Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

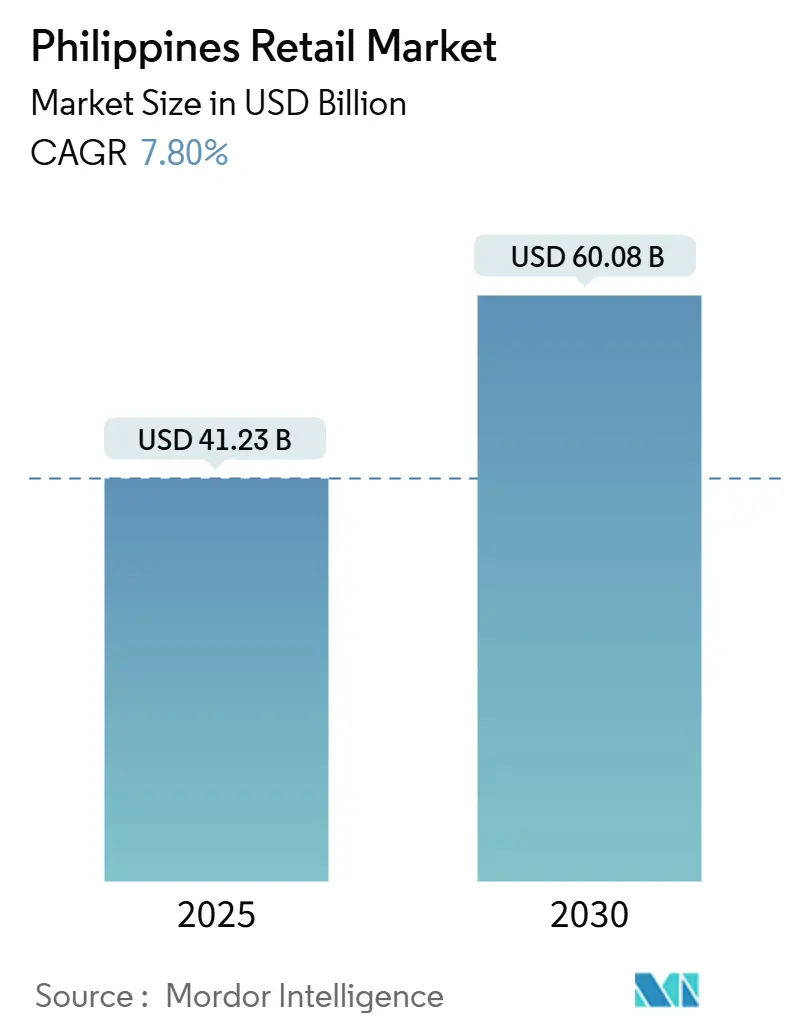

| Market Size (2025) | USD 41.23 Billion |

| Market Size (2030) | USD 60.08 Billion |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Philippines Retail Market Analysis by Mordor Intelligence

The Philippines retail market reached USD 41.23 billion in 2025 and is forecast to advance to USD 60.08 billion by 2030, reflecting a sturdy 7.8% CAGR. Digital transformation, a rising middle-income segment, and steady remittance inflows underpin this trajectory. Household spending is rising from 5.0% in 2024 to 5.3% in 2025 as disposable incomes climb, encouraging retailers to broaden assortments and upgrade store formats. Simultaneously, the share of retail in national output is moving from 18.6% in 2022 toward 20% by late 2024, underscoring the sector’s growing macroeconomic weight. Rapid e-commerce uptake, now 52.8% of transactions, has pushed retailers to integrate mobile wallets and social shopping, while massive public-private infrastructure projects lower logistics barriers and open provincial growth corridors.

Key Report Takeaways

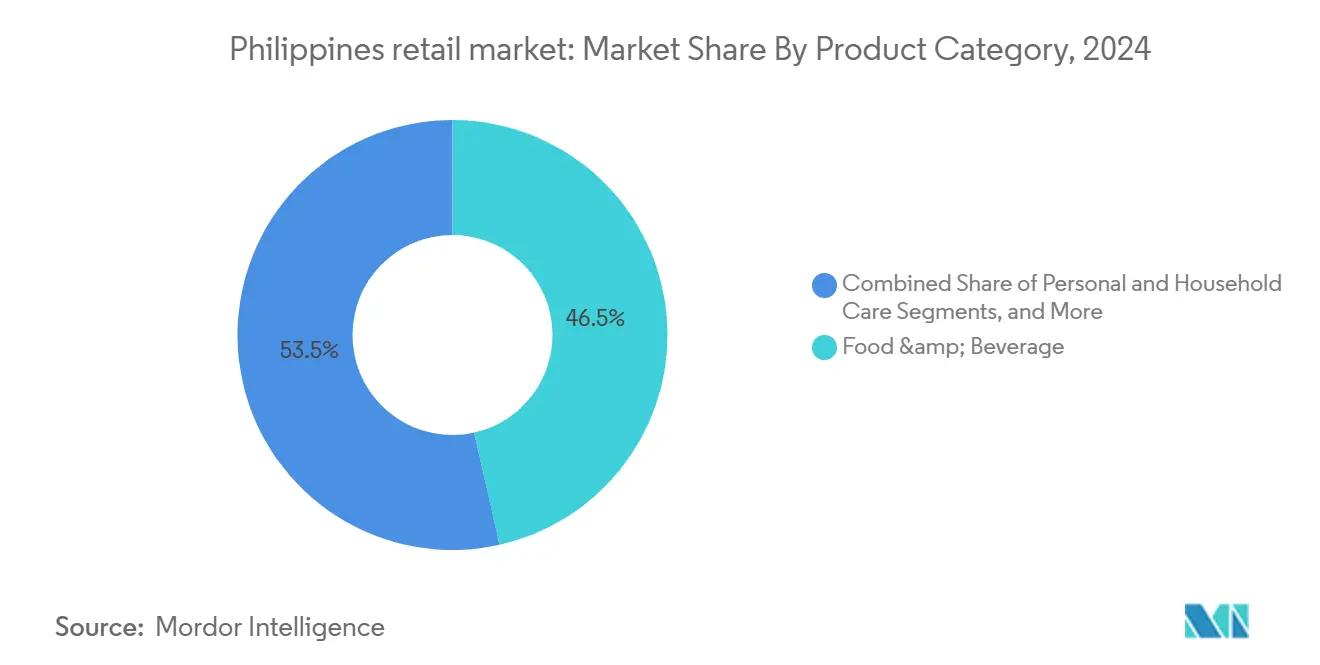

• By product category, food and beverage held 46.52% of the Philippines' retail market share in 2024; cosmetics and personal care are projected to grow at a 10.2% CAGR through 2030.

• By distribution channel, supermarkets/hypermarkets accounted for 38.56% of the Philippines' retail market share in 2024, whereas online channels are poised to expand at a 9.56% CAGR to 2030.

• By retail format, traditional trade captured 56.69% of the Philippines' retail market size in 2024, while omnichannel and dark stores are set to rise at an 8.88% CAGR over the forecast period.

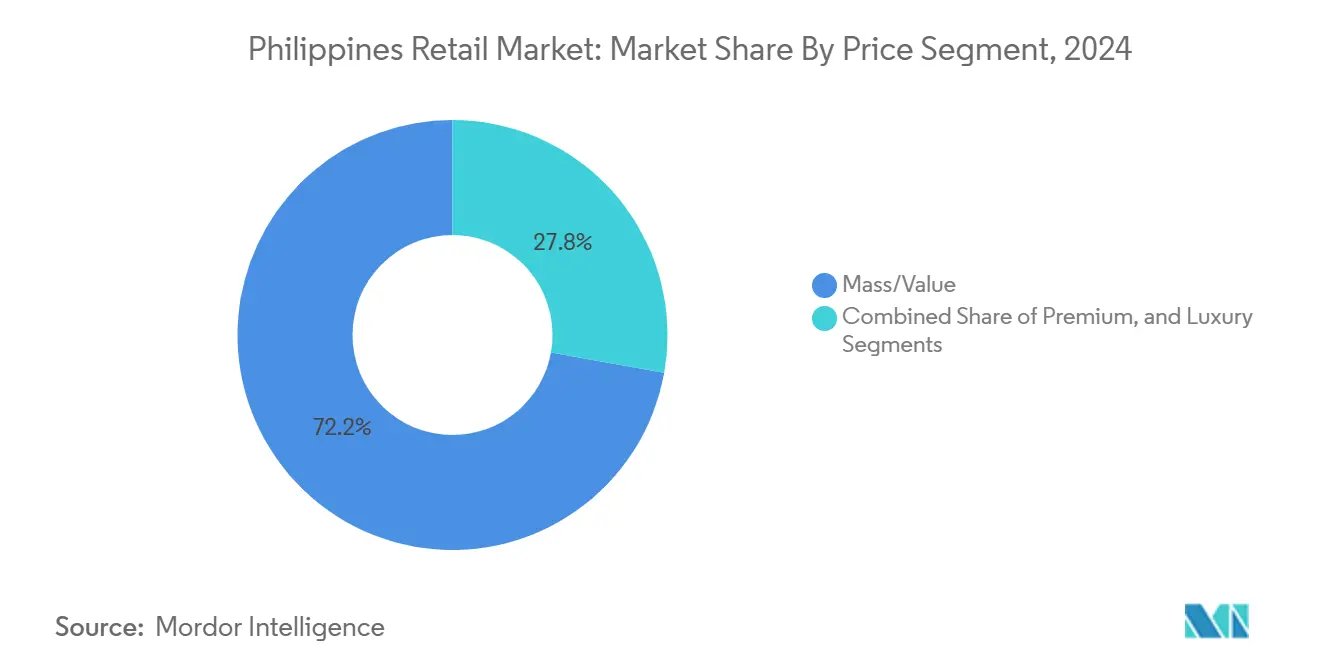

• By price segment, mass/value represented 72.21% of the Philippines' retail market size in 2024; luxury is expected to record a 12.21% CAGR up to 2030.

• By region, Luzon commanded 63.32% of the Philippines' retail market share in 2024, whereas Mindanao is forecast to register the fastest 10.45% CAGR through 2030.

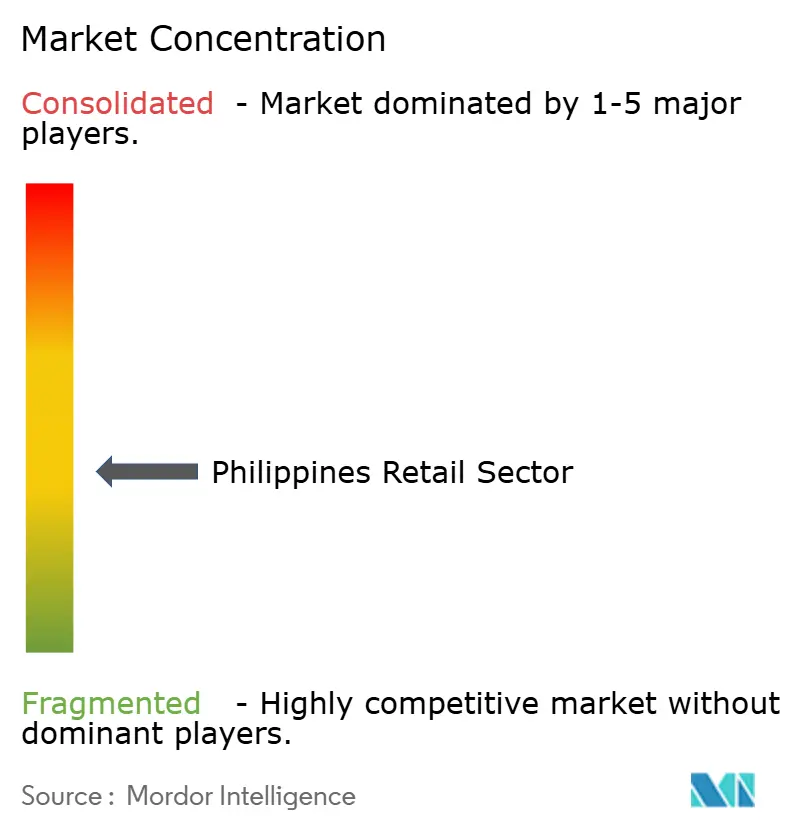

• The five leading groups—SM Investments, Robinsons Retail, Puregold Price Club, Metro Retail, and SSI—collectively hold a sizeable but not dominant slice of the Philippines' retail market.

Philippines Retail Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & expanding middle class | +2.1% | National, with early gains in Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Accelerating e-commerce adoption & digital payments | +1.8% | Global, spill-over to rural areas via mobile penetration | Short term (≤ 2 years) |

| Growth of convenience-oriented F&B retailing | +1.2% | Urban centers, expanding to suburban markets | Medium term (2-4 years) |

| Government logistics infrastructure improvements | +0.9% | Luzon Economic Corridor, Visayas, Mindanao connectivity | Long term (≥ 4 years) |

| Overseas remittances fueling discretionary consumption | +0.8% | National, concentrated in remittance-receiving provinces | Short term (≤ 2 years) |

| Emergence of micro-fulfilment "dark stores" | +0.4% | Metro Manila, Cebu, expanding to tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Expanding Middle Class

Average per-capita income is expected to almost double from USD 3,541 in 2025 to USD 6,500 in 2030. This enlarges the consuming class and lifts demand for premium labels as well as modern shopping ambiances. Luxury categories are therefore growing at 12.21%—well above the Philippines retail market average. Retailers answer with wider private-label assortments, renovated store layouts, and loyalty programs that emphasize quality and experience. Department stores and specialty chains that curate global brands are seeing traffic from aspirational shoppers, while sari-sari owners leverage digital supply hubs to stock higher-margin goods.

Accelerating E-commerce Adoption and Digital Payments

Digital payments already account for 52.8% of retail transactions, overshooting the government’s 50% target two years early. Monthly electronic transfers now approach 2.62 billion, worth USD 110 billion, and mobile wallet penetration exceeds 30 million active users. Retailers consequently embed click-and-collect counters, live-stream selling and single-cart checkout across channels. Social commerce thrives as 85% of shoppers expect live selling to grow, motivating MSMEs to extend reach nationally. Broad payment choice and friction-free returns reduce cart abandonment and build trust among first-time online buyers.

Growth of Convenience-Oriented FandB Retailing

Convenience chains plan over 700 new outlets in 2025, led by 7-Eleven’s 500-store pipeline and SM Group’s 200 Alfamart launches. Time-pressed consumers prefer frequent top-up trips for fresh meals and snacks, helping FandB keep a 46.52% category share. Logistics specialists such as Ninja Van deploy micro-fulfilment “Ninja Restock” routes that let neighborhood grocers replenish multiple times weekly, protecting freshness and limiting stock-outs. Cosmetics and Personal Care, while smaller, benefits indirectly from the same quick-commerce model by surfacing trial-size beauty products alongside everyday baskets.

Government Logistics Infrastructure Improvements

The USD 600 billion Luzon Economic Corridor connects Subic, Clark, Manila, and Batangas via rail and expressways, complemented by the Subic-Clark Railway and Clark National Food Hub [1]Source: International Trade Administration, “Philippines – Logistics Infrastructure Projects,” trade.gov. . By lowering logistics costs—now 25.5% of GDP—the overhaul lets retailers extend next-day shipping to Visayas and Mindanao. The Build Better More program, with 169 PPP projects, enhances seaports, airports, and fiber lines, shrinking delivery lead times and attracting foreign brands to provincial malls.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic traffic congestion & last-mile inefficiencies | -1.4% | Metro Manila, Cebu, Davao urban centers | Short term (≤ 2 years) |

| Rising utility and operating costs for modern formats | -1.1% | National, particularly energy-intensive formats | Medium term (2-4 years) |

| Dominance of informal sari-sari stores | -0.8% | Rural and suburban markets nationwide | Long term (≥ 4 years) |

| VAT equalisation on foreign e-commerce platforms | -0.3% | National, affecting online retail competition | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Traffic Congestion and Last-Mile Inefficiencies

Gridlock in Metro Manila inflates freight costs by up to 20% versus efficient cities. Retailers must over-invest in urban depots and widen delivery windows for perishables, eroding margins. Government freight-route mapping and “no truck ban” policies aim to cut delays, yet implementation lags and businesses still adopt AI routing tools alongside motorbike fleets to skirt bottlenecks.

Rising Utility and Operating Costs for Modern Formats

Higher electricity tariffs and global fuel volatility squeeze large-format stores. Metro Retail’s PHP 230 million solar roll-out covers only 15% of consumption, indicating long payback times. Inflation also prompts 50% of consumers to switch brands for better value, forcing chains to discount more aggressively. While automation and renewable energy lower unit costs over time, smaller operators lack the capital to follow suit, widening competitive gaps.

Segment Analysis

By Product Category: Food and Beverage Reinforces Everyday Stability

Food and Beverage claimed 46.52% of the Philippines' retail market share in 2024, anchoring day-to-day traffic and buffering the sector against cyclical shocks. The Philippines' retail market size for this category benefits from robust tourism, hotel openings, and strong agricultural links with the United States. Layered onto staples, Cosmetics and Personal Care expands at a 10.2% CAGR, fueled by heightened wellness awareness and growing disposable incomes. Apparel, Electronics, and Furniture register steady single-digit gains tied to urbanization and housing upgrades, while Confectionery and Ice Cream post 8% annual growth on rising leisure spending.

Expanding middle-income wallets allow premium gourmet grocers to carve niches, yet the mass-market grocery core remains vital. Imported delicacies and plant-based offerings sit alongside local rice and canned fish, illustrating basket polarisation. Multinational brands partner with sari-sari owners for rural penetration, whereas mall-based supermarkets emphasise experiential bakery corners and dine-in counters to extend dwell time.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Modern Stores Scale, Online Rockets

Supermarkets and hypermarkets combined delivered 38.56% of Philippines retail market share in 2024, supported by Robinsons, SM Hypermarket and Savemore’s dense outlet matrix. Their bundled promotions and loyalty schemes nurture repeat traffic, yet footfall is fragmenting as consumers explore faster fulfilment choices. The online grocery segment exceeded USD 1 billion in 2023 and will likely outpace headline Philippines retail market growth with a 15% CAGR anchored in mobile wallet habituation.

Convenience chains continue to seed secondary cities, reaching commuters and students after working hours. Department and specialty stores refocus on curation, leveraging beauty consultation and pet-care services to defend margins. Dark-store platforms test 15-minute delivery in Metro Manila, showing where the next incremental dollar of Philippines retail market size could emerge.

By Retail Format: Tradition Meets Omnichannel

Traditional Trade still accounts for 56.69% of the Philippines retail market size, proving that micro-stores remain indispensable in barangays. Digitalisation projects link 175,000 sari-sari outlets to supply-chain dashboards, trimming stock-outs and aligning prices with nearby supermarkets. Meanwhile, Omnichannel and Dark Stores, posting an 8.88% CAGR, serve as the physical back-bone for pure-play e-commerce and quick-commerce operators.

Modern Trade’s mall-anchored supermarkets and department stores shift toward smaller neighbourhood concepts to keep pace with residential sprawl. Warehouse clubs and discount grocers ride on cost-of-living concerns, while pop-up kiosks inside transport hubs test impulse categories under a lean capex model.

By Price Segment: Mass Dominance with Premium Upswing

Mass/Value keeps a commanding 72.21% share of Philippines retail market size in 2024 as budget sensitivity persists. Retailers push private labels and sachet packaging, stretching pesos without sacrificing quality perceptions. Parallel to this, Luxury climbs at 12.21% CAGR thanks to higher-income city residents and returning overseas professionals. Flagship boutiques for prestige fashion, wine and specialty coffee are opening in Greenbelt and Bonifacio Global City as landlords re-tenant malls for experiential draw.

The price ladder is widening: mid-tier shoppers treat themselves to imported skincare monthly, while affluent consumers shift toward investment handbags and fine jewelry. Installment financing via Buy Now Pay Later apps bridges affordability gaps and broadens cart depths.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Store Size: Small Formats Dominate Access Point Real-Estate

Small and Micro stores below 400 m² delivered 65.55% of 2024 sales and will grow at an 11.10% CAGR through 2030, showing how proximity retail captures frequent mission shopping. Contactless top-ups, e-money cash-in and parcel pick-ups turn these spaces into community hubs. Mid-sized formats between 400 and 2,500 m² accommodate wider assortments in suburbs, whereas large-format hypermarkets concentrate in regional centres as full-day destinations featuring cinemas, clinics and co-working lounges.

Fragmented geography encourages cross-docking: wholesalers break bulk in central depots and trans-ship via motorcycle fleets to island outlets. AI inventory forecasting minimises spoilage for high-velocity SKUs such as milk and snack foods, a critical metric when power costs climb.

Geography Analysis

Luzon’s outsized role in the Philippines retail market comes not only from population density but also from its concentration of transport assets that lower inbound freight costs and make same-day delivery realistic for 60% of households. New toll roads, automated ports and cold-chain facilities create a virtuous cycle that attracts international tenants and unlocks premium mall rents. Retail footprints therefore widen beyond Metro Manila to Pampanga, Bulacan and La Union where residential estates dovetail with mixed-use centres.

Visayas follows an opportunistic pattern, building on tourism, OFW remittance flows and tighter community bonds. Metro Retail’s partnerships in Samar and Negros Occidental bring supermarket footprints to catchments where modern trade penetration had lingered below 20%. Sari-sari digitisation is particularly vibrant in Western Visayas, which recorded 62% user growth on Packworks’ platform. A hybrid ecosystem of public markets for fresh goods and air-conditioned neighbourhood stores for packaged items underlines local preference for convenience and sociability.

Mindanao’s consumer story is underpinned by agricultural incomes and mining royalties that diversify spending power. Infrastructure grants under Build Better More, including airport expansions in Davao and General Santos, shrink travel times and give brands confidence to enter. Retailers deploy hub-and-spoke distribution that stages non-perishables in Davao, forwarding weekly to satellite branches. Local entrepreneurs, often family conglomerates, co-locate supermarkets with hardware depots and pharmacies, creating one-stop retail clusters that reduce the need for lengthy city trips.

Competitive Landscape

The five leading groups—SM Investments, Robinsons Retail, Puregold Price Club, Metro Retail, and SSI—collectively hold a sizeable but not dominant slice of the Philippines' retail market. SM Investments alone earmarked PHP 100 billion (USD 1.73 billion) for 2025 capex, covering three new malls, hotel towers, and renewable projects, pushing its store tally above 4,470 outlets[2]SM Prime Holdings Investor Relations, “Investor Presentation 2025,” SM Prime Holdings, smprime.com. Robinsons Retail focuses on higher-margin formats such as pet care and drugstores while scaling private labels to protect gross margin. Metro Retail turns to public-private pacts to anchor grocery complexes in newly urbanizing towns, underscoring provincial ambitions.

Puregold accelerates warehouse-style Puregold Price Club builds in Iloilo and Davao, aligning value proposition to inflation-sensitive households. SSI leverages global brand ties, acquiring Rustan Marketing and cementing joint ventures with JD Sports and Alo Yoga to dominate premium lifestyle niches. Competitive emphasis rests on omnichannel tech, renewable power adoption, and rural network roll-out. Emerging tech firms like Packworks and Growsari integrate micro-fulfilment algorithms into 1.3 million sari-sari stores, offering established chains a turnkey last-mile grid. Foreign entrants such as Nitori and DALI inject fresh concept formats, further elevating competitive intensity.

Strategic playbooks now pair loyalty super-apps with fulfilment nodes to secure consumer stickiness. Cash-back wallets, grocery subscriptions and in-app financing keep value seekers engaged, while luxury counters host personal stylists and immersive VR showcases. Retailers that orchestrate inventory transparency across bricks and clicks, and who tilt energy mix toward solar, stand to compress cost-to-serve and fund expansion.

Philippines Retail Industry Leaders

-

SM Investments Corp. (SM Retail)

-

Robinsons Retail Holdings Inc

-

Puregold Price Club Inc

-

Metro Retail Stores Group Inc.

-

SSI Group Philippines

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: SSI Group completed a 99.44% acquisition of Rustan Marketing Corp. for PHP 232 million, expanding access to 1,300 wholesale doors while adding seven fresh luxury brands for 2025.

- February 2025: Philippine Seven Corp. set aside PHP 5 billion to open 400+ new 7-Eleven stores, targeting white-space in Luzon, Visayas, and Mindanao.

- February 2025: SM Prime Holdings Incorporated is investing P100 billion in 2025, with around a fifth of its capital expenditures going to three new malls that are opening this year and the renovation of some existing mall spaces.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Philippines retail market as the full value of consumer goods that reach households through modern formats such as supermarkets, convenience stores, department stores, specialty chains, pure-play e-commerce sites, and the still-dominant sari-sari and wet markets. We count each sale at its final ticket price in pesos and convert it to U S dollars using the yearly average rate.

Scope Exclusion: wholesale trade, duty-free shops serving tourists, and offshore e-commerce orders fulfilled outside the country are not included.

Segmentation Overview

- By Product Category

- Food and Beverage

- Personal and Household Care

- Apparel

- Footwear and Accessories

- Furniture

- Toys and Hobbies

- Electronics and Household Appliances

- Other Products

- By Distribution Channel

- Supermarkets / Hypermarkets

- Convenience Stores

- Department Stores

- Specialty Stores

- Online

- Other Channels

- By Retail Format

- Modern Trade

- Traditional Trade

- Discount Stores and Warehouse Clubs

- Omnichannel and Dark Stores

- By Price Segment

- Mass / Value

- Premium

- Luxury

- By Store Size

- Large-Format (Greater than 2,500 m²)

- Mid-Format (400-2,500 m²)

- Small / Micro (Less than 400 m²)

- By Region

- Luzon

- Visayas

- Mindanao

Detailed Research Methodology and Data Validation

Primary Research

We interview store managers across Luzon and Visayas, FMCG distributors, mall developers, fintech payment executives, and logistics providers. Their insights refine average selling prices, the modern-trade share shift, and emerging online basket sizes.

Desk Research

Mordor analysts first build a demand stack from the Philippine Statistics Authority's spending surveys, Bangko Sentral household tables, Department of Trade and Industry registrations, and UN Comtrade import codes tied to consumer goods. Company filings, investor decks, and press archives accessed through Dow Jones Factiva and D&B Hoovers clarify channel turnover and pricing. White papers from the Philippine Retailers Association and ASEAN retail forums help us gauge informal volumes and inflation. The sources named are illustrative; many others underpin validation.

Market-Sizing & Forecasting

A top-down model starts with national retail turnover and splits it into product and channel pools using production data, import flows, and shopper-penetration surveys. Select bottom-up checks, rolling up listed chain revenues and estimating online gross merchandise value from payment volumes, test totals. Key drivers include real disposable income, inflation-adjusted ASPs, e-wallet penetration, new gross leasable area, and mandated wage hikes. Multivariate regression projects each driver while scenario analysis gauges shocks such as typhoons or supply disruptions; proxy ratios from comparable ASEAN markets bridge any residual gaps.

Data Validation & Update Cycle

Outputs pass dual peer reviews and variance scans against indicators like power use and freight flows. Reports refresh annually, with mid-cycle updates triggered by major policy moves or price spikes, ensuring clients receive our latest view.

Why Mordor's Philippines Retail Sector Baseline Earns Trust

Published estimates often diverge because firms vary channel scope, inflation handling, and refresh cadence. Our team shares model inputs openly, letting users trace every peso back to a public series or interview note.

Key gap drivers elsewhere include mixing wholesale with retail sales, applying blanket growth to informal outlets, or fixing peso-to-dollar rates at a single point in time. We isolate each variable first, then apply the average exchange rate for the base year, delivering a stable yet transparent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 41.23 B (2025) | Mordor Intelligence | - |

| USD 69.42 B (2024) | Global Consultancy A | Includes wholesale and duty-free sales; older base year; unclear FX method |

| USD 45.62 B (2024) | Regional Consultancy B | Omits informal trade; uniform price-rise assumption |

These comparisons show that Mordor's disciplined scope selection, driver-level modeling, and timely refresh supply a balanced, transparent baseline that decision-makers can rely on.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Philippines retail market?

The Philippines retail market size reached USD 41.23 billion in 2025 and is projected to climb to USD 60.08 billion by 2030 at a 7.8% CAGR.

Which product category leads Philippine retail sales?

Food and beverage leads with 46.52% market share thanks to everyday necessity status and strong tourism-linked consumption.

How fast is e-commerce growing relative to physical stores?

Online retail is advancing at a 9.56% CAGR—faster than the overall 7.8% market rate—as digital payments now account for more than half of transactions.

Why do sari-sari stores remain relevant?

About 1.3 million sari-sari outlets maintain deep community ties, flexible credit and proximity convenience, keeping Traditional Trade at 56.69% of market sales.

Which region will deliver the strongest retail growth through 2030?

Mindanao is forecast to record a 10.45% CAGR, leveraging new rail, airport and road projects that improve connectivity and stimulate local spending.

Page last updated on: