Resins In Paints And Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

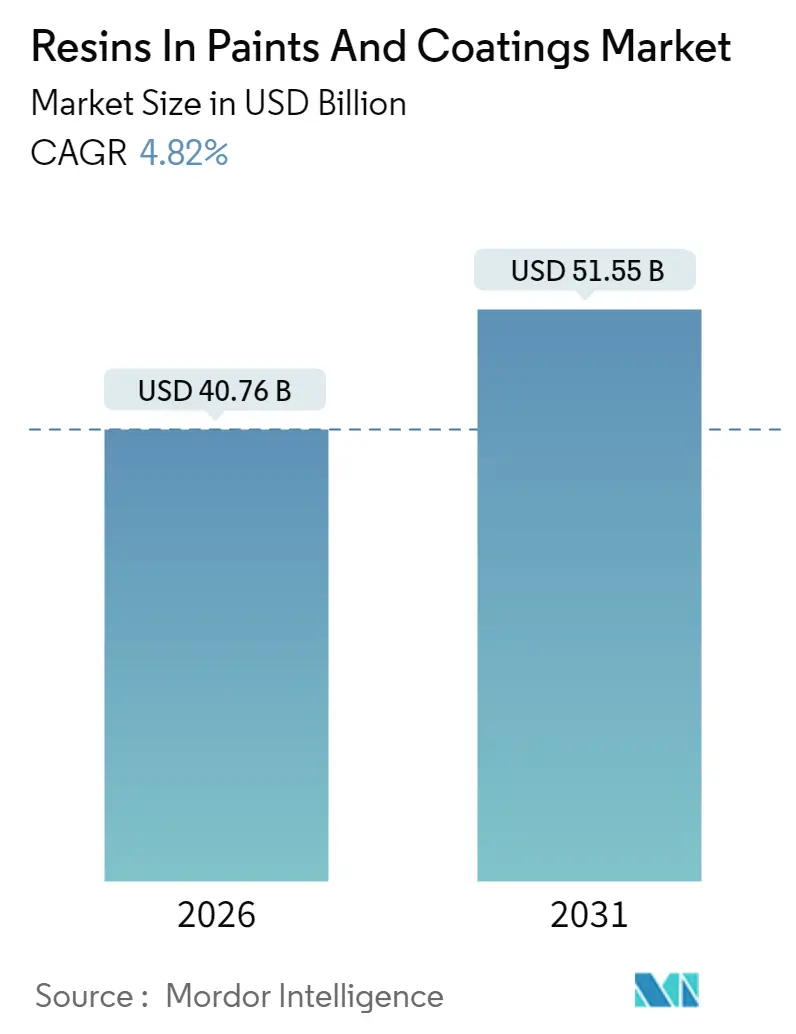

| Market Size (2026) | USD 40.76 Billion |

| Market Size (2031) | USD 51.55 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resins In Paints And Coatings Market Analysis by Mordor Intelligence

Resins In Paints And Coatings market size in 2026 is estimated at USD 40.76 billion, growing from 2025 value of USD 38.89 billion with 2031 projections showing USD 51.55 billion, growing at 4.82% CAGR over 2026-2031. Although the headline growth rate appears measured, policy-driven shifts away from solvent-borne chemistries are forcing formulators to retool their portfolios around waterborne acrylic, polyurethane dispersion, and other biocircular technologies. Governments on three continents tightened volatile-organic-compound (VOC) ceilings in 2024-2025, accelerating the transition timeline. The Asia-Pacific region continues to dominate value creation, thanks to infrastructure spending. However, North America and Europe are staging multi-year renovation programs that favor premium, low-VOC resins. Competitive intensity is rising as incumbents integrate renewable feedstocks, build regional dispersion plants, and deploy digital formulation platforms to compress product-development cycles.

Key Report Takeaways

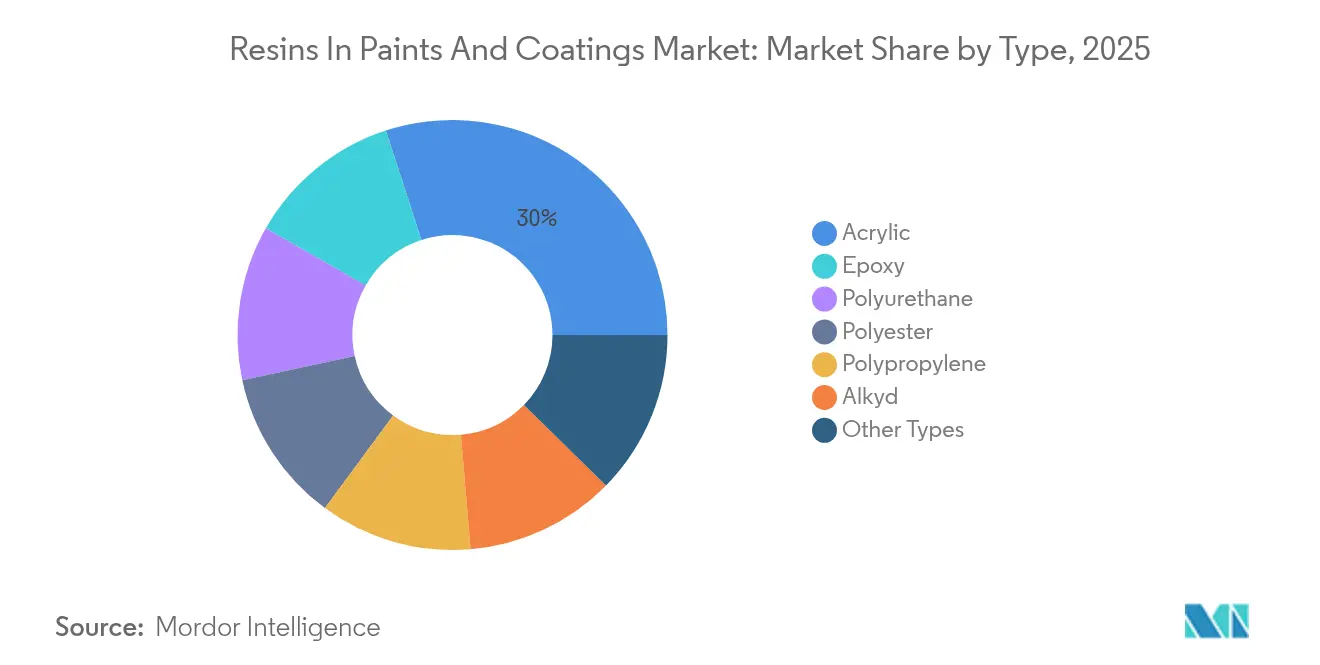

- By type, acrylic resins captured 30.02% of the coating resins market share in 2025 and are projected to grow at a 5.28% CAGR through 2031.

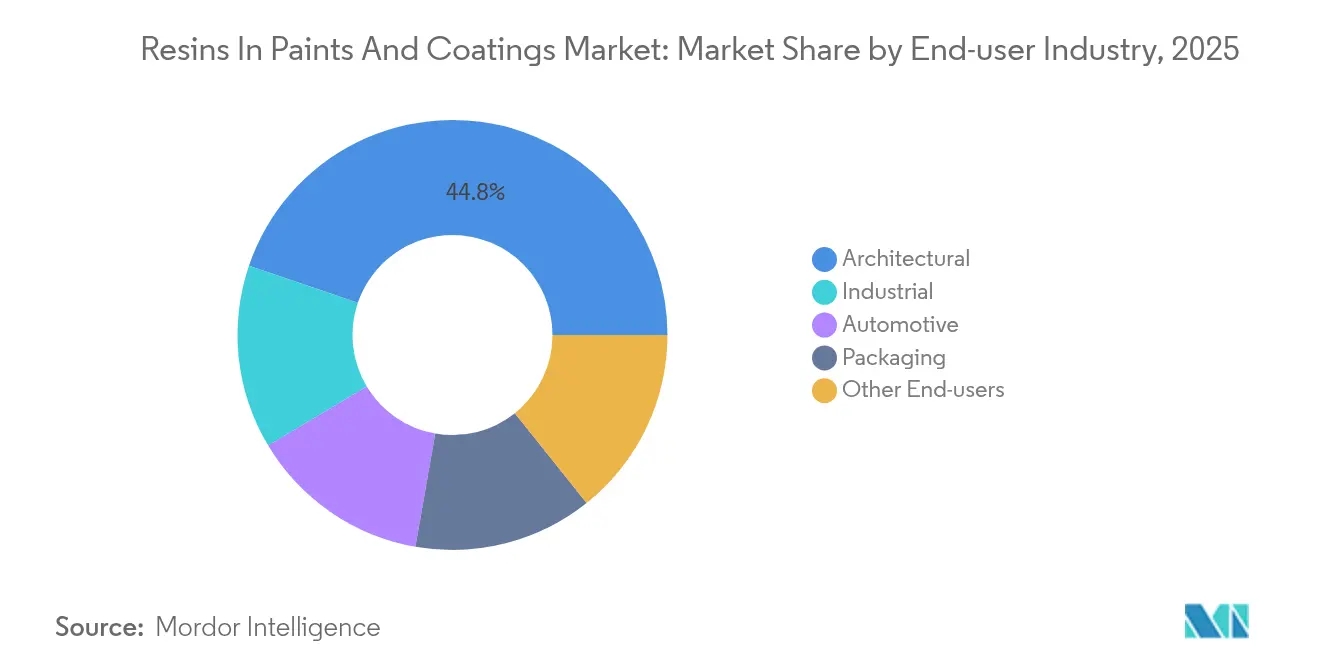

- By end-user industry, architectural coatings accounted for 44.78% of the coating resins market size in 2025 and are projected to advance at a 4.94% CAGR during 2026-2031.

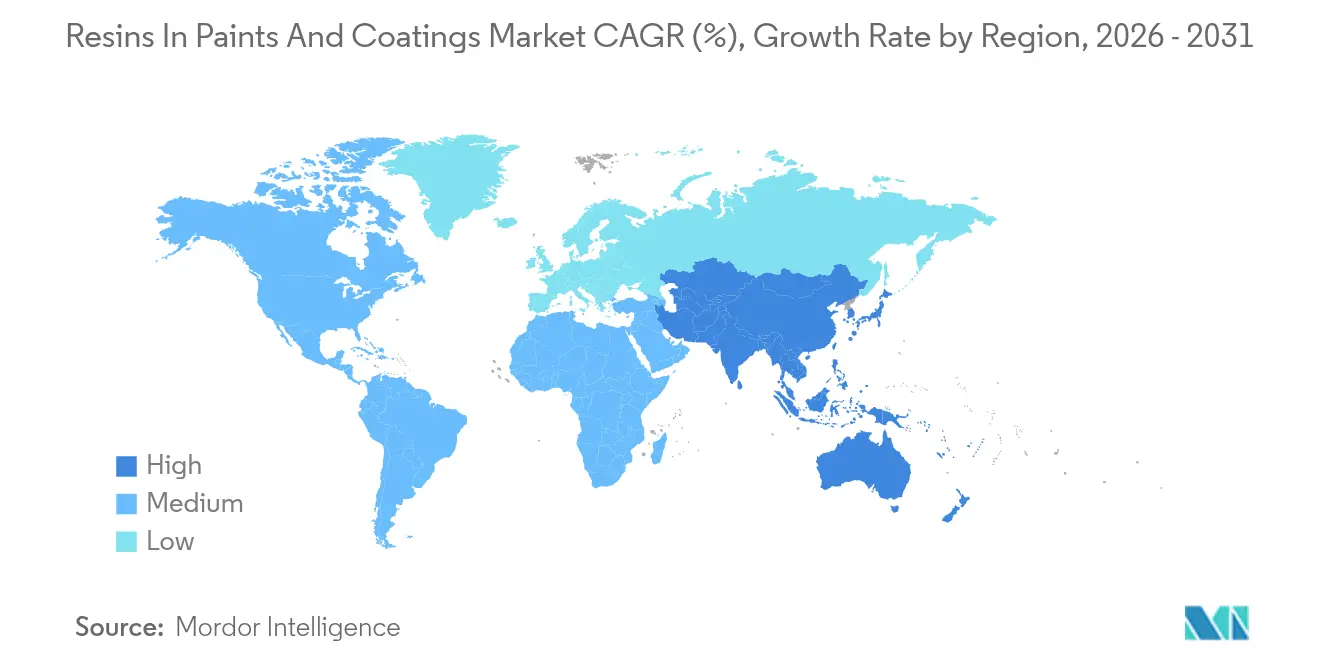

- By geography, the Asia-Pacific region led with a 44.12% coating resins market share in 2025, achieving the highest regional CAGR of 5.33% for the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Resins In Paints And Coatings Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom across the Asia-Pacific | + 1.8% | Asia-Pacific core, spillover to the Middle East and Africa | Medium term (2-4 years) |

| Tightening VOC-emission regulations | + 1.5% | Global, led by North America and the EU, accelerating in China | Short term (≤ 2 years) |

| Automotive output revival post-2024 | + 0.9% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Refurbishment wave in OECD housing | + 0.7% | North America and EU, emerging in Japan | Long term (≥ 4 years) |

| On-site 3D printing repair resins | + 0.3% | North America and EU pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Boom Across the Asia-Pacific

Public-sector infrastructure pipelines remain the single largest demand engine for architectural and protective coatings. India’s National Infrastructure Pipeline alone targets USD 1.4 trillion in cumulative capital outlays through 2025, generating a multi-year pull-through for epoxy- and polyurethane-rich bridge, port, and rail coatings[1]NITI Aayog, “National Infrastructure Pipeline: Status Update 2025,” niti.gov.in. Singapore’s Building and Construction Authority now requires Green Mark Platinum performance on all new public housing projects from 2025, effectively mandating water-based acrylic or polyurethane chemistries for factory-applied panels[2]Building and Construction Authority, Singapore, “Green Mark 2025 Roadmap,” bca.gov.sg. The Philippines allocated PHP 1.1 trillion (approximately USD 20 billion) to its Build Better More program in 2024, which includes industrial coating-intensive airports, roads, and energy assets. Across the region, state-owned developers are bundling low-VOC specifications into tender documents, accelerating the adoption of dispersion technology. Resin suppliers have responded by announcing the establishment of dispersion reactors in Indonesia and Vietnam, aiming to shorten lead times and reduce freight emissions. These moves provide global incumbents with a volume hedge while enabling regional formulators to localize their supply.

Tightening VOC-Emission Regulations

The compliance window for high-solvent resins is narrowing rapidly. In January 2025 the U.S. Environmental Protection Agency capped aerosol-coating VOC content at 25% by weight—down from prior category ceilings of 45%—forcing an immediate shift in binder selection. Georgia followed with Rule 391-3-1-.02(7)(c), effective July 2025, limiting flat architectural finishes to 50 grams per liter. Europe raised the bar again when the European Commission published draft Ecolabel criteria in October 2024 that impose a 30 grams-per-liter ceiling for interior paints, achievable only with high-solids acrylic or hybrid systems. China mirrored the EU thresholds in its GB 18582-2024 standard, signaling that the world’s largest construction market can no longer serve as a VOC-light haven. Resin suppliers with ready-to-scale waterborne portfolios—especially acrylic- and polyurethane-based dispersions—are winning share as formulators scramble to meet the cliff.

Automotive Output Revival Post-2024

Semiconductor bottlenecks eased in 2024, enabling global vehicle production to surpass 91 million units and rekindling demand for OEM coatings. Electric vehicles (EVs) account for the steepest slope, with their parc expected to double between 2023 and 2030, according to International Energy Agency scenarios. EV battery housings impose new thermal management and flame resistance criteria that favor epoxy and polyurethane systems. Lightweighting programs are driving automakers toward powder-based multilayer stacks, which eliminate primer steps and reduce oven energy by up to 30%. BASF reported an 18% jump in powder-coatings shipments to vehicle plants in 2024, underscoring the pivot. For resin vendors, this resurgence offers double leverage: higher volumes per unit and premium pricing for specialty functionality.

Refurbishment Wave in OECD Housing

The European Commission’s Renovation Wave initiative aims to double building renovation rates and mobilize EUR 275 billion annually, generating steady, policy-driven demand for low-VOC architectural coatings through 2030. The OECD has shown that current retrofit rates are below 1%, far from the 3% needed to reach net-zero real estate targets, leaving a structural growth gap for suppliers. Japan has joined the push: the Ministry of Land, Infrastructure, Transport and Tourism launched seismic-retrofit subsidies for pre-1981 structures in 2024, bundling envelope upgrades that require exterior resin performance improvements. Aged stock in the United States is also central; the Joint Center for Housing Studies estimated USD 485 billion in 2024 remodeling outlays, with exterior repainting one of the top spending categories. These programs create a long-duration revenue stream for dispersion suppliers positioned in low-odor, quick-dry portfolios.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility | -0.6% | Global, acute in Asia-Pacific due to naphtha dependency | Short term (≤ 2 years) |

| Shift toward powder-only systems | -0.4% | North America and EU automotive OEM, spreading to industrial | Medium term (2-4 years) |

| Microplastic phase-out rules | -0.2% | EU-led, early adoption in California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Price swings for propylene, benzene, and ethylene remain a significant headwind. ICIS Chemical Business reported that Asian contract propylene prices increased by 25% quarter-on-quarter in Q2 2024, following three unplanned cracker outages. Similar squeezes in Europe turned ethylene-derivative margins negative, compelling smaller epoxy producers to idle plants. Resin makers without upstream petrochemical integration face 60- to 90-day pass-through lags in the price-sensitive architectural channel. Partial insulation is emerging; Covestro has disclosed bio-circular polyols derived from waste vegetable oils that reached price parity with fossil feedstock by 2024, thereby trimming exposure to naphtha volatility. Still, the commodity link will limit margins until bio-feedstock adoption scales.

Shift Toward Powder-Only Systems

Powder coatings already hold a sizable share of the vehicle exterior market and are expanding into industrial segments for zero-VOC compliance. The American Coatings Association noted that single-coat powder lines cut energy use by 20-35% and eliminate flash-off time, making them attractive for OEM cost benchmarks. PCI Magazine’s 2024 technical survey revealed that low-temperature-cure powders are now workable on medium-density fiberboard, eroding the waterborne acrylic niche in furniture. European suppliers are accelerating the adoption of technology to meet the Industrial Emission Directive limits on solvent lines, effective 2025. Although powders struggle with fine-finish requirements in architecture, the shift trims liquid-resin demand in high-margin industrial applications, forcing suppliers to diversify into hybrid chemistries or expand dispersion lines.

Segment Analysis

By Type: Waterborne Acrylic Dominance Reshapes Formulation

Acrylic resins commanded 30.02% of the 2025 resins in paints and coatings market share, supported by their superior fit in low-VOC waterborne systems. Coupled with a 5.28% CAGR, they anchor value migration as regulators tighten emission ceilings. Epoxy resins are used in high-stress applications, such as those in the marine and wind-turbine industries; Hexion noted robust orders from turbine OEMs in its 2024 report. Polyurethane dispersions benefit from EV battery use cases. Polyester, a workhorse for powder coatings, faces margin compression as buyers mix polyester-epoxy hybrids that cure at lower temperatures. Alkyds, long the backbone of solvent-borne architectural paints, retain a niche in premium wood finishes but fade in mainstream wall-coating lines due to their slower dry time and higher VOC. ISO 14040 life-cycle assessments are now mandatory in Scandinavian public tenders, funneling share toward resins with verified environmental declarations.

Acrylic’s dispersion superiority also underpins factory-applied panel lines for modular housing. Prefabrication sites prefer quick-dry, single-pass coatings to meet tight takt times, making waterborne acrylic a natural choice. Epoxy suppliers are responding with nano-modified systems that cut bake curves, while polyurethane vendors push humidity-cure versions that eliminate forced-air ovens. Across the resins in paints and coatings market, supplier innovation is converging on CO₂-reduced feedstocks, evidenced by BASF’s pledge to integrate renewable propylene into its acrylic value chain by 2026. This feedstock strategy aligns with European public-procurement rules granting price premiums to materials with ≥20% bio-content.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Architectural Segment Anchors Growth

Architectural coatings absorbed 44.78% of the 2025 demand and are projected to carry a 4.94% CAGR through 2031, underpinned by large-scale renovation schemes in Europe and persistent new housing pipelines in India and Southeast Asia. Industrial coatings covering protective, marine, and general industrial sub-segments that rely on epoxy and polyurethane binders. Offshore wind, LNG terminals, and desalination plants all specify high-solids epoxy for corrosion service lives above 25 years. Automotive coatings are undergoing a disruptive change as OEMs transition from solvent-borne basecoats to waterborne metallics and powder clearcoats to comply with new VOC caps. Packaging formulators face bisphenol-A migration rules in both the U.S. FDA’s updated 21 CFR 175 and the EU’s Food Contact Materials Regulation, pushing them to polyester or acrylic alternatives. Other segments—such as wood, leather, and electronics—remain fragmented, providing niche resin suppliers with limited but stable profit pools.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific accounted for a 44.12% share of the resins in paints and coatings market in 2025 and is growing fastest at a 5.33% CAGR, propelled by China’s construction recovery and India’s megaproject pipelines. China’s residential completions rebounded in 2024 as municipal authorities eased credit, translating into higher drawdowns. India’s National Infrastructure Pipeline drives protective-coating resin consumption for bridges and railways, while the IKN Nusantara capital-city buildout in Indonesia and the Philippines’ Build Better More program lift regional baseline volumes. Japan’s seismic-retrofit subsidy and South Korea’s Green New Deal mandate low-VOC coatings in public procurement, driving the use of acrylic and polyurethane dispersions through local converting channels.

North America’s momentum rests on remodeling spending that hit USD 485 billion in 2024, with energy-efficient exteriors and siding replacements at the top of the wallet. The EPA’s 2025 VOC rule accelerates waterborne adoption, and Sherwin-Williams has flagged premium pricing on low-odor emulsions as margin-accretive. Canada’s carbon price reached CAD 80 per metric ton in 2024 and is nudging building owners toward retrofit packages that include high-albedo roof coatings to cut cooling loads.

Europe advances at a mid-single-digit pace led by the Renovation Wave and the Industrial Emission Directive, both of which prioritize low-solvent or powder chemistries. Nordic municipalities now require product-specific environmental product declarations in tenders, advantaging suppliers with fully audited dispersion lines. South America and the Middle East and Africa collectively account for a smaller share of coating resins market size but offer pocket-growth linked to oil-and-gas, mining, and stadium construction in Brazil, Saudi Arabia, and the United Arab Emirates.

Competitive Landscape

The resins in paints and coatings market is moderately fragmented, with the top five companies controlling a considerable portion of the global capacity. Strategic thrusts cluster around vertical integration into bio-feedstocks, regional capacity adds in Asia-Pacific, and co-development with major paint formulators. Regional producers such as Allnex and Arkema are betting on bio-refinery stakes to secure glycerin-based monomer supplies, while Hexion is leveraging lignin-based epoxy to address wood-adhesive markets. Digital formulation platforms and integrated life-cycle assessment modules are becoming table stakes as public buyers request cradle-to-gate carbon data. Smaller participants face twin pressures: rising compliance costs for VOC and microplastic rules, and volatile petrochemical feedstock pricing that magnifies working-capital stress. Yet white space remains in low-temperature-cure powder, offshore wind-blade epoxy, and biocircular polyester hybrids.

Resins In Paints And Coatings Industry Leaders

BASF SE

Dow

Covestro AG

Arkema

Allnex GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: BASF announced plans to incorporate renewable propylene into its acrylic resin value chain by 2026. This initiative aims to achieve 20% bio-content, meeting EU green procurement standards. The company is collaborating with European bio-refinery operators to implement this strategy, which is projected to lower the carbon footprint of acrylic dispersions by 25% compared to fossil-based alternatives.

- June 2024: Dow inaugurated a USD 100 million Texas Innovation Center focused on waterborne coatings and digital color-matching.

- July 2024: Hexion launched a lignin-based epoxy resin with 40% renewable content targeting wood adhesives and composites.

- April 2024: Allnex partnered with a European paint formulator to develop waterborne polyurethane dispersions for automotive refinish below 250 g/L VOC.

Global Resins In Paints And Coatings Market Report Scope

| Epoxy |

| Acrylic |

| Polyurethane |

| Polyester |

| Polypropylene |

| Alkyd |

| Other Types |

| Industrial |

| Architectural |

| Automotive |

| Packaging |

| Other End-users |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Type | Epoxy | |

| Acrylic | ||

| Polyurethane | ||

| Polyester | ||

| Polypropylene | ||

| Alkyd | ||

| Other Types | ||

| By End-user Industry | Industrial | |

| Architectural | ||

| Automotive | ||

| Packaging | ||

| Other End-users | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the resins in paints and coatings market in 2031?

It is forecast to reach USD 51.55 billion, reflecting a 4.82% CAGR from 2026.

Which resin type is expected to grow fastest?

Waterborne acrylics lead with a 5.28% CAGR, thanks to strengthening VOC regulations.

Why is Asia-Pacific so important for resins in paints and coatings market demand?

The region accounts for 44.12% of global demand and benefits from large infrastructure outlays in China, India, and Southeast Asia.

How are VOC regulations influencing product development?

U.S., EU, and Chinese regulations reduce VOC ceilings, prompting formulators to shift toward waterborne and powder systems that utilize acrylic, polyurethane, and hybrid resins.

What strategies are market leaders using to stay competitive?

Integration into bio-based feedstocks, regional dispersion capacity development, and AI-enabled formulation platforms are currently dominating investment programs.