Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 6.57 Billion |

| Market Size (2031) | USD 7.39 Billion |

| Growth Rate (2026 - 2031) | 2.37% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Home Furniture Market Analysis by Mordor Intelligence

The Russia Home Furniture Market size is estimated at USD 6.57 billion in 2026, and is expected to reach USD 7.39 billion by 2031, at a CAGR of 2.37% during the forecast period (2026-2031).

Capacity growth clustered in the Volga and Central Federal Districts, where state support for wood-panel clusters catalyzed integrated supply chains and lifted particleboard production to 13.9 million cubic meters in 2024, building a stronger base for case-goods manufacturing. Macroeconomic volatility moderated the headline growth path, as the economy contracted by nearly 10% in the third quarter of 2025 while the key rate peaked at 21%, which tightened mortgages and slowed discretionary fit-outs linked to new home purchases. Distribution continued to shift online as marketplaces scaled next-day oversized-goods delivery and augmented reality visualization, creating faster conversion funnels in a market that lacked a strong legacy of big-box furniture retail. Meanwhile, logistics delays on eastern rail corridors and ruble swings raised input-cost uncertainty for fittings and specialty materials that remain import-dependent for many categories.

Key Report Takeaways

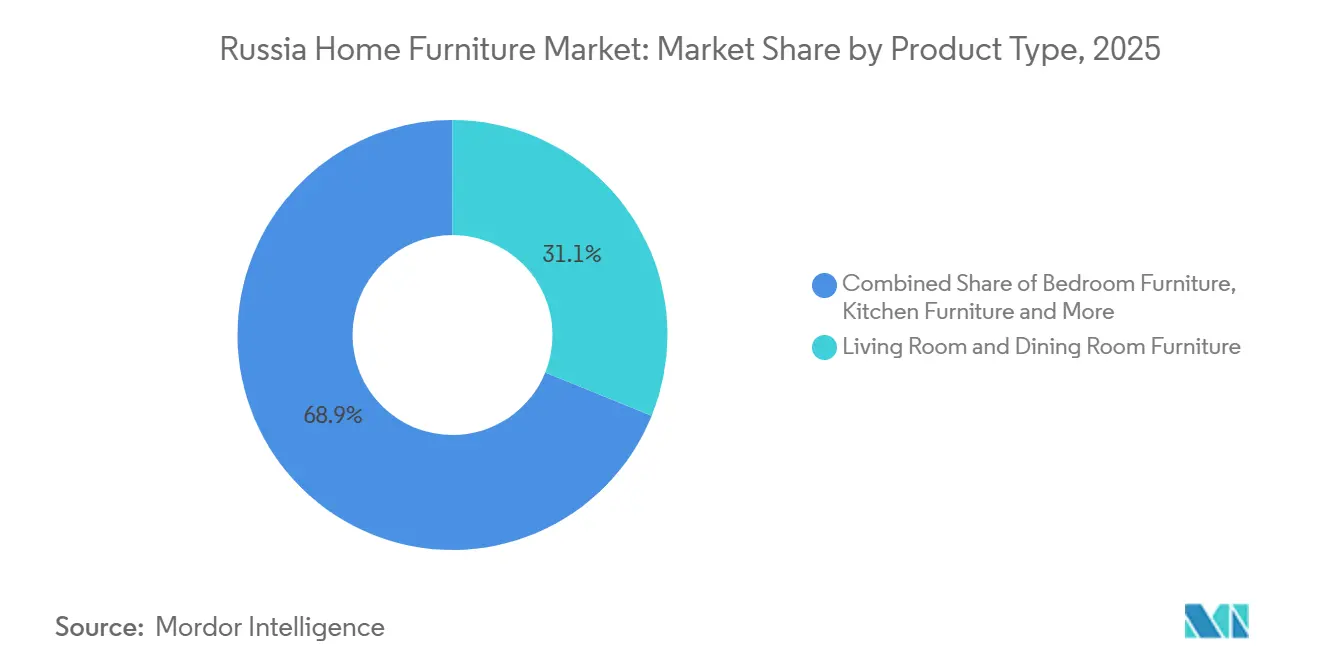

- By product type, living room & dining room furniture led with 31.12% of the Russia home furniture market share in 2025, while home office furniture is projected to expand at a 3.63% CAGR through 2031.

