Rubidium Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

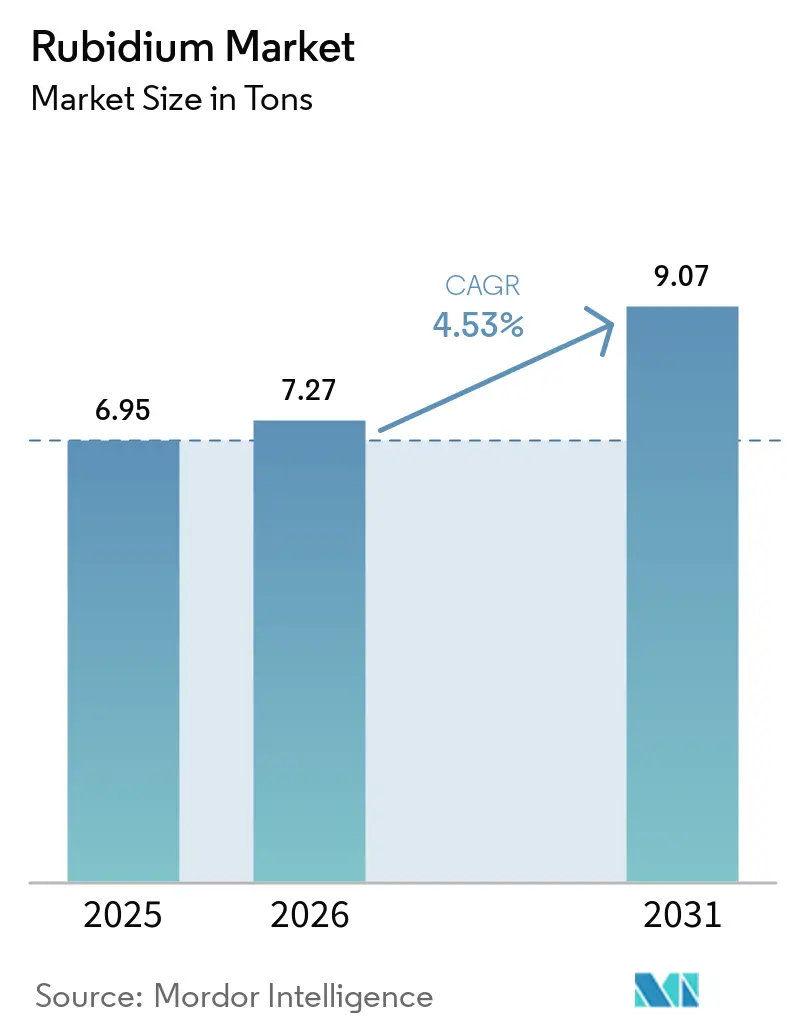

| Market Volume (2026) | 7.27 tons |

| Market Volume (2031) | 9.07 tons |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rubidium Market Analysis by Mordor Intelligence

The Rubidium Market size is projected to expand from 6.95 tons in 2025 and 7.27 tons in 2026 to 9.07 tons by 2031, registering a CAGR of 4.53% between 2026 to 2031. This expansion reflects rising adoption of rubidium atomic clocks in 5G base stations, neutral-atom quantum computers moving from prototypes to pilot lines, and growing uptake of rubidium-82 PET imaging in cardiology departments. Lepidolite-based co-production with lithium refining keeps incremental supply costs low, yet the supply chain remains geographically concentrated in China, amplifying geopolitical risk. Tight availability allows integrated refiners such as Sinomine Resource Group to exercise pricing power when downstream demand spikes. Meanwhile, breakthroughs in brine extraction and chip-scale atomic-clock miniaturization present both cost-reduction opportunities and competitive challenges for incumbents in the rubidium market.

Key Report Takeaways

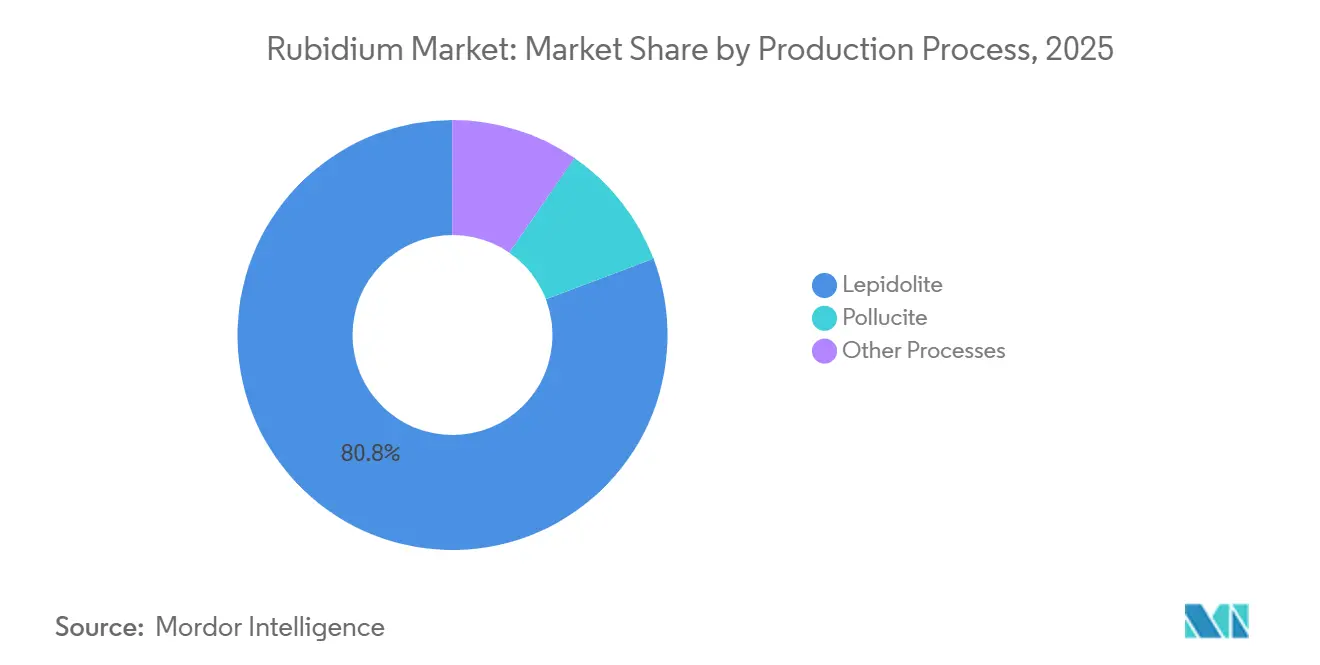

- By production process, lepidolite held 80.79% of the rubidium market share in 2025, while the same route is forecast to expand at 5.06% CAGR through 2031.

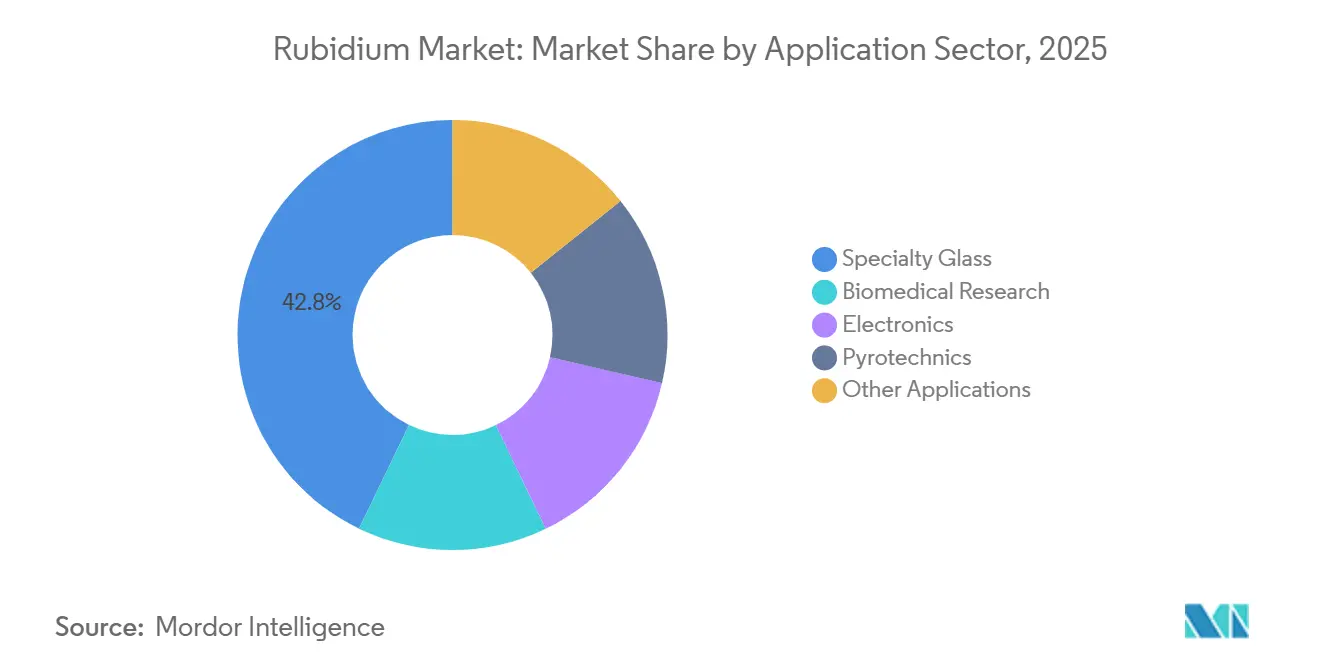

- By application sector, specialty glass commanded 42.85% of the rubidium market size in 2025 and is projected to grow at a 6.15% CAGR to 2031.

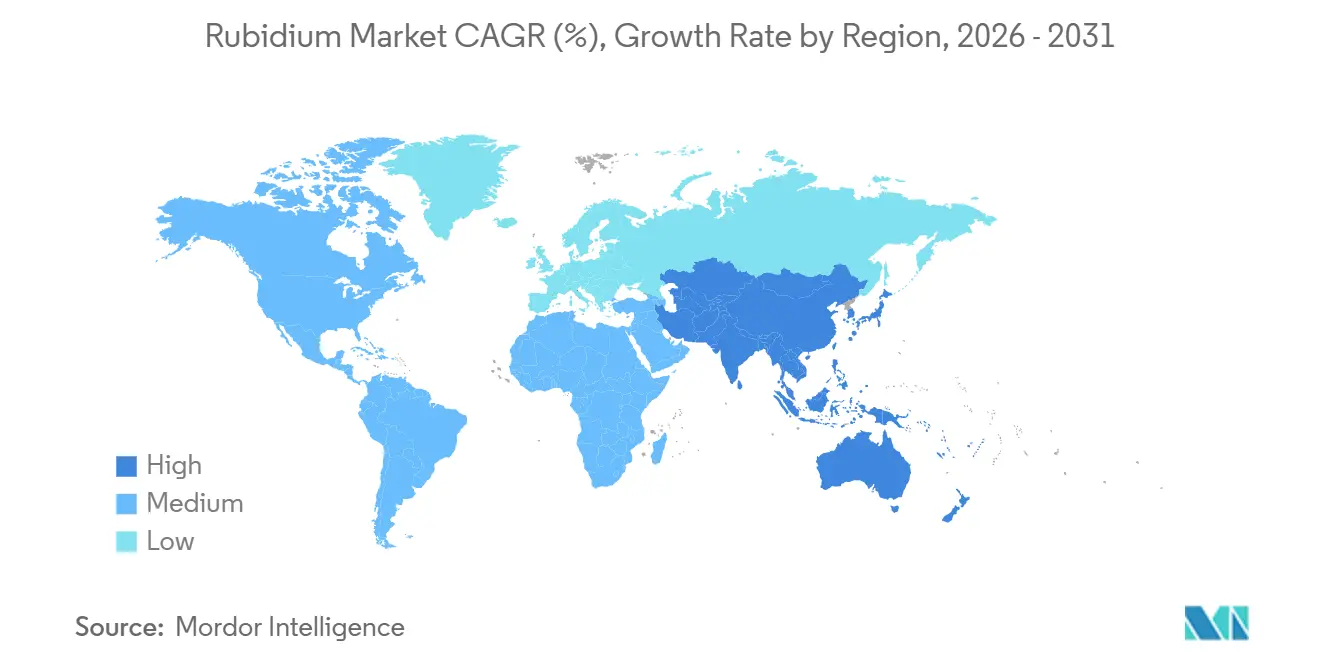

- By geography, Asia-Pacific captured 39.43% of the rubidium market share in 2025; the region is expected to advance at a 5.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rubidium Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing biomedical applications | +0.8% | North America, Europe, APAC (Japan, South Korea) | Medium term (2-4 years) |

| Expanding use in specialty optical-glass and fibre networks | +1.2% | Global, with concentration in APAC and North America | Short term (≤ 2 years) |

| 5G and satellite rollout driving demand for rubidium atomic clocks | +1.5% | Global, led by China, India, Southeast Asia, Middle East | Short term (≤ 2 years) |

| Quantum-technology research and development scale-up (cold-atom sensors, qubits) | +0.6% | North America, Europe, China | Long term (≥ 4 years) |

| Co-production synergies from lithium-mica waste streams | +0.4% | APAC (China, Australia), Africa (Zimbabwe, Namibia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Biomedical Applications

Rubidium-82 PET generators are displacing older isotopes because the 76-second half-life enables on-demand myocardial imaging without daily radiopharmaceutical deliveries. Clinical trials show higher diagnostic accuracy for coronary artery disease than SPECT scans, encouraging hospitals in the United States, Canada, and Germany to install generators during cardiology-suite upgrades[1]Springer, “Rubidium-82 PET Myocardial Perfusion Imaging,” springer.com. Multiple generator systems hold FDA and EMA clearance, smoothing reimbursement approvals and lowering adoption hurdles. Pharmaceutical laboratories also use rubidium compounds as tracers, although these volumes remain small relative to imaging. Continued growth depends on maintaining reimbursement levels for PET studies and on the rollout of hybrid PET-CT scanners in community hospitals. If reimbursement policy remains favorable, the rubidium market could capture additional upside from wider cardiac-imaging use.

Expanding Use in Specialty Optical Glass and Fiber Networks

Rubidium carbonate and oxide act as flux agents and index modifiers in low-dispersion glass for fiber-optic cables and high-resolution lenses. Explosive data-center growth is forcing hyperscalers to densify optical interconnects, pushing demand for single-mode fiber that supports 400 Gbps and 800 Gbps transmission with minimal chromatic dispersion[2]IEEE Communications Society, “Data Center Interconnect,” comsoc.org. Rubidium-doped glass improves thermal stability, reducing signal attenuation on long-haul submarine routes. The same chemistry underpins rubidium titanyl phosphate crystals used in frequency-doubled lasers for lidar and additive manufacturing. Although glass producers continually seek lower-cost substitutes, performance requirements in subsea networks and precision optics make rubidium difficult to eliminate without design compromises. As long as photonics integration accelerates, specialty glass will stay the anchor end-use in the rubidium market.

5G and Satellite Rollout Driving Demand for Rubidium Atomic Clocks

In 2025, global installations of 5G base stations expanded significantly, with China leading in deployments. These stations, requiring nanosecond-level timing, rely on rubidium atomic clocks for dependable synchronization, especially in urban areas where GNSS signals are vulnerable to jamming. Microchip Technology's SA65 clock, a chip-scale solution, consumes minimal power and is compact enough to fit into small-cell radios, now prevalent in urban deployments. Frequency Electronics provides rubidium frequency standards for GPS III satellites, while AccuBeat's clocks ensure stability for Galileo ground stations. Furthermore, commercial satellite constellations are integrating miniature rubidium references to adhere to phase-noise budgets. This surge in the telecom and space sectors bolsters the rubidium market's immediate prospects, although the potential future shift towards optical clocks might moderate long-term demand.

Quantum-Technology Scale-Up

Rubidium-87 atoms serve as qubits in neutral-atom quantum computers and as sensing media in cold-atom interferometers. Pilot systems from Pasqal and QuEra are now moving from research labs into limited-volume production funded by defense and cloud-computing contracts. Government roadmaps in the United States, China, and the European Union collectively earmark billions of dollars for quantum-sensor deployment in navigation, gravimetry, and timing applications. Rubidium-filled photonic-crystal fibers enable chip-scale magneto-optical traps, shrinking power budgets for field units. Commercialization timelines remain uncertain, but even moderate success could lift baseline demand projections. The rubidium market, therefore, enjoys optionality should one or more quantum applications scale ahead of expectations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce primary deposits and high purification cost | -0.9% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Handling/transport safety for highly reactive metal | -0.5% | Global, particularly cross-border shipments | Short term (≤ 2 years) |

| Geopolitical risk: greater than 70% refining in China | -0.7% | North America, Europe, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarce Primary Deposits and High Purification Cost

Natural ores rarely yield rubidium in significant quantities, and dedicated mines for the element are nonexistent. The U.S. Geological Survey notes that global reserves are limited, which hampers swift capacity expansion. For applications in atomic clocks and quantum sensors, refiners aim for a stringent 99.9% purity. Achieving this purity often relies on energy-intensive methods like fractional crystallization or vacuum distillation, both of which produce hazardous by-products. While lab-scale micro-extraction has significantly reduced energy consumption, its commercial rollout remains several years away. Buyers face potential spot-price surges due to long lead times for custom salts and metals. These structural challenges not only cap short-term volume growth but also limit the rubidium market's potential unless there's a breakthrough in purification technologies.

Geopolitical Risk: Greater Than 70% Refining in China

China dominates the global rubidium refining landscape. Notably, the Sinomine Resource Group commands a significant portion of the known pollucite resources, primarily sourced from the Tanco and Bikita mines. The U.S. Geological Survey has highlighted that since 2019, no primary rubidium production has emerged outside of China. While export-control tensions have yet to encompass rubidium, its pivotal role in satellites and 5G networks keeps the spotlight on potential risks. Frequency Electronics has taken steps to insource vapor-cell production, aiming to bolster its GPS III contracts. Concurrently, defense agencies are investing in alternatives to cesium clocks. However, these measures fall short of completely mitigating the fragility of the supply chain. A breakthrough in 2025 saw Chinese brine-extraction techniques yielding high-purity rubidium chloride from brines with minimal rubidium content. This advancement not only solidifies Beijing's grip on the market but also poses a significant challenge to non-Chinese endeavors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Lepidolite Dominance Reflects Lithium Co-Production

Lepidolite contributed 80.79% of the rubidium market size under production-process segmentation in 2025 and is projected to climb at a 5.06% CAGR to 2031. Lithium refiners, leveraging co-production economics, can capture rubidium during acid-leach or roasting steps without incurring standalone capital expenditures. This advantage solidifies lepidolite's dominant position in the rubidium market. Preliminary micro-extraction trials indicate significant energy savings in purification, hinting at potential margin increases if the process is scaled. Pollucite, primarily controlled by Sinomine Resource Group, caters to aerospace contractors with its niche high-purity volumes, meeting the stringent requirements for vapor-cell fabrication. While alternative sources like carnallite and brine are still in the experimental phase, they could gain momentum if the Qinghai Institute's brine process achieves commercialization.

Pollucite’s share lags but carries strategic significance because its high cesium content supports cesium formate drilling fluids, providing cross-subsidy for rubidium yields. Brine extraction offers longer-term upside for the rubidium industry, especially if energy use and reagent recovery mirror laboratory results. However, capital intensity and permitting delays keep new entrants cautious. Supply growth, therefore, remains tethered to lithium and cesium cycles, making price signals in the rubidium market more sensitive to downstream demand surges than to directed mine investment.

By Application Sector: Specialty Glass Leads, Electronics Accelerates

Specialty glass accounted for 42.85% of the rubidium market share in 2025 and is forecast to expand at a 6.15% CAGR through 2031. Rubidium carbonate enhances refractive-index control in fiber-optic preforms and stabilizes laser-grade glass used in lidar systems. Demand correlates with hyperscale data-center expansion and generative-AI traffic, which push fiber-link bandwidths beyond 400 Gbps. Subsea-cable builders also favor rubidium-doped glass for long-haul signal integrity. Although substitution risk exists, performance penalties deter rapid reformulation, sustaining glass leadership in the rubidium market.

As 5G densification and small-cell deployments proliferate, the demand for precise timing nodes has surged, with atomic clocks at the forefront of this electronics boom. Microchip Technology has made significant strides with its compact SA65 device, occupying a mere 17 cm³, which has found favor in both drones and edge servers. Meanwhile, IQD Frequency Products strategically positions its mid-range rubidium oscillators for LTE-Advanced networks, especially in scenarios where GPS jamming poses a threat. In the biomedical realm, rubidium-82 PET tracers are gaining traction in imaging, adding to the market's volume. Additionally, the pyrotechnics industry continues to show a consistent demand for violet fireworks. Together, these diverse applications fortify the rubidium market, shielding it from potential downturns in any one sector.

Geography Analysis

Asia-Pacific led with 39.43% of the rubidium market share in 2025 and is expected to grow at a 5.97% CAGR through 2031. China's dominance in the rubidium market is underscored by its vertical integration, spanning from mining to compound production. Sinomine reported a significant year-on-year revenue surge. Meanwhile, Ganfeng Lithium's Xinyu refinery is not just producing lithium carbonate but also capturing rubidium nitrate, bolstering supply security for domestic clock manufacturers. While Japan and South Korea turn to imports of rubidium carbonate for their high-index camera lenses and precision optics, India's ambitious target of establishing 5G base stations by 2027 is set to further fuel demand.

North America contributes modest volume but enjoys stable defense and medical demand. Frequency Electronics insulates GPS III and classified satellite programs by fabricating vapor cells on Long Island, while Microchip clocks underpin U.S. data-center synchronization. Rubidium-82 PET adoption grows steadily in U.S. hospitals, aided by established reimbursement codes. However, the U.S. Geological Survey reports zero domestic primary production post-2019, leaving buyers reliant on imports or stockpile drawdowns.

Europe mirrors North America’s supply vulnerability but benefits from a processing plant in Germany that upgrades imported concentrates. AccuBeat’s rubidium clocks secure nanosecond-level timing for Galileo ground stations across the continent. The United Kingdom, France, and Germany fund cold-atom sensor programs tapping rubidium vapor cells for autonomous navigation, creating research-driven demand pockets. South America, the Middle East, and Africa remain small today, though Namibia’s Karibib project - optioned by International Lithium Corp in 2025 - could offer regional supply if financing aligns. Overall, geographic dynamics underscore how the rubidium market balances concentrated supply with globally dispersed technology pull.

Competitive Landscape

The global rubidium market is moderately consolidated. White-space opportunities revolve around non-Chinese refining, brine extraction scale-up, and quantum-technology supply chains. Qinghai Institute’s 99.9%-purity brine process could reshape cost curves if proven at an industrial scale, though it may further entrench Chinese dominance. Startups could lift demand if neutral-atom processors reach commercial payback timelines, opening new offtake avenues for refiners. Conversely, Lepidico’s 2024 insolvency shows the financing hurdles facing greenfield lepidolite ventures, reinforcing the high barriers to entry in the rubidium industry.

Rubidium Industry Leaders

Ganfeng Lithium

Sinomine Resource Group

Merck KGaA

American Elements

Lepidico

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Panther Minerals Inc. completed the acquisition of a 100% interest in the Rubidium Ridge pegmatite project located in Ontario, Canada, from Usha Resources Ltd. The transaction enables Panther to pursue lithium and rubidium exploration in an established pegmatite district.

- August 2025: Frequency Electronics projected initial FY 2026 revenue of USD 1 million from its TURbO compact rubidium atomic clock aimed at defense drones and missile systems.

Global Rubidium Market Report Scope

Rubidium is a soft, silvery-white metallic element of the alkali metals group. It can be liquid at ambient temperature, but only on a hot day, given that its melting point is about 40°C. The rubidium market is segmented based on the production process, application sector, and geography. By production process, the market is segmented into lepidolite, pollucite, and other production processes. By application sector, the market is segmented into biomedical research, electronics, specialty glass, pyrotechnics, and other application sectors. The report also covers the market size and forecasts in 18 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of volume (Tons).

| Lepidolite |

| Pollucite |

| Other Processes |

| Biomedical Research |

| Electronics |

| Specialty Glass |

| Pyrotechnics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Production Process | Lepidolite | |

| Pollucite | ||

| Other Processes | ||

| By Application Sector | Biomedical Research | |

| Electronics | ||

| Specialty Glass | ||

| Pyrotechnics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the rubidium market in 2026?

The rubidium market size reached 7.27 tons in 2026 and is projected to grow steadily to 9.07 tons by 2031, registering a CAGR of 4.53%.

Which production route dominates global supply?

Lepidolite co-production with lithium refining provided 80.79% of output in 2025 and remains the fastest-growing extraction path.

What is the main end-use for rubidium today?

Specialty optical glass leads demand with 42.85% share in 2025, followed by electronics applications such as atomic clocks.

Why is rubidium considered a strategic material?

Its use in precision timing, quantum computing, and cardiac imaging makes supply security critical for telecom, defense, and healthcare sectors.

Which region consumes the most rubidium?

Asia-Pacific held 39.43% of global volume in 2025, driven by China’s vertically integrated supply chain and expansive 5G rollout.

Page last updated on: