Market Trends of Residential Real Estate Industry

Increased urbanization and homeownership by elderly

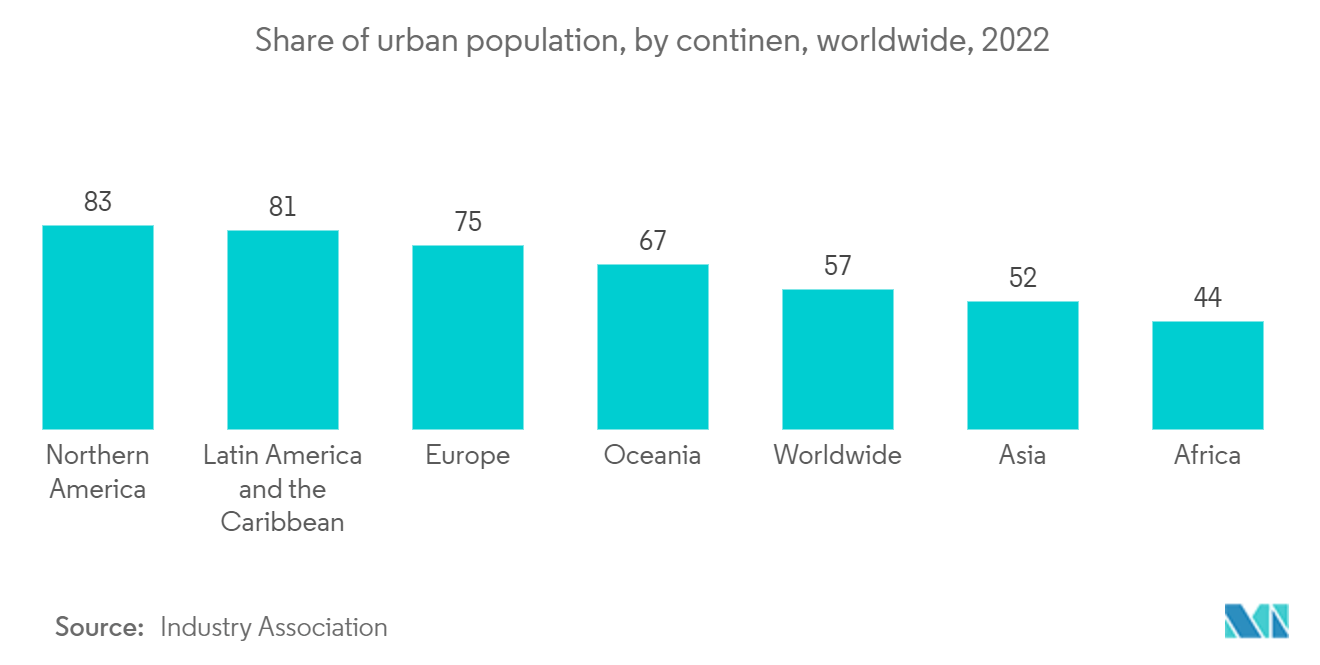

- Approximately 4.4 billion people, or 56% of the world's population, now reside in cities. By 2050, approximately 7 out of 10 people will live in cities, with the urban population predicted to surpass its current level. Nevertheless, the speed and scale of urbanization present difficulties, such as meeting the increased demand for affordable housing and functional infrastructure, including transportation systems, essential services, and jobs, particularly for the nearly 1 billion urban poor who live in informal settlements to be close to opportunities.

- In the United States, 75.3% of persons between the ages of 55 and 64 and 79.4% of people over 65 are homeowners. People under 35 had the lowest homeownership rate, with 38.3%.

- Gen X, born between 1965 and 1979, makes up the majority of American homebuyers (24%). They are the largest generation in terms of home sales. At 23%, older millennials (born between 1980 and 1989) are the second-largest homebuyers. While the younger generations tend to buy more frequently, the older generations predominately sell.

- According to experts, the ongoing rise of tall structures is a necessary component of the urban sustainability agenda as a housing solution. Major skylines are changing quickly in urban centers all around the world right now. The degree of development in cities like Shanghai, Shenzhen, Hong Kong, Dubai, Riyadh, Mumbai, and London, to name a few, is evidence of the diversity of these worldwide trends. The majority of development is taking place in the GCC and Asia's expanding economies.

Understand The Key Trends Shaping This Market

Download PDF

Increase in residential properties across the United States due to less mortgage rates

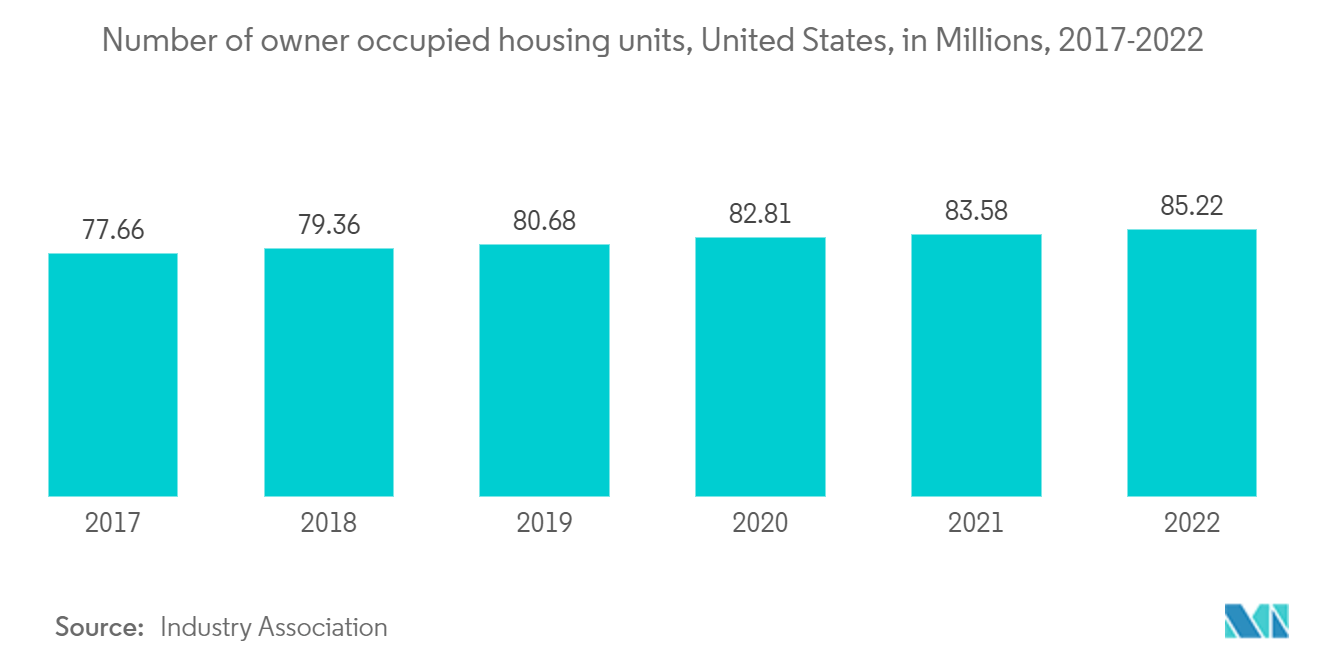

- When mortgage rates are low, it becomes more affordable for people to borrow money to purchase homes. Lower mortgage rates mean lower monthly mortgage payments, which can make homeownership more accessible to a larger number of people. This increased affordability can lead to a higher demand for residential properties.

- Lower mortgage rates often stimulate activity in the housing market. Potential homebuyers, motivated by the opportunity to secure a lower interest rate, may be more inclined to enter the market and purchase a property. This increased demand can contribute to an overall increase in residential property sales.

- Lower mortgage rates not only attract new homebuyers but also incentivize existing homeowners to refinance their mortgages. Refinancing allows homeowners to replace their current mortgage with a new one that has a lower interest rate. This can result in reduced monthly mortgage payments or even cash-out refinancing, where homeowners take advantage of the lower rates to access additional funds for other purposes.

- The increased demand for residential properties due to lower mortgage rates can also influence the construction and development sector. Developers and builders may respond to the demand by initiating new residential projects to meet the needs of potential homebuyers. This can lead to an increase in the supply of residential properties in certain areas.

- Mortgage rates are influenced by various economic factors, such as inflation, monetary policy, and market conditions. When mortgage rates decrease, it can be an indicator of a more accommodative monetary policy or a slower economy. Lower mortgage rates can stimulate economic activity by encouraging consumer spending and investment in the housing market.

- It's important to note that the impact of lower mortgage rates on residential properties can vary across different regions within the US. Factors such as local housing market conditions, employment rates, and population growth can influence the extent to which lower mortgage rates drive an increase in residential property activity.

Get Analysis on Important Geographic Markets

Download PDF