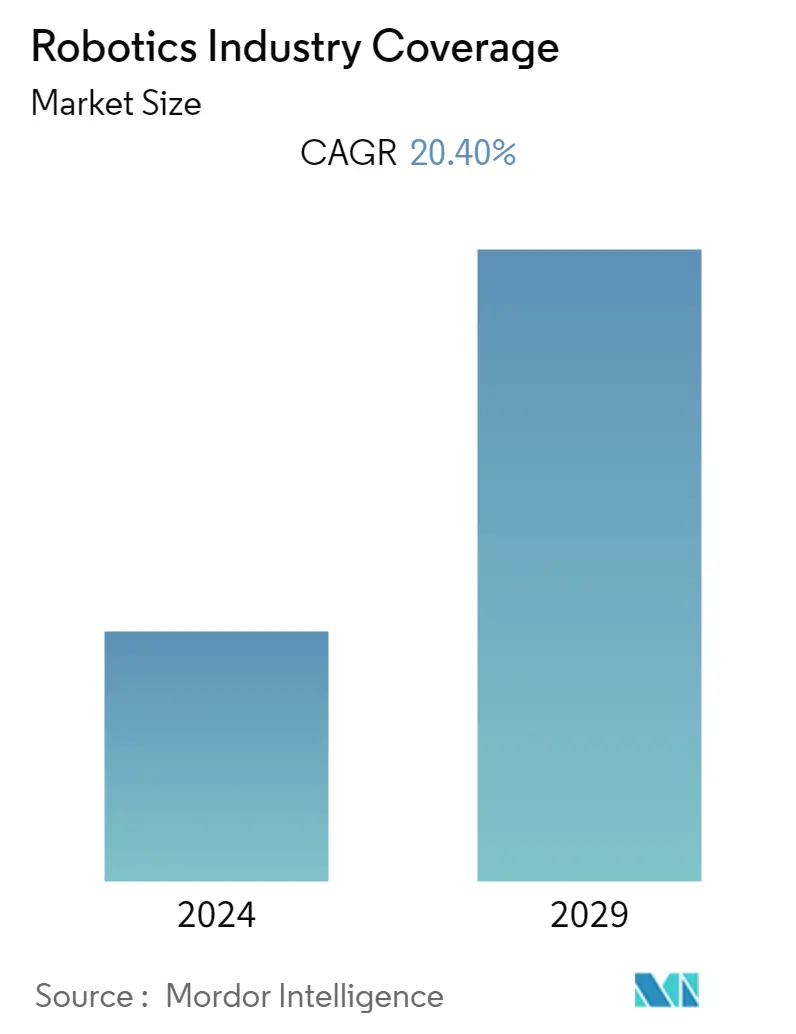

Market Size of Robotics Industry Coverage

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 20.40 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Robotics Market Analysis

The robotics industry market was valued at USD 23.67 billion in 2020 and expected to reach USD 74 billion by 2026 and register a CAGR of 20.4% during the forecast period (2021 - 2026). Robots have gained immense popularity in both the manufacturing and non-manufacturing environments globally.

- Robots continue to gain popularity for their productivity and profitability, especially driven by the automation policies and the Industry 4.0 initiatives globally. According to the World Robotics report presented by the International Federation of Robotics, operatinal stock of industrial robots is expected to reach 3788 thousand units by 2021.

- The market is further expanding into new territories, with small- and medium-sized industries adopting automation, thereby creating demand for robots. The availability of small-capacity and cost-effective solutions from major providers is enabling the penetration of robots into industries.

- Warehouses are susceptible to accidents. According to OSHA, 'Slips, trips, and falls constitute the majority of general industry accidents. They cause 15% of all accidental deaths, and are second only to motor vehicles as a cause of fatalities." Robots in warehouses assist with alleviating workers of the inhuries caused by physical fatigue. Many of these machines are specifically designed to lift heavy objects.

- The spread of COVID-19 has positively impacted the market. This is because companies are using robots to increase social distancing and reduce the number of staff that have to physically come to work. Robots are also being used to perform roles workers cannot do at home. For instance, Walmart is using robots to scrub its floors.Robots in South Korea have been used to measure temperatures and distribute hand sanitiser.

Robotics Industry Segmentation

In terms of robotics industry, the market studied is segmented into industrial robots and service robots. Industrial robots are majorly used in the manufacturing industries. Service robots assist human beings, typically by performing tasks. The types of service robots considered in the scope are professional and personal robots.

Software solutions offered by vendors, for operating or gathering data from robotic systems, are not considered in the scope of the study.

| BY MOBILE ROBOTS | ||||||||||||||||

| ||||||||||||||||

| ||||||||||||||||

| ||||||||||||||||

| ||||||||||||||||

|

| BY ROBOTICS INDUSTRY | ||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||

|

Robotics Industry Coverage Size Summary

The robotics industry is experiencing significant growth, driven by the increasing adoption of automation and Industry 4.0 initiatives across various sectors. Robots are becoming integral in both manufacturing and non-manufacturing environments, enhancing productivity and profitability. The market is expanding as small- and medium-sized enterprises embrace automation, facilitated by the availability of cost-effective robotic solutions. The COVID-19 pandemic has further accelerated this trend, as companies leverage robots to maintain social distancing and reduce on-site workforce requirements. In warehouses, robots are mitigating the risk of injuries from physical labor, while mobile robots are gaining traction in intralogistics and aviation, offering efficient solutions for transporting goods and handling heavy loads.

In North America, the robotics market is bolstered by the rise in warehouse automation and automated material handling, driven by factors such as increasing labor costs and the need for larger distribution centers. The region's advanced industries are at the forefront of adopting robotic technologies, with significant investments in autonomous robots and vehicles. The growth of e-commerce and logistics companies is also contributing to the market's expansion, as the demand for smarter workforce and equipment utilization rises. The competitive landscape is dominated by major players who are expanding their global presence through strategic collaborations. Innovations in robotics, such as disinfecting robots and self-healing biological machines, are further shaping the industry's future.

Robotics Industry Coverage Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Advent Of Industry 4.0 Driving Automation

-

1.2.2 Increasing Emphasis On Safety

-

-

1.3 Market Restraints

-

1.3.1 High Cost of Installation

-

-

1.4 Value Chain Analysis

-

1.5 Porters Five Force Analysis

-

1.5.1 Threat of New Entrants

-

1.5.2 Bargaining Power of Buyers/Consumers

-

1.5.3 Bargaining Power of Suppliers

-

1.5.4 Threat of Substitute Products

-

1.5.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 BY MOBILE ROBOTS

-

2.1.1 Product Type

-

2.1.1.1 Automated Guided Vehicle (AGV)

-

2.1.1.2 Autonomous Mobile Robot (AMR)

-

-

2.1.2 Form Factor

-

2.1.2.1 Fork lifts

-

2.1.2.2 Tow/Tractor/ Tug

-

2.1.2.3 Unit Load

-

2.1.2.4 Assembly Line

-

2.1.2.5 Special Purpose

-

-

2.1.3 End-user Vertical

-

2.1.3.1 Retail and Warehousing

-

2.1.3.2 Automotive

-

2.1.3.3 Food & Beverage

-

2.1.3.4 Pharmaceutical & Healthcare

-

2.1.3.5 Electrical & Electronics

-

2.1.3.6 General Manufacturing

-

-

2.1.4 Geography

-

2.1.4.1 United States

-

2.1.4.2 China

-

2.1.4.3 Europe

-

2.1.4.4 Asia Pacific (Excluding China)

-

2.1.4.5 Rest of the World

-

-

2.1.5 COMPETITIVE INTELLIGENCE

-

2.1.5.1 Vendor Ranking Analysis

-

2.1.5.2 Company Profiles

-

2.1.5.2.1 ECA Group Pty Ltd

-

2.1.5.2.2 Blue Frog Robotics SAS

-

2.1.5.2.3 Geckosystems International Corp

-

2.1.5.2.4 Boston Dynamics Inc

-

2.1.5.2.5 iRobot Corporation

-

2.1.5.2.6 KUKA AG

-

2.1.5.2.7 Kongsberg Maritime AS

-

2.1.5.2.8 Northrop Grumman Corp

-

2.1.5.2.9 SoftBank Robotics Group Corp

-

2.1.5.2.10 UBTech Robotics Ltd

-

- *List Not Exhaustive

-

2.1.5.3 Key Differentiators - Global Vs. Asia Vendors

-

-

-

2.2 BY ROBOTICS INDUSTRY

-

2.2.1 BY INDUSTRIAL ROBOTS

-

2.2.1.1 Product Type

-

2.2.1.1.1 Articulated

-

2.2.1.1.2 SCARA

-

2.2.1.1.3 Linear

-

2.2.1.1.4 Parallel

-

2.2.1.1.5 Other Types

-

-

2.2.1.2 Payload

-

2.2.1.2.1 Low (Less than 20kg)

-

2.2.1.2.2 Medium (20kg -100kg)

-

2.2.1.2.3 High (100kg - 300kg)

-

2.2.1.2.4 Heavy (Greater than 300kg)

-

-

2.2.1.3 End-user Vertical

-

2.2.1.3.1 Automotive

-

2.2.1.3.2 Electrical/Electronics

-

2.2.1.3.3 Plastic & Chemical Products

-

2.2.1.3.4 Food & Beverages

-

2.2.1.3.5 Metal & Machinery

-

2.2.1.3.6 Other Industries

-

-

2.2.1.4 Geography

-

2.2.1.4.1 North America

-

2.2.1.4.2 Europe

-

2.2.1.4.3 Asia Pacific

-

2.2.1.4.4 Africa

-

2.2.1.4.5 Rest of the World

-

-

-

2.2.2 BY SERVICE ROBOTS

-

2.2.2.1 Professional Robots

-

2.2.2.1.1 Field Robots

-

2.2.2.1.2 Professional Cleaning

-

2.2.2.1.3 Inspection and Maintenance

-

2.2.2.1.4 Construction and Demolition

-

2.2.2.1.5 Medical Robots

-

2.2.2.1.6 Rescue & Security Robots

-

2.2.2.1.7 Defense Robots

-

2.2.2.1.8 Underwater Systems (Civil/General)

-

2.2.2.1.9 Powered Human Exoskeletons

-

2.2.2.1.10 Public Relation Robots

-

-

2.2.2.2 Personal/Domestic Robots

-

2.2.2.2.1 Robots for Domestic Tasks

-

2.2.2.2.2 Entertainment Robots

-

2.2.2.2.3 Elderly and Handicap Assistance

-

2.2.2.2.4 Home Security and Surveillance

-

-

2.2.2.3 Geography

-

2.2.2.3.1 North America

-

2.2.2.3.2 Europe

-

2.2.2.3.3 Asia Pacific

-

2.2.2.3.4 Rest of the World

-

-

2.2.2.4 COMPETITIVE INTELLIGENCE

-

2.2.2.4.1 Company Profiles*

-

2.2.2.4.1.1 Denso Corporation

-

2.2.2.4.1.2 Fanuc Corporation

-

2.2.2.4.1.3 KUKA AG

-

2.2.2.4.1.4 Kawasaki Robotics

-

2.2.2.4.1.5 Toshiba Corporation

-

2.2.2.4.1.6 Panasonic Corporation

-

2.2.2.4.1.7 Staubli Mechatronics Company

-

2.2.2.4.1.8 Yamaha Robotics

-

-

-

-

-

Robotics Industry Coverage Market Size FAQs

What is the current Robotics Market size?

The Robotics Market is projected to register a CAGR of 20.40% during the forecast period (2024-2029)

Who are the key players in Robotics Market?

ABB Ltd., Fanuc Corp, KUKA AG, Denso Corp and Kawasaki Robotics GmbH are the major companies operating in the Robotics Market.