Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.01 Billion |

| Market Size (2031) | USD 17.19 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Roofing Tiles Market Analysis by Mordor Intelligence

The Roofing Tiles Market size is estimated at USD 13.01 billion in 2026, and is expected to reach USD 17.19 billion by 2031, at a CAGR of 5.51% during the forecast period (2026-2031). Heightened climate volatility, stricter energy codes, and evolving insurance underwriting are reshaping roof-system specifications in favor of durable, cool-reflective tiles that surpass commodity asphalt shingles. Concrete tiles kept momentum through 2025 because of their cost advantage and Class A fire performance, yet clay tiles are expanding faster as heritage-zone approvals and premium coastal demand accelerate adoption. Insurance surcharges on non-impact-rated roofs, combined with utility rebates for cool surfaces, have intensified homeowner migration to high-SRI tile solutions. On the supply side, vertically integrated manufacturers are investing in low-carbon kilns and photovoltaic-ready profiles to comply with carbon-border rules and to monetize renovation incentives across major economies.

Key Report Takeaways

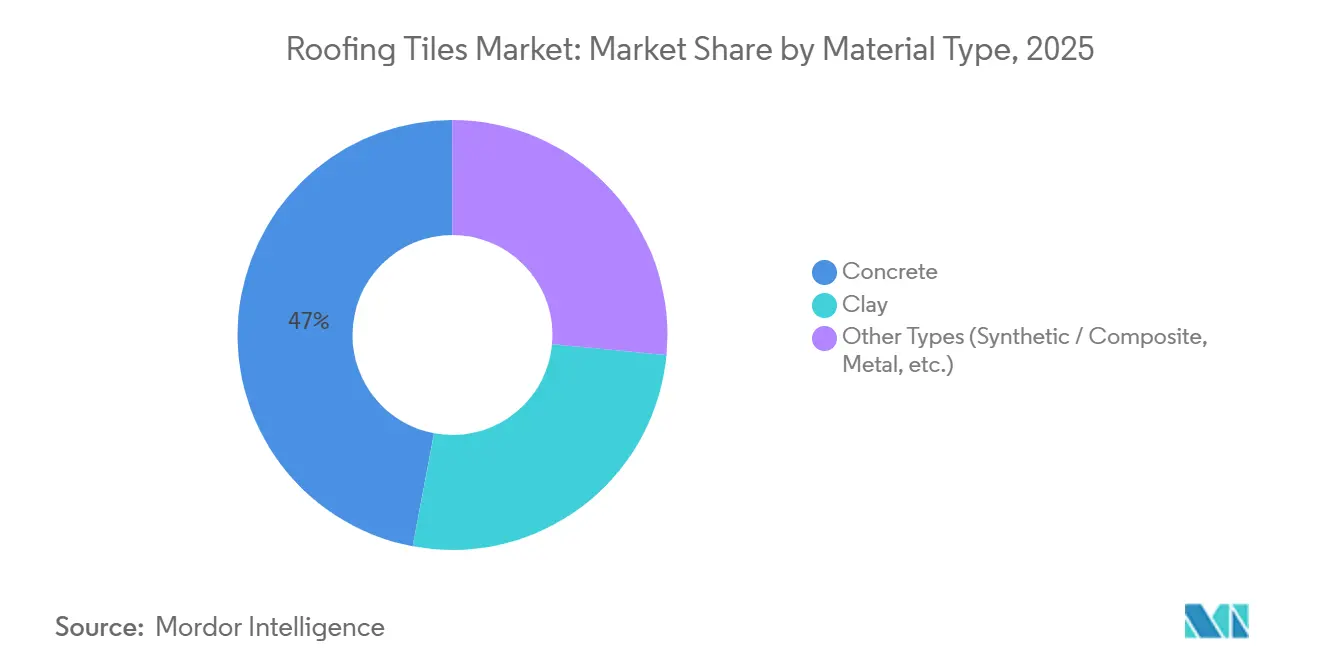

- By material type, concrete maintained a 47.05% roofing tiles market share in 2025 while clay is advancing at a 6.74% CAGR through 2031.

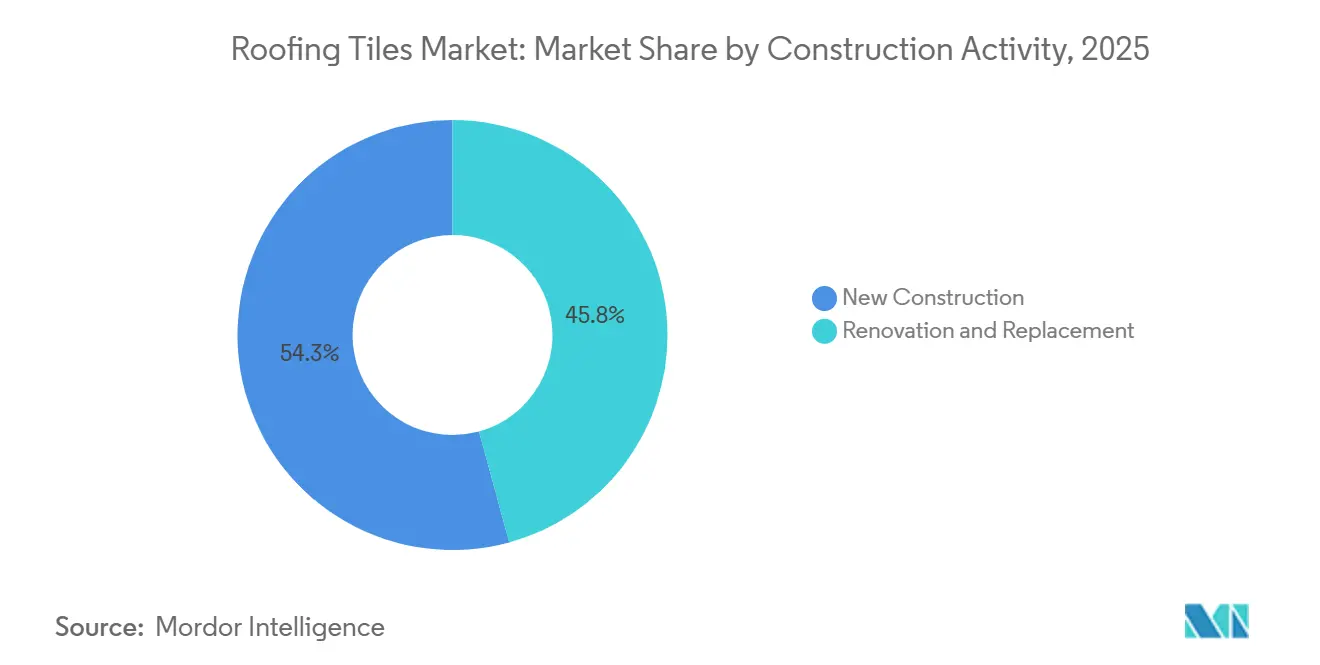

- By construction activity, new construction captured 54.25% of the roofing tiles market size in 2025 and is expected to accelerate at a 6.68% CAGR through 2031.

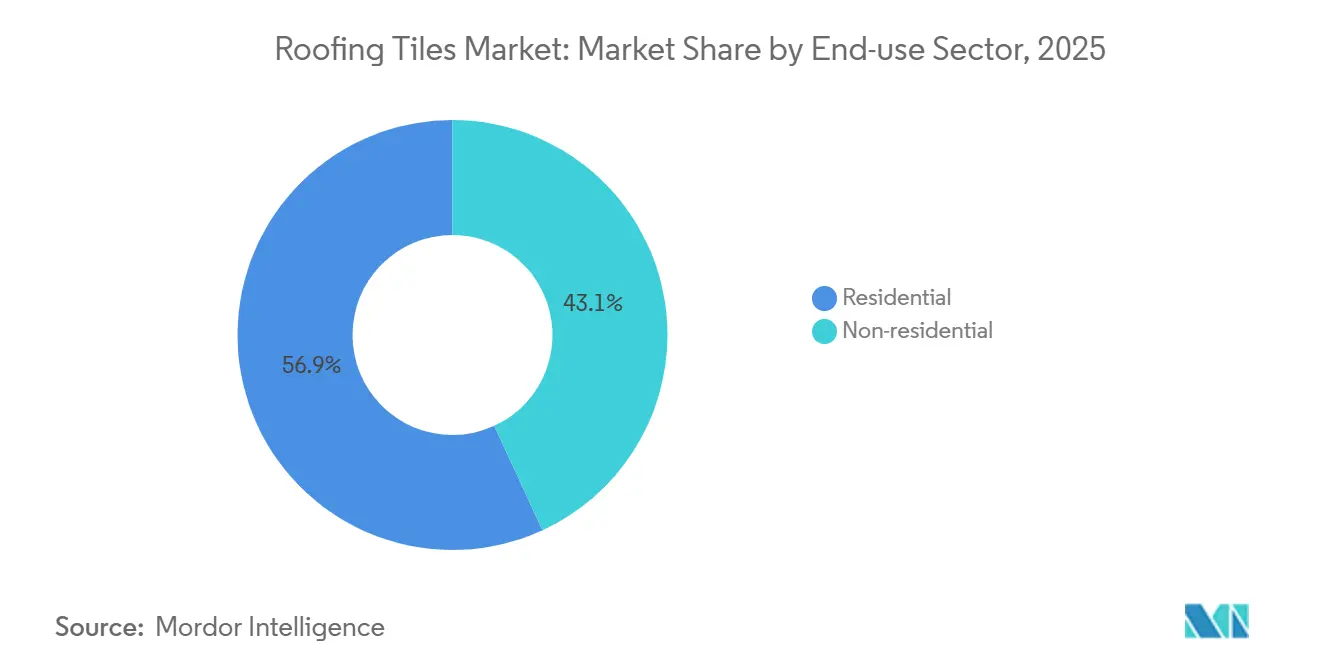

- By end-use sector, residential held 56.87% share of the roofing tiles market size in 2025 and is expanding at a 7.05% CAGR to 2031.

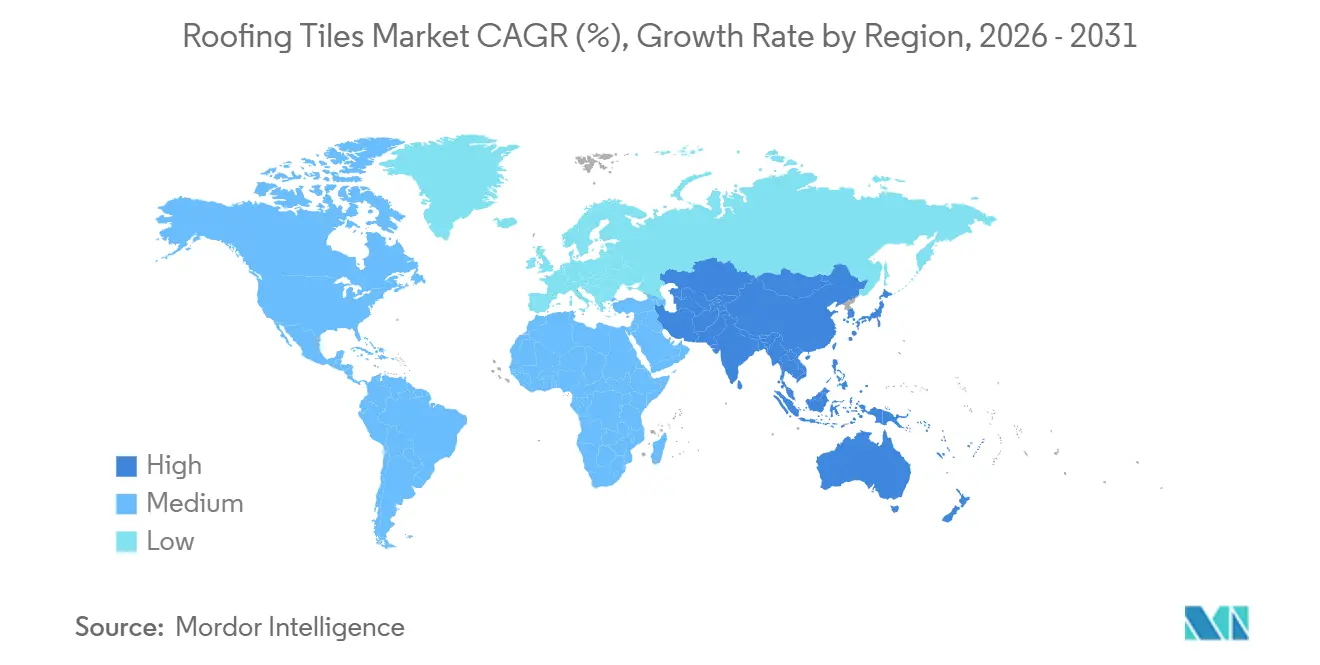

- By geography, Europe accounted for 40.02% of the roofing tiles market in 2025, whereas Asia-Pacific is the fastest-growing region with a 7.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Roofing Tiles Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanization and new-build activity in APAC and Africa | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Aging housing stock drives reroofing demand in North America and Europe | +0.9% | North America and Europe | Medium term (2-4 years) |

| Concrete-tile substitution for asphalt after extreme-weather insurance losses | +0.8% | North America (coastal and hail-prone states), Europe (storm zones) | Short term (≤ 2 years) |

| Mandatory cool-roof codes in heat-island cities | +0.7% | Global, with early gains in California, EU member states, Middle East | Medium term (2-4 years) |

| 3D-printed lightweight tiles shorten installation time and cut logistics costs | +0.3% | North America, Europe (pilot deployments) | Long term (≥ 4 years) |

| Carbon-border levies accelerate adoption of low-carbon kiln technology | +0.5% | Europe (CBAM enforcement), spill-over to export-oriented APAC manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urbanization and New-Build Activity

Residential starts in India, Indonesia, Vietnam, and the Philippines are expanding as urban populations grow and public infrastructure programs unlock greenfield housing. Workforce migration into secondary cities supports demand for weather-resilient roofs that mitigate heat-island effects and qualify for government energy incentives. Developers in Saudi Arabia and the UAE are specifying high-SRI tile systems for mega-projects to satisfy national energy-efficiency frameworks. Lightweight concrete profiles with 20-30% lower mass are enabling use on wood-framed structures in emerging markets, widening the addressable base. Manufacturers are localizing production in Southeast Asia to minimize freight costs and navigate carbon-border policies.

Aging Housing Stock Fuels Reroofing

North American and European roofs installed during post-war booms are reaching end-of-life, compressing the reroof cycle to 15-18 years in high-UV or coastal zones. France’s Climate & Resilience Act targets 370,000 annual home renovations through 2030, and many projects include roof upgrades that reduce winter heat loss by up to 40%. In the United States, homeowners spent USD 45.8 billion on roofing projects in 2023, with insurers in hail-prone states requiring Class 4 impact ratings to retain coverage. Programs such as California Title 24 boost demand for cool-roof tiles that deliver measurable energy savings and qualify for utility rebates.

Concrete-Tile Substitution After Extreme-Weather Losses

Insured roof losses reached USD 31 billion in 2024, with hailstorms and hurricanes disproportionately damaging asphalt shingle roofs lacking Class 4 impact ratings[1]National Oceanic and Atmospheric Administration, “Billion-Dollar Weather and Climate Disasters,” noaa.gov . Insurers in Texas, Florida, and Colorado now impose surcharges exceeding 30% on non-rated roofs, prompting a shift toward concrete and clay tiles that meet ASTM D3746 and UL 2218 standards. Eagle Roofing Products expanded its North Las Vegas facility in 2025 to serve this insurance-driven demand, adding regional capacity for tiles that deliver superior compressive strength above 6,000 psi. European windstorms are producing similar specification shifts as policies mandate wind-uplift testing per EN 14437.

Mandatory Cool-Roof Codes in Heat-Island Cities

California Title 24 requires a minimum Solar Reflectance Index (SRI) of 64 on steep-slope residential roofs in several climate zones, redirecting specifications toward clay and concrete tiles with reflective coatings. The EU Energy Performance of Buildings Directive 2024/1275 compels member states to embed cool-roof thresholds in national codes by 2026, accelerating adoption in France, Spain, and Italy. Middle Eastern authorities are adopting parallel measures to curb cooling loads in commercial facilities. High-SRI tiles cut roof surface temperatures by up to 50 °F, reducing HVAC demand by 10–15% and helping projects secure LEED credits.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-competitive asphalt shingles and metal panels | -0.6% | Global, most acute in North America price-sensitive new-build | Short term (≤ 2 years) |

| Skilled-labor shortages raise installation costs | -0.4% | North America, Europe | Medium term (2-4 years) |

| Volatile energy prices disrupt clay-kiln economics | -0.3% | Europe, Asia-Pacific (natural gas-dependent producers) | Short term (≤ 2 years) |

| Water-extraction limits in drought-prone regions | -0.2% | North America (Southwest), Spain, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Competitive Asphalt Shingles and Metal Panels

Asphalt shingles retain major share of U.S. residential roofing because installed costs remain 40-50% lower than concrete or clay tiles. Owens Corning and GAF plan new plants entering service between 2027 and 2029, reinforcing supply-chain economies. Metal panels are capturing commercial and agricultural demand by offering 50-year life and recyclability, although thermal expansion and noise limit residential use. Tile producers counter through insurance discounts, 50-year warranties, and Class 4 ratings that narrow the lifetime cost gap.

Skilled-Labor Shortages Raise Installation Costs

Median U.S. roofer wages rose to USD 50,970 in 2024, reflecting a tight labor pool and increasing competition for installers skilled in tile systems that require battens, flashings, and underlayment[2]U.S. Bureau of Labor Statistics, “Occupational Employment and Wage Statistics—Roofers,” bls.gov . Labor accounts for USD 3.00–5.00 per square foot on tile jobs, compared with USD 1.50–2.50 for asphalt shingles, constraining uptake in price-sensitive segments. Edilians Academy certified more than 400 roofers in 2023 to expand the labor pipeline for photovoltaic-integrated tiles. Lightweight profiles and interlocking designs are simplifying installation, yet wage inflation remains a near-term headwind.

Segment Analysis

By Material Type: Concrete Still Leads While Clay Gains Premium Share

Concrete commanded a 47.05% roofing tiles market share in 2025 due to cost efficacy and compressive strength, yet clay is growing at 6.74% CAGR on heritage-zone preference and premium coastal demand. Wienerberger’s CO₂-neutral plant in Hungary produces 3 million m² annually and underscores investment in low-carbon concrete. Clay suppliers such as Edilians offer more than 380 colors, helping historic districts comply with SRI requirements without altering vernacular aesthetics. Synthetic composites, including BRAVA’s recycled-polyethylene lines, are carving niche share in salt-spray environments with 50-year warranties. Recycled-aggregate concrete tiles, 15-20% lighter than legacy products, enable installation on wood-framed roofs without deck reinforcement.

Concrete tiles accounted largely for multifamily and commercial projects in 2025 because structural load limits are generous, while clay served the moderate consumption of premium residential demand. Clay is projected to capture fastest growth as production lines retrofit to low-carbon kilns and photovoltaic-ready formats. Manufacturers are diversifying into metal and fiber-cement tiles, yet these materials combined capture low volumes through 2026.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Construction Activity: Renovation Dominates Today, New-Build Gains Pace

Renovation and replacement activities delivered 45.75% of 2025 revenue because aging asphalt shingles from the 1990s are at end-of-life and insurers demand impact-rated upgrades. Reroofing now cycles every 15–18 years in high-UV regions, versus 20–25 previously, accelerating demand for tile systems with Class A fire and Class 4 impact ratings. France’s Climate & Resilience Act alone channels more than 370,000 roof refurbishments annually through 2030.

New construction captured 54.25% of the roofing tiles market size in 2025 and is expected to outpace renovation at a 6.68% CAGR through 2031 as Asia-Pacific urbanization lifts single-family starts and Middle Eastern commercial corridors adopt high-SRI tiles. Developers favor lightweight concrete profiles that cut transport emissions and meet local seismic codes, particularly in Indonesia, Vietnam, and the Philippines. U.S. suburban migration supports fresh detached-home starts, and builders in Colorado and Florida specify concrete tiles to secure insurance discounts on new dwellings.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-use Sector: Residential Leads While Non-Residential Diversifies

Residential captured 56.87% share in 2025 and are rising at 7.05% CAGR on insurer rebates, cool-roof incentives, and improving mortgage affordability in several Asia-Pacific and Middle Eastern economies. Tile demand is most pronounced in single-family detached homes where aesthetics and insurance mandates converge. Eagle Roofing Products operates four U.S. plants and eight design centers to service this segment, with a North Las Vegas hub opened in 2025.

Non-residential demand spans commercial, institutional, and infrastructure roofs where durability and low maintenance support whole-life cost targets. Holcim’s Elevate metal roofing expansion and ROCKWOOL’s new stone-wool insulation line illustrate supplier moves to deliver integrated building-envelope packages. Hospitals and schools in Europe now specify Class A tile systems with high-SRI surfaces to achieve public-procurement sustainability thresholds. Industrial parks in Mexico and ASEAN countries leverage clay and concrete tiles to meet fire regulations while lowering internal temperatures.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Europe sustained a 40.02% share of the roofing tiles market in 2025, upheld by EU-mandated cool-roof codes and aggressive renovation quotas. France alone mandates 370,000 annual home retrofits through 2030, and leaders such as Edilians supply clay tiles with SRI more than 80 that satisfy both energy and heritage criteria. Nordic retrofit programs prefer lightweight tiles to upgrade timber-framed dwellings without extra structural reinforcement, while Spain and Portugal export high-SRI clay tiles to the Americas and Middle East. Consolidation advanced when Wienerberger acquired Terreal for EUR 600 million in 2024, broadening distribution across Western Europe.

Asia-Pacific is the fastest-growing region at 7.19% CAGR through 2031 as India, Indonesia, Vietnam, and the Philippines expand housing and infrastructure pipelines. Urbanization in Indonesia is projected to hit 71% by 2030, and government programs in India underpin strong residential starts. Seismic codes in Japan and South Korea drive adoption of lightweight clay profiles that integrate photovoltaic cells. Chinese demand remains muted amid property deleveraging, but retrofit activity in coastal provinces supports high-SRI tiles that mitigate urban heat.

North American demand is propelled by leading insurers in Texas, Florida, and Colorado that require impact-rated roofs. California Title 24 mandates SRI thresholds on steep-slope roofs, driving tile substitution in heat-island areas. Canada’s single-family starts rebounded in Ontario and British Columbia after rate cuts, while Mexico’s nearshoring trend fuels new commercial roofs that favor cool-roof concrete tiles. South American uptake remains concentrated in Brazil’s recovering residential sector.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The roofing tiles industry exhibits moderate fragmentation. The combined share of Wienerberger, Westlake DaVinci Roofscapes LLC, BMI Group, Crown Roof Tiles, and Etex stood near 35% in 2025, while numerous local firms serve heritage and niche markets. Vertical integration is common: Wienerberger’s CO₂-neutral Hungary plant employs heat-pump drying that lowers gas use by 35%. BMI and Etex are channeling R&D into photovoltaic-ready tiles to capitalize on EU solar-prepared-roof mandates.

Synthetic composite disruptors such as BRAVA produce 100% recycled-plastic tiles with 50-year warranties and Class 4 impact ratings, appealing to insurers and coastal homeowners. 3D printing is reducing concrete tile weight by up to 30%, enabling single-installer handling and lowering shipping costs. Material circularity is also gaining momentum: Holcim’s Malarkey brand reuses 3,000 plastic bags per roof in its shingle backing, suggesting future tile-recycling pathways. IKO’s USD 120 million granule plant in Missouri, opening in 2026, illustrates supply-chain localization to control raw-material inputs.

The industry’s strategic focus spans kiln decarbonization, lightweight formulations, and installer-training academies. These investments aim to secure compliance with incoming carbon-border levies while capturing renovation and new-build opportunities tied to cool-roof regulations and insurance incentives.

Roofing Tiles Industry Leaders

Standard Industries Inc. (BMI Group)

Wienerberger AG

Etex Group

Westlake DaVinci Roofscapes LLC

Crown Roof Tiles

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Hangzhou Singer Building Materials Co., Ltd. launched innovative black and red stone-coated solar roof tiles. These solar roof tiles combine renewable energy generation with durable, weather-resistant roofing, offering a dual-purpose solution that replaces traditional roofing materials and bulky solar panels.

- August 2024: KPG Roofings initiated local manufacturing of ceramic roof tiles in India for the first time. This move aimed to address challenges in the roofing industry caused by fluctuating shipping costs and supply chain disruptions, ensuring a consistent and reliable supply of roofing materials for the Indian market.

Global Roofing Tiles Market Report Scope

Roofing tiles are a type of roofing system comprising overlapping roof tiles attached securely to the roof deck. Various types are available and can be installed in residential, commercial, and industrial settings. Aside from being economical to use, these have properties such as durability, lightweight, and aesthetic appeal. The roofing tile market is segmented by material type, end-use sector, and geography. By material type, the market is segmented into, concrete, clay and other types. By end-use sector, the market is segmented into residential and non-residential. The non-residential segment is sub-segmented into commercial, infrastructure, and industrial and institutional. The report also covers the market size and forecasts for the roffing tiles in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Material Type

| Concrete |

| Clay |

| Other Types (Synthetic / Composite, Metal, etc.) |

By Construction Activity

| Renovation and Replacement |

| New Construction |

By End-use Sector

| Residential | |

| Non-residential | Commercial |

| Infrastructure | |

| Industrial and Institutional |

By Geography

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Material Type | Concrete | |

| Clay | ||

| Other Types (Synthetic / Composite, Metal, etc.) | ||

| By Construction Activity | Renovation and Replacement | |

| New Construction | ||

| By End-use Sector | Residential | |

| Non-residential | Commercial | |

| Infrastructure | ||

| Industrial and Institutional | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the roofing tiles market in 2026?

The roofing tiles market size stands at USD 13.01 billion in 2026 and is forecast to reach USD 17.19 billion by 2031.

What is the expected growth rate for roofing tiles to 2031?

The market is projected to expand at a 5.51% CAGR during the 2026-2031 period.

Which material segment is growing fastest?

Clay tiles, supported by heritage-zone acceptance and coastal demand, are expanding at a 6.74% CAGR through 2031.

Why are insurers influencing tile adoption?

Insurers in storm-prone regions impose surcharges or deny coverage for non-impact-rated roofs, steering homeowners toward Class 4-rated concrete and clay tiles.