value and ensuring pigment security.

Competitive Landscape

Saudi Arabia Architectural Paints market is moderately consolidated. Multinationals, AkzoNobel, Jotun, PPG, Sherwin-Williams, Hempel, retain specification pull in premium segments but struggle to match local pricing in commodity acrylics. SIPCO’s 2025 acquisitions of Premium Paints and Excellent Paints highlight an accelerating consolidation cycle as firms seek volume leverage against raw-material volatility. Emerging opportunities hinge on cool-roof, antimicrobial, and coil-coated solutions, while digital tinting and AI advice tools gain traction in customer engagement. Compliance burdens around substances of very great concern elevate entry barriers and favor players with global stewardship programs in place.

Saudi Arabia Architectural Paints Industry Leaders

Jotun

Jazeera Paints

Hempel A/S

NATIONAL PAINTS FACTORIES CO. LTD.

Caparol Paints

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Jazeera Paints opened its new showroom in Riyadh, Al-Arid district. The showroom demonstrates Jazeera Paints' commitment to maintaining the standards of quality, fostering creativity, and delivering customer-focused innovation for architectural and other kinds of paints.

- March 2025: Saudi Industrial Paint Company (SIPCO), under the umbrella of Kaizen Paint Middle East, took over Premium Paints Company, a coatings manufacturer based in Saudi Arabia. With this acquisition, SIPCO aims to bolster its presence in the Kingdom, ramp up production capacity, further localization initiatives, and provide decorative coatings for residential, commercial, and industrial uses.

Saudi Arabia Architectural Paints Market Report Scope

Architectural paint includes interior and exterior paints, primers, sealers, varnishes, and stains. The report covers all types of paints used for office buildings, warehouses, convenience stores, shopping malls, and homes. The infrastructure segment, which consists of roads, bridges, and railways, does not fall within this category. Architectural paint also includes paints that are applied to new constructions and renovation works in old buildings.

The architectural paints market is segmented by resin type, technology, and application. On the basis of resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types (vinyl). On the basis of technology, the market is segmented into water-borne, solvent-borne, and other technologies (oil-based). On the basis of application, the market is segmented into professional and DIY. For each segment, the market sizing and forecasts were made based on revenue (USD).

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

| Water-borne |

| Solvent-borne |

| Commercial |

| Residential |

| Professional |

| DIY |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User Industry | Commercial |

| Residential | |

| By Application | Professional |

| DIY |

Key Questions Answered in the Report

How fast is demand growing for coatings specified in Saudi giga-projects?

Coatings tied to NEOM, Diriyah Gate, New Murabba, and related ventures are collectively expanding at roughly 5.5% CAGR, outpacing the 4.89% growth of the broader Saudi Arabia architectural coatings market.

Which resin category is gaining the most share?

Polyurethane grades are registering the quickest 5.48% CAGR as hotels, entertainment parks, and industrial sites require superior abrasion resistance and gloss retention.

What is driving the shift toward water-borne formulations?

Energy-efficiency regulation, voluntary LEED targets, and the Green Saudi Initiative’s emissions goals have lifted water-borne technology to 52.47% share and a 5.51% CAGR.

Will DIY channels overtake professional contractors?

Professional applicators still command around two-thirds of volume, but DIY sales are growing 5.46% annually and could approach 40% of demand by 2031 if e-commerce reaches its projected penetration.

How are raw-material duties affecting costs?

Proposed anti-dumping tariffs of 18–34% on Chinese TiO₂ and 7.1–20% on painted aluminum sheets could raise pigment and coil-coat costs, pressuring margins for manufacturers lacking long-term supply contracts.

What is the current market size of Saudi Arabia Architectural Paints Market?

The Saudi Arabia Architectural Paints Market size is estimated at USD 1.09 billion in 2026, and is expected to reach USD 1.38 billion by 2031, at a CAGR of 4.89% during the forecast period (2026-2031).