- By material, wood held a 64.67% share of the Russia home furniture market size in 2025, and plastic & polymer furniture is projected to grow at a 3.34% CAGR through 2031.

- By price range, the economy segment captured 54.61% of the Russia home furniture market share in 2025, while the premium segment is forecast to rise at a 3.79% CAGR through 2031.

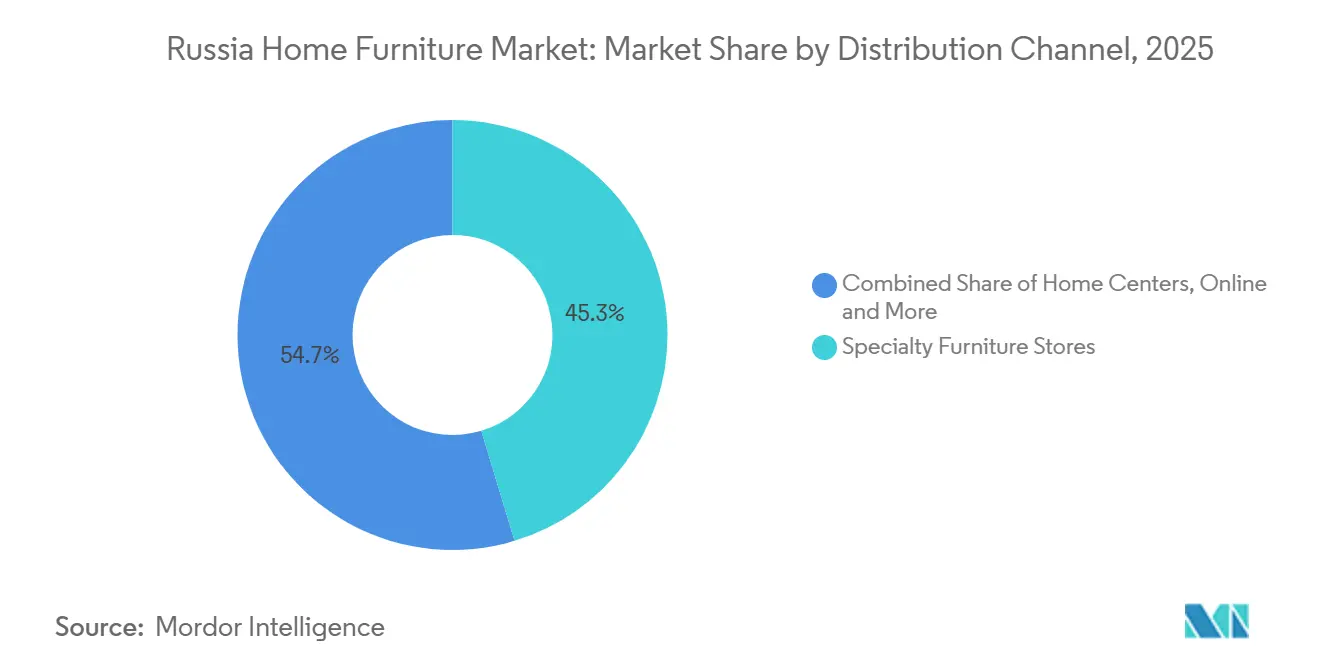

- By distribution channel, specialty furniture stores accounted for 45.34% of the Russia home furniture market share in 2025, and online channels are projected to grow at a 4.67% CAGR through 2031.

- By geography, Moscow & Moscow Oblast commanded 36.53% of the Russia home furniture market share in 2025, and Siberia & the Far East are expected to grow at a 3.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Home Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic production boom after IKEA exit | +1.8% | Global, concentrated in the Volga and the Central Federal Districts | Medium term (2-4 years) |

| Explosive marketplace growth (Wildberries and Ozon) | +1.4% | Global, with early gains in Moscow, St. Petersburg, and Siberian cities | Short term (≤ 2 years) |

| Renewed mortgage subsidies driving housing fit-outs | +1.2% | National, centered in Moscow Oblast, Leningrad Oblast, Krasnodar Krai | Short term (≤ 2 years) |

| Real-wage rebound among the urban middle class | +1.1% | Central, Northwestern, Southern Federal Districts | Short term (≤ 2 years) |

| State grants for wood-panel cluster modernisation | +0.9% | Volga, Urals, Siberian Federal Districts | Long term (≥ 4 years) |

| Retailers’ tie-ups with ex-IKEA suppliers shorten design cycles | +0.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Domestic-Production Boom After IKEA Exit

IKEA’s withdrawal in 2022 catalyzed a fast reallocation of capacity, with industry data showing the brand had represented less than 3% of Russia’s manufacturing base, yet the exit accelerated repositioning that compressed years of change into two cycles[1]https://tadviser.com/index.php/Article:Manufacture,_sale,_export_and_import_of_furniture_in_Russia. Former contract manufacturers, including Angstrem and partners, pivoted quickly to direct relationships with large retailers, which preserved tooling, molds, and shop-floor know-how for rapid SKU expansion. Luzales reactivated the Tikhvin and Vyatka plants bought from IKEA Industry, reached a 250-SKU assortment by February 2024, and started exports to Kazakhstan and Belarus using its own brand structure. Rosstat data reflect this momentum, with 75.7 million physical units produced in 2024 versus 67.3 million in 2023 and a total output value of USD 6.93 billion, up 25.8% year over year. Retail choreography is changing as well, with Angstrem converting about 100 showrooms into room-vignette formats with flat-pack assembly areas to lower consumer switching costs.

Explosive Marketplace Growth (Wildberries and Ozon)

E-commerce gross market value (GMV) in Russia reached nearly USD 114.01 billion in 2024, rising 41% year over year, while furniture and household goods accounted for 14.8% of all online purchases as logistics and visualization tools reduced the need for long showroom visits[2]https://www.taitra.org.tw/en/News_Content.aspx?n=215&s=109469. Wildberries, the largest marketplace, reported strong GMV growth and expanded its seller base from China as cross-border payment options and low commission structures improved seller economics[3]https://www.caixinglobal.com/2025-07-16/chinese-sellers-turn-to-russias-booming-e-commerce-market-amid-us-tariffs-102341590.html. The platform’s footprint spans tens of thousands of pick-up points and extensive warehousing, which supports next-day delivery for most orders and improves conversion for large items that once required 3 to 6 weeks from order to delivery. Furniture-specific investments such as large-format facilities in Novosibirsk supported an acceleration of oversized-goods throughput and catalyzed double-digit growth in Siberian cities. Ozon expanded the local-currency and settlement infrastructure for cross-border sellers, which helped speed up flows of furniture components during 2025 despite broader logistics friction in other cross-border channels.

Renewed Mortgage Subsidies Driving Housing Fit-Outs

The Family Mortgage scheme anchored subsidized lending and comprised a large share of new subsidized loans in early 2025, which maintained transaction volumes near 2023 to 2024 levels despite a very high policy rate environment [4].https://mordorintelligence1-my.sharepoint.com/personal/sarika_singh_mordorintelligence_com/Documents/Work 2025/RD's/Russia Home Furniture Market/CBR.RU The September 2025 update expanded eligibility to select resale housing and capped interest for qualifying families at 6%, which sustained demand in areas where new builds were limited and supported downstream furniture purchases upon completion. Commissioning trends softened in early 2025, although the policy floor prevented a sharper collapse and helped stabilize orders for fittings and project-based furniture among developers completing earlier pipeline projects. The policy set drove activity in smaller towns that benefit from targeted subsidies for housing finance, which is relevant because value-segment furniture sees stronger turnover where construction is distributed outside the capitals. On the retail side, chains with larger warehousing footprints have managed working-capital cycles and showroom stock more efficiently during long construction and handover phases, improving time-to-delivery scores.

Real-Wage Rebound Among the Urban Middle Class

Real disposable income rose in 2024, and payroll tax collections signaled broad-based wage growth that covered most federal subjects and lifted purchasing capacity for mid-range and premium categories. Official wage statistics showed nominal pay around USD 1,263.14 in October 2025, yet real wage growth slowed to 4.9% in the third quarter, narrowing the gap against prior expansion. The progressive tax update trimmed take-home growth, and slowing momentum compressed discretionary categories, which intersected with retailer margin pressure as discounting absorbed higher input costs in a price-sensitive mass segment. Relationships between income and demand remain elastic near the middle and upper tiers, which helps explain the outperformance of some subcategories during peaks in wage growth in 2023 and moderating results in 2024 and 2025 as household budgets tightened. Strategies that align with value for money in the economy segment and curated assortments in premium names remain most effective given the polarization of purchasing power.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-key rate inflation squeezes consumers | -1.5% | National | Short term (≤ 2 years) |

| Ruble volatility inflates import-dependent fittings | -0.9% | National, acute in Central and Northwestern regions | Medium term (2-4 years) |

| Rail-corridor bottlenecks are delaying Asian component inflows | -0.7% | Far Eastern and Siberian Federal Districts | Medium term (2-4 years) |

| Design-talent brain-drain limits product innovation | -0.4% | National, concentrated in Moscow and St. Petersburg | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-Key Rate Inflation Squeeze on Consumers

The key rate peaked at 21% in October 2024 and stood at 16% in December 2025, which created the most restrictive borrowing setting since 2015 and shifted consumption toward saving and delayed deferrable purchases. Mortgage flows fell sharply in early 2025, and consumer installment financing became scarcer or more costly, which weighed on categories with average ticket sizes above USD 1,266.85, such as bedroom sets and fitted storage. Retailers reported pressure on profitability and conversions, with several chains citing credit access and household sentiment as drags on full-price sales and mix. Real-time trackers showed spending declines in the furniture category through late 2025, which aligned with a rotation toward deposits as rates on savings rose. Forward guidance points to gradual easing from 2026 onward, yet normalization implies a multi-year recovery in credit-sensitive sales rather than a fast snapback.

Ruble Volatility Inflates Import-Dependent Fittings

The ruble saw large two-way swings between late 2024 and 2025, which complicated costing for import-reliant inputs such as fittings, coatings, and edge banding that are used at high penetration in kitchens and wardrobes. Industry statements highlighted the difficulty of hedging volatile inputs due to thin derivatives markets and high collateral requirements, which left many medium and small manufacturers exposed to spot pricing. Changes to tariff classifications at customs further disturbed cost planning in 2024, as component inputs for slides and rails faced higher rates than finished furniture imports in some cases. The sector most sensitive to currency swings includes exporters of timber and panels, since dollar revenues translate into fewer rubles when the currency appreciates, which influences reinvestment decisions and capex planning. Localization of specialty fittings is progressing but remains early, and most producers still depend on imported items across key component categories.

Segment Analysis

By Product Type: Home Office Demand Reshapes Production Mix

Living room and dining room furniture held 31.12% of 2025 volumes, and this mature category anchors large-scale upholstered production that favors long replacement cycles in urban households. The Russia home furniture market share concentration in these staples supports stable throughput for plants that produce sofas and storage systems at scale, although slower mix upgrades limit price growth during tight credit cycles. Home office furniture is forecast at a 3.63% CAGR to 2031 as hybrid work norms lead households to convert rooms into permanent desk zones and as public procurement upgrades institutional office spaces in regional centers. The Russia home furniture market size dynamics show wooden office furniture production rising in value, which aligns with mid-tier growth where practical desks, shelving, and ergonomic seating gain share. Kitchen and bedroom systems benefit from new-build deliveries and staged renovations, although margin pressure rises where modular formats standardize designs and compress differentiation.

