Satellite Bus Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.79 Billion |

| Market Size (2031) | USD 7.31 Billion |

| Growth Rate (2026 - 2031) | 14.28% CAGR |

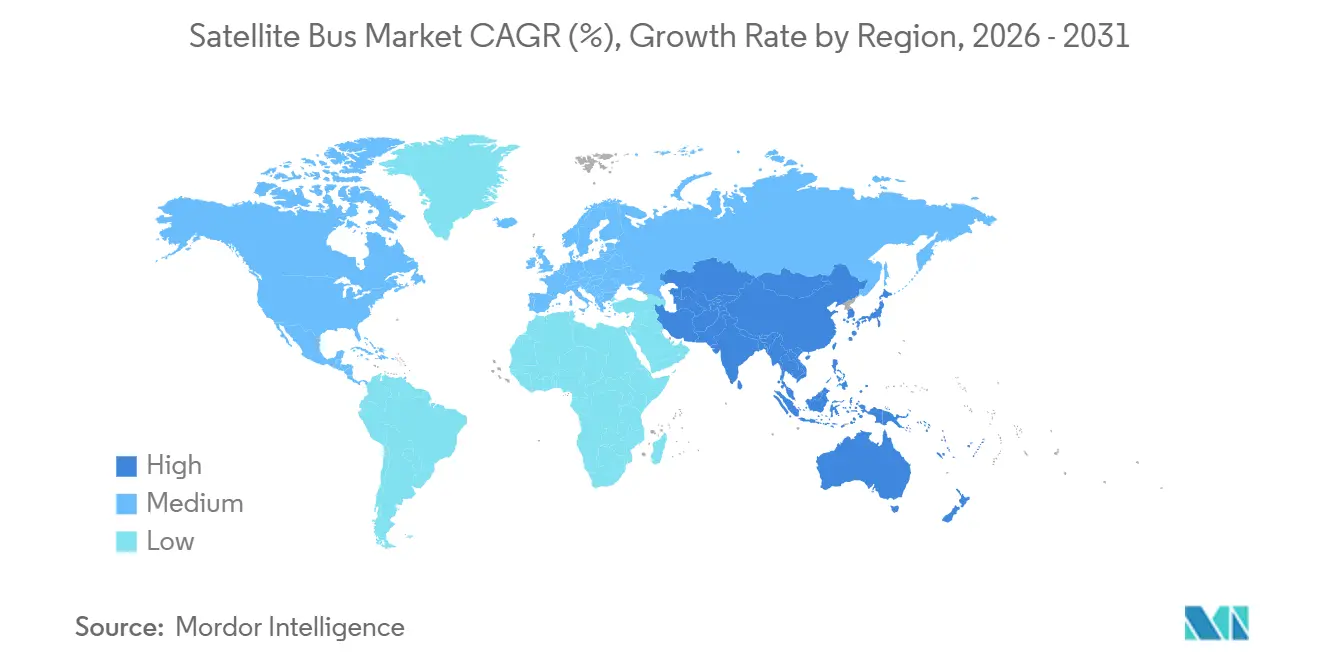

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

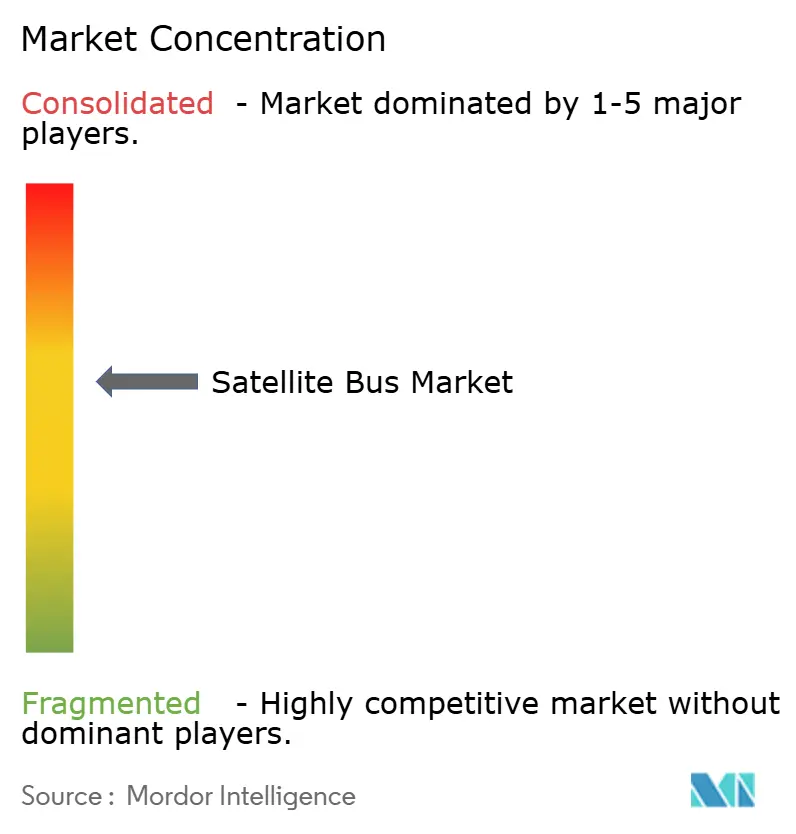

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Bus Market Analysis by Mordor Intelligence

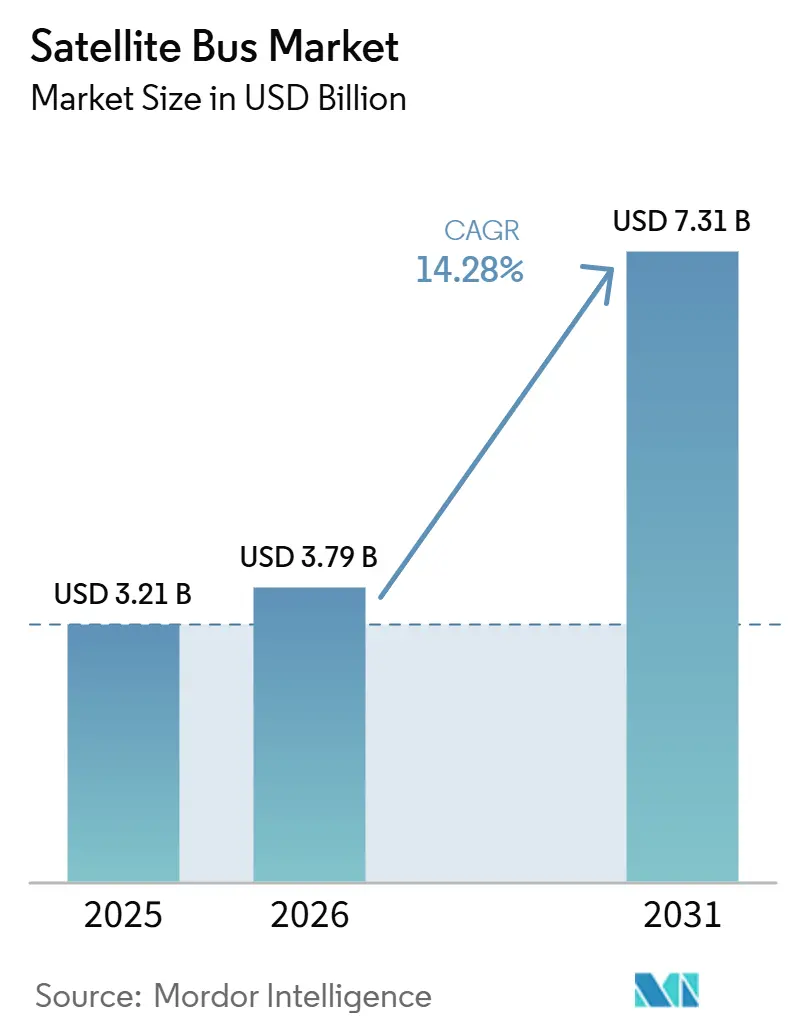

The satellite bus market size was valued at USD 3.21 billion in 2025 and estimated to grow from USD 3.79 billion in 2026 to reach USD 7.31 billion by 2031, at a CAGR of 14.28% during the forecast period (2026-2031). The market is moving away from custom spacecraft programs and toward factory-based production that supports repeat orders and shorter delivery cycles. Standardized electrical power systems, attitude-control units, and software-defined avionics (SDA) are making bus designs more modular, which is reducing build complexity and improving output consistency. Demand is rising from both commercial constellation programs and government resilience programs, which is widening the addressable base for bus manufacturers. Competition is also changing, because newer manufacturers with scalable production models are challenging established defense primes on speed, cost, and configurability. Procurement pauses in selected defense programs and shortages in key components still matter. Still, they are also pushing buyers to favor suppliers that can combine secure delivery with faster manufacturing cycles.

Key Report Takeaways

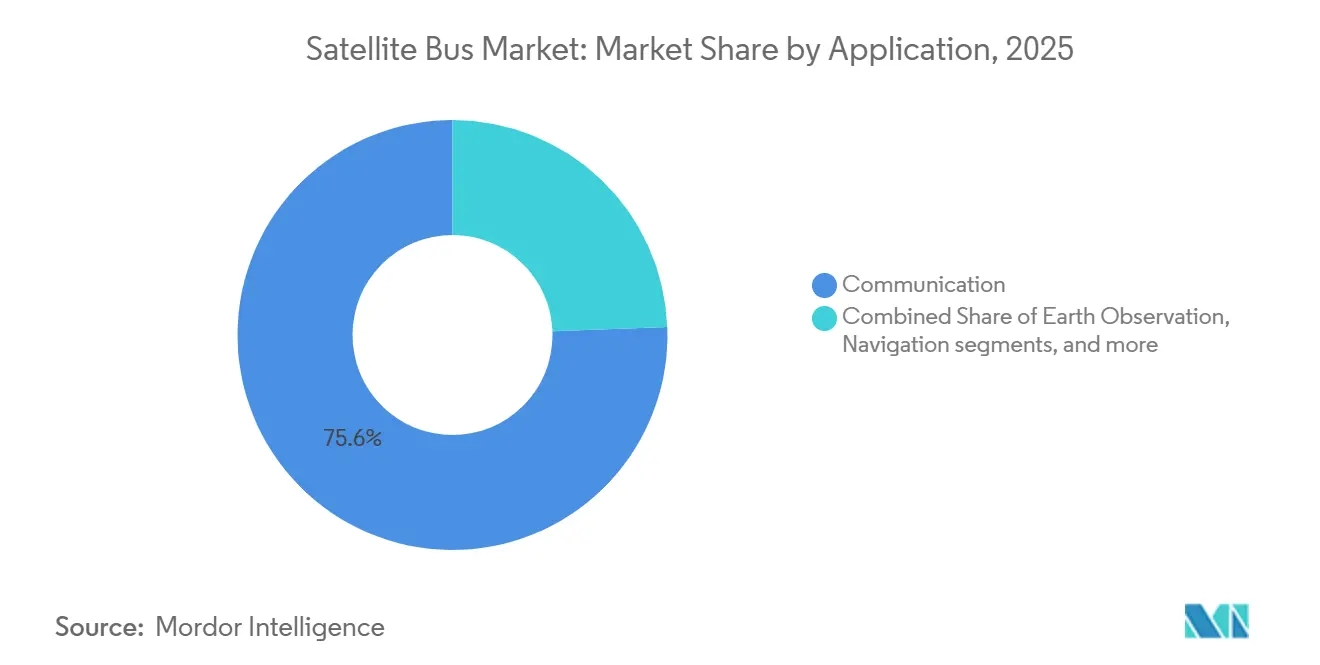

- By application, communication satellites held 75.60% of the satellite bus market share in 2025, while navigation is projected to grow at a 16.01% CAGR through 2031.

- By satellite mass, platforms weighing more than 1,000 kg accounted for 53.55% of the satellite bus market size in 2025, while the 100 to less than 500 kg segment is forecast to expand at a 16.20% CAGR through 2031.

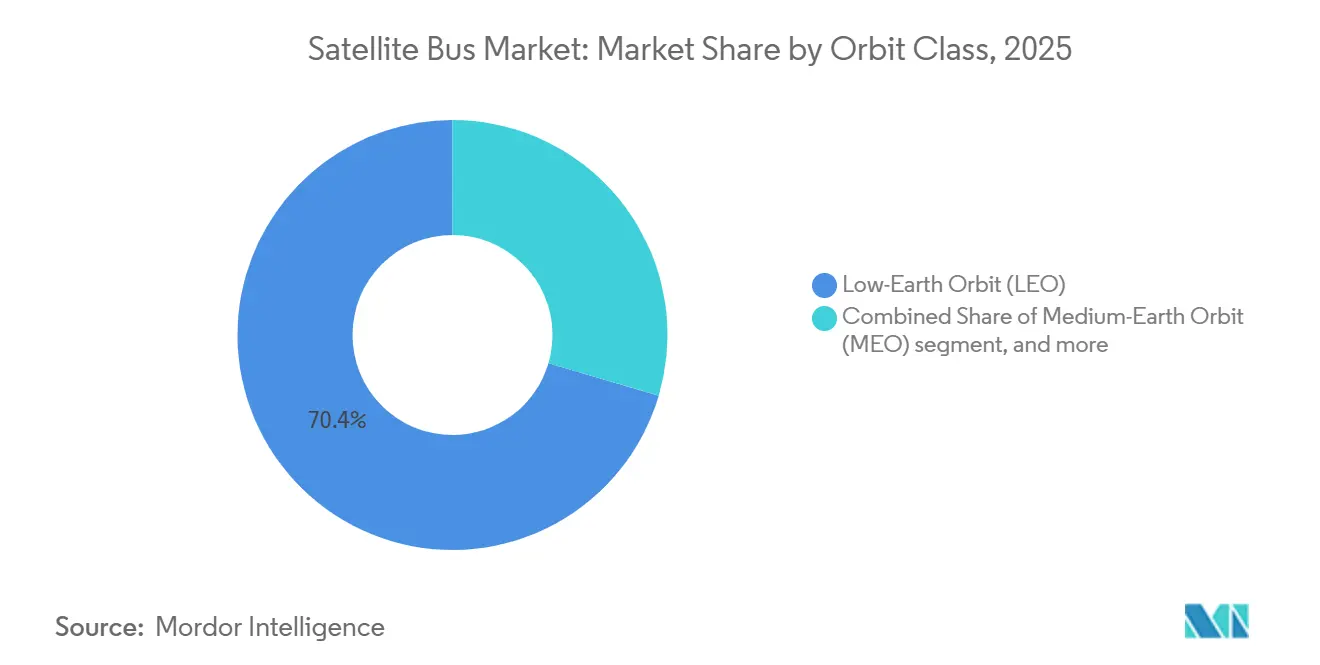

- By orbit class, LEO captured 71.15% of the market share in 2025, while GEO is projected to grow at a 15.50% CAGR through 2031.

- By end user, commercial operators accounted for 66.20% of the satellite bus market share in 2025, while government and military are forecast to grow at a 16.45% CAGR through 2031.

- By geography, North America accounted for 68.40% of the satellite bus market share in 2025, while Asia-Pacific is projected to grow at a 17.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Satellite Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive demand for broadband mega-constellations | +4.50% | Global (North America, Asia-Pacific, European Union core) | Short term (≤ 2 years) |

| Government resilience programs and SDA architectures | +2.50% | North America, expanding to European Union and Asia-Pacific | Medium term (2-4 years) |

| Price inflection from mass-produced modular buses | +2.00% | Global | Medium term (2-4 years) |

| Dual-use intelligence-surveillance requirements | +1.80% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Venture-backed “bus-as-a-service” business models | +1.00% | Global, early gains in North America and European Union | Long term (≥ 4 years) |

| On-orbit servicing compatibility mandates | +0.80% | GEO operators globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Demand for Broadband Mega-Constellations Rewrites Bus Economics

Volume has become the main competitive variable in the satellite bus market as large constellation operators continue to favor repeatable designs over mission-specific platforms. SpaceX has maintained a high deployment cadence and produced more than 7,000 Starlink buses since 2019, demonstrating the rapid shift in the satellite bus market toward industrial-scale output rather than low-volume engineering cycles.[1]SpaceX, “Starlink Mission Updates,” SpaceX Official Website, spacex.com That production logic is influencing buyer behavior, because operators now expect shorter lead times and more predictable unit economics from the satellite bus market. Standardized architectures also support recurring replenishment cycles, which makes the demand base less dependent on one-time launches. The same pattern is evident in secure communications planning, where customers are increasingly willing to adopt common bus architectures if they improve delivery speed and manufacturing scalability. This keeps the satellite bus market focused on throughput, supplier flexibility, and reusable design blocks.

Government Resilience Programs and SDA Architectures Drive Specialized Volume

Government resilience programs are adding a second large demand stream to the satellite bus market, especially for constellations that need secure communications, tactical data relay, and fast replenishment cycles. The core procurement logic favors repeated bus designs that can host interchangeable payloads and move from contract award to deployment on tighter schedules. That approach reduces the value of one-off engineering and increases the value of certified production lines in the satellite bus market. It also creates a split in demand between very high-security buses for strategic missions and commercial-standard buses adapted for proliferated defense networks. Suppliers that can serve both tiers are better placed to win follow-on work as procurement models continue to evolve. This keeps the satellite bus market closely tied to defense modernization plans, even when individual programs are paused or reviewed.

Price Inflection from Mass-Produced Modular Buses Resets Buyer Expectations

Pricing in the satellite bus market is changing as manufacturers build more capacity around repeatable modular platforms rather than custom development cycles. Apex announced more than USD 200 million in additional funding in June 2026 at a USD 2.30 billion valuation to scale high-rate satellite production for proliferated constellations, which supports that factory-led shift.[2]Apex Space, “Apex Announces Additional Fundraising at $2.3B Valuation to Scale High-Rate Satellite Production for Proliferated Constellations,” Apex Space, apexspace.com In September 2025, Apex had also disclosed a USD 200 million Series D round and its plans to expand Factory One to more than 100,000 square feet, targeting a 50% increase in output capacity. As more suppliers publish clearer production targets and platform road maps, buyers in the satellite bus market are treating the bus as a standardized input rather than a fully bespoke asset. That shifts differentiation toward payload capability, mission software, and integration speed. It also puts pressure on slower manufacturers whose cost base still relies on long engineering cycles and low factory utilization.

Dual-Use Intelligence-Surveillance Requirements Expand Total Addressable Market

Dual-use mission planning is broadening the addressable customer base in the satellite bus market, as a single bus family can now support both civil and defense payload options. Buyers are placing more value on secure interfaces, hardened data handling, and architectures that can support rapid mission reconfiguration. This is significant in the satellite bus market because it improves bus utilization across multiple customer classes and spreads engineering costs over larger production runs. The design trade-off is a higher unit cost, but that premium becomes easier to justify when government contracts support the production baseline. It also favors suppliers that already understand compliance, mission assurance, and flexible subsystem integration. As a result, the satellite bus market is seeing stronger demand for platforms that sit between pure commercial buses and fully bespoke military spacecraft.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent semiconductor/reaction-wheel shortages | -1.90% | Global (most acute in Asia-Pacific manufacturing hubs) | Short term (≤ 2 years) |

| Orbital-debris mitigation costs | -1.20% | Global | Long term (≥ 4 years) |

| ITAR/export-control compliance burden | -1.00% | Global, particularly non-US operators | Medium term (2-4 years) |

| Insurance premium spikes for small-sat buses | -0.80% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Semiconductor and Reaction-Wheel Shortages Constrain Production Ramp

The satellite bus market still faces a real bottleneck in critical subsystems, especially in radiation-hardened electronics and motion-control components. Factory expansion alone does not solve this issue, because final output still depends on a narrow supplier base for flight-qualified parts. That makes the satellite bus market vulnerable when replenishment and new constellation orders arrive simultaneously. The pressure is stronger for companies that do not control subsystem production in-house and must compete for long-lead inventory. Manufacturers with internal capability in star trackers, wheels, power distribution, or avionics, therefore, hold an operational advantage. This supply imbalance slows capacity ramp-up across the satellite bus market even when customer demand remains strong.

Orbital-Debris Mitigation Costs Add Structural Expense to Small-Sat Bus Programs

Debris mitigation rules are increasing the cost floor for the satellite bus market, especially for LEO programs that depend on large fleets and frequent replenishment. The FCC adopted a five-year post-mission disposal rule for LEO satellites, which tightened compliance expectations for propulsion, deorbit planning, and related hardware. NASA documented that deorbit systems, active propulsion, and full regulatory compliance can add meaningful unit costs to small spacecraft programs.[3]National Aeronautics and Space Administration, “Small Spacecraft Technology State of the Art 2024, Deorbit Systems Chapter,” NASA, nasa.gov Those requirements matter in the satellite bus market because non-revenue compliance spending rises quickly as fleets reach the hundreds. They also add design complexity for manufacturers serving operators across several jurisdictions. Over time, the satellite bus market is likely to adopt these rules as standard engineering requirements, but near-term cost pressures remain significant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Communication Infrastructure Anchors Demand While Navigation Leads Growth

Communication satellites accounted for 75.60% of revenue in 2025, which shows that the satellite bus market still depends most heavily on broadband and connectivity deployments. This lead reflects the volume effect created by constellation programs that need repeated bus purchases rather than isolated mission builds. In the market, communication missions also benefit from design reuse, as operators often maintain common platform families across several payload refresh cycles. That lowers integration risk and helps sustain production cadence across multiple launch windows. SpaceX's multi-year Starlink production record illustrates that demand for communications continues to drive the pace of the satellite bus market.

Navigation is forecast to grow at a 16.01% CAGR through 2031, making it the fastest-growing application in the satellite bus market. The growth case extends beyond GPS augmentation and increasingly includes backup positioning, timing resilience, and defense-related navigation architectures. The US NTIA inventory in May 2025 confirmed a contract for 258 Pulsar LEO satellites intended to provide complementary and backup PNT services in the L- and C-bands. That supports demand for buses with stronger interference protection, secure operations, and more reliable power and pointing performance. It also means the satellite bus market is becoming more exposed to navigation use cases where commercial and national security needs overlap.

By Satellite Mass: Large Platforms Hold Share as Mid-Weight Class Accelerates

Platforms above 1,000 kg accounted for 53.55% of revenue in 2025, indicating that the satellite bus market continues to derive most of its value from large spacecraft, even as unit volumes shift toward smaller buses. These heavier platforms remain important for high-throughput communications, strategic missions, and payloads that need high power, long life, or large apertures. In value terms, they anchor the satellite bus market because one program can generate far more revenue than a larger batch of lighter spacecraft. This explains why major contractors remain active in the large-bus competition even as the broader market focus shifts toward proliferated constellations. The segment, therefore, remains critical to revenue stability for suppliers with deep integration and mission-assurance capability.

The 100 to less than 500 kg segment is projected to expand at a 16.20% CAGR through 2031, making it the most dynamic mass class in the satellite bus market. Apex highlighted the Nova platform in the 200 to 500 kg range when it announced its April 2025 Series C funding round, showing how suppliers are targeting this weight band with productized offerings. In February 2026, Kepler Communications selected Kongsberg NanoAvionics as a preferred European bus provider for hosted payload missions weighing up to 500 kg, confirming active demand in this class. This weight range suits missions that need more capability than nanosatellites but lower cost and faster deployment than large buses. It is also the part of the satellite bus market where modular power systems, optical links, and flexible payload accommodation can scale most efficiently. As a result, the 100 to less than 500 kg class is becoming a focal point for the satellite bus industry and for competition between new-space specialists and established suppliers.

By Orbit Class: LEO Commands Revenue Share as GEO Posts the Fastest Growth

LEO accounted for 71.15% of revenue in 2025 and represented the largest share of the satellite bus market, as deployment volumes remain concentrated in low Earth orbit. In the satellite bus market, LEO benefits from broadband constellations, Earth observation fleets, and shorter replacement cycles that support recurring orders. The FCC five-year disposal rule also reinforces that replacement rhythm by tightening end-of-life requirements for LEO operators. That combination keeps LEO central to factory planning, supplier scheduling, and modular bus design across the satellite bus market. It also favors manufacturers that can support batch production and rapid integration without long customization cycles.

GEO is projected to grow at a 15.50% CAGR through 2031, indicating that the satellite bus market still has a strong, high-value pipeline beyond proliferated LEO systems. This growth is being supported by demand for defense and strategic communications rather than by a broad rebound in traditional commercial GEO orders. In July 2026, Space Systems Command awarded Boeing a USD 2.80 billion contract for the first 2 Evolved Strategic Satellite Communications satellites, with options that could lift the program to USD 3.75 billion. Large strategic programs like this keep high-mass GEO bus lines active and preserve specialist capabilities in secure communications and mission assurance. They also help the satellite bus market maintain revenue depth in orbital segments where unit volume is lower, but contract value is much higher.

By End User: Commercial Leadership Intact as Defense Demand Accelerates

Commercial operators accounted for 66.20% of revenue in 2025, indicating that the satellite bus market still leans most heavily on private constellation deployment. That position reflects the scale of broadband programs and the willingness of commercial operators to buy repeated batches of similar spacecraft. The satellite bus market benefits from this pattern because recurring commercial orders enable better factory utilization and clearer platform roadmaps. KONGSBERG signed a contract in April 2025 to deliver 280 microsatellites to SpinLaunch's Meridian Space LEO communications constellation, underscoring the depth of commercial demand for repeatable bus supply. Even as individual launch schedules shift, commercial demand remains the primary driver of volume for the satellite bus market.

The government and military end-user segment is projected to grow at a 16.45% CAGR through 2031, making them the fastest-growing end-user group in the satellite bus market. This reflects rising interest in resilient architectures, sovereign constellations, and mission sets that need faster refresh cycles. In March 2025, Kongsberg NanoAvionics launched the first satellite for Norway's N3X maritime surveillance constellation, contracted by the Norwegian Armed Forces, underscoring sustained government demand for proliferated systems. The government pipeline also rewards suppliers that can combine secure interfaces with scalable manufacturing. That is why the satellite bus market is seeing stronger overlap between commercial production methods and defense procurement requirements.

Geography Analysis

North America retained 68.40% of revenue in 2025 and held the largest regional share of the satellite bus market. The region remains the center of the satellite bus market because it combines deep government demand with the world's largest commercial constellation base. SpaceX's sustained Starlink build-and-deployment program continues to shape production expectations and supply chain behavior across the regional satellite bus market. In July 2026, Space Systems Command awarded Boeing a USD 2.80 billion strategic communications contract, which shows that high-value government demand remains active in North America. Apex also raised more than USD 200 million in June 2026 to support the scale-up of proliferated constellations, confirming that capital continues to back domestic manufacturing expansion in the satellite bus market.

Asia-Pacific is projected to record the fastest CAGR of 17.05% through 2031, and that keeps the satellite bus market pointed toward a broader manufacturing base over the forecast period. Growth in the region is being supported by state-backed constellation plans, domestic supply chain development, and more active private-sector participation. Japan's 2025 space strategy supports low-cost, mass-producible solar cells and arrays, giving the regional satellite bus market a clearer hardware foundation for future bus output. In April 2025, Aerospacelab announced that JAXA had selected it, through Mitsui Bussan Aerospace, to supply a satellite bus platform for a maritime domain awareness demonstration mission in Japan. These moves show that the satellite bus market in Asia-Pacific is developing through both institutional backing and targeted supplier partnerships.

Europe held the third-largest regional share, and the satellite bus market there is defined by sovereign capability building and institutional program continuity. The region still relies heavily on established primes, but the supplier base is widening to include smaller manufacturers that win targeted science, defense, and hosted-payload work. In October 2025, ESA selected Kongsberg NanoAvionics to build a 12-16U CubeSat platform for the IOD/IOV in-orbit demonstration program, which shows continued institutional support for smaller European bus providers. In February 2026, Kepler selected Kongsberg NanoAvionics as a preferred European satellite bus provider for hosted payload missions up to 500 kg, reinforcing Europe's position in configurable mid-weight platforms. South America, the Middle East, and Africa remain smaller opportunity pools in the satellite bus market, but selective sovereign communications and Earth observation programs still create openings for aligned suppliers.

Competitive Landscape

The satellite bus market is moderately concentrated at the top, but it is becoming broader in the middle tiers as new manufacturers build capacity around repeatable bus families. Established companies still hold an advantage in large GEO and sensitive government missions because customers value integration depth, heritage, and mission assurance. At the same time, the satellite bus market is rewarding companies that can deliver standardized platforms at faster rates and with more transparent production plans. That is changing competition from a heritage-led model to a capacity-led model in several program categories. It also means suppliers that once played only supporting roles are now visible competitors in the satellite bus market.

Boeing's July 2026 award for the first 2 Evolved Strategic Satellite Communications satellites is a clear example of how legacy primes continue to win the most demanding secure missions. Apex's June 2026 funding round shows the opposite side of the market, where capital is being used to scale factory throughput for proliferated constellations and faster-turn production. KONGSBERG's April 2025 contract to deliver 282 microsatellites to SpinLaunch is another strong signal that commercial volume programs are opening real space for scalable suppliers. These examples show that the satellite bus market is not moving toward one uniform competitive pattern. Instead, it is separating into large secure missions, high-rate commercial production, and a mid-weight segment where supplier positions are still forming.

The 100 to less than 500 kg class remains the main white-space opportunity in the satellite bus market because no single company fully controls it at scale. Suppliers are competing there through configurable product lines, hosted payload capability, and easier integration with optical links and software-defined subsystems. Kepler's February 2026 selection of Kongsberg NanoAvionics for missions up to 500 kg suggests that preferred-supplier relationships are increasingly important in this part of the satellite bus market. The result is a multi-tier competitive map in which legacy primes dominate sensitive, high-value work, while specialized manufacturers continue to gain ground in scalable constellation programs. This keeps the satellite bus market open enough for new contract wins, but not fragmented enough to remove the value of heritage and compliance credentials.

Satellite Bus Industry Leaders

Airbus SE

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Alenia Space (Thales Group)

Honeywell Aerospace Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Apex raised more than USD 200 million in growth funding, increasing its valuation to USD 2.3 billion. The funding supports the expansion of its Los Angeles manufacturing campus, the vertical integration of key subsystems, and the production of ahead-of-need satellite buses for proliferated commercial and national security constellations at scale.

- February 2026: Kepler selected Kongsberg NanoAvionics as its preferred European satellite bus provider for hosted payload missions up to 500 kg. The partnership enables NanoAvionics customers to access Kepler’s optical data relay network and on-orbit compute services, supporting low-latency, high-throughput inter-satellite connectivity on MP42 microsatellite and CubeSat platforms.

- October 2025: ESA selected Kongsberg NanoAvionics to build a 12–16U CubeSat platform for its ESA-EC IOD/IOV program. NanoAvionics will manage design, assembly, integration, testing, ground segment, and operations, while the spacecraft will demonstrate and validate next-generation European technologies in orbit after final payload selection.

Global Satellite Bus Market Report Scope

A satellite bus is the primary spacecraft platform that houses and integrates the non-payload subsystems required to operate a satellite in orbit. It provides mechanical structure, electrical power generation and distribution, propulsion, thermal regulation, attitude determination and control, command and data handling, and telemetry, tracking, and communication interfaces. The bus maintains spacecraft stability, manages onboard resources, supports payload pointing, controls orbital maneuvers, routes mission data, and enables continuous health monitoring, fault management, and command execution throughout the satellite's operational life.

The satellite bus market is segmented by application, satellite mass, orbit class, end-user, and geography. By application, the market is segmented into communications, Earth observation, navigation, space observation, and others. By satellite mass, the market is segmented into less than 10 kg, 10 to less than 100 kg, 100 to less than 500 kg, 500 to less than 1,000 kg, and greater than 1,000 kg. By orbit class, the market is segmented into low Earth orbit (LEO), medium Earth orbit (MEO), and geosynchronous Earth orbit (GEO). By end-user, the market is segmented into commercial, government and military, and others. The report also covers the market sizes and forecasts for the satellite bus market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

| Less than 10 kg |

| 10 to Less than 100 kg |

| 100 to Less than 500 kg |

| 500 to Less than 1,000 kg |

| Greater than 1,000 kg |

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geosynchronous Earth Orbit (GEO) |

| Commercial |

| Government and Military |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Communication | ||

| Earth Observation | |||

| Navigation | |||

| Space Observation | |||

| Others | |||

| By Satellite Mass | Less than 10 kg | ||

| 10 to Less than 100 kg | |||

| 100 to Less than 500 kg | |||

| 500 to Less than 1,000 kg | |||

| Greater than 1,000 kg | |||

| By Orbit Class | Low Earth Orbit (LEO) | ||

| Medium Earth Orbit (MEO) | |||

| Geosynchronous Earth Orbit (GEO) | |||

| By End User | Commercial | ||

| Government and Military | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.