Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

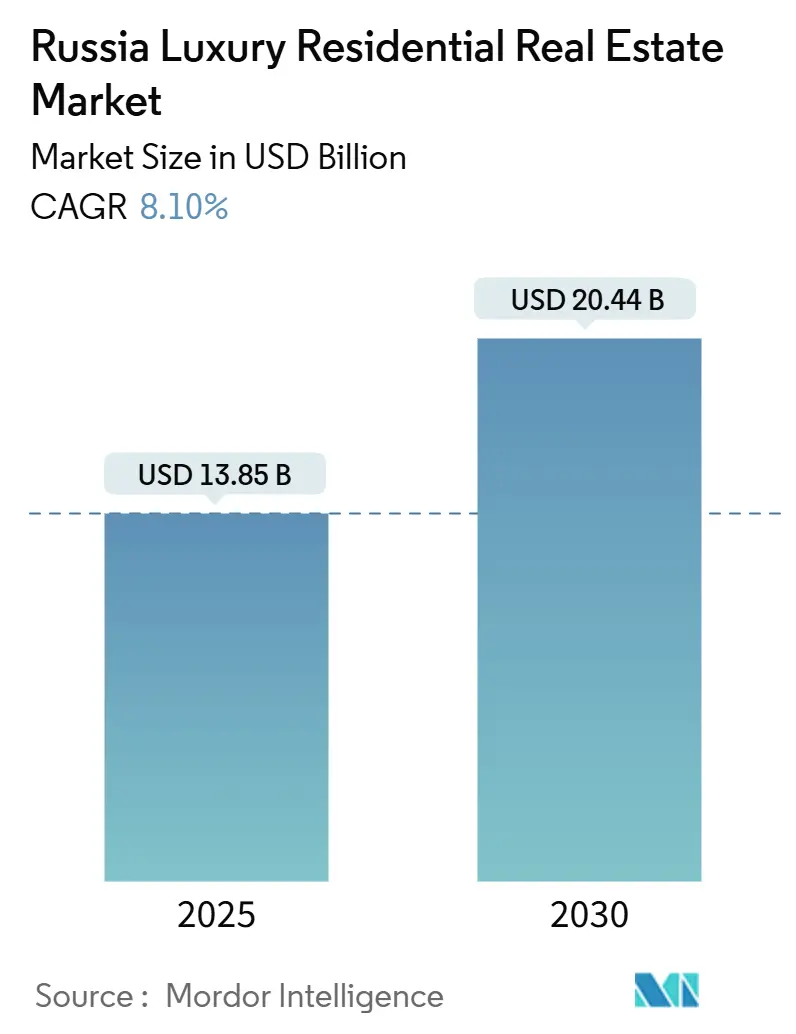

| Market Size (2025) | USD 13.85 Billion |

| Market Size (2030) | USD 20.44 Billion |

| Growth Rate (2025 - 2030) | 8.10% CAGR |

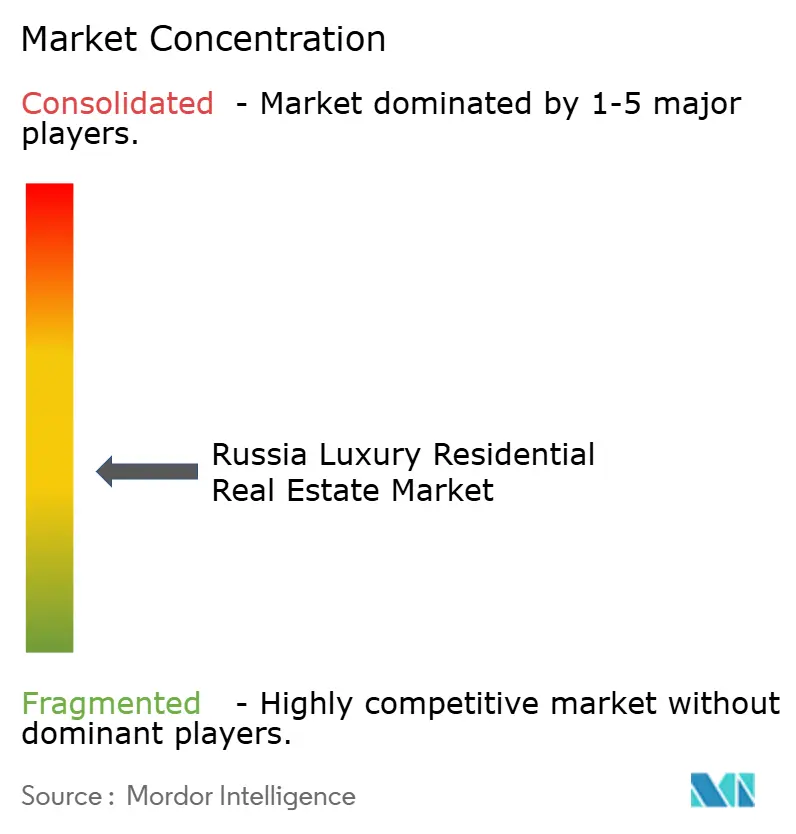

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Russia Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Russia Luxury Residential Real Estate Market size is estimated at USD 13.85 billion in 2025, and is expected to reach USD 20.44 billion by 2030, at a CAGR of 8.10% during the forecast period (2025-2030). The sector’s durability, even under sanctions and tighter monetary policy, highlights how domestic wealth concentration, currency volatility, and elite migration keep transaction volumes elevated. Market momentum rests on cash-rich households reallocating capital from overseas options toward domestic hard assets, while energy-efficient design and smart-home technology lift premiums in top-tier developments. Although the July 2024 expiry of the state mortgage-subsidy program trimmed mainstream demand, luxury segments remain buoyed by buyers who seldom rely on bank financing. Overall, the Russia luxury residential real estate market continues to benefit from ruble hedging dynamics, residence-permit inflows from neutral jurisdictions, and a growing preference for turnkey concierge living near Moscow’s business corridors.

Key Report Takeaways

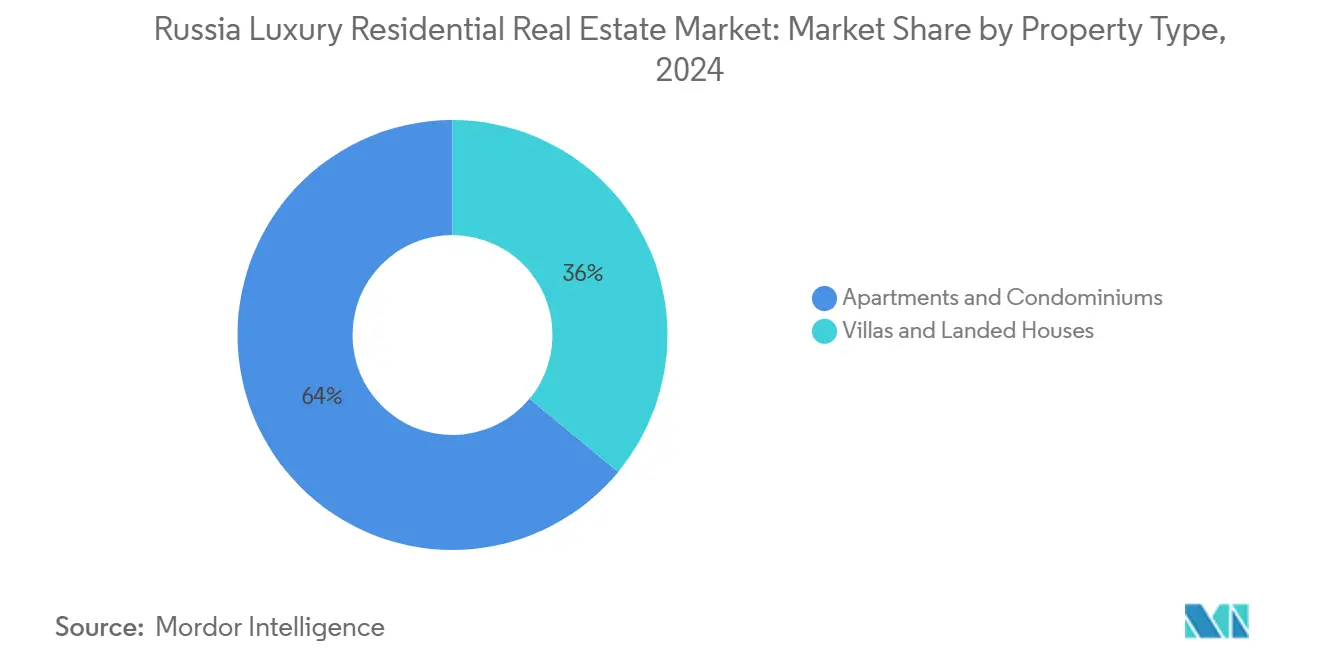

- By property type, apartments and condominiums held 64% of the Russia luxury residential real estate market size in 2024, whereas villas and landed houses are set to expand at an 8.52% CAGR through 2030.

- By business model, sales transactions controlled 71% of the Russia luxury residential real estate market in 2024, while rental income streams are rising at a 9.27% CAGR to 2030.

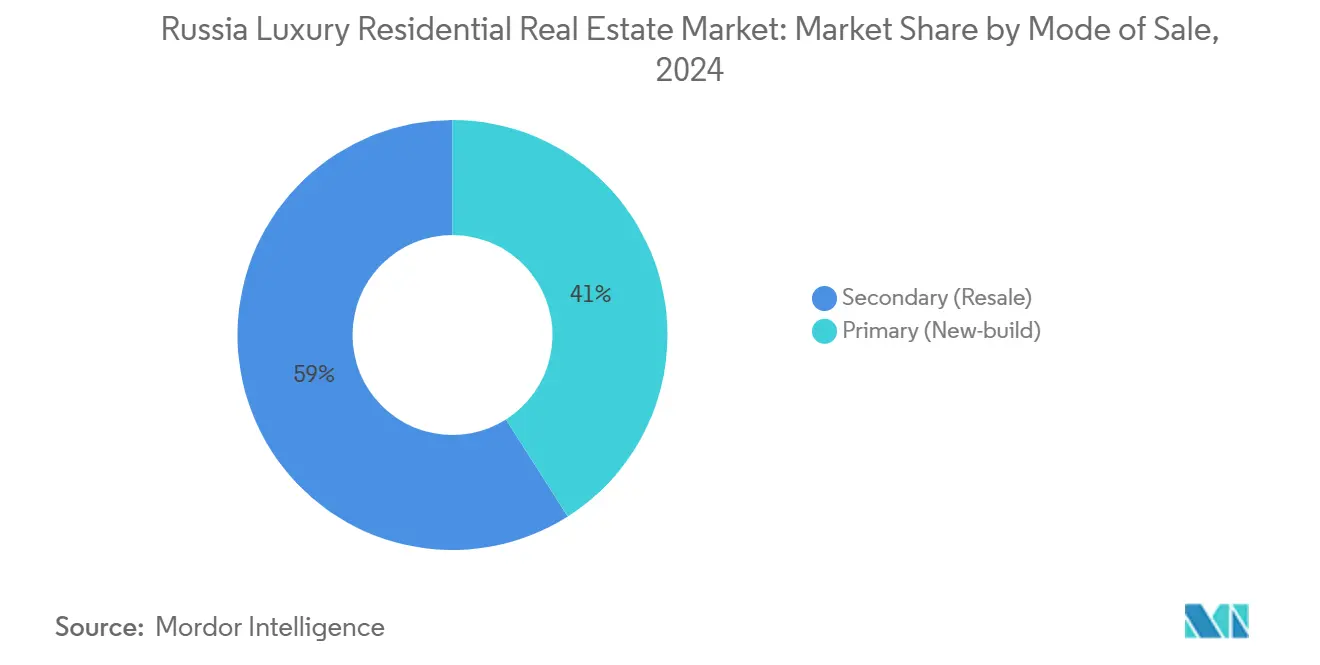

- By mode of sale, secondary transactions accounted for a 59% share of the Russia luxury residential real estate market size in 2024; primary new-build assets are advancing at an 8.74% CAGR.

- By city, Moscow led with 46% Russia luxury residential real estate market share in 2024; Kazan is projected to grow at a 9.56% CAGR to 2030.

Russia Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ruble depreciation driving hard-asset allocation | +1.8% | National, with stronger impact in major cities | Short term (≤ 2 years) |

| Domestic wealth concentration amid capital controls | +1.6% | Moscow & St. Petersburg core; spillover to regional centers | Medium term (2-4 years) |

| Regional luxury demand from elite migration | +1.2% | Secondary cities such as Kazan, Sochi, Yekaterinburg | Medium term (2-4 years) |

| Energy-efficient luxury developments commanding premiums | +1.0% | Large metropolitan areas with green-conscious clientele | Long term (≥ 4 years) |

| Residence-permit programs attracting foreign investment | +0.8% | Moscow & St. Petersburg primarily | Long term (≥ 4 years) |

| Tech-sector growth in Moscow boosting prime demand | +0.5% | Moscow IT districts and adjacent zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Domestic Wealth Concentration Amid Capital Controls

Russia’s 2022 capital-control regime sharply limited overseas transfers, compelling affluent households to recycle funds domestically. As traditional foreign holdings became harder to acquire, prime apartments in Moscow and St. Petersburg emerged as favored stores of value. Several family-office surveys confirm an uptick in Russian allocations to high-end domestic housing, widening demand for concierge-serviced towers and gated villa communities. The trend radiates toward regional hubs where elite buyers seek portfolio diversification without leaving the country. High entry tickets and scarce land keep prices resilient, supporting the Russia luxury residential real estate market even during macro headwinds[1]Mikhail Krutikhin, “Capital Controls and Domestic Asset Allocation in Russia,” Journal of Economic Geography, academic.oup.com.

Ruble Depreciation Driving Hard-Asset Allocation Preferences

Intense currency swings through 2024 sharpened the appeal of brick-and-mortar assets. High-net-worth individuals (HNWIs) accelerated purchases of luxury homes to hedge against ruble weakness, viewing real estate as a quasi-foreign-currency proxy with tangible collateral. Prime Moscow addresses, quoted in USD benchmarks, thus attracted investors keen on wealth preservation. The hedging motive also widened lot-size preferences, prompting buyers to favor larger floor plans suitable for combined residence and investment objectives. Elevated interest rates had little deterrent effect because most luxury deals remain all-cash.

Regional Luxury Demand From Moscow & St. Petersburg Elite Migration

Lifestyle shifts and traffic congestion have nudged a share of Russia’s wealthiest households toward quieter secondary cities. Kazan benefits most, registering the fastest growth due to its technology parks and lower cost base. Meanwhile, Sochi and Yekaterinburg lure entrepreneurs seeking diversified holdings and recreational amenities. These inflows place upward pressure on limited luxury stock, encouraging developers to introduce international-standard design in previously untapped districts. Such geographic dispersion anchors future upside for the Russia luxury residential real estate market.

Residence-Permit Programs Attracting Foreign Investment

Despite Western sanctions, residence-by-investment pathways continue to pull buyers from Central Asia, the Middle East, and selected Asian economies. The legal minimum spend thresholds sit naturally within the luxury bracket, channeling inbound capital toward high-spec apartments in Moscow City and St. Petersburg’s historic waterfronts. These acquisitions tend to stay off the rental market, reducing effective supply and cushioning prices. Transaction volumes remain modest yet critical as incremental demand that offsets sanction-triggered shortfalls from Europe and North America.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| International sanctions limiting foreign buyer participation | -1.0% | Moscow & St. Petersburg international districts | Short term (≤ 2 years) |

| Construction material cost inflation from import restrictions | -0.7% | National; acute in new-builds | Medium term (2-4 years) |

| Limited luxury land availability in core Moscow & St. Petersburg | -0.6% | Prime metropolitan areas with zoning ceilings | Long term (≥ 4 years) |

| Regulatory uncertainty affecting cross-border deals | -0.4% | International corridors and border regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

International Sanctions Limiting Foreign Buyer Participation

Tight banking curbs and payment-system blocks deter many Western buyers who once formed a sizeable slice of demand in Moscow’s embassy quarters. Brokers now target domestic purchasers and investors from sanction-neutral nations, but transaction lead times lengthen as compliance checks intensify. Developers previously marketing to expatriate executives must recalibrate unit layouts and branding for Russian HNWIs, compressing absorption speeds and raising marketing costs. The net effect subtracts roughly 1% from the projected CAGR yet does not derail long-term prospects given robust domestic liquidity.

Construction Material Cost Inflation From Import Restrictions

High-spec marble, Swiss elevators, and German HVAC systems have become harder to source since 2023, forcing developers to find costlier substitutes or redesign interiors. Material inflation clips margins on ongoing projects and raises presale prices on future launches. Secondary resale stock thus gains a relative edge, shifting some demand from primary to secondary segments. While developers pursue bulk-buy alliances and local vertical integration, elevated input costs still shave an estimated 0.7 percentage points off growth.

Segment Analysis

By Property Type: Apartments Maintain Scale While Villas Accelerate

Apartments and condominiums captured 64% of the Russia luxury residential real estate market in 2024. Dense urban cores, established concierge management, and proximity to Grade-A offices keep multi-family formats dominant. Leading examples include Moscow’s OKO Tower and St. Petersburg’s Club House projects that offer biometric access, spa suites, and direct metro links. Investors favor these units for predictable rental yields and liquidity, reinforcing depth in the secondary apartment marketplace[2]Olga Turina, “Housing Stock and New-Build Completions 2024,” Federal State Statistics Service (Rosstat), rosstat.gov.ru.

Growth, however, tilts toward villas and landed houses at an 8.52% CAGR, propelled by buyers seeking privacy and larger plots for wellness amenities. Gated communities in Rublyovka and suburban Kazan now bundle geothermal systems and electric-vehicle charging, commanding premiums over city-centre apartments. Developers such as PIK Group unlock additional margin by positioning villas as estate-style campuses with on-site schools and medical clinics. Consequently, the segment’s outperformance enlarges its revenue contribution to the wider Russia luxury residential real estate market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Business Model: Sales Still Rule, Rentals Gather Pace

Sales transactions represented 71% of Russia luxury residential real estate market activity in 2024, consistent with domestic culture valuing outright ownership for wealth security. HNWIs typically acquire in cash, side-stepping double-digit mortgage rates. LSR Group’s recent sell-out of a USD 550 million Moscow mid-rise exemplifies this upfront-payment trend. Rapid closing cycles allow developers to reinvest quickly, preserving the sales model’s primacy.

Rental formats, though smaller, are expanding at a 9.27% CAGR. Institutional landlords convert entire floors of prime towers into serviced residences for corporate tenants in tech and finance. Gross yields of 5%–6% surpass local bond returns, attracting capital from family offices. As a result, professionally managed rental stock becomes a meaningful supplement to the Russia luxury residential real estate market, balancing owner-occupier dominance with income-centric plays.

By Mode of Sale: Secondary Stock Prevails While Primary Stock Innovates

Secondary resales accounted for 59% of the Russia luxury residential real estate market size in 2024, underscoring buyer preference for immediate handover and established neighborhoods. Units built during the 2014–2020 boom now circulate actively, often refreshed with smart-home retrofits to match new-build standards. Brokers highlight proven service charges, which reduce perceived risk for conservative investors.

Conversely, primary new-build supply is scaling at an 8.74% CAGR on the back of eco-label certification and integrated digital concierge platforms. Etalon Group’s flagship “Smart-Eco Residence” in St. Petersburg achieved 85% presales within six months by guaranteeing 30% energy savings and 24-hour telemedicine access. Although build-cost inflation squeezes margins, differentiated smart-green propositions sustain end-user appetite, raising the innovation bar across the Russia luxury residential real estate market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Moscow continues to serve as the epicentre of high-end residential demand, benefitting from its 46% share of the Russia luxury residential real estate market in 2024. The capital’s dominance draws on an agglomeration of elite schools, Michelin-level dining, and Grade-A office density that keeps executives anchored near core districts. Cash buyers sidestep the Central Bank’s 2024 rate hikes, ensuring steady take-up of penthouses in complexes such as Neva Towers. Energy-efficient retrofits, including façade insulation and smart ventilation, command 10% price premiums, reinforcing sustainability as a price driver[3]Sergey Sobyanin, “Moscow Real-Estate Market Dashboard 2025,” Moscow City Analytical Center, mos.ru.

St. Petersburg stands out for cultural prestige, maritime trade, and burgeoning fintech clusters. Its historic waterfront conversions, notably at the English Embankment, attract financiers and creatives who prize UNESCO-listed architecture paired with modern interiors. Secondary residences purchased by Moscow elites add depth to transaction volumes, while seasonal tourists underpin robust short-term rental yields. The city benefits from relatively milder regulatory constraints on adaptive reuse, streamlining luxury refurbishments in heritage assets.

Kazan’s trajectory underscores a decentralization narrative, recording a 9.56% forecast CAGR as young millionaires in e-commerce and software seek upscale housing with lower congestion. Government investment in smart-city services, 5G coverage, and international schools cements its attractiveness. Meanwhile, Sochi, Yekaterinburg, and Novosibirsk capture lifestyle-driven relocations, each leveraging niche strengths ranging from winter sports to aerospace supply chains. Collectively, these emerging nodes diversify the Russia luxury residential real estate market, cushioning it from single-city shocks and embedding a multi-polar growth map.

Competitive Landscape

The Russia luxury residential real estate market exhibits moderate fragmentation, with the top five developers together controlling roughly 45% of completed unit deliveries. PIK Group and LSR Group concentrate on ultra-prime land banking in Moscow’s Third Ring Road, fortifying barriers to entry. Land scarcity amplifies first-mover advantage, enabling incumbents to dictate project phasing and pre-launch pricing. Etalon Group and SETL Group differentiate through in-house modular construction that trims build times by up to four months, partially offsetting material inflation.

Strategic alliances between developers and domestic tech firms are proliferating. PIK Group’s partnership with Yandex integrates voice-activated concierge systems, while LSR Group collaborates with SberDevices for AI-driven energy management. Such tie-ups generate data-enabled services that amplify customer stickiness and justify higher service fees. Simultaneously, vertical integration into prefabricated façade plants spreads overhead across multiple projects, guarding margins in a high-cost import environment.

Regional expansion defines the third competitive vector. Etalon Group’s entry into Kazan and Sochi pairs local contractors with Moscow-grade design consultants, delivering premium product in markets that lack established luxury benchmarks. These moves pre-empt rivals and lock in early adopter market share. International brokers like Knight Frank Russia and Sotheby’s International Realty Russia focus on bespoke mandates for ultra-high-net-worth families, leveraging global referral channels despite sanctions on Western counterparts. Collectively, these strategies intensify rivalry yet lift product quality and professionalism within the broader Russia luxury residential real estate market.

Russia Luxury Residential Real Estate Industry Leaders

-

LSR Group

-

PIK Group

-

Etalon Group

-

Ingrad

-

SETL Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Etalon Group opened a regional design studio in Kazan to tailor smart-home packages and sustainability features for upcoming luxury towers. The hub accelerates presales on the 700-unit Smart-Eco Residence and spearheads the company’s expansion into high-growth regional markets.

- March 2025: LSR Group closed a ruble-denominated green bond that was 2.4× oversubscribed, channeling proceeds into a 62-story LEED-Platinum tower in the Moscow International Business Center. The issue locks in sub-market financing costs and signals robust domestic demand for sustainably certified prime assets.

- January 2025: PIK Group committed USD 140 million for a 120-villa enclave on Novorizhskoye Highway that blends geothermal grids, biometric access, and EV-ready garages. Groundbreaking is set for Q3 2025, with handover in Q4 2026, strengthening the developer’s low-density eco-luxury pipeline.

- December 2024: The Central Bank lifted its key rate past 17%, sending conventional mortgage costs sharply higher and sidelining leverage-dependent buyers. Cash-rich purchasers in the luxury tier stayed active, widening the performance gap between prime and mainstream housing.

Russia Luxury Residential Real Estate Market Report Scope

Luxury residential real estate is defined differently across different areas, as property values, median resident income, and area development vary widely depending on the metro area. The Russian luxury residential real estate market is segmented by Type (Apartments and Condominiums and Villas and Landed Houses) and City (Moscow, St. Petersburg, Novosibirsk, and Other Cities). The report offers market size and forecasts for the Russian luxury homes market in value (USD Billion) for all the above segments.

By Property Type

| Apartments & Condominiums |

| Villas & Landed Houses |

By Business Model

| Sales |

| Rental |

By Mode of Sale

| Primary (New-build) |

| Secondary (Resale) |

By City

| Moscow |

| St. Petersburg |

| Kazan |

| Other Cities |

| By Property Type | Apartments & Condominiums |

| Villas & Landed Houses | |

| By Business Model | Sales |

| Rental | |

| By Mode of Sale | Primary (New-build) |

| Secondary (Resale) | |

| By City | Moscow |

| St. Petersburg | |

| Kazan | |

| Other Cities |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Russia luxury residential real estate market?

The market is valued at USD 13.85 billion in 2025 and is projected to expand to USD 20.44 billion by 2030.

Which city dominates luxury home sales in Russia?

Moscow dominates with a 46% share of the Russia luxury residential real estate market in 2024.

What property type is most popular among high-net-worth buyers?

Apartments and condominiums hold 64% of luxury transactions, thanks to their central locations and concierge amenities.

How fast is the villa segment growing?

Villas and landed houses are forecast to grow at an 8.52% CAGR through 2030, outpacing multifamily formats.

Why are rentals gaining ground in the luxury segment?

Institutional investors and family offices are targeting prime units for yields of 5%–6%, boosting rental activity at a 9.27% CAGR.

What are the main restraints affecting the market’s growth?

International sanctions, rising construction costs, and limited prime land supply collectively temper growth by roughly 2.7 percentage points over the forecast horizon.

Page last updated on: