| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 2.02 Billion |

| Market Size (2030) | USD 4.77 Billion |

| CAGR (2025 - 2030) | 18.76 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

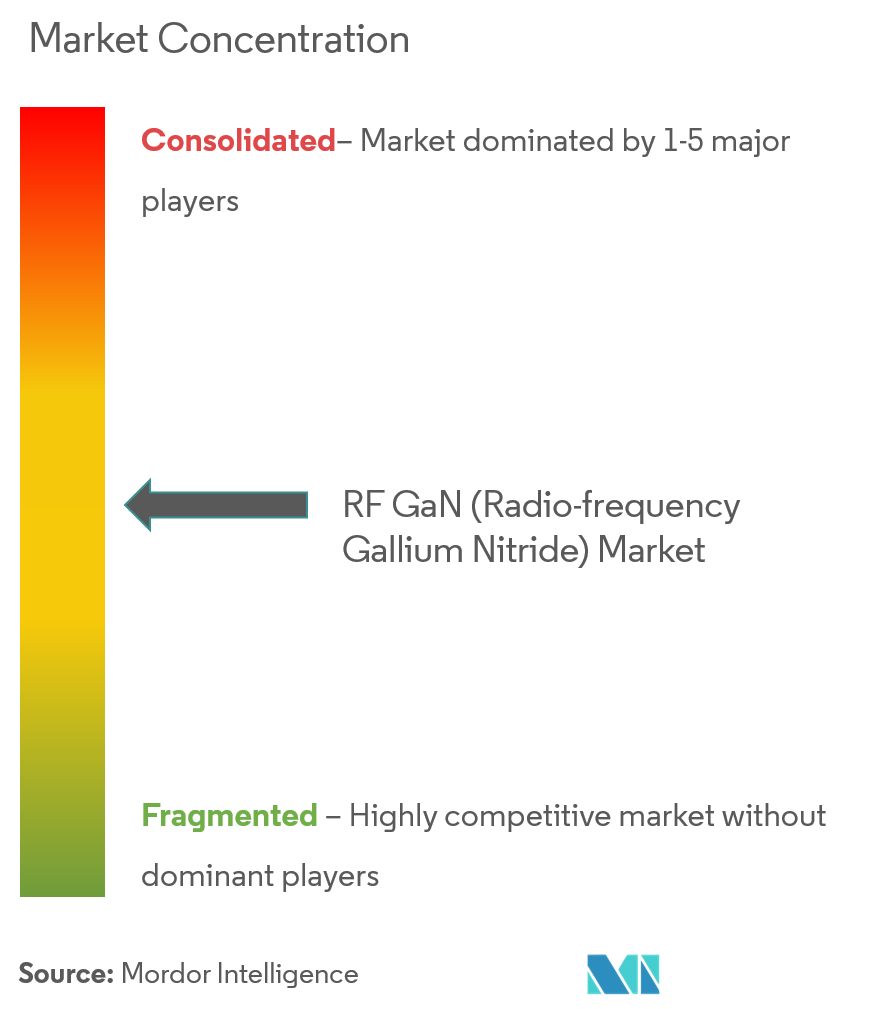

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Radiofrequency Gallium Nitride Market Analysis

The RF GaN Market size is estimated at USD 2.02 billion in 2025, and is expected to reach USD 4.77 billion by 2030, at a CAGR of 18.76% during the forecast period (2025-2030).

The RF GaN industry is experiencing transformative growth driven by the increasing convergence of advanced technologies across multiple sectors. The proliferation of Internet of Things (IoT) technology has created unprecedented demand for RF GaN solutions, as these components enable efficient operation across a wide range of real-time connected devices and applications. GaN semiconductor technology continues to evolve, enabling higher frequencies in complex applications such as phased arrays, radar systems, and sophisticated communication infrastructure. The technology's ability to handle higher power densities while maintaining efficiency has made it increasingly essential for next-generation electronic systems.

The automotive sector has emerged as a significant growth catalyst for RF GaN technology, particularly in electric vehicle applications. Silicon carbide devices, which often incorporate GaN power device technology, are being widely deployed in onboard battery chargers across various vehicle categories, including electric buses, taxis, and passenger cars. The integration of RF electronics in automotive applications extends beyond power systems, playing a crucial role in advanced driver assistance systems (ADAS) and vehicle-to-everything (V2X) communication platforms. This automotive revolution has spurred significant technological innovations in RF GaN design and implementation.

The advancement of autonomous systems has created new opportunities for RF GaN technology deployment. The infrastructure requirements for autonomous vehicles and drones have intensified the demand for high-performance RF components, with RF GaN devices becoming increasingly central to these applications. In June 2022, Integra demonstrated this trend by expanding its 100V RF GaN product portfolio with seven new products targeting avionics, directed energy, electronic warfare, and radar applications, delivering power levels of up to 5kW in a single transistor. This development exemplifies the industry's push toward higher power density and efficiency in autonomous system applications.

Despite the market's robust growth trajectory, manufacturers face several technical challenges in GaN power electronics production and implementation. The optimization of device processing and packaging remains a significant hurdle, while issues such as charge trapping and current collapse continue to require innovative solutions. The industry is actively working to overcome these challenges through advanced research and development initiatives. The rapidly increasing data consumption has intensified the need for more efficient communication networks, with global mobile data traffic projected to reach 77.5 exabytes per month, driving continued innovation in RF GaN technology to support these growing bandwidth requirements.

Radiofrequency Gallium Nitride Market Trends

Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

The telecommunications industry's transition toward 5G networks has emerged as a significant driver for 5G RF semiconductor adoption, with the technology becoming increasingly critical for network service providers due to its ability to provide higher frequency data bandwidth connections. These RF power amplifier devices are instrumental in ensuring maximum frequency generation at necessary bands while preventing interference from other frequency bands, making them ideal for next-generation wireless infrastructure. The deployment of dense, small-scale antenna arrays in 5G infrastructure has created unique challenges around power and thermal management in RF systems, which GaN devices effectively address through their superior wideband performance, efficiency, and power density capabilities.

The rapid expansion of 5G infrastructure is evidenced by the growing number of mobile subscriptions and network deployments worldwide. According to recent industry projections, 5G mobile subscriptions are expected to reach 400 million by 2025, driving substantial demand for RF GaN technology. Major industry players like Qorvo are actively investing in product solutions covering relevant 5G bands, including 3.5, 4.8, 28, and 39GHz, to support both sub-6 GHz and cmWave/mmWave wireless infrastructure development. This is further complemented by strategic industry collaborations, as demonstrated by STMicroelectronics and MACOM Technology Solutions' successful production of RF GaN-on-Silicon prototypes in 2022, which promises to deliver competitive performance while enabling significant economies of scale through integration into standard semiconductor process flows.

Understand The Key Trends Shaping This Market

Download PDF

Favorable Attributes Such as High-Performance and Small Form Factor to Drive Adoption in Military Segment

The military sector's increasing demand for high-power semiconductor devices has become a crucial driver for RF GaN adoption, particularly due to its superior performance characteristics in radar, electronic warfare, and communication systems. GaN technology's ability to deliver high-power density, enhanced efficiency, and operation at higher frequencies makes it an ideal choice for replacing traditional vacuum tube designs with solid-state technologies in military applications. The technology's collective combination of high frequency, wide bandwidth, and high-power capabilities, along with high-temperature operation, has established GaN devices as a strategic material for military applications ranging from radar systems to counter IED jammers and satellite communications.

The adoption of GaN technology in military applications continues to accelerate through ongoing innovation and development programs. For instance, companies like Qorvo have achieved Manufacturing Readiness Level 10 (MRL 10) rating from the US Department of Defense, demonstrating the maturity and reliability of their GaN technology. The technology's application versatility is further evidenced by its successful deployment across various military platforms - GaN on SiC has been effectively utilized in broadband electronic warfare jammers and radar systems, while GaN on silicon (Si) has found success in military communications applications. This widespread adoption is supported by the technology's ability to provide superior heat extraction, optimal power density, and long-term reliability, particularly crucial for mission-critical defense applications. Additionally, the use of RF power semiconductor devices in these applications underscores the importance of GaN technology in modern military systems.

Segment Analysis: By Application

Military Segment in RF GaN Market

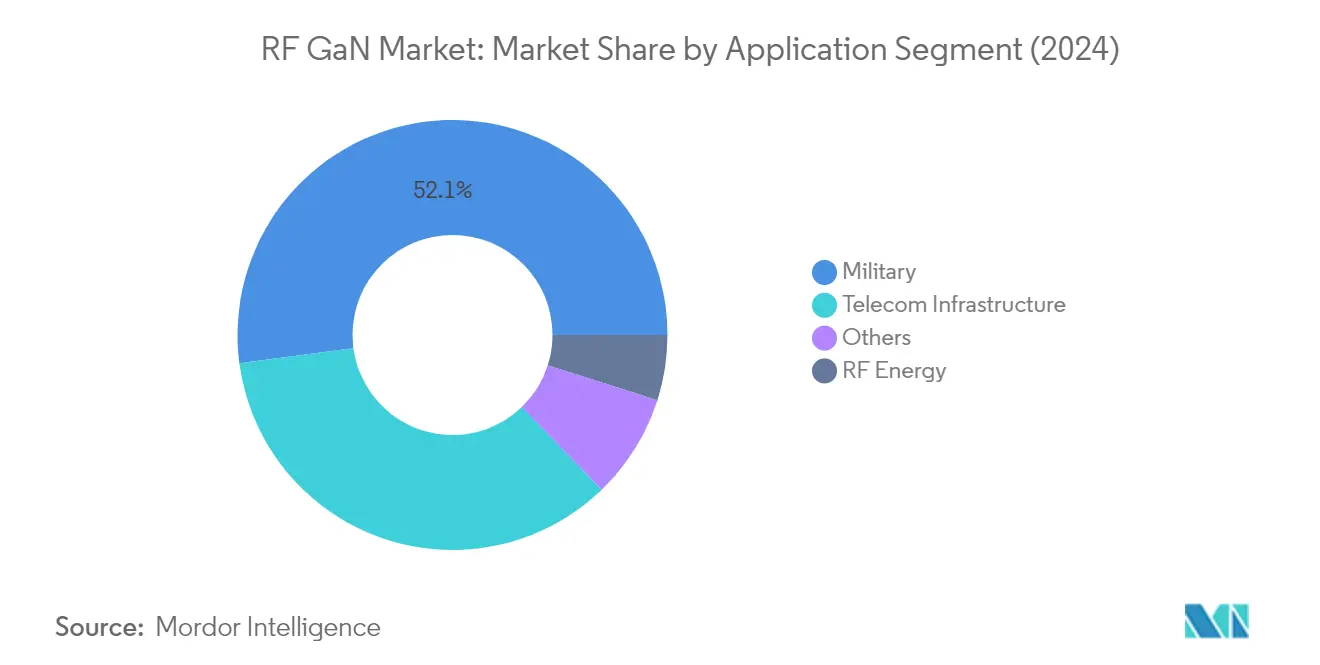

The military segment continues to dominate the RF GaN market, commanding approximately 52% of the total market share in 2024. This significant market position is primarily driven by the increasing adoption of GaN technology in various military applications, including radar systems, electronic warfare equipment, and communication systems. The segment's leadership is reinforced by the superior performance characteristics of GaN technology, such as high power density, improved efficiency, and small form factor, which are crucial for modern military applications. The defense sector's continuous focus on modernization and the need for high-performance RF solutions in mission-critical applications further solidifies this segment's dominant position in the market. The use of RF power transistors in these applications enhances the overall system capabilities.

RF Energy Segment in RF GaN Market

The RF energy segment is emerging as the fastest-growing segment in the RF GaN market, with an expected growth rate of approximately 83% during the forecast period 2024-2029. This remarkable growth trajectory is driven by the increasing adoption of RF energy applications in various industrial processes, including plasma lighting, industrial heating, and medical applications. The segment's growth is further accelerated by the superior capabilities of GaN technology in delivering precise power control and improved efficiency in RF energy applications. The expanding scope of RF energy applications across different industries and the continuous technological advancements in GaN-based solutions are expected to maintain this segment's high growth momentum. The integration of GaN power amplifiers in these applications is pivotal for achieving enhanced performance.

Remaining Segments in RF GaN Market

The remaining segments in the RF GaN market include telecom infrastructure, satellite communication, wired broadband, commercial radar and avionics, and other applications. The telecom infrastructure segment holds particular significance due to the ongoing 5G network deployments and infrastructure development. Satellite communication and wired broadband segments are gaining traction due to increasing demand for high-speed connectivity and communication solutions. The commercial radar and avionics segment serves critical applications in civil aviation and weather monitoring systems, while other applications encompass emerging use cases in various industrial and commercial sectors. The role of RF integrated circuits in these segments is crucial for optimizing performance and efficiency.

Segment Analysis: By Material Type

GaN-on-Si Segment in RF GaN Market

The GaN-on-Si segment continues to dominate the RF GaN market, holding approximately 63% of the market share in 2024. This significant market position is primarily driven by the segment's widespread adoption in base stations and telecommunication applications, particularly in 5G infrastructure development. The deployment of GaN-on-Si-based devices provides multiple benefits in terms of efficiency, thermal performance, weight, and size. While GaN-on-Si within a 150mm wafer diameter is already being deployed for various end-use applications, 200mm diameter GaN-on-Si wafers are in active development by leading players in the manufacturing space. The increasing demand for technologically advanced electronic wafers, coupled with the rising trend of digitalization, has driven substantial investment by power semiconductor manufacturers to build advanced, cost-effective RF products. The integration of microwave semiconductors in these devices enhances their performance and efficiency.

GaN-on-SiC Segment in RF GaN Market

The GaN-on-SiC segment is experiencing remarkable growth in the RF GaN market, with an expected growth rate of approximately 41% during 2024-2029. This exceptional growth is driven by its superior performance characteristics in high-power and high-voltage switching applications. The technology provides an excellent crystallographic match between the epi and substrate layers, along with an electrically and thermally conductive path from top to bottom of the wafer. The segment's growth is particularly accelerated by increasing demand for power amplifier chips and other RF devices in 5G base stations, where GaN-on-SiC devices have emerged as a preferred choice in the high band of 5G FR1, effectively replacing LDMOS technology. The technology's suitability for deployment in 48V Doherty amplifiers, achieving high efficiency and ruggedness for high-power amplifiers in 5G base stations, further strengthens its growth trajectory. The use of GaN RF devices in these applications is crucial for achieving optimal performance.

Remaining Segments in RF GaN Market by Material Type

Other material types in the RF GaN market, including GaN-on-GaN and GaN-on-Diamond technologies, play a crucial role in specific applications requiring specialized performance characteristics. GaN-on-Diamond technology offers unique advantages in thermal management and form factor optimization, making it particularly valuable for high-power RF applications in military radar systems, satellite communications, and commercial base stations. Meanwhile, GaN-on-GaN technology is emerging as a solution for applications demanding high power density, with its lower defectivity in epitaxial devices enabling higher efficiency and current density while providing extended device durability. These alternative material technologies continue to evolve and find their niches in specialized applications where their unique properties provide distinct advantages.

RF GaN Market Geography Segment Analysis

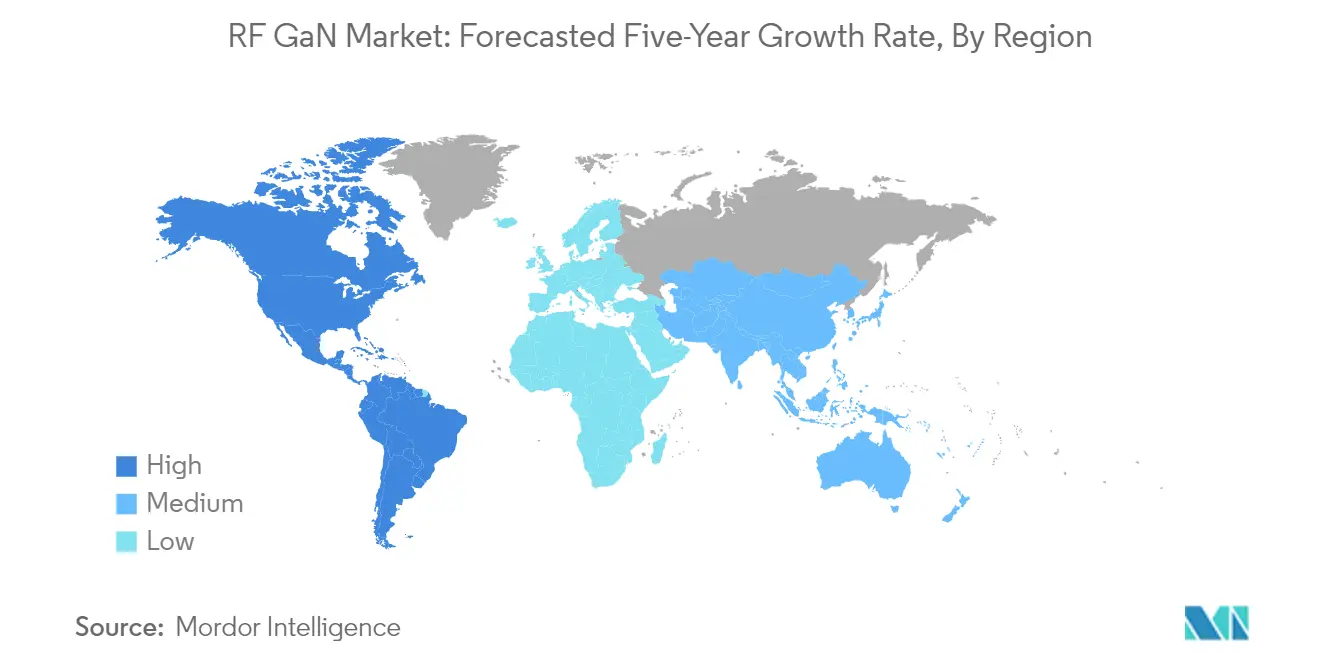

RF GaN Market in North America

North America represents a significant market for the RF GaN sector, holding approximately 24% of the global market share in 2024. The region's dominance is primarily driven by its robust defense and aerospace sectors, coupled with extensive 5G infrastructure development. The United States, in particular, maintains its position as a pioneer in advanced military applications, with substantial investments in radar systems, electronic warfare capabilities, and communication technologies. The presence of major RF semiconductor manufacturers and research institutions has fostered continuous innovation in the sector. The region's semiconductor industry demonstrates strong research and development capabilities, particularly in GaN-on-silicon technology for high-frequency applications. The increasing adoption of RF GaN in commercial applications, including wireless infrastructure and satellite communications, further strengthens the market position. Additionally, the region benefits from strong government support and defense contracts, which continue to drive technological advancements and market growth.

RF GaN Market in Europe

The European RF GaN sector has demonstrated remarkable growth, achieving an approximately 25% annual growth rate between 2019 and 2024. The region's market expansion is driven by significant investments in defense modernization programs and 5G infrastructure development across multiple countries. European manufacturers have established strong capabilities in GaN technology, particularly in areas such as radar systems and telecommunications equipment. The presence of leading research institutions and technology centers has fostered innovation in RF GaN applications, especially in the automotive and industrial sectors. The region's focus on renewable energy and electric vehicles has created additional demand for RF GaN components. European countries' collaborative approach to defense and telecommunications projects has facilitated knowledge sharing and technological advancement. The market also benefits from strong regulatory frameworks and standardization efforts that promote the adoption of advanced semiconductor technologies. Furthermore, the region's emphasis on reducing dependency on external semiconductor suppliers has led to increased investments in domestic manufacturing capabilities.

RF GaN Market in Asia-Pacific

The Asia-Pacific region continues to dominate the global RF GaN sector, with strong growth prospects projected for 2024-2029. The region's market is characterized by rapid technological advancement and expanding manufacturing capabilities, particularly in countries like China, Japan, and South Korea. The massive deployment of 5G infrastructure across the region drives substantial demand for RF GaN components. The presence of major semiconductor manufacturing facilities and continued investments in production capabilities strengthens the region's market position. Countries in the region are increasingly focusing on developing domestic semiconductor capabilities, including RF GaN technology, to reduce dependency on imports. The growing defense modernization programs in various Asian countries further fuel the demand for RF GaN components in military applications. The region also benefits from strong government support for semiconductor industry development, including research grants and infrastructure investments. Additionally, the increasing adoption of RF GaN in commercial applications, such as wireless communications and automotive systems, continues to drive market expansion.

RF GaN Market in Rest of the World

The Rest of the World region, comprising Latin America, the Middle East, and Africa, represents an emerging market for RF GaN technology with growing potential. These regions are witnessing increased adoption of RF GaN components, primarily driven by the modernization of military equipment and the expansion of telecommunications infrastructure. The Middle East, in particular, shows strong potential due to its focus on defense modernization and smart city initiatives. Latin American countries are gradually increasing their investments in telecommunications infrastructure, creating opportunities for RF GaN applications. The region's market is characterized by growing awareness of GaN technology benefits and increasing investments in wireless communication networks. Defense modernization programs in several countries are creating new opportunities for RF GaN applications in radar and communication systems. Additionally, the increasing focus on satellite communications and broadcasting services is driving the adoption of RF GaN technology in these regions. The market also benefits from technology transfer through international partnerships and collaborations.

Get Analysis on Important Geographic Markets

Download PDF

Radiofrequency Gallium Nitride Industry Overview

Top Companies in RF GaN Market

The RF GaN market features a mix of established semiconductor manufacturers and specialized RF component providers who are driving innovation through continuous R&D investments. Companies are focusing on expanding their GaN product portfolios through both internal development and strategic acquisitions, particularly targeting 5G infrastructure and defense applications. The industry demonstrates strong operational agility through flexible manufacturing approaches, combining in-house production with foundry partnerships to optimize capacity and capabilities. Strategic moves include vertical integration efforts to control the supply chain, especially in GaN-on-SiC technology, while geographic expansion emphasizes establishing a presence in key markets like China and Europe. Manufacturers are also prioritizing the development of application-specific solutions and investing in advanced packaging technologies to meet evolving customer requirements across telecom, defense, and industrial sectors.

Market Structure Shows Strategic Regional Dominance

The RF GaN market exhibits a moderately consolidated structure with a blend of global semiconductor conglomerates and specialized RF component manufacturers. Major conglomerates leverage their extensive R&D capabilities and established relationships with defense contractors and telecom equipment manufacturers, while specialized players differentiate themselves through focused innovation in specific applications. The market demonstrates strong regional characteristics, with American and Japanese companies historically dominating the patent landscape, though Chinese manufacturers are rapidly expanding their presence, particularly in commercial wireless applications.

The industry has witnessed significant M&A activity, primarily driven by larger semiconductor companies seeking to strengthen their RF GaN capabilities and expand their market presence. These strategic acquisitions often target companies with specialized GaN technology expertise or established positions in key application segments. The consolidation trend is particularly evident in the defense and 5G infrastructure sectors, where companies aim to create comprehensive solution portfolios. Market participants are also forming strategic alliances and joint ventures to share technology expertise and access new geographical markets, especially in regions with growing defense modernization and 5G deployment initiatives.

Innovation and Adaptability Drive Market Success

Success in the RF GaN market increasingly depends on companies' ability to develop differentiated technologies while maintaining cost competitiveness. Incumbent players are focusing on strengthening their intellectual property portfolios, expanding manufacturing capabilities, and deepening relationships with key customers in defense and telecommunications sectors. Companies are also investing in advanced packaging solutions and system-level integration capabilities to provide more complete solutions to end customers. The ability to navigate complex supply chains and maintain reliable production capabilities, particularly in light of recent global disruptions, has become a critical success factor.

Market contenders are finding opportunities by focusing on specific application niches and developing innovative solutions for emerging applications like satellite communications and industrial RF systems. The increasing emphasis on domestic semiconductor capabilities in major markets creates opportunities for regional players to establish stronger positions. Success factors also include the ability to manage regulatory compliance across multiple jurisdictions and maintain strong relationships with government customers, particularly in defense applications. Companies must also address the growing importance of sustainability and energy efficiency in their product development strategies, as these factors increasingly influence customer decisions in both commercial and military applications. The RF power semiconductor market is evolving with a focus on these innovative and adaptable strategies, which are critical for maintaining a competitive edge.

Radiofrequency Gallium Nitride Market Leaders

-

Mitsubishi Electric Corporation

-

STMicroelectronics NV

-

Qorvo Inc.

-

Analog Devices Inc.

-

Raytheon Technologies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Radiofrequency Gallium Nitride Market News

- September 2022: MaxLinear Inc. and RFHIC announced a collaboration to deliver a production-ready 400MHz Power Amplifier solution for 5G Macrocell radios, utilizing MaxLinear MaxLIN Digital Predistortion and Crest Factor Reduction technologies to optimize the performance of RFHIC's latest ID-400W series GaN RF Transistors. Combining RFHIC's dual-reverse GaN RF transistor ID41411DR with MaxLIN DPD and making it available as a pre-verified solution would allow Radio Access Network (RAN) product developers to quickly deliver ultra-wideband 400MHz Macro PAs for all global 5G mid-band deployments with high power efficiency and low emissions.

- June 2022: For their line of 100 V RF GaN products, Integra announced the inclusion of seven more devices with power levels up to 5 kW in a single transistor for the avionics, directed energy, electronic warfare, radar, and scientific application areas. These items use Integra's 100 V RF GaN technology, which is designed to give the maximum power and efficiency possible in a single transistor while maintaining stable operating junction temperatures.

Radiofrequency Gallium Nitride Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

- 4.5 Assessment of the Impact of COVID-19 on the Industry

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

- 5.1.2 Favorable Attributes Such As High-performance and Small Form Factor to

-

5.2 Market Restraints

- 5.2.1 Cost & Operational Challenges

6. MARKET SEGMENTATION

-

6.1 By Application

- 6.1.1 Military

- 6.1.2 Telecom Infrastructure (Backhaul, RRH, Massive MIMO, Small Cells)

- 6.1.3 Satellite Communication

- 6.1.4 Wired Broadband

- 6.1.5 Commercial Radar and Avionics

- 6.1.6 RF Energy

-

6.2 By Material Type

- 6.2.1 GaN-on-Si

- 6.2.2 GaN-on-SiC

- 6.2.3 Other Material Types (GaN-on-GaN, GaN-on-Diamond)

-

6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Aethercomm Inc.

- 7.1.2 Analog Devices Inc.

- 7.1.3 Wolfspeed Inc. (Cree Inc.)

- 7.1.4 Integra Technologies Inc.

- 7.1.5 MACOM Technology Solutions Holdings Inc.

- 7.1.6 Microsemi Corporation (Microchip Technology Incorporated)

- 7.1.7 Mitsubishi Electric Corporation

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Qorvo Inc.

- 7.1.10 STMicroelectronics NV

- 7.1.11 Sumitomo Electric Device Innovations Inc.

- 7.1.12 HRL Laboratories

- 7.1.13 Raytheon Technologies

- 7.1.14 Mercury Systems, Inc

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Radiofrequency Gallium Nitride Industry Segmentation

GAN stands out in RF applications because of several reasons, such as high breakdown field, high saturation velocity, and robust thermal properties, as they have been instrumental in transmitting signals over long distances or at high-end power levels.

This report segments the market by Application (Military, Telecom Infrastructure, Satellite Communication, Wired Broadband, Commercial Radar and Avionics, and RF Energy), Material (GaN-on-Sic and GaN-on-Silicon), and Geography (North America, Europe, Asia-Pacific, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Application | Military |

| Telecom Infrastructure (Backhaul, RRH, Massive MIMO, Small Cells) | |

| Satellite Communication | |

| Wired Broadband | |

| Commercial Radar and Avionics | |

| RF Energy | |

| By Material Type | GaN-on-Si |

| GaN-on-SiC | |

| Other Material Types (GaN-on-GaN, GaN-on-Diamond) | |

| Geography | North America |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Radiofrequency Gallium Nitride Market Research FAQs

How big is the RF GaN Market?

The RF GaN Market size is expected to reach USD 2.02 billion in 2025 and grow at a CAGR of 18.76% to reach USD 4.77 billion by 2030.

What is the current RF GaN Market size?

In 2025, the RF GaN Market size is expected to reach USD 2.02 billion.

Who are the key players in RF GaN Market?

Mitsubishi Electric Corporation, STMicroelectronics NV, Qorvo Inc., Analog Devices Inc. and Raytheon Technologies are the major companies operating in the RF GaN Market.

Which is the fastest growing region in RF GaN Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in RF GaN Market?

In 2025, the North America accounts for the largest market share in RF GaN Market.

What years does this RF GaN Market cover, and what was the market size in 2024?

In 2024, the RF GaN Market size was estimated at USD 1.64 billion. The report covers the RF GaN Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the RF GaN Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

RF GaN Market Research

Mordor Intelligence provides a comprehensive analysis of the RF GaN industry. We leverage our extensive expertise in both RF semiconductor and GaN semiconductor research. Our detailed report examines the evolution of RF power amplifier technology. This includes advances in GaN on SiC as well as GaN on silicon implementations. The analysis covers crucial developments in RF component manufacturing, RF electronics integration, and RF transistor innovations. We pay particular attention to RF integrated circuit applications and microwave semiconductor technologies.

Stakeholders gain valuable insights through our downloadable report PDF. It details the latest developments in GaN power device technology and GaN transistor applications. The research encompasses RF power transistor developments and GaN power amplifier innovations. It also covers emerging 5G RF semiconductor technologies. Our analysis explores the RF power semiconductor landscape, examining GaN power electronics applications across various sectors. The report provides comprehensive coverage of RF component evolution and GaN RF device implementations. It offers stakeholders actionable intelligence for strategic decision-making in the rapidly evolving RF semiconductor industry.