| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 6.00 % |

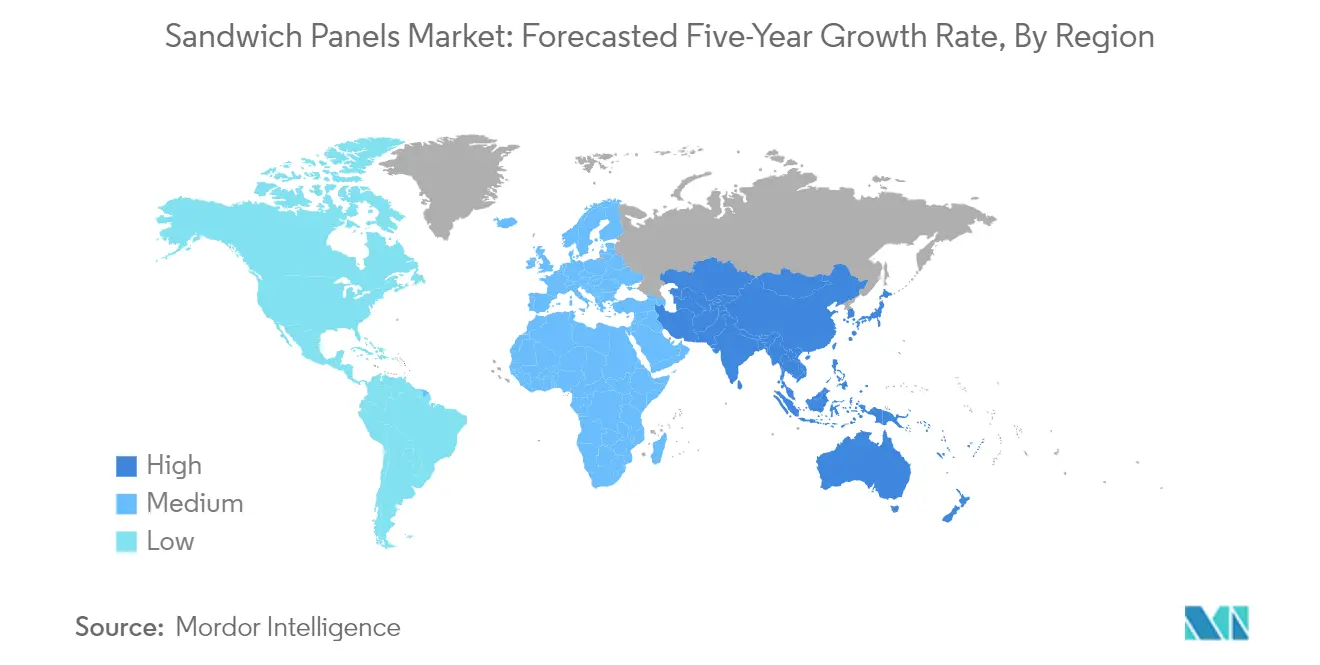

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

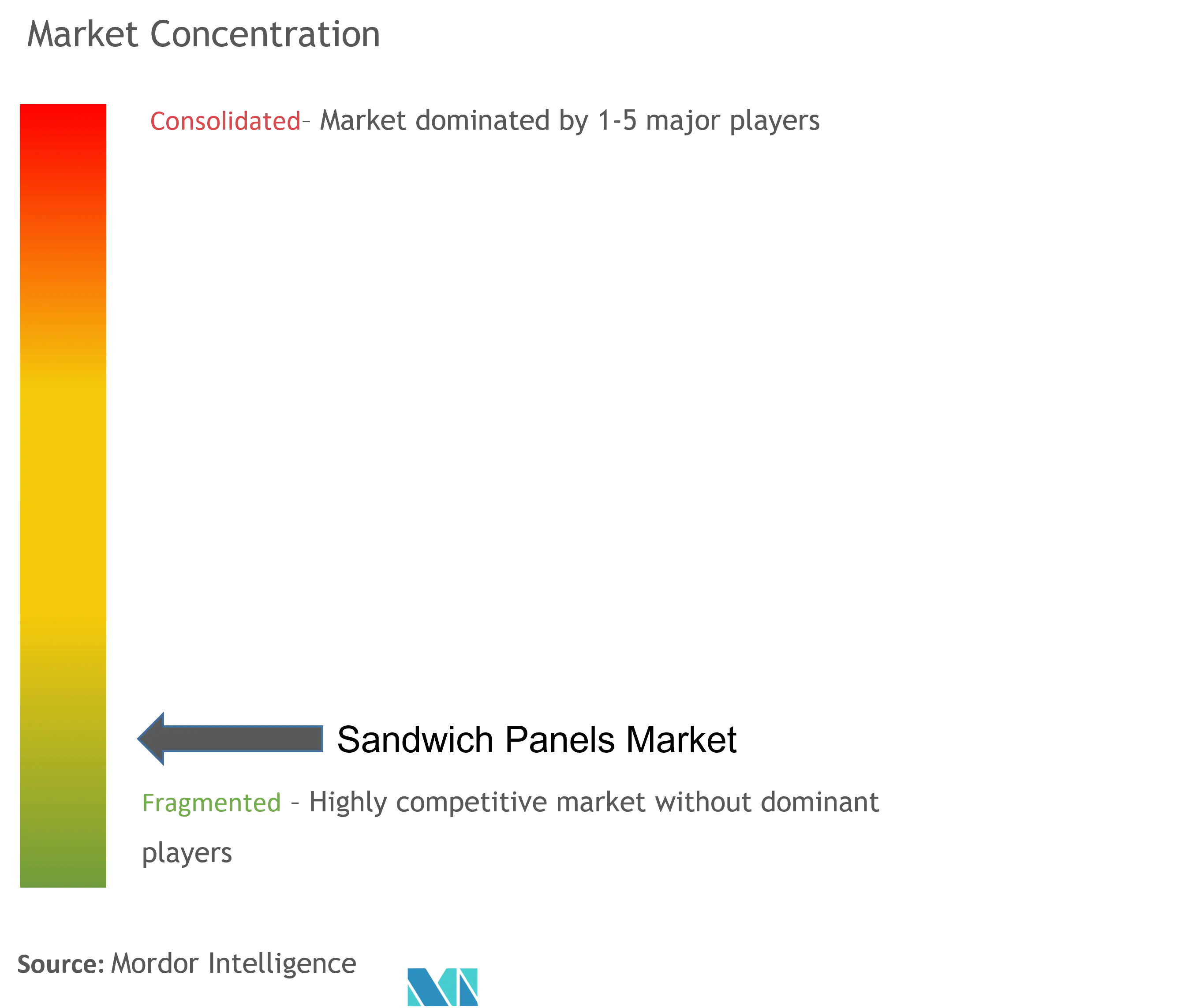

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Sandwich Panel Market Analysis

The Sandwich Panels Market is expected to register a CAGR of greater than 6% during the forecast period.

The sandwich panels industry continues to evolve alongside robust growth in the global construction sector, particularly driven by increasing industrialization and infrastructure development worldwide. In China, a key market, the construction sector demonstrated significant strength with construction output value reaching CNY 31.2 trillion (~USD 4.5 trillion) in 2022, highlighting the massive scale of development activities. The construction industry's transformation towards modern building techniques and prefabricated panel components has accelerated the adoption of sandwich panels across various applications, from industrial facilities to commercial complexes.

The commercial construction segment has witnessed substantial activity, particularly in developing economies where rapid urbanization is driving demand for modern building panels solutions. According to the US Census Bureau, the value of private construction in the United States reached USD 1,434.2 billion in 2022, demonstrating the robust nature of construction activities in developed markets. This trend is complemented by the growing emphasis on sustainable and efficient building practices, which has led to increased adoption of advanced construction materials, including structural insulated panels.

The residential construction sector has shown remarkable resilience and growth, particularly in key markets. In the United Kingdom, according to the National House Building Council (NHBC), new home registrations increased by 33% in Q3 2022 compared to the same period in 2021, indicating strong momentum in residential construction activities. This growth has been accompanied by increasing demands for high-performance insulated panel materials that can meet stringent building codes and sustainability requirements, positioning sandwich panels as a preferred choice for modern construction projects.

The hospitality sector has emerged as a significant growth driver for sandwich panels, particularly in emerging markets where tourism infrastructure development is gaining momentum. In Dubai alone, as of January 2023, there were 85 hotel projects under construction with 23,549 hotel rooms in total, showcasing the scale of commercial construction activities. The versatility of sandwich panels in providing both structural and aesthetic solutions has made them increasingly popular in such large-scale commercial developments, where speed of construction and energy efficiency are paramount considerations.

Sandwich Panel Market Trends

Growing Importance of Energy-Efficient Building Construction

The building sector has emerged as a critical focus area for energy efficiency improvements, with buildings and construction currently accounting for 30% of global energy consumption and 27% of total energy emissions, according to the International Energy Agency. In Europe alone, buildings contribute approximately 40% of energy consumption and 36% of carbon dioxide emissions, with almost 75% of building stock being energy inefficient while only 0.4% to 1.2% undergoes renovation annually. This has led to increased adoption of sandwich panels as they provide superior thermal insulation, helping reduce energy costs associated with heating, cooling, and ventilation of buildings. The panels' continuous insulation layers can be customized according to specific requirements, while their excellent airtightness helps meet increasingly stringent energy efficiency regulations.

Several major economies have implemented strict energy efficiency mandates for buildings in 2023. The United States now requires all new federal buildings and major retrofits to comply with the 2021 International Energy Conservation Code and 2019 ASHRAE Standard 90.1 building energy codes. The European Union has proposed that all new buildings must meet zero-emission requirements from January 2030, while Germany plans to spend EUR 13-14 billion annually in subsidies for energy-efficient building renovations. China's housing ministry's green construction plan aims to complete energy-efficiency renovations across more than 350 million square meters by 2025, including 100 million square meters of residential buildings and 250 million square meters of public buildings.

Understand The Key Trends Shaping This Market

Download PDF

Growing Cold Storage Applications of Structural Insulated Panels

The rapid expansion of cold storage operations globally has created substantial demand for structural insulated panels, driven by the need to extend the shelf life of fresh agricultural produce, seafood, frozen food, photographic films, chemicals, and pharmaceutical products. The global cold chain logistics market, valued at USD 255.82 billion in 2021, is projected to exceed USD 410 billion over the next eight years, indicating massive infrastructure development requirements. Sandwich panels are increasingly preferred in cold storage applications due to their superior insulation properties, ability to maintain consistent temperatures, and excellent moisture resistance characteristics that are crucial for preserving perishable goods.

The pharmaceutical sector has emerged as a major driver for cold storage applications, with pharmaceutical items accounting for over two-thirds of India's cold storage capacity by 2021. This trend is reinforced by significant investments in cold chain infrastructure - India plans to invest INR 21,000 crore (USD 2.53 billion) in setting up or upgrading cold storage panels over the next 4-5 years to address the challenges of stockpiling perishable commodities. The expansion of retail food chains by multinational companies has further accelerated the demand for cold storage facilities. Major retailers are making substantial investments in cold chain infrastructure - for instance, Walmart plans to invest around CNY 8 billion (USD 1.2 billion) in its distribution centers in China over the next two decades.

Increasing Demand for PVDF-based Aluminum Composite Panels

PVDF-based aluminum composite panels have gained significant traction in the construction industry due to their superior weatherability and durability characteristics. These panels combine thermoplastic resin as the matrix with continuous glass fiber as reinforcement material, offering an optimal balance of low cost, high strength, and low density. The PVDF coating, with a content typically exceeding 70% to ensure color durability, provides exceptional resistance to external environmental damage and can maintain its performance for over twenty years, making it particularly suitable for building exterior applications.

The growing emphasis on sustainable and long-lasting building materials has further accelerated the adoption of PVDF-based aluminum composite panels. These panels demonstrate excellent resistance to water, fine dust, and various pollutants, incorporating self-cleaning characteristics through Nano-PVDF technology. The panels are also highly valued for their versatility in architectural applications, as they can be manufactured with various surface finishes and colors while maintaining consistent quality and performance. Their application has expanded beyond traditional commercial construction to include high-rise buildings and skyscrapers, where their lightweight nature, ease of installation, and aesthetic appeal make them particularly advantageous for exterior cladding applications.

Segment Analysis: Core Material

Polyurethane (PUR) Segment in Sandwich Panels Market

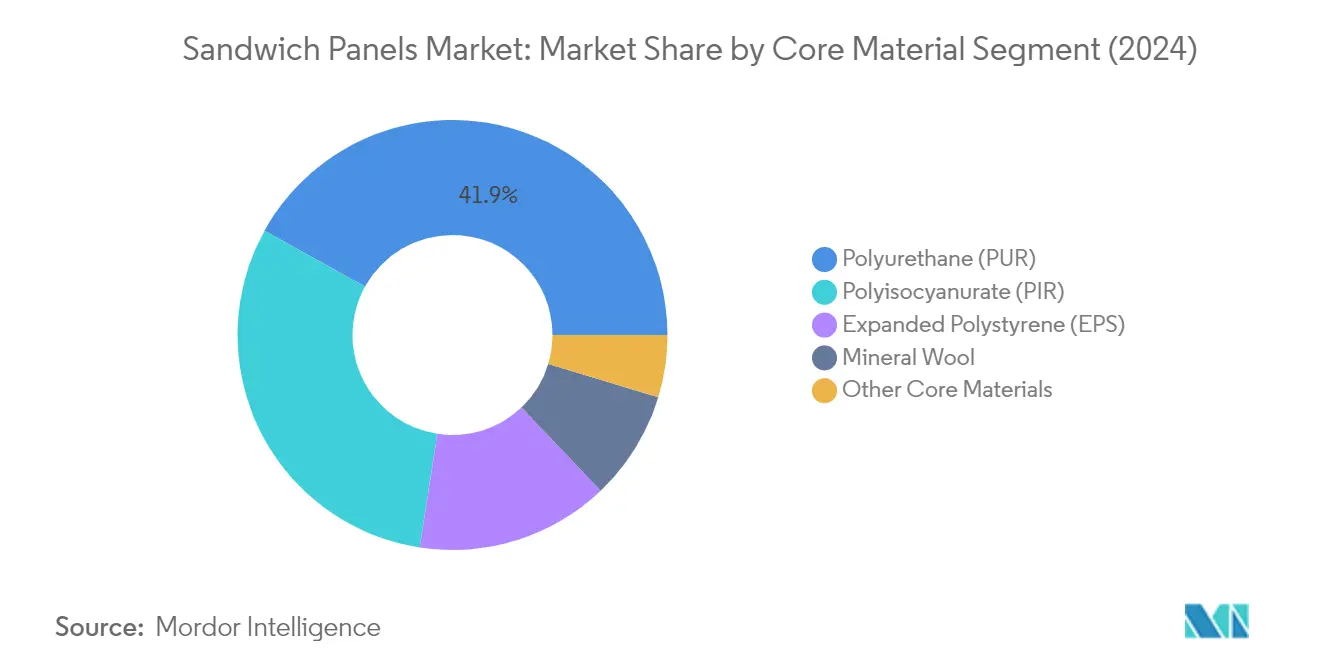

The Polyurethane (PUR) segment dominates the global sandwich panels market, commanding approximately 42% of the total market share in 2024, while also exhibiting the highest growth rate of around 6% for the forecast period 2024-2029. Polyurethane sandwich panels have gained significant traction due to their versatile advantages, including precise sizing and specification capabilities, easy deconstruction and relocation features, and superior thermal insulation properties. These panels are becoming increasingly popular in various applications due to their ability to be designed in advance with exact specifications, making them highly suitable for prefabricated construction projects. The material's excellent thermal insulation properties and durability have made it particularly attractive for industrial buildings, cold storage facilities, and commercial construction projects where energy efficiency is paramount. Additionally, PUR sandwich panels offer significant advantages in terms of weight reduction, installation efficiency, and long-term performance, contributing to their market leadership position.

Remaining Segments in Core Material Market

The sandwich panels market encompasses several other significant core materials, including Polyisocyanurate (PIR), Expanded Polystyrene (EPS), and Mineral Wool, each serving specific applications and requirements. PIR panels have gained prominence due to their enhanced fire resistance properties and superior thermal performance compared to traditional materials. EPS sandwich panels have established themselves as a cost-effective solution for various construction applications, particularly in regions where budget considerations are paramount. Mineral wool sandwich panels are preferred in applications requiring high fire resistance and acoustic insulation, especially in commercial and industrial buildings where safety regulations are stringent. Each of these materials contributes uniquely to the market, with their selection often depending on specific project requirements, local building codes, and environmental considerations.

Segment Analysis: Skin Material

Aluminum Segment in Sandwich Panels Market

Aluminum holds the dominant position in the sandwich panels market, commanding approximately 46% of the total market share in 2024. This significant market presence is attributed to aluminum's superior properties as a skin material, making it perfectly suited for appealing surface elements and sophisticated surface applications. The material's versatility allows its application in various sectors including interior and exterior architectural cladding, partitions, sign trays, false ceilings, individual logos, counter cladding, column cladding, screens and grilles, display panels, and machine parts covers. Aluminum sandwich panels offer remarkable advantages such as outstanding thermal comfort, improved sound dampening, long-lasting durability, low maintenance requirements, and excellent weather resistance. The lightweight nature of aluminum panels enables their use in large dimensions, achieving weight savings of up to 80% compared to solid aluminum of the same structural performance.

CFRT Segment in Sandwich Panels Market

Continuous Fiber Reinforced Thermoplastics (CFRT) represents the fastest-growing segment in the sandwich panels market, projected to expand at approximately 6% during 2024-2029. The exceptional growth trajectory is driven by CFRT's unique combination of properties including lightweight characteristics, ease of assembly, high strength, waterproof and moisture-proof capabilities, excellent chemical resistance, and high weather ability. These panels incorporate various resins such as PE, PP, PVC, PPS, PEEK, ABS, and PC-polycarbonate as skin materials, offering versatile solutions for different applications. The thermal properties of these fibers are particularly noteworthy, as they can be protected from oxidation above 1,000°Celsius and remain stable at 2000°Celsius. The growing adoption in high-rise buildings and skyscrapers, where lightweight and easy-to-install materials with aesthetic appeal are crucial, continues to drive the segment's growth.

Remaining Segments in Skin Material

The sandwich panels market features several other significant skin materials including Steel, Fiberglass Reinforced Panels (FRP), and other specialized materials. Steel skin materials contribute substantially to the market, offering advantages such as durability, dimensional stability, consistent manufacturing quality, and resistance to mold and pests. FRP panels have gained traction due to their scratch resistance, efficient cleaning capabilities, UV resistance, and high sanitation protection features. These materials are particularly valuable in specific applications such as kitchens, restrooms, dining rooms, offices, classrooms, hospital rooms, and recreational areas. The remaining specialized skin materials, though representing a smaller market share, continue to serve niche applications where specific material properties are required, contributing to the overall diversity and adaptability of sandwich panel solutions.

Segment Analysis: By Application

Wall Panels Segment in Sandwich Panels Market

Wall panels continue to dominate the global sandwich panels market, holding approximately 44% market share in 2024. The rising demand for a new kind of sandwich insulation composite wall structure has been driving this segment's growth, as these panels retain and carry forward the existing advantages of traditional sandwich insulation composite walls. Wall panels offer superior mechanical performance and seismic resistance while providing continuous insulation layers that can be modified according to specific requirements. The outer layers of wall panels can incorporate various decorative function blocks, especially high-strength and high-density decorative blocks, meeting demanding outdoor durability requirements. Additionally, these panels serve dual purposes - not only providing decorative elements but also ensuring durability of the load-bearing structure while eliminating or reducing masonry cracks.

Insulated Panels Segment in Sandwich Panels Market

The insulated panels segment is projected to witness the fastest growth rate of approximately 6% during the forecast period 2024-2029. The growth is primarily attributed to the increasing demand for temperature-controlled environments across various industries. These panels are extensively utilized in freezers, clean rooms, cool rooms, portable buildings, food production facilities, and cost-effective partitions. The segment's growth is further supported by the panels' long-term R-value, chemical inertness, energy efficiency, anti-bacterial properties, dimensional stability, high thermal resistance, and measurable energy savings. Additionally, rigid polyurethane (PUR) and polyisocyanurate (PIR) foam sandwiched between metal or flexible facings are becoming increasingly successful in meeting the construction industry's requirements, particularly in applications like cold storage warehouses, medical buildings, airports, and various manufacturing facilities.

Remaining Segments in Sandwich Panels Market by Application

The roof panels and other applications segments complete the market landscape for sandwich panels. Roof panels serve as crucial components in building construction, offering superior insulation and load-bearing capabilities for various structures. These panels are specifically designed to withstand strong storms while providing fire and heat resistance. The other applications segment encompasses interior decoration, cladding, and flooring applications, where sandwich panels are utilized for their versatility and aesthetic appeal. These panels find extensive use in creating elegant, water-resistant, stain-resistant, and durable furniture, bookshelves, and wardrobes, while also serving practical purposes in bathrooms, kitchens, kiosks, ceilings, doors, walls, and partitions.

Segment Analysis: End-Use Sector

Industrial Segment in Sandwich Panels Market

The industrial sector maintains its dominant position in the global sandwich panels market, commanding approximately 44% of the total market revenue in 2024. This significant market share is primarily driven by the rising diversification and ranges in the construction of industrial buildings using insulated roof and wall panels. The sector's prominence is further reinforced by the increasing demand from cold storage buildings and warehouses, particularly due to the rapid expansion of food retail chains by multinational companies. The industrial segment is also projected to witness the fastest growth rate of around 6% during 2024-2029, driven by substantial investments in new manufacturing facilities, logistics centers, and cold storage units globally. The growth is particularly notable in emerging economies where there is a surge in industrial infrastructure development and modernization of existing facilities to meet energy efficiency standards.

Remaining Segments in End-Use Sector

The commercial, residential, and institutional segments collectively form a significant portion of the sandwich panels market, each serving distinct construction needs. The commercial sector represents the second-largest segment, driven by the increasing adoption of sandwich panels in showrooms, hypermarkets, shopping malls, hotels, and office buildings, particularly due to their superior thermal insulation properties and aesthetic appeal. The residential sector continues to grow steadily with the rising awareness of energy-efficient building materials and the increasing implementation of sustainable construction practices. The institutional and infrastructure segment has gained considerable traction due to extensive government investments in public infrastructure, educational facilities, healthcare centers, and other institutional buildings, where sandwich panels are preferred for their durability and cost-effectiveness.

Sandwich Panels Market Geography Segment Analysis

Sandwich Panels Market in Asia-Pacific

The Asia-Pacific region represents a dominant force in the global sandwich panels market, driven by rapid industrialization and extensive construction activities across major economies. China leads the regional sandwich panels market, followed by significant contributions from Japan, India, and South Korea. The region's growth is primarily attributed to increasing investments in industrial buildings, warehouses, cold storage facilities, and infrastructure development projects. Government initiatives promoting energy-efficient construction and sustainable building practices have further accelerated market expansion across these countries.

Sandwich Panels Market in China

China dominates the Asia-Pacific sandwich panels market through its massive construction sector and ambitious infrastructure development plans. The country holds approximately 64% share of the regional market, driven by its focus on sustainable urban development and energy-efficient building solutions. The construction sector remains a key contributor to China's continued economic development, with significant investments in new infrastructure projects. The country's 14th Five-Year Plan emphasizes new infrastructure development in energy, transportation, water systems, and urbanization, while also focusing on making the construction sector more sustainable and quality-driven.

Sandwich Panels Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's construction sector is witnessing substantial growth driven by various government initiatives such as Smart Cities projects and Housing for All. The availability of affordable housing is expected to rise significantly, supported by increased government spending in the real estate market. India's huge construction sector is positioned to become the world's third-largest construction market, creating substantial opportunities for sandwich panel applications in both residential and commercial segments.

Sandwich Panels Market in North America

The North American sandwich panels market demonstrates strong growth potential, supported by robust construction activities and increasing focus on energy-efficient building solutions across the United States, Canada, and Mexico. The region's market is characterized by significant investments in commercial, industrial, and residential construction projects. The adoption of advanced building panels and stringent energy efficiency regulations continues to drive the demand for sandwich panels across these countries.

Sandwich Panels Market in United States

The United States maintains its position as the largest market in North America, commanding approximately 82% of the regional market share. The country's construction sector remains one of the major economic sectors, with significant investments in both residential and commercial projects. The implementation of stringent energy efficiency regulations, including the International Energy Conservation Code (IECC) and American Society of Heating, Refrigerating, and Air Conditioning Engineers standards, has further boosted the demand for insulated panels in building applications.

Sandwich Panels Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected growth rate of approximately 5% during 2024-2029. The country's construction sector is experiencing steady growth, particularly in residential and commercial construction activities. The Canadian Construction Association's initiatives and various government projects, such as the New Building Canada Plan and Affordable Housing Initiative, continue to support the sector's growth, creating sustained demand for construction panels across various applications.

Sandwich Panels Market in Europe

The European sandwich panels market showcases strong growth potential, supported by increasing focus on energy-efficient construction and renovation activities across Germany, United Kingdom, Italy, and France. The region's market is driven by stringent building energy efficiency regulations and various sustainability initiatives. The construction sector across these countries continues to adopt advanced building panels and technologies, creating sustained demand for sandwich panels.

Sandwich Panels Market in United Kingdom

The United Kingdom leads the European sandwich panels market, driven by its strong construction sector and world-class expertise in design, architecture, and engineering. The country's focus on sustainable construction solutions and significant investments in infrastructure development projects continues to drive market growth. The government's commitment to improving building energy efficiency and various construction projects, including high-rise buildings and commercial developments, maintains steady demand for insulated panels.

Sandwich Panels Market in Italy

Italy demonstrates the highest growth potential in the European region, supported by its National Recovery and Resilience Plan and significant investments in construction activities. The country's focus on improving commercial infrastructure and civil engineering activities, combined with changes in government policies for foreign direct investments and tax deductions, drives the construction industry growth. The launch of various infrastructure development projects and renovation initiatives continues to create substantial opportunities for sandwich panel applications.

Sandwich Panels Market in South America

The South American sandwich panels market, primarily driven by Brazil and Argentina, shows promising growth potential despite economic challenges in the region. Brazil emerges as both the largest and fastest-growing market in the region, supported by various government initiatives and infrastructure development projects. The Brazilian government's massive privatization initiative through a pipeline of concession auctions and regulatory reforms aims at attracting financing to assist in closing Latin America's largest infrastructure funding gap. Argentina's market growth is supported by public-private partnership project investments and increasing demand from the food processing industry.

Sandwich Panels Market in Middle East & Africa

The Middle East & Africa region demonstrates significant growth potential in the sandwich panels market, driven by extensive construction activities and infrastructure development projects across Saudi Arabia and South Africa. Saudi Arabia emerges as both the largest and fastest-growing market in the region, supported by its Vision 2030 initiative and various mega-construction projects. South Africa's market is driven by the National Infrastructure Plan 2050 and increasing investments in commercial and industrial construction projects. The region's focus on developing energy-efficient buildings and sustainable construction practices continues to drive the demand for sandwich panels across various applications.

Get Analysis on Important Geographic Markets

Download PDF

Sandwich Panel Industry Overview

Top Companies in Sandwich Panels Market

The global sandwich panels market features prominent players like Kingspan Group, ArcelorMittal, Tata Steel, Rautaruukki Corporation, and Romakowski GmbH & Co. KG leading the industry through continuous innovation and strategic expansion. Companies are focusing on developing energy-efficient and sustainable panel solutions, particularly targeting the growing demand for green building materials and cold storage applications. The industry witnesses regular product launches featuring advanced insulation technologies, fire-resistant properties, and improved aesthetic options. Operational excellence is being achieved through vertical integration strategies, with many leaders maintaining control over raw material supply chains while also providing installation and maintenance services. Strategic moves in the sector predominantly involve geographical expansion through acquisitions and partnerships, particularly in emerging markets, while research and development investments are directed towards bio-based materials and enhanced thermal performance solutions.

Fragmented Market with Regional Leadership Dynamics

The sandwich panels market exhibits a highly fragmented structure with no single player commanding a dominant global market share, though certain companies maintain strong regional leadership positions. The competitive landscape is characterized by a mix of large multinational conglomerates like ArcelorMittal and Tata Steel, who leverage their integrated steel manufacturing capabilities, alongside specialized manufacturers like Kingspan Group who focus exclusively on building envelope solutions. The market features numerous local and regional players who compete effectively in their respective territories through customized solutions and strong distribution networks.

The industry has been witnessing strategic consolidation through mergers and acquisitions, particularly in Europe and North America, as companies seek to expand their geographical presence and technological capabilities. Forward integration is a notable trend, with manufacturers increasingly offering comprehensive solutions including design, installation, and after-sales services. Market leaders are strengthening their positions through acquisitions of regional players, particularly those with specialized technological expertise or strong market presence in high-growth regions. The competitive dynamics are further shaped by the presence of vertically integrated steel manufacturers who have expanded into construction panels production to capture additional value in the construction materials supply chain.

Innovation and Service Excellence Drive Success

Success in the sandwich panels market increasingly depends on companies' ability to offer comprehensive solutions that combine product innovation with superior service delivery. Market leaders are strengthening their positions by developing proprietary technologies, particularly in areas of thermal efficiency and fire resistance, while also expanding their service offerings to include technical support and installation expertise. The ability to provide customized solutions for specific end-user requirements, particularly in commercial and industrial applications, has become a crucial differentiator. Companies are also focusing on developing sustainable products and obtaining relevant certifications to address growing environmental concerns and regulatory requirements.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products or focusing on specific geographical regions where they can build strong customer relationships and efficient distribution networks. The increasing importance of energy efficiency in construction creates opportunities for companies that can develop innovative insulated panel solutions. Market participants must also consider the growing influence of architects and consultants in product specification, making strong relationships with these stakeholders crucial for success. Additionally, companies need to maintain flexibility in their manufacturing processes to accommodate varying customer requirements while ensuring competitive pricing through operational efficiency.

Sandwich Panel Market Leaders

-

Tata Steel

-

Rautaruukki Corporation

-

ArcelorMittal

-

ITALPANNELLI SRL

-

ArcelorMittal

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Sandwich Panel Market News

- October 2022: Kingspan acquired Invespane, a mineral wool-based sandwich panel producer. The strategic acquisition of Invespanel into Kingspan will create an opportunity to complement their product offerings in sandwich panels for different applications.

- November 2021: Industrial Engineering Company for Construction and Development (ICON) received an offer from Kingspan Insulated Panels seeking a collaboration in manufacturing sandwich panels.

- September 2021: L&L Products launched a new FST aircraft interior edge and core filler compound. L&L Reinforce L-9060 brings a new approach to fill and reinforce aerospace interior sandwich panels by providing a solution to improve the traditional manual process of other two-component honeycomb panel reinforcements.

Sandwich Panel Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Cold Storage Applications of Structural Insulated Panels

- 4.1.2 Increasing Demand for PVDF-based Aluminum Composite Panels

-

4.2 Restraints

- 4.2.1 Fire Performance of Some Sandwich Panels

- 4.2.2 Oriented Stranded Board (OSB) Emissions of Volatile Organic Compounds (VOCs)

- 4.3 Industry Value-Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size by Value)

-

5.1 Core Material

- 5.1.1 Polyurethane (PUR)

- 5.1.2 Polyisocyanurate (PIR)

- 5.1.3 Mineral Wool

- 5.1.4 Expanded Polystyrene (EPS)

- 5.1.5 Other Core Materials

-

5.2 Skin Material

- 5.2.1 Continuous Fiber Reinforced Thermoplastics (CFRT)

- 5.2.2 Fiberglass Reinforced Panel (FRP)

- 5.2.3 Aluminum

- 5.2.4 Steel

- 5.2.5 Other Skin Materials

-

5.3 Application

- 5.3.1 Wall Panels

- 5.3.2 Roof Panels

- 5.3.3 Insulated Panels

- 5.3.4 Other Applications

-

5.4 End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Institutional and Infrastructure

-

5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 ArcelorMittal

- 6.4.2 Areco

- 6.4.3 Assan Panel A.Ş.

- 6.4.4 Building Components Solutions LLC

- 6.4.5 Cornerstone Building Brands

- 6.4.6 DANA Group of Companies

- 6.4.7 ITALPANNELLI SRL

- 6.4.8 Kingspan Group

- 6.4.9 Multicolor Steels (India) Pvt Ltd

- 6.4.10 Rautaruukki Corporation

- 6.4.11 Safal group

- 6.4.12 Sintex

- 6.4.13 Tata Steel

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Construction of Industrial and Commercial Buildings

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Sandwich Panel Industry Segmentation

A sandwich panel consists of a core/insulating material of low density sandwiched between two layers of metal bonded under pressure. The sandwich panels market is segmented by core material, skin material, application, end-use sector, and geography. By core material, the market is segmented into polyurethane, polyisocyanurate, mineral wool, expanded polystyrene, and other core materials. The market is segmented by skin material: continuous fiber-reinforced thermoplastics, fiberglass-reinforced panels, aluminum, steel, and other skin materials. By application, the market is segmented into wall panels, roof panels, insulated panels, and other applications. The end-use sector segments the market into residential, commercial, industrial, institutional, and infrastructure. The report also covers the market size and forecasts for the structural insulated panels market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD million).

| Core Material | Polyurethane (PUR) | ||

| Polyisocyanurate (PIR) | |||

| Mineral Wool | |||

| Expanded Polystyrene (EPS) | |||

| Other Core Materials | |||

| Skin Material | Continuous Fiber Reinforced Thermoplastics (CFRT) | ||

| Fiberglass Reinforced Panel (FRP) | |||

| Aluminum | |||

| Steel | |||

| Other Skin Materials | |||

| Application | Wall Panels | ||

| Roof Panels | |||

| Insulated Panels | |||

| Other Applications | |||

| End-use Sector | Residential | ||

| Commercial | |||

| Industrial | |||

| Institutional and Infrastructure | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Qatar | |||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Sandwich Panel Market Research FAQs

What is the current Sandwich Panels Market size?

The Sandwich Panels Market is projected to register a CAGR of greater than 6% during the forecast period (2025-2030)

Who are the key players in Sandwich Panels Market?

Tata Steel, Rautaruukki Corporation, ArcelorMittal, ITALPANNELLI SRL and ArcelorMittal are the major companies operating in the Sandwich Panels Market.

Which is the fastest growing region in Sandwich Panels Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Sandwich Panels Market?

In 2025, the Asia Pacific accounts for the largest market share in Sandwich Panels Market.

What years does this Sandwich Panels Market cover?

The report covers the Sandwich Panels Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Sandwich Panels Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Sandwich Panels Market Research

Mordor Intelligence provides a comprehensive analysis of the sandwich panels industry, drawing on decades of expertise in construction materials research. Our latest report explores the full range of panel technologies. This includes structural insulated panels, SIP panels, and various composite solutions such as EPS sandwich panels, rockwool sandwich panels, mineral wool sandwich panels, polyurethane sandwich panels, and foam sandwich panels. The analysis offers detailed insights into metal sandwich panels, honeycomb panels, and composite panels. It provides stakeholders with crucial data on market dynamics and growth trajectories.

The report, available in an easy-to-download PDF format, delivers valuable insights for stakeholders across various applications. These include cleanroom panels, cold storage panels, industrial panels, and architectural panels. Our research thoroughly examines wall panel systems and roof panel systems. It also analyzes trends in prefabricated panel construction and building panels implementation. The comprehensive coverage extends to insulated metal panels applications and emerging opportunities in construction panels. This enables businesses to make informed decisions based on robust market analysis and future growth projections in the insulated panel industry.