Satellite Antenna Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

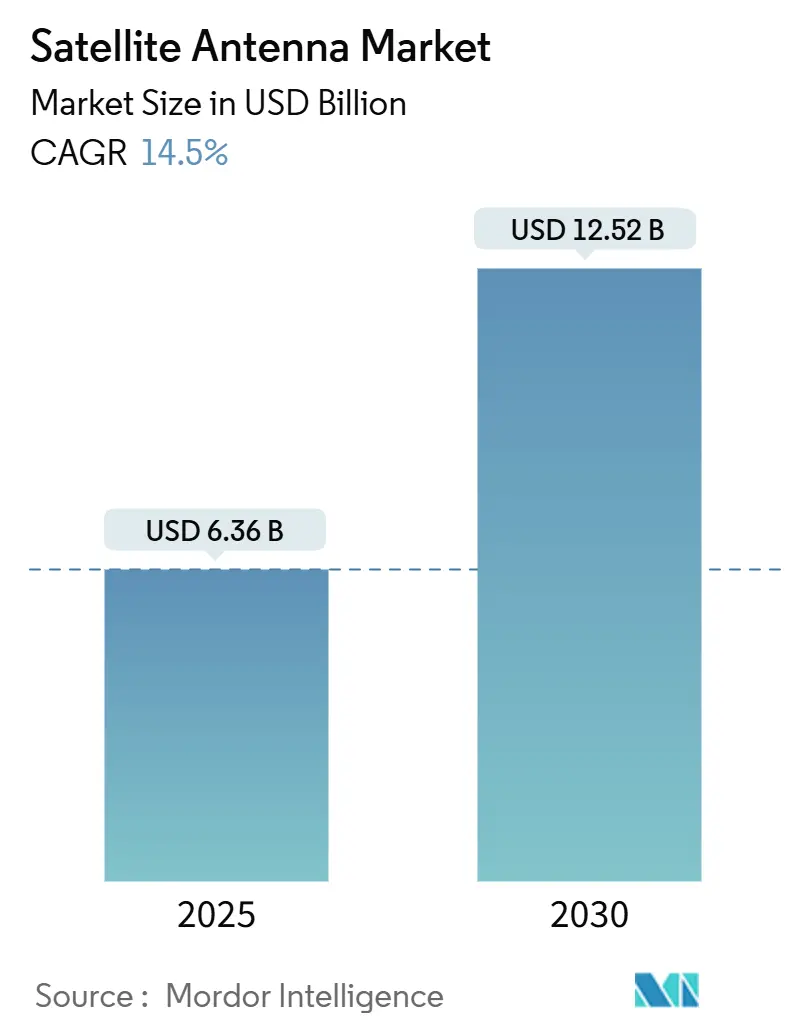

| Market Size (2025) | USD 6.36 Billion |

| Market Size (2030) | USD 12.52 Billion |

| Growth Rate (2025 - 2030) | 14.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

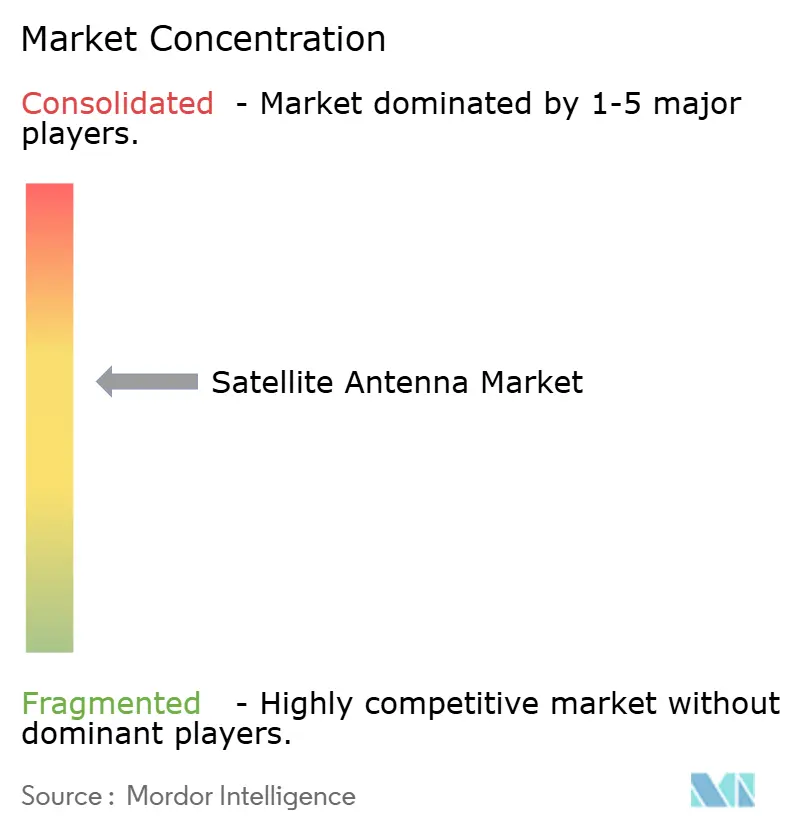

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Satellite Antenna Market Analysis by Mordor Intelligence

The Satellite Antenna Market size is estimated at USD 6.36 billion in 2025, and is expected to reach USD 12.52 billion by 2030, at a CAGR of 14.5% during the forecast period (2025-2030).

Strong demand for high-throughput connectivity, the roll-out of multi-orbit constellations, and falling antenna production costs are accelerating adoption across commercial and defense domains. Software-defined beam steering, lighter composites, and highly integrated chipsets are improving performance while lowering lifetime ownership costs for operators. Growth is also being reinforced by strategic mergers that broaden product portfolios and by governments treating space infrastructure as a pillar of digital sovereignty. These converging factors keep the satellite antenna market on a double-digit growth path even as suppliers navigate regulatory and orbital-debris complexities.[1]Federal Communications Commission, “Part 25—Satellite Communications Service Rules,” fcc.goV

Key Report Takeaways

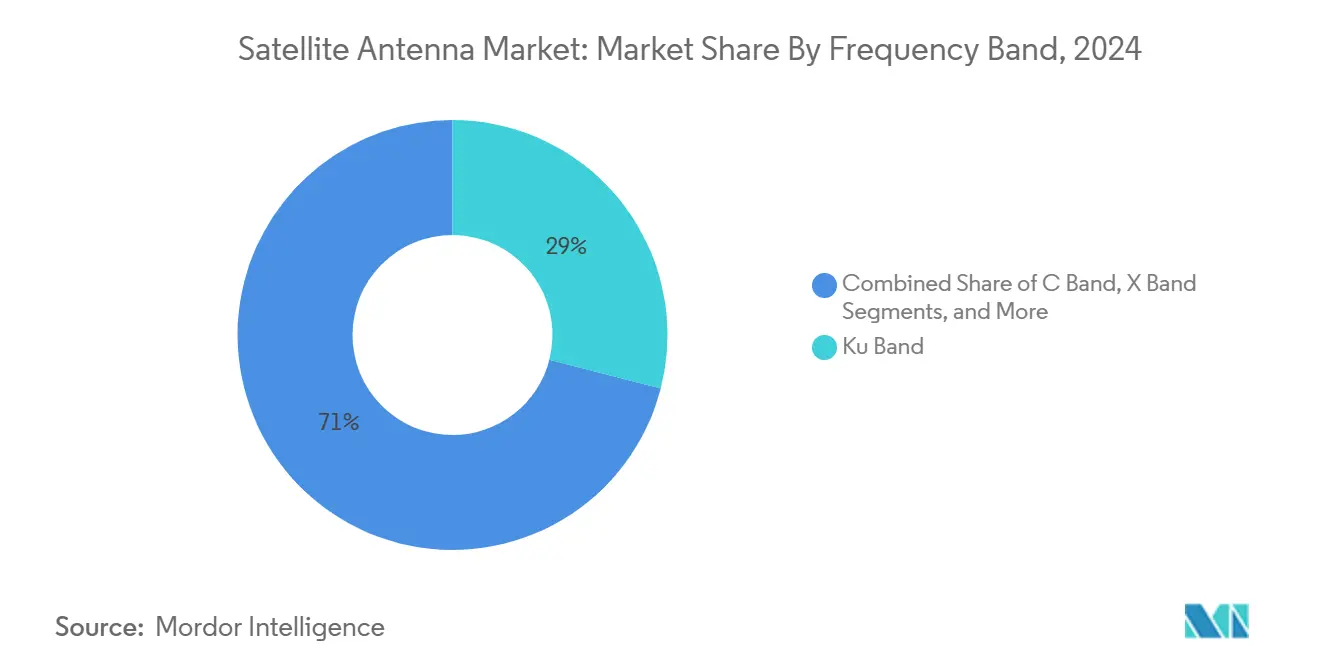

- By frequency band, Ku Band led with 29% satellite antenna market share in 2024; Ka Band shows the fastest trajectory with a 15.2% CAGR through 2030.

- By antenna type, parabolic reflector systems commanded 38% of the satellite antenna market size in 2024, while flat-panel ESA solutions are expanding at an 18.4% CAGR to 2030.

- By application, maritime captured 28% revenue share of the satellite antenna market in 2024; airborne connectivity is advancing at a 15.4% CAGR to 2030.

- By end user, government and defense held 54% of the satellite antenna market size in 2024; commercial services record a 14.9% CAGR through 2030.

- Asia Pacific registers the fastest regional CAGR at 14.6% between 2025-2030, fueled by large-scale constellation and ground segment investments in China and India.

Global Satellite Antenna Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of LEO broadband constellations | +3.9% | North America, Europe, global underserved regions | Medium term (2-4 years) |

| Rapid militarization of space (MilSATCOM) | +2.8% | North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| High-throughput satellite (HTS) adoption | +2.6% | Global | Medium term (2-4 years) |

| Commercial in-flight connectivity boom | +2.4% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| ESA flat-panel cost curve deflation | +1.7% | North America, Europe first; global thereafter | Medium term (2-4 years) |

| Lunar and cislunar communications demand | +1.2% | North America, Europe, China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of LEO broadband constellations

Low Earth Orbit projects such as Starlink and OneWeb are rewriting link-budget assumptions, pushing operators to deploy electronically steered arrays that can track dozens of fast-moving satellites per minute. In September 2024, 411 constellations were registered, yet only 5% were fully launched, leaving extensive runway for antenna suppliers. Compact phased arrays now include integrated GNSS receivers and edge computing, letting terminals auto-switch beams across LEO, MEO, and GEO layers. Remote communities, maritime routes, and disaster-response teams are early beneficiaries. Because phased arrays eliminate mechanical parts, lifetime maintenance costs fall, reinforcing the economic case for large-scale roll-outs. Vendors able to mass-produce dual-orbit terminals at consumer-electronics price points will capture outsized value as the satellite antenna market broadens to handset-like volumes.

Rapid militarization of space (MilSATCOM)

Defense authorities see assured, jam-resistant links as mission-critical. The U.S. FY 2025 budget allocates USD 25.2 billion to space-based systems, triggering procurement of multi-band, directive antennas that operate in contested electromagnetic environments. Battle-proven requirements include side-lobe suppression, anti-spoofing, and dynamic beam hopping to mitigate interference. Parallel programs in Europe and Asia-Pacific further widen demand. Militaries also push for lighter terminals to fit small UAVs and dismounted soldiers, encouraging breakthroughs in GaN power amplifiers and conformal composites. Over the long term, secure optical cross-links will complement RF, but near-term spending remains anchored in advanced phased-array RF architectures, sustaining momentum for the satellite antenna market.

High-throughput satellite (HTS) payload adoption

HTS platforms increase spectral efficiency via spot beams and frequency reuse, reducing cost per bit by an order of magnitude. NASA’s Ka-band relay evolution targets up to 26 Tb/day for Earth-observation missions like NISAR, demanding antennas that handle wider instantaneous bandwidths without self-heating.[2]National Aeronautics and Space Administration, “Ka-band Relay Communications Roadmap,” nasa.gov Ground and aero terminals now integrate multi-beam capability, enabling on-the-fly switching between HTS clusters for load balancing. Suppliers invest in AI-driven beam management to curb cross-pol interference and make the most of scarce Ka-band spectrum. As operators proliferate HTS payloads, especially in GEO and MEO, antenna ecosystems that support automated spectrum coordination will secure a durable competitive edge.

Commercial in-flight connectivity (IFC) boom

Passenger expectations for streaming-grade Wi-Fi have transformed connectivity from a differentiator into table stakes. ThinKom’s ThinAir Ka1717, tailored for regional jets, slashes drag and weight penalties compared with earlier radomes. Fleet-retrofit programs accelerate because airlines monetize connectivity through ancillary revenue and operational analytics. Viasat’s Amara platform pairs a new aero antenna with beam-roaming software, promising crew interfaces similar to standard ACARS systems. As flight hours rebound beyond pre-pandemic levels, antenna OEMs that certify multi-orbit terminals across Airbus and Boeing families will ride the fastest compound-annual demand within the satellite antenna market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ku/Ka-band rain fade in equatorial regions | -0.7% | Southeast Asia, tropical Africa, equatorial Latin America | Long term (≥ 4 years) |

| Export-control bottlenecks on phased-array ICs | -0.6% | China, Russia, emerging markets | Medium term (2-4 years) |

| Mounting orbital-debris insurance premiums | -0.5% | Global, higher for LEO operators | Medium term (2-4 years) |

| CAPEX crunch at emerging-market telcos | -0.4% | Africa, Latin America, Southeast Asia, Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ku/Ka-band rain fade in equatorial regions

Heavy rainfall events attenuate Ku and Ka signals by up to 20 dB, forcing operators to oversize link margins or revert to lower frequencies. Tropical micro-bursts in Indonesia and Brazil create unpredictable fades that undermine SLAs for enterprise and backhaul customers. Mitigation tactics include adaptive coding, site diversity, and dual-band terminals that fall back to C band during storms, yet these solutions raise capex and opex for service providers. Future climate variability adds uncertainty, making some telcos reluctant to commit to Ka-centric networks despite their capacity advantages. Consequently, adoption curves in equatorial belts may lag the global satellite antenna market trend.

Export-control bottlenecks on phased-array chipsets

ITAR and EAR restrictions limit access to advanced RF beam-former ICs, slowing phased-array roll-outs in sanctioned or high-risk jurisdictions. FCC rule changes in August 2024 further tightened compliance obligations for U.S. firms selling dual-use components fcc.gov. Chinese, Russian, and several Global South manufacturers respond by launching indigenous chip programs, but performance parity remains elusive. The added licensing paperwork and potential penalties lengthen product lead times and increase inventory buffers, constraining supply elasticity for the satellite antenna market.

Segment Analysis

By Frequency Band: Ka-Band Reshapes Connectivity Economics

Ku Band accounted for 29% of the satellite antenna market in 2024, capitalizing on mature ground infrastructure and balanced rain-fade resilience. The segment continues to anchor broadcast and VSAT services, especially where regulatory clearances already exist. In contrast, Ka Band is scaling rapidly at a 15.2% CAGR, attracting broadband operators that seek lower cost per bit and flexible spot-beam architectures. This growth trajectory translates to an expanding satellite antenna market size for Ka terminals, underpinned by NASA’s requirement to route 26 Tb/day on its upcoming Earth-observation constellation. C Band maintains relevance in cyclone-prone zones, while X Band remains a defense niche thanks to interference immunity. Emerging multi-band antennas blur traditional silos, permitting real-time frequency switching, a capability that uplifts overall system availability and widens supplier addressable revenue streams within the satellite antenna market.

Multi-beam flat-panel designs now facilitate simultaneous Ku and Ka connectivity, enabling operators to reverse traffic when rain fade hits. Suppliers integrating programmable RF front-ends can dynamically allocate power where needed, lifting spectral efficiency. These advances transform value propositions for mobile VSAT, cruise, and oil-and-gas platforms. As such, the satellite antenna market size for high-frequency terminals is forecast to double by 2030, though suppliers must embed weather-adaptive intelligence to unlock full demand across tropical geographies.

Note: Segment shares of all individual segments available upon report purchase

By Antenna Type: Flat-Panels Disrupt Traditional Dominance

Parabolic reflectors held 38% share of the satellite antenna market size in 2024, favored for static gateways that prize high gain per dollar. Mechanical gimbals remain cost-effective for large cruise ships and teleport hubs. Yet flat-panel electronically steered arrays, expanding at an 18.4% CAGR, are redefining mobility use cases. Anokiwave-powered panels are now factory-calibrated, slashing installation time and supporting conformal fuselage mounting on narrow-body aircraft. Inflatable dishes under prototyping promise 20:1 packing efficiency, catering to launch-mass-sensitive small satellites.

Hybrid architectures blend small parabolic segments with phase-shifter sub-arrays, extracting the high-gain benefits of dishes and the agility of ESAs. Vendors exploring flexible dielectric materials can bend antennas around vehicle roofs, erasing aerodynamic drag penalties. Consequently, the addressable satellite antenna market widens to include personal vehicles, trains, and urban drone taxis, all of which require ultra-low-profile terminals. Reflector incumbents respond by embedding auto-pointing and health-monitoring firmware to protect installed bases, signaling a coexistence rather than outright displacement scenario through 2030.

By Application: Maritime Leads While Airborne Accelerates

Maritime vessels generated 28% of 2024 revenue for the satellite antenna market, relying on continuous links for navigation, weather avoidance, and crew welfare. Premium cruise operators adopt redundant tri-band terminals to meet passenger streaming demand, boosting average antenna counts per hull. Offshore oil rigs likewise require high-availability networks that withstand salt corrosion and mechanical vibration, favoring robust radome-protected systems. Airborne applications, however, record the fastest 15.4% CAGR, propelled by regional jet and business-aviation upgrades. Gogo’s 2Ku network leverages more than 180 Ku satellites, and its proprietary dual-array antenna yields 15% lower drag than first-generation radomes.

Spaceborne use-cases, although smaller in unit terms, involve high-margin contracts for deep-space probes and cross-link networks. Recent dual-band horn antennas qualified for the Tian Wen-2 mission demonstrate iso-flux beam shaping with 4 dB axial ratio, a benchmark for future lunar relays. Land-mobile segments expand as NGOs and emergency responders deploy auto-acquire terminals that fold into backpacks, broadening humanitarian connectivity. Collectively, these diverse environments bolster resilience of the satellite antenna market against single-segment downturns.

Note: Segment shares of all individual segments available upon report purchase

By End User: Defense Dominance Amid Commercial Growth

Government and defense customers accounted for 54% of satellite antenna market share in 2024, sustaining secure, resilient links for command, ISR, and nuclear-command-and-control. A recent USD 33 million U.S. Air Force contract awarded to Viasat for multi-band ground antennas typifies continuous modernization cycles. Military requirements for anti-jamming, rapid beam switching, and survivability at the physical layer keep average selling prices higher than commercial equivalents, supporting supplier gross margins.

Commercial segments, expanding at 14.9% CAGR, are diversifying from maritime and aero into connected agriculture, mining, and direct-to-device messaging. Iridium’s ThinSat 300 qualification for the FlexMove network underscores a push toward smaller, battery-powered phased arrays for field crews. Enterprise VSAT providers bundle cloud gateway services, reducing integration overhead for end-users and tilting procurement toward turnkey solutions. As private-sector orders rise, competitive dynamics intensify, pushing vendors to accelerate product refresh cycles and add AI-based spectrum management.

Geography Analysis

Satellite Antenna Market in North America

Asia Pacific records the quickest expansion, charting a 14.6% CAGR to 2030 as China, India, Japan, and South Korea scale multi-orbit systems and indigenous manufacturing. China’s fifth Antarctic outpost, opened in February 2024, showcases dual-use satellite dishes that serve science and defense agendas.[3]Center for Strategic and International Studies, “China’s Antarctic Station Footprint,” csis.org India’s production-linked incentives, aligned with its “Make in India” drive, catalyze local fabrication of feed horns, radomes, and RFIC subsystems, lowering costs for regional operators. Japan’s auto sector readies connected-car services using non-terrestrial backhaul, prompting suppliers to miniaturize antennas for rooftop integration.

North America remains the largest satellite antenna market thanks to deep aerospace supply chains, heavy defense spending, and entrepreneurial space ventures. The U.S. Space Force maintains the Satellite Control Network, operating 19 dishes at 75% utilization, with plans for 12 new high-capacity antennas starting 2025. Canada’s Polar communications programs add demand for low-temperature-tolerant antennas. Mexico and other Latin peers leverage GEO gateways for internet-community Wi-Fi, although capex pressures curb near-term scale.

Europe holds robust share, reinforced by ESA technology demonstrators such as the shaped mesh reflector from the AMPER project that supports military and climate-monitoring missions. Germany and the UK fund sovereign teleports to secure data autonomy, while mobile network operators test backhaul-over-satellite in rural Scotland and Bavaria. Eastern European telcos adopt lease-to-own models to overcome currency volatility, a tactic that smooths order pipelines for antenna suppliers. The Middle East, buoyed by GCC sovereign wealth funds, backs GEO VHTS projects, and Saudi Arabia’s roadmap foresees a trebling of national space revenues by 2030. South America trails but shows pockets of growth in Brazil, where oil-and-gas offshore connectivity mandates dual-redundant antennas. Collectively, these dynamics keep regional demand diversified within the satellite antenna market, insulating global revenue from macro shocks.

Competitive Landscape

The satellite antenna market shows moderate consolidation: top ten vendors control roughly 60% of global revenue, yet niche newcomers disrupt with focused innovations. MDA Space’s planned USD 193 million acquisition of SatixFy secures beam-forming ASIC intellectual property, allowing tighter vertical integration.[4]MDA Space, “MDA to Acquire SatixFy,” mdaspace.com ThinKom partners with AI routing firm Quvia to blend hardware with intelligent traffic steering, pointing to software as a value-multiplier.

Technology differentiation centers on multi-orbit readiness and integrated spectrum management. Kymeta’s patent for an ESA that roams across LEO, MEO, and GEO under a single panel demonstrates this shift. White-space opportunities loom in direct-to-device IoT, evidenced by Iridium’s Project Stardust targeting NB-IoT connectivity on existing LEO assets. Suppliers also court enterprise customers with consumption-based pricing, cushioning opex for remote mining and energy clients.

Mergers among ground-segment specialists mirror satellite operator consolidation. DirecTV’s merger with Dish reshapes U.S. pay-TV, potentially standardizing antenna SKUs for set-top installs. EQT’s bid for an 80% stake in Eutelsat’s ground-station business hints at private-equity appetite for infrastructure support services, further redrawing partner ecosystems. Market incumbents must therefore balance defensive M&A with organic R&D to maintain share in a satellite antenna market where innovation cycles shorten to under three years.

Satellite Antenna Industry Leaders

-

Honeywell International Inc.

-

CPI International Inc.

-

Kymeta Corporation

-

Norsat International Inc.

-

COBHAM LIMITED (AI Convoy (Luxembourg) S.a r.l.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ThinKom showcased the ThinAir Plus antenna at Aircraft Interiors Expo 2025 and partnered with Quvia for AI-driven routing software

- April 2025: Viasat introduced its Amara in-flight connectivity platform alongside a new aero antenna

- April 2025: NanoAvionics won a EUR 122.5 million contract to build 280 satellites for Meridian Space’s broadband constellation

- April 2025: Iridium completed its purchase of Satelles, expanding secure satellite time-and-location services

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the satellite antenna market as all newly manufactured parabolic, flat-panel, horn, and related antenna systems operating in Ku, Ka, C, X, L/S, and VHF/UHF bands that enable space-to-space or space-to-ground links across land, maritime, airborne, and spaceborne platforms. We value factory-gate hardware revenue in constant 2025 USD.

Scope Exclusion: We exclude VSAT airtime contracts, consumer TV-sat dishes, and phased-array modules already embedded inside full aircraft connectivity kits.

Segmentation Overview

- By Frequency Band

- C Band

- X Band

- Ku Band

- Ka Band

- L/S Band

- VHF/UHF Band

- By Antenna Type

- Parabolic Reflector

- Flat-Panel (ESA/RSA)

- Horn

- Dielectric-Resonator

- FRP-Radome

- Metal-Stamp

- By Application

- Spaceborne

- Airborne

- Maritime

- Land (Mobile and Fixed)

- By End-User

- Commercial

- Government and Defense

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- UAE

- Saudi Arabia

- Rest of the Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We validated secondary insights through interviews with antenna OEM engineers, launch-service buyers, naval communications officers, and airborne connectivity integrators across North America, Europe, and Asia-Pacific. Their guidance sharpened adoption timelines, realistic average selling prices, and failure-rate assumptions that literature alone could not reveal.

Desk Research

We began by harvesting numeric clues from tier-1 public sources, such as ITU network filings, FCC earth-station logs, NASA and ESA launch manifests, International Maritime Organization vessel registries, and SIPRI defense spending tables; these datasets let us trace annual antenna demand by platform and band with credible lineage. Our team also accessed D&B Hoovers financials, Dow Jones Factiva archives, and MarkLines aerospace parts data to cross-check supplier revenue splits and contract volumes. Company 10-Ks, investor decks, trade-show proceedings, and IEEE papers rounded out the evidence pool. The catalogue cited here is illustrative; many additional repositories informed our desk work.

Market-Sizing & Forecasting

We applied a top-down launch-and-installation reconstruction that starts with platform build counts, orbit deployments, and retrofit cycles, which are then multiplied by penetration rates and calibrated ASP curves. Select bottom-up supplier roll-ups and channel checks served as guardrails that flagged over-counts. We run a multivariate regression to 2030 using six core drivers: annual Ku/Ka launch manifests, high-throughput satellite capacity additions, defense SATCOM capital budgets, commercial in-flight connectivity fleet counts, maritime broadband activations, and flat-panel cost deflation trends. This is where Mordor Intelligence differentiates by aligning each variable with consensus ranges gathered from expert calls.

Data Validation & Update Cycle

We triangulate every forecast with independent metrics, trigger anomaly alerts inside the model, and route outputs through a two-step peer review before sign-off. Reports refresh yearly, and we perform interim updates when major launches slip, large defense contracts are awarded, or currency swings distort ASPs, ensuring clients receive a freshly reviewed dataset at delivery.

Why Mordor's Satellite Antenna Baseline Commands Reliability

Published values often diverge because firms pick different antenna families, pricing anchors, refresh cadences, and currency bases. We acknowledge those realities upfront so buyers can gauge fit.

Gap drivers usually stem from whether consumer dishes are counted, how flat-panel ASP erosion is treated, and if dual-orbit replacements are netted out. Mordor Intelligence posts figures in constant 2025 USD, updates annually, and tests scope choices with end-user interviews, whereas several publishers rely on earlier datasets, broader service inclusions, or one-off shipment extrapolations.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.36 B (2025) | Mordor Intelligence | n/a |

| USD 6.96 B (2024) | Global Consultancy A | Includes flat-panel radome service revenue and does not net out dual-orbit replacements |

| USD 4.82 B (2024) | Regional Consultancy B | Excludes defense antenna procurements and freezes Ku-band ASPs |

| USD 4.10 B (2021) | Trade Journal C | Uses older base year and relies on shipment extrapolation without recent ASP erosion adjustment |

The comparison shows that when scope breadth, price curves, and update rhythm line up coherently, estimates converge toward our balanced baseline. According to Mordor Intelligence, this disciplined, transparent path makes our numbers a dependable foundation for strategic decisions.

Key Questions Answered in the Report

What is the current size of the satellite antenna market?

The satellite antenna market size is USD 6.36 billion in 2025 and is forecast to grow to USD 12.52 billion by 2030 at a 14.5% CAGR.

Which frequency band is expanding fastest?

Ka Band is the fastest-growing frequency segment, advancing at a 15.2% CAGR thanks to high-throughput satellite adoption and broadband demand.

Why are flat-panel antennas gaining traction?

Electronically steered flat-panel antennas eliminate mechanical parts, reduce maintenance, and enable low-profile installation on aircraft, vehicles, and maritime vessels, leading to an 18.4% CAGR through 2030.

Which region represents the highest growth potential?

Asia Pacific leads growth with a 14.6% CAGR as China and India invest heavily in satellite infrastructure and domestic manufacturing capabilities.

How dominant is the defense sector in this market?

Government & defense entities hold 54% of 2024 revenue, leveraging secure, multi-band antennas for mission-critical communications, although commercial uptake is accelerating at nearly 15% CAGR.

What are the key restraints affecting market growth?

Rain fade in tropical regions, export-control constraints on phased-array chipsets, rising orbital-debris insurance costs, and limited telco capex in emerging economies collectively shave roughly 2.2 percentage points from the forecast CAGR.

Page last updated on: