| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 6.02 Billion |

| Market Size (2030) | USD 7.24 Billion |

| CAGR (2025 - 2030) | 3.77 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Respiratory Disease Testing Market Analysis

The Global Respiratory Disease Testing Market size is estimated at USD 6.02 billion in 2025, and is expected to reach USD 7.24 billion by 2030, at a CAGR of 3.77% during the forecast period (2025-2030).

The respiratory disease testing landscape is experiencing significant transformation driven by the increasing integration of advanced diagnostic technologies into routine clinical practice. Healthcare facilities worldwide are adopting multiplexed testing approaches that enable simultaneous detection of multiple respiratory pathogens from a single sample, improving diagnostic efficiency and patient care outcomes. This shift is particularly evident in the emergence of sophisticated molecular diagnostic platforms that offer rapid results while maintaining high sensitivity and specificity. For instance, recent developments in 2023 have seen the introduction of advanced testing platforms capable of detecting multiple respiratory pathogens within 15-30 minutes, significantly reducing the time-to-diagnosis compared to traditional methods.

The industry is witnessing a notable trend toward the decentralization of testing services, with a growing emphasis on point-of-care testing solutions. This transformation is reshaping how respiratory diagnostics market services are delivered, making them more accessible to patients in various healthcare settings, including primary care clinics and urgent care centers. Healthcare providers are increasingly adopting rapid diagnostic tests that can be performed outside traditional laboratory settings, enabling faster clinical decision-making and more timely patient care. According to recent industry data, diagnostic laboratories reported a significant increase in the adoption of point-of-care molecular diagnostic tests for respiratory diseases in 2023.

Standardization and quality assurance in respiratory disease testing have become paramount, with healthcare organizations implementing more rigorous protocols to ensure accurate and reliable test results. This focus on quality has led to the development of new guidelines and standards for respiratory disease testing, particularly in molecular diagnostics. Industry stakeholders are collaborating to establish standardized testing protocols and quality metrics, ensuring consistency across different healthcare settings and geographical regions. These efforts are complemented by initiatives to improve the interoperability of diagnostic platforms and data management systems.

The market is experiencing a shift toward personalized diagnostic approaches, with healthcare providers increasingly utilizing advanced analytics and artificial intelligence to interpret test results and guide treatment decisions. This trend is supported by the growing integration of digital health technologies and laboratory information systems, enabling better data management and analysis. Recent innovations include the development of AI-powered diagnostic algorithms that can help identify patterns and predict disease progression based on test results. These technological advancements are enhancing the precision and efficiency of respiratory disease testing while potentially reducing healthcare costs through more targeted testing approaches.

Respiratory Disease Testing Market Trends

Growing Burden of Respiratory Diseases

The increasing prevalence of respiratory disorders, including influenza, the common cold, and pneumonia, has created significant demand for respiratory disease testing globally. The identification of causative pathogens is crucial for selecting appropriate treatments, saving lives, stopping epidemics, and avoiding unnecessary antibiotic use. According to the Centers for Disease Control and Prevention's May 2023 update, nearly 27 million infections and 290,000 hospitalizations were reported in the United States due to influenza, highlighting the substantial burden of respiratory diseases. Additionally, pneumonia remains one of the most prevalent respiratory diseases in the Asia-Pacific region, with UNICEF reporting in December 2022 that the estimated annual incidence of pneumonia in the South Asia region is 2,500 per 100,000 children, significantly higher than the global average of 1,400.

The severity and frequency of respiratory syncytial virus (RSV) infections have also increased substantially in recent years. According to research published by the National Center for Biotechnology Information in December 2022, Germany experienced an extremely high burden of out-of-season RSV cases in 2021-2022, with 67 reporting hospitals recording an average of 471 hospitalized pediatric RSV cases per day. Furthermore, recurrent respiratory infections (RRIs) affect approximately 25% of children under one year of age and 6% of children during their first six years of life, as reported by the Italian Journal of Pediatrics in October 2021. This increasing disease burden has created a pressing need for accurate and timely diagnostic solutions, driving the demand for respiratory infection testing products and services.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements

The transformation in respiratory disease testing technology has led to significant improvements in diagnostic capabilities, particularly with the advent of syndromic multiplex PCR panels that allow laboratories to rapidly provide highly sensitive and specific test results for a wide range of pathogens with a single test. For instance, the QIAstat-Dx syndromic testing solution connects to the QIAsphere cloud-based platform, enabling fast and accurate syndromic testing while providing remote monitoring of instruments and test status, allowing customers to receive push notifications on their personal devices. Similarly, the NxTAG Respiratory Pathogen Panel, developed by DiaSorin (Luminex Corporation), represents next-generation technology that enables the simultaneous detection of 20 respiratory pathogens, accommodating higher throughput requirements with scalable throughput of 1-96 samples at a time.

Recent technological innovations have also focused on improving the accessibility and efficiency of testing procedures. In May 2023, Hologic received FDA 501(k) approval for its Panther Fusion SARS-CoV-2/Flu A/B/RSV assay with the new RespDirect collection kit, which enables laboratories to directly load samples for processing without any uncapping or specimen transfer steps, saving time and lowering the risk of error and repetitive stress injuries. Additionally, the development of rapid diagnostic tests has benefited target populations by providing better diagnostics in limited time and resource settings. These tests can be carried out without sophisticated laboratories, making them particularly beneficial in low-and-middle-income countries with less sophisticated diagnostic centers, while maintaining high sensitivity and specificity standards. The advancements in respiratory pathogen testing kits have significantly contributed to the growth of the respiratory panel assays market, enhancing the ability to quickly and accurately diagnose a wide array of respiratory infections.

Segment Analysis: By Technology

Nucleic Acid-Based Tests Segment in Respiratory Disease Testing Market

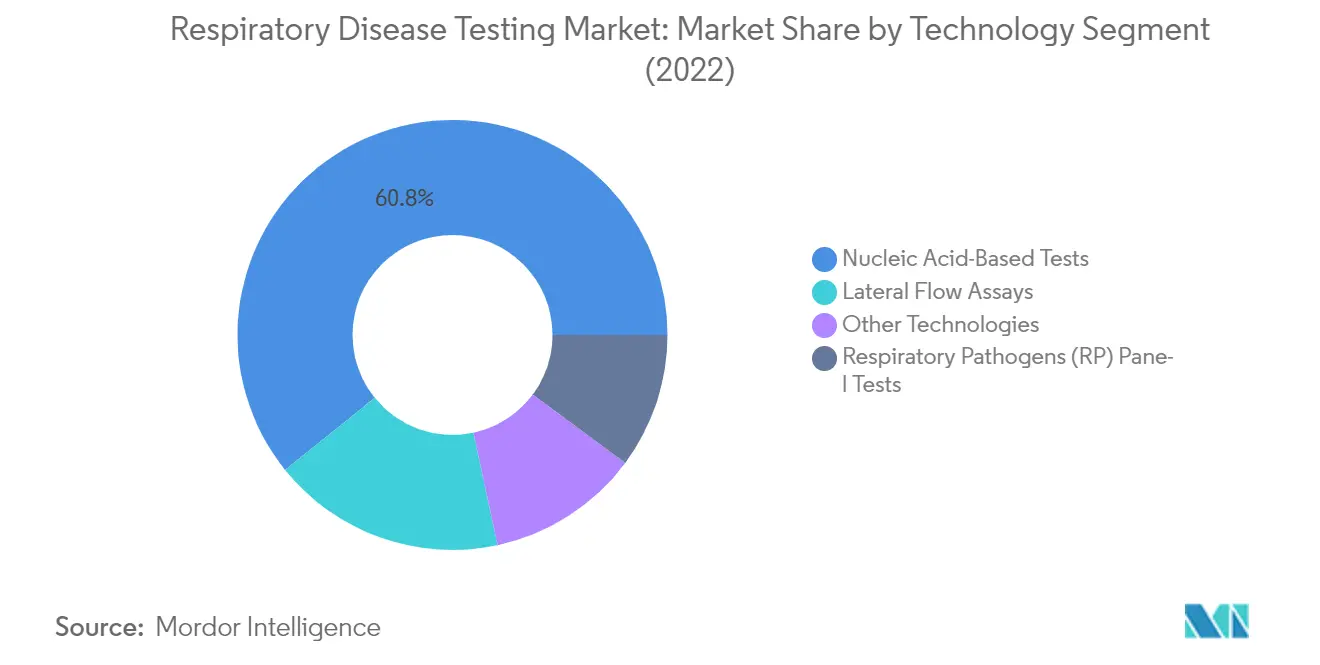

The Nucleic Acid-Based Tests segment dominates the respiratory disease testing market, commanding approximately 61% of the market share in 2024. This significant market position is attributed to the segment's high sensitivity and specificity in detecting respiratory pathogens. The segment's leadership is reinforced by continuous technological advancements in PCR and LAMP-based testing methods, enabling rapid and accurate detection of multiple respiratory pathogens simultaneously. Healthcare providers increasingly prefer nucleic acid-based tests for their ability to detect emerging variants and provide quantitative results, particularly in cases requiring precise viral load measurements. The segment's prominence is further supported by its widespread adoption in both clinical laboratories and point-of-care settings, along with its capability to detect a broad spectrum of respiratory pathogens including influenza, RSV, and other respiratory viruses.

Respiratory Pathogens (RP) Panel Tests Segment in Respiratory Disease Testing Market

The Respiratory Pathogens (RP) Panel Tests segment is emerging as the most resilient segment in the respiratory disease testing market, projected to experience the most favorable growth trajectory from 2024 to 2029. This segment's growth is driven by the increasing demand for comprehensive diagnostic solutions that can simultaneously detect multiple respiratory pathogens in a single test. Healthcare facilities are increasingly adopting RP panel tests due to their ability to provide rapid and accurate identification of various respiratory pathogens, enabling more efficient patient management and treatment decisions. The segment's growth is further supported by ongoing innovations in multiplexing technologies, improved automation capabilities, and the rising need for rapid syndromic testing approaches in clinical settings. The development of more sophisticated and user-friendly RP panel platforms continues to enhance their adoption across various healthcare settings.

Remaining Segments in Technology

The Lateral Flow Assays and Other Technologies segments continue to play vital roles in the respiratory disease testing market. Lateral Flow Assays maintain their significance due to their cost-effectiveness, ease of use, and rapid results, making them particularly valuable in resource-limited settings and point-of-care applications. The Other Technologies segment, which includes various emerging and specialized testing methodologies, contributes to market diversity by offering alternative approaches to respiratory pathogen testing kits. These segments collectively enhance the market's ability to meet diverse testing needs across different healthcare settings, from sophisticated laboratory environments to primary care facilities, ensuring comprehensive coverage of respiratory disease diagnostics requirements.

Segment Analysis: By End User

Hospitals and Clinics Segment in Respiratory Disease Testing Market

The hospitals and clinics segment dominates the respiratory disease testing market, commanding approximately 58% of the total market share in 2024. This significant market position is attributed to hospitals and clinics being the primary healthcare facilities equipped with advanced infrastructure and staffed by medical professionals to conduct a wide array of respiratory infection testing. The segment's dominance is further strengthened by increasing awareness programs and the establishment of new hospitals globally. For instance, specialized respiratory departments and institutes are being established in various regions to handle the growing burden of respiratory diseases. Additionally, hospitals and clinics offer vital services for diagnosing and treating respiratory conditions through regular check-ups and screenings for high-risk individuals, enabling early detection and prevention efforts.

Diagnostic Laboratories Segment in Respiratory Disease Testing Market

The diagnostic laboratories segment is projected to demonstrate the strongest growth trajectory in the respiratory disease testing market from 2024 to 2029. This growth is driven by the increasing adoption of advanced diagnostic technologies and the rising demand for specialized testing services. Diagnostic laboratories differ from hospitals and clinics as they are specialized facilities solely focused on laboratory testing and analysis, offering high-throughput testing capabilities and expertise in handling complex diagnostic procedures. The segment's growth is further supported by strategic agreements and product launches, such as the recent development of combination testing capabilities that can detect multiple respiratory viruses from a single patient sample. These laboratories are also at the forefront of implementing new technologies and automated solutions, improving testing efficiency and accuracy while reducing turnaround times.

Remaining Segments in End User Market

The other end users segment, which includes research institutes and long-term care facilities such as residential and nursing homes, plays a crucial role in the respiratory disease testing market. Research institutes contribute significantly to studying respiratory diseases and developing new testing methods, while residential care facilities implement regular testing protocols as part of their infection control measures. These facilities are particularly important for monitoring vulnerable populations and conducting epidemiological studies. The segment's impact is enhanced by increasing initiatives such as product launches and favorable regulations mandating disease testing in various healthcare settings, contributing to the overall market dynamics and innovation in respiratory disease testing methodologies.

Segment Analysis: By Indication

COVID-19 Segment in Respiratory Disease Testing Market

The COVID-19 segment continues to dominate the respiratory disease testing market, holding approximately 80% market share in 2024. This significant market position is maintained due to the ongoing need for COVID-19 testing across healthcare facilities worldwide, particularly with the emergence of new variants requiring continuous monitoring and surveillance. The segment's dominance is further strengthened by the widespread availability of various testing methods, including PCR-based tests, rapid antigen tests, and multiplex assays that can simultaneously detect COVID-19 along with other respiratory pathogens. Healthcare providers and diagnostic laboratories have maintained robust testing infrastructure developed during the pandemic, contributing to the segment's substantial market presence. Additionally, many corporate centers and industrial complexes continue to implement mandatory COVID-19 testing protocols, while healthcare facilities maintain testing requirements for patient screening and management.

Common Cold Segment in Respiratory Disease Testing Market

The common cold segment is emerging as the fastest-growing segment in the respiratory disease testing market, with a projected growth rate of approximately 8% during 2024-2029. This remarkable growth is driven by increasing awareness about early diagnosis and the importance of differentiating common cold symptoms from other respiratory infections. Healthcare providers are increasingly adopting advanced diagnostic solutions that can accurately identify various viral pathogens responsible for common cold symptoms. The segment's growth is further supported by the development of multiplex testing platforms that can simultaneously detect multiple respiratory pathogens, including rhinoviruses and coronaviruses commonly associated with colds. The rising demand for rapid and accurate diagnostic tests in primary care settings, coupled with increasing patient awareness about the importance of proper diagnosis for appropriate treatment selection, continues to drive innovation and adoption in this segment.

Remaining Segments in Respiratory Disease Testing Market

The respiratory disease testing market encompasses several other significant segments including influenza, respiratory syncytial virus (RSV), pneumonia, and other respiratory infections. The influenza segment maintains a strong presence due to seasonal testing requirements and the need for rapid diagnosis during flu seasons. The RSV segment is gaining importance, particularly in pediatric care settings, where early detection is crucial for proper patient management. The pneumonia testing segment continues to be vital in both hospital and clinical settings, driven by the need for pathogen identification and appropriate treatment selection. These segments collectively contribute to the market's diversity and comprehensive coverage of respiratory disease diagnostics, with each addressing specific clinical needs and patient populations. The continued development of advanced diagnostic technologies and increasing healthcare awareness further supports the growth and evolution of these segments.

Global Respiratory Disease Testing Market Geography Segment Analysis

Respiratory Disease Testing Market in North America

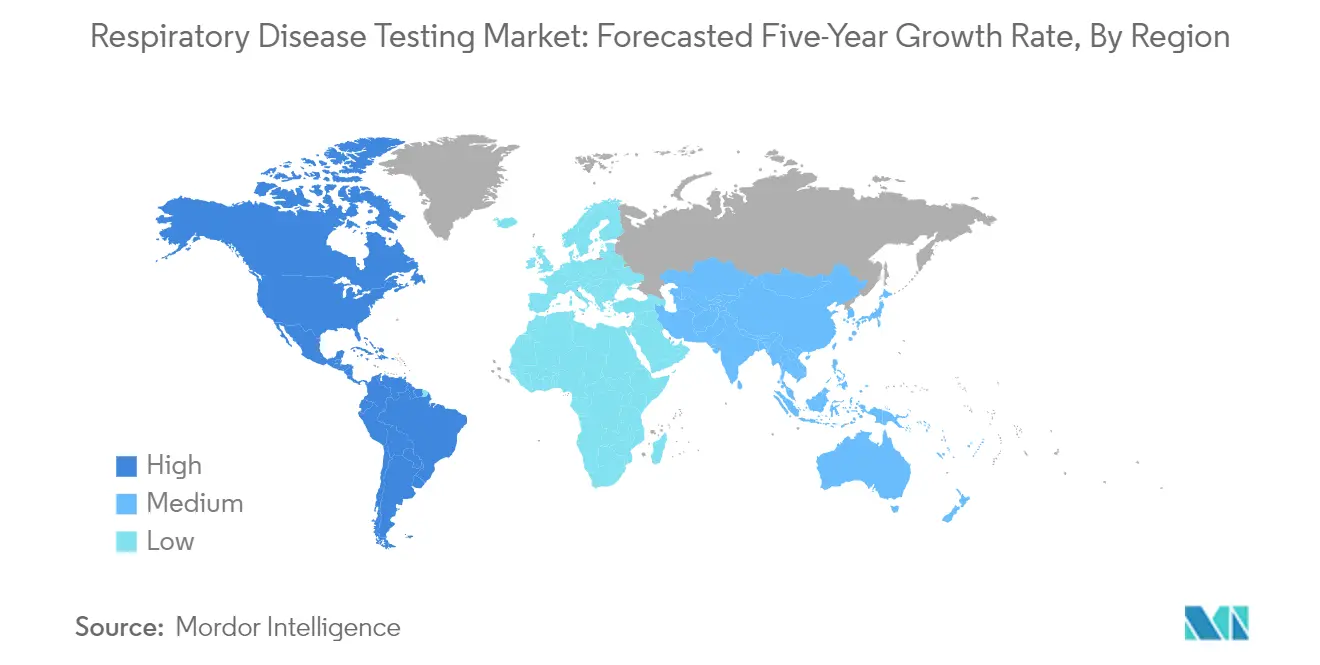

North America represents a significant respiratory disease testing market, driven by advanced healthcare infrastructure, high awareness levels, and substantial investment in diagnostic technologies. The region benefits from well-established reimbursement policies and a strong presence of major market players. The United States, Canada, and Mexico each contribute to the market's dynamics, with varying levels of healthcare accessibility and disease burden. The region's market is characterized by the rapid adoption of new testing technologies and a robust regulatory framework that ensures quality standards in respiratory disease testing.

Respiratory Disease Testing Market in the United States

The United States dominates the North American respiratory diagnostics market, holding approximately 89% of the regional market share. The country's market leadership is supported by its extensive healthcare network, high healthcare expenditure, and strong presence of major diagnostic companies. The Centers for Disease Control and Prevention (CDC) plays a crucial role in disease surveillance and testing guidelines, particularly for influenza and other respiratory infections. The country's robust healthcare infrastructure, including numerous diagnostic laboratories and healthcare facilities, enables widespread access to respiratory disease testing services. The market is further driven by the high prevalence of respiratory diseases and continuous technological advancements in testing methodologies.

Respiratory Disease Testing Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 2% during 2024-2029. The country's growth is driven by its universal healthcare system and increasing focus on preventive healthcare measures. The Public Health Agency of Canada (PHAC) actively monitors respiratory diseases through various surveillance programs, contributing to a systematic approach in disease testing. Canadian healthcare policies emphasize early detection and management of respiratory conditions, supported by well-established laboratory networks across provinces. The country's market is characterized by strong public-private partnerships in healthcare delivery and a growing emphasis on point-of-care testing solutions within the respiratory diagnostic market.

Get Analysis on Important Geographic Markets

Download PDF

Respiratory Disease Testing Industry Overview

Top Companies in Global Respiratory Disease Testing Market

The respiratory disease testing market features prominent players like Abbott, Becton Dickinson, Thermo Fisher Scientific, and Siemens Healthineers leading the competitive landscape. These companies are heavily investing in expanding their product portfolios through continuous innovation in molecular diagnostics and rapid testing technologies. Strategic collaborations with healthcare providers and research institutions have become increasingly common to enhance market presence and technological capabilities. Companies are focusing on developing automated, high-throughput testing solutions while simultaneously expanding their point-of-care testing offerings to meet diverse healthcare needs. Geographic expansion, particularly in emerging markets, remains a key growth strategy, with companies establishing local manufacturing facilities and strengthening distribution networks. The industry has seen significant investment in digital integration and connectivity solutions, enabling better data management and improved testing efficiency.

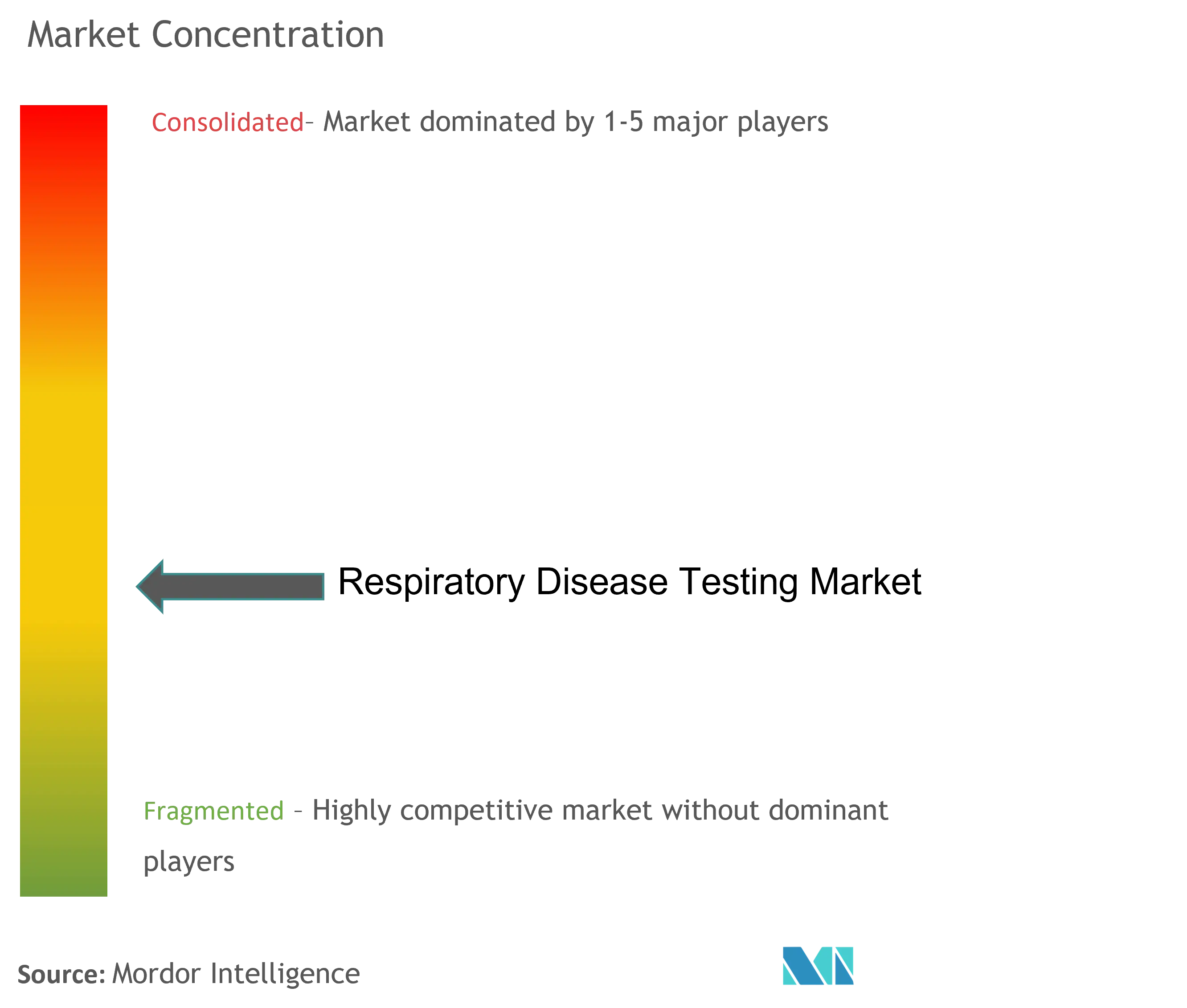

Consolidated Market with Strong Regional Players

The respiratory diagnostics market exhibits a relatively consolidated structure, dominated by large multinational corporations with diverse healthcare portfolios. These major players leverage their extensive research capabilities, established distribution networks, and strong financial positions to maintain market leadership. Regional players maintain a significant presence in specific geographies through specialized product offerings and a deep understanding of local healthcare systems. The market has witnessed strategic acquisitions aimed at expanding technological capabilities and geographic reach, with larger companies acquiring innovative startups and regional players to strengthen their market position. The competitive dynamics are further shaped by the presence of specialized diagnostic companies focusing exclusively on respiratory disease testing solutions, bringing targeted innovations to specific market segments.

The industry landscape is characterized by high entry barriers due to stringent regulatory requirements and substantial investment needs in research and development. Companies with established manufacturing capabilities and regulatory expertise hold significant advantages in navigating complex approval processes and maintaining quality standards. The market has seen increasing collaboration between diagnostic companies and healthcare providers, creating integrated testing solutions and establishing long-term partnerships. Local manufacturing initiatives and customized product development for specific markets have become crucial strategies for both global and regional players to maintain competitive advantages and market share.

Innovation and Adaptability Drive Market Success

Success in the respiratory disease testing market increasingly depends on companies' ability to develop innovative, cost-effective solutions while maintaining high accuracy and reliability standards. Market leaders are focusing on expanding their automated testing platforms, reducing turnaround times, and improving ease of use to address healthcare provider needs. The ability to offer comprehensive testing solutions, including both high-throughput laboratory systems and point-of-care devices, has become crucial for maintaining market position. Companies are also investing in building strong relationships with healthcare institutions and laboratories through enhanced service offerings, technical support, and customized solutions. The development of multiplexed testing capabilities and integration with digital health platforms has emerged as a key differentiator in the competitive landscape.

Future success in the market will require companies to demonstrate agility in responding to evolving healthcare needs and regulatory requirements. Manufacturers must balance the development of sophisticated testing platforms with the need for accessible, affordable solutions suitable for various healthcare settings. The ability to maintain strong quality control systems while scaling production capabilities will remain crucial for market success. Companies must also focus on building robust supply chains and distribution networks to ensure reliable product availability across markets. The increasing focus on preventive healthcare and regular monitoring creates opportunities for companies to develop innovative screening solutions and establish stronger positions in emerging market segments. Regulatory compliance and quality assurance will continue to be critical factors in maintaining market position and building customer trust.

Respiratory Disease Testing Market Leaders

-

Thermo Fisher Scientific

-

Abbott Laboratories

-

QIAGEN

-

Seimens Healthineers AG

-

Beckton Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Respiratory Disease Testing Market News

- January 2022: Highmark Health and Bosch entered into a research partnership to explore using innovative sensor technology and artificial intelligence (AI) to detect pediatric pulmonary conditions, such as asthma. The collaboration builds upon an age-old practice in healthcare.

- May 2022: QuantuMDx Group Limited, a UK-based developer of transformational point-of-care diagnostics, launched its new respiratory panel test Q-POC SARS-CoV-2, Flu A/B & RSV Assay. With the launch of the Q-POC respiratory panel test, the company is expanding its multiplex capabilities and providing customers with rapid, point-of-care testing.

Respiratory Disease Testing Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Growing Burden of Respiratory Diseases

- 4.2.2 Technological Advancements

-

4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework

-

4.4 Porter Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Test Type

- 5.1.1 Imaging Tests

- 5.1.2 Mechanical Tests

- 5.1.3 In-vitro Diagnostic Tests

-

5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Diagnostic Centres

- 5.2.3 Others

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Beckton Dickinson and Company

- 6.1.2 Koninklijke Philips N.V.

- 6.1.3 ResMed Inc.

- 6.1.4 Medtronic

- 6.1.5 Carestream Health

- 6.1.6 MG Diagnostic Corporation

- 6.1.7 Abbott

- 6.1.8 ThermoFisher Scientific

- 6.1.9 Biomerieux

- 6.1.10 QIAGEN

- 6.1.11 Seimens Healthineers AG

- 6.1.12 F. Hoffmann-La Roche Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Respiratory Disease Testing Industry Segmentation

As per the scope of the report, respiratory disease testing is used for the diagnosis of respiratory conditions in an individual. Some respiratory diseases include chronic obstructive pulmonary disease, asthma, and infections such as bacterial pneumonia and enterovirus respiratory virus. The respiratory disease testing market is segmented by Test Type (Imaging Tests, Mechanical Tests, and In-vitro Diagnostic Tests), End-user (Hospitals, Diagnostic Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Test Type | Imaging Tests | ||

| Mechanical Tests | |||

| In-vitro Diagnostic Tests | |||

| By End User | Hospitals | ||

| Diagnostic Centres | |||

| Others | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle-East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Respiratory Disease Testing Market Research FAQs

How big is the Global Respiratory Disease Testing Market?

The Global Respiratory Disease Testing Market size is expected to reach USD 6.02 billion in 2025 and grow at a CAGR of 3.77% to reach USD 7.24 billion by 2030.

What is the current Global Respiratory Disease Testing Market size?

In 2025, the Global Respiratory Disease Testing Market size is expected to reach USD 6.02 billion.

Who are the key players in Global Respiratory Disease Testing Market?

Thermo Fisher Scientific, Abbott Laboratories, QIAGEN, Seimens Healthineers AG and Beckton Dickinson and Company are the major companies operating in the Global Respiratory Disease Testing Market.

Which is the fastest growing region in Global Respiratory Disease Testing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Respiratory Disease Testing Market?

In 2025, the North America accounts for the largest market share in Global Respiratory Disease Testing Market.

What years does this Global Respiratory Disease Testing Market cover, and what was the market size in 2024?

In 2024, the Global Respiratory Disease Testing Market size was estimated at USD 5.79 billion. The report covers the Global Respiratory Disease Testing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Respiratory Disease Testing Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Global Respiratory Disease Testing Market Research

Mordor Intelligence delivers a comprehensive analysis of the respiratory disease testing market. We leverage our extensive experience in healthcare industry research to provide detailed insights into respiratory diagnostics technologies. These include lung function tests and respiratory infection testing methodologies. The report thoroughly examines respiratory pathogen testing kits, preclinical respiration and inhalation lab equipment, and advanced solutions for chronic pulmonary infections. This ensures stakeholders receive actionable intelligence about this evolving sector.

This detailed report, available as an easy-to-download PDF, offers valuable insights into respiratory disease testing trends and technological advancements in respiratory analyzer systems. Our analysis covers crucial aspects of lung function testers and respiratory panel assays. We also examine developments in breath molecular diagnosis technologies. Stakeholders benefit from our thorough examination of respiratory infections patterns across regions. This includes a specific focus on North America respiratory device procedures and emerging solutions for human respiratory disease treatment. The report provides essential data about PCR for respiratory infection diagnostic methods and the latest innovations in respiratory viruses tests. This enables informed decision-making for industry participants.