Bathroom lines remain a smaller niche led by a handful of domestic producers using water-resistant medium-density fiberboard (MDF) and laminated chipboard, and the niche faces price pressure from import competition in select sub-categories. Outdoor furniture concentrates in southern resort destinations and is seasonal in volume, which limits dedicated capacity and favors flexible production that can shift across categories as demand cycles change. Soft transformable lines, including sofa beds for compact urban apartments, maintain steady volumes and benefit from vertically integrated producers that use component commonality to manage cost. E-commerce shifts the product mix toward standardized flat-pack items that fit parcel logistics and compress delivery times, while complex kitchens and built-ins remain anchored to consultative showrooms with in-home measurement. This split creates a two-track product strategy across large retailers as they balance rapid online throughput with higher-margin bespoke projects that require installation talent and longer lead times.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Chipboard Dominance Faces Polymer Challenge

Wood-based materials held a 64.67% share in 2025 as a result of domestic timber abundance and consumer preferences for durable case goods that fit mid-range budgets. The Russia home furniture market share advantage of chipboard widened as capacity additions in Kaluga and Tatarstan expanded supply, and larger mills pushed quality improvements and lowered lead times for downstream factories. MDF and fiberboard maintained niches for smooth facades and premium finishes, with select plants raising environmental certifications and creating re-export options for specialty cabinet goods. Panel oversupply began to pressure smaller mills that lacked scale, which continued a gradual consolidation trend where ISO-certified producers hold a larger share of contract volumes. Compliance with formaldehyde-emission limits created cost hurdles for small producers without in-house testing, and these requirements favored capitalized operators.

Plastic and polymer goods grew from a low base and captured demand for outdoor furniture and children’s items where lightweight construction and weather resistance matter most. The Russia home furniture market size exposure to polymer feedstocks benefited from regional petrochemical ecosystems, which strengthened Tatarstan’s growth across rubber and plastic categories in early 2025. Synthetic stone counters and specialty laminates widened material choices for mid-range kitchens and offered price points below natural granite while preserving durability and aesthetics for daily use. Local production of decorative plastics and textiles improved supply security and shortened timelines, which cushioned volatility from currency swings in sensitive categories. Import reliance remained elevated for edge banding, hardware, and film in many plants, which sustained exposure to exchange-rate moves until further localization scales.

By Price Range: Premium Growth Defies Macro Headwinds

Economy held 54.61% of 2025 sales, and this tier aligns with household budgets that rely on installment plans and discount windows to manage ticket sizes in the USD 126.68-633.45 range for many items. The Russia home furniture market share in the economy reflects income distribution and sensitivity to lending conditions, which slows replacement cycles when rates are high, and access to zero-rate plans is limited. Mid-range demand centers on mass-market quality at moderate price points for wardrobes, bedroom sets, and dining storage, and this segment remains vulnerable to real wage deceleration. Premium grew at a 3.79% CAGR on a small base as high-income clusters in Moscow and St. Petersburg prioritized imported brands through parallel channels despite significant price inflation over 2021 levels. Export-oriented strategies emerged among domestic premium producers who moved into Gulf markets to diversify margin pools and reduce exposure to domestic cycles.

The Russia home furniture market size dynamics by tier show sustained polarization, with defense-linked and financial-sector workers supporting premium orders while state employees and pensioners anchor economy volumes. The middle tier is pressured by progressive taxation and slower real wage gains in late 2025, which narrows the range of customers stepping up to mid-range packages. Rental and subscription models remain nascent but preview different demand rhythms for younger cohorts that may value flexibility over ownership in large metropolitan regions. Scale in distribution and procurement underpins economic leadership among national chains, while premium specialists rely on curated assortments and higher-touch services to justify margin levels. This price-tier map remains sensitive to macro settings and interest rates, and gradual easing would support mid-range recovery as credit-access conditions improve.

By Distribution Channel: E-Commerce Disrupts Specialty Incumbents

Specialty furniture stores accounted for 45.34% of 2025 volumes, anchored by national hypermarket and specialty formats that organize consultative sales for complex categories and support in-home measurement, design, and installation. The Russia home furniture market share of online accelerated as marketplaces captured 14.8% of all national e-commerce transactions for furniture and household goods and delivered next-day service to most postal codes. Marketplaces employed augmented reality visualization to improve purchase confidence for large items and leveraged oversized-goods fulfillment centers to reduce lead times for heavy categories. Home centers retained a limited share where projects combine furniture with flooring and fixtures, and other channels covered B2B contracts for developers and hospitality. Specialty retailers countered with omnichannel investments and faster local delivery from urban warehouses to maintain a service edge in complex categories.

E-commerce growth outpaced store-based sales in 2024 and 2025, and the Russia home furniture market size exposure to digital channels will increase as younger cohorts display lower brand and channel loyalty for commodity items. Specialty chains are investing in virtual planning studios, mobile visualization tools, and faster delivery for custom orders to retain an advantage in bespoke kitchens and wardrobes that require precision installation. Cross-channel experiments such as furniture SKUs on grocery-delivery platforms signal broader retail convergence and new impulse-purchase opportunities in entry-level price points. Regulatory labeling mandates and customs controls increase compliance costs for cross-border marketplaces and may favor domestic logistics ecosystems that can integrate labeling and tracking into fulfillment. Distribution will likely keep bifurcating between high-volume online flows in standardized goods and in-store engagement for complex, higher-ticket installations that need measurement and service assurance.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Geographic fragmentation defines demand, with Moscow and Moscow Oblast absorbing 36.53% of volumes but ceding incremental share to Siberia and the Far East, which carry a 3.27% CAGR outlook on the strength of infrastructure spending and industrial expansion. The capital region’s advantage rests on higher incomes and a dense pipeline of new buildings, which supports complete-room packages and fast delivery from large urban warehouses that improve conversion by reducing wait times. St. Petersburg and Leningrad Oblast, while smaller in share, show strong online penetration and a preference for space-saving cabinetry in older housing stock that favors transformable designs and modular storage. Logistics investments, such as new regional warehouses, extend next-day delivery across Northwestern districts and enable wider assortments that fit local preferences and price points. The Russia home furniture market share in these city clusters benefits from retailer scale and mature last-mile networks that reduce stock-outs and support larger basket sizes for high-ticket categories.

Siberia and the Far East form the fastest-growing region as large-scale investments generate secondary needs in office furnishings, dormitories, and warehouse installations, all of which align with product categories oriented to practical durability. Cross-border trade flows with Asia continue to influence component availability and delivery times, although capacity expansions in domestic panels help cushion some volatility in fittings and specialty materials. Freight distances add costs for shipments to the west, which limits the penetration of Siberian producers in premium segments centered near Moscow and St. Petersburg. Eastern rail bottlenecks raise transit times for routine cargo and slow replenishment for smaller assemblers, which increases the importance of regional inventory pools and local sourcing agreements for frequently used components. Persistent constraints favor retailers with the capital to build warehouses close to demand and reduce dependence on real-time cross-border flows during peak periods and seasonal surges.

The rest of Russia aggregates the Volga, Southern, North Caucasus, and Urals districts, which display diverse growth paths tied to industry mix and infrastructure quality. Volga clusters contribute a large portion of tables, storage, and metal office furniture, supported by proximity to panels, fittings, and transport corridors to both western cities and Central Asia. The Urals maintain demand for institutional and office formats that fit industrial settings, while the south shows seasonality that tracks tourism and renovation cycles in warmer periods. Targeted mortgage support helps smaller towns where developers are less active, and completed units generate follow-on demand for basic furnishings and kitchen fit-outs. Over the forecast, the Russia home furniture market size will spread more evenly across these districts as domestic panel supply increases and logistics reliability improves on the country’s eastern corridors.

Competitive Landscape

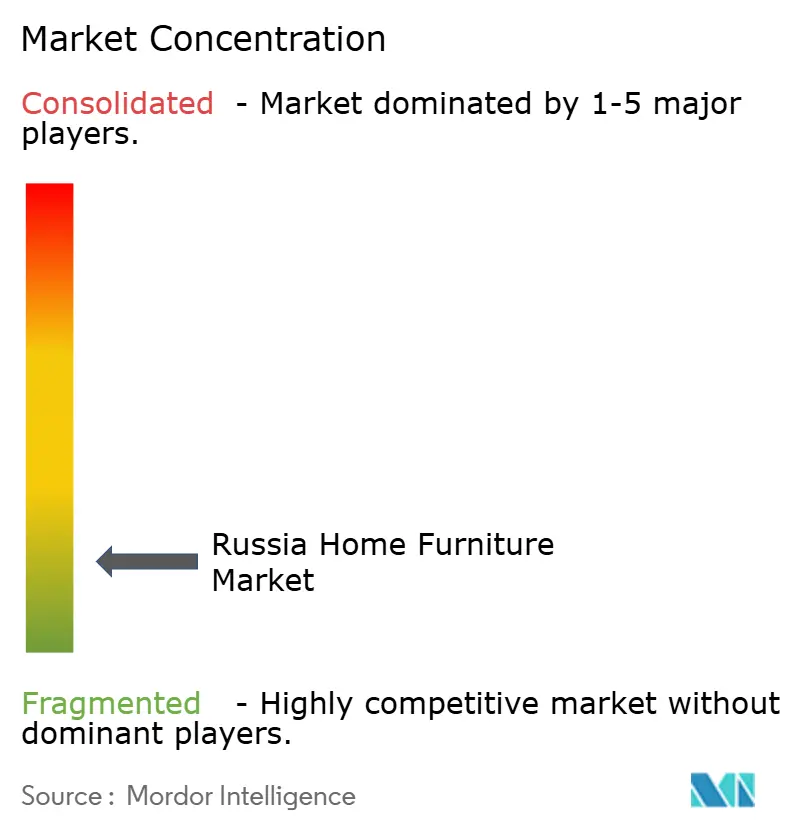

The competitive field is fragmented, with the top 20 manufacturers holding less than half of the total market share, which leaves a large long tail of regional producers and direct-to-consumer brands that compete on distribution reach and speed-to-delivery. Large omnichannel retailers have invested in warehousing, planning studios, and digital engagement to hold share in complex categories, yet profitability remained challenged in 2024 and 2025 as discounting and higher input costs compressed margins. Marketplace platforms continued to pull entry-level sales online, but specialty retailers defended bespoke kitchens and wardrobes, where in-home measurement and installation determine customer choice. Retail experiments with new formats in secondary cities targeted geographies with high online demand and fewer large-format stores, which helps extend reach without the cost of full hypermarket footprints. Vertical integration by leading manufacturers sought to control quality and shorten lead times, while also defending margins through better capture of value-added processing in facades and frames.

Strategic moves in 2025 reflected these patterns. A leading hypermarket chain launched a 28,500-square-meter warehouse in St. Petersburg to extend next-day delivery and add thousands of SKUs to the regional assortment, which improved fulfillment speed and lowered markdown risk on slow movers. A well-known mattress and sleep brand completed a change in ownership structure to a domestic entity, which opened regional expansion plans across the CIS and allowed a clearer export strategy without Western ownership constraints. A major case-goods producer finished implementation of a digital platform across hundreds of stores, centralizing lead management and improving service coverage while lowering contractor and support costs. Another manufacturer commissioned an automated line that scaled monthly output to five-figure set volumes and added value-added material workshops for quartz and veneer processing.

A key theme is the rising role of ex-IKEA suppliers who now partner with national chains and sell branded collections at price points below parallel-imported legacy references, which helps them win middle-tier shoppers switching from stalled European offerings. Omnichannel growth remained a requirement as chains balanced online discovery and in-store installation for kitchens and closets, and investments in visualization and planning lifted attachment rates for custom projects. Marketplaces’ logistics advantages pose a persistent challenge in standardized goods, and specialty retailers defend by emphasizing service steps that marketplaces cannot easily replicate at a low cost. The Russia home furniture market will therefore continue to split between high-volume online staples and showroom-led projects, and players that straddle both can manage category risk and smooth earnings through cycles. Consolidation will likely continue in panels and mid-sized factories as compliance costs, logistics complexity, and financing requirements raise the minimum efficient scale for sustained profitability.

Russia Home Furniture Industry Leaders

Hoff (Domashnii Interior OOO)

Mnogo Mebeli

Askona Vek

Shatura Furniture

Lazurit

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Stool Group launched a full-cycle furniture production and logistics complex in Voskresensk, Moscow Region, investing around USD 6.33 (RUB 500 million) in automation for welding, painting, and sewing processes.

- December 2025: Wildberries announced construction of a 100,000-square-meter logistics center in Uzbekistan with investment exceeding USD 139.35 million (RUB 11 billion), with phased commissioning by end-2026 and up to 7,500 jobs.

- November 2025: Shatura completed rollout of Bitrix24 across its 600-plus store network, centralizing service handling and reducing support and contractor costs substantially.

- August 2025: Hoff opened its 68th store in Serpukhov, Moscow Oblast, with a compact hypermarket format and an in-store design studio for kitchens and wardrobes.

Russia Home Furniture Market Report Scope

In Russia, the home furniture market encompasses the entire journey of furniture - from manufacturing and import to distribution and retail. This furniture, catering to spaces like living rooms, bedrooms, kitchens, and home offices, spans a spectrum from mass-market offerings to premium selections. Demand is shaped by factors such as housing construction, renovation activities, urbanization, income levels, and a consumer preference for affordable, functional, and locally sourced furniture.

The Russia Home Furniture Market Report is Segmented by Product Type (Living Room & Dining Room Furniture, Bedroom Furniture, Kitchen Furniture, Home Office Furniture, Bathroom Furniture, Outdoor Furniture, Other Furniture), Material (Wood, Metal, Plastic & Polymer, Others), Price Range (Economy, Mid-Range, Premium), Distribution Channel (Home Centers, Specialty Furniture Stores, Online, Other Distribution Channels), and Geography (Moscow & Moscow Oblast, St Petersburg & Leningrad Oblast, Siberia & Far East, Rest of Russia).

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| Moscow & Moscow Oblast |

| St Petersburg & Leningrad Oblast |

| Siberia & Far East |

| Rest of Russia |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | Moscow & Moscow Oblast |

| St Petersburg & Leningrad Oblast | |

| Siberia & Far East | |

| Rest of Russia |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Russia Home Furniture Market size and growth outlook to 2031?

The Russia Home Furniture Market size is USD 6.57 billion in 2026 and is forecast to reach USD 7.39 billion by 2031 at a 6.2% CAGR.

Which product categories lead demand in Russia’s home furniture space?

Living Room and Dining Room Furniture leads with 31.12% share, while Home Office Furniture is projected to grow at a 3.63% CAGR through 2031 as hybrid work formalizes.

How are channels shifting between stores and online platforms in Russia?

Specialty stores account for 45.34% of sales, but online channels are growing at a 4.67% CAGR as marketplaces scale next-day oversized delivery and augmented reality visualization.

Which regions show the strongest demand momentum for home furniture in Russia?

Moscow and Moscow Oblast command 36.53% of demand, while Siberia and the Far East are the fastest-growing, with a 3.27% CAGR outlook supported by infrastructure investment.