Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

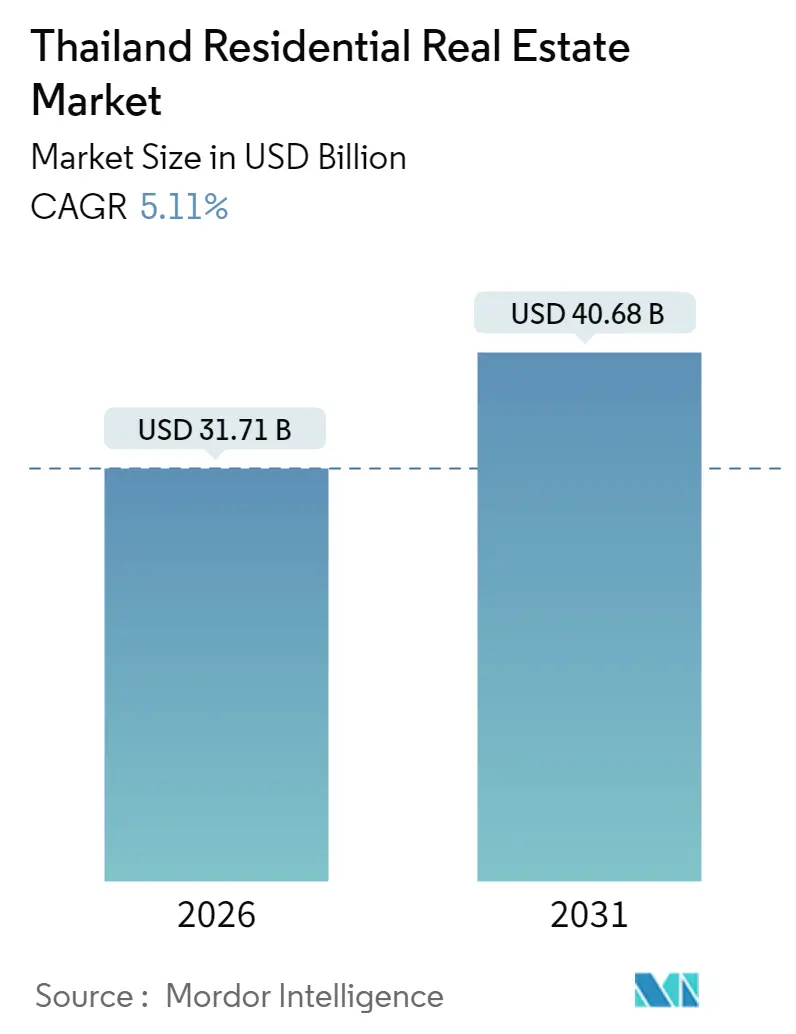

| Market Size (2026) | USD 31.71 Billion |

| Market Size (2031) | USD 40.68 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Residential Real Estate Market Analysis by Mordor Intelligence

Thailand residential real estate market size in 2026 is estimated at USD 31.71 billion, growing from 2025 value of USD 30.17 billion with 2031 projections showing USD 40.68 billion, growing at 5.11% CAGR over 2026-2031. Several powerful forces are shaping this trajectory. Structural urbanization keeps Bangkok and emerging provincial corridors in constant demand, while mortgage subsidies and sharply reduced transfer fees encourage first-time buyers despite a national household-debt ratio of 91.3% of GDP. Developers have responded by redirecting supply toward premium, low-volume projects, leaning on stronger pricing to offset rising construction costs. A rebound in tourism and a liberalized social climate, including same-sex marriage, is lifting rental yields in resort destinations. At the same time, stricter bank underwriting, condominium oversupply in secondary city sub-markets, and regulatory uncertainty around long-term leases for foreigners temper near-term expansion.

Key Report Takeaways

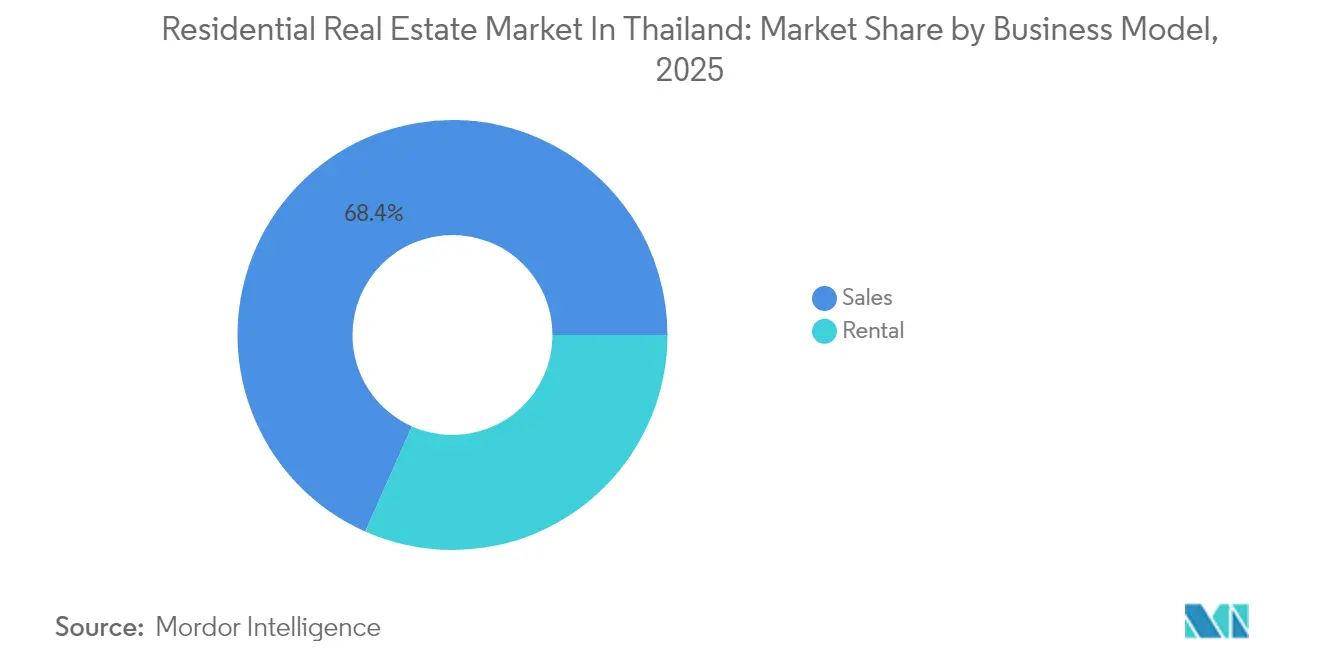

- By business model, the sales channel led with 68.35% of the Thailand residential real estate market size in 2025, while rentals are advancing at a 5.58% CAGR to 2031.

- By property type, apartments and condominiums held 63.25% share of the Thailand residential real estate market size in 2025; villas and landed houses post the fastest 6.44% CAGR to 2031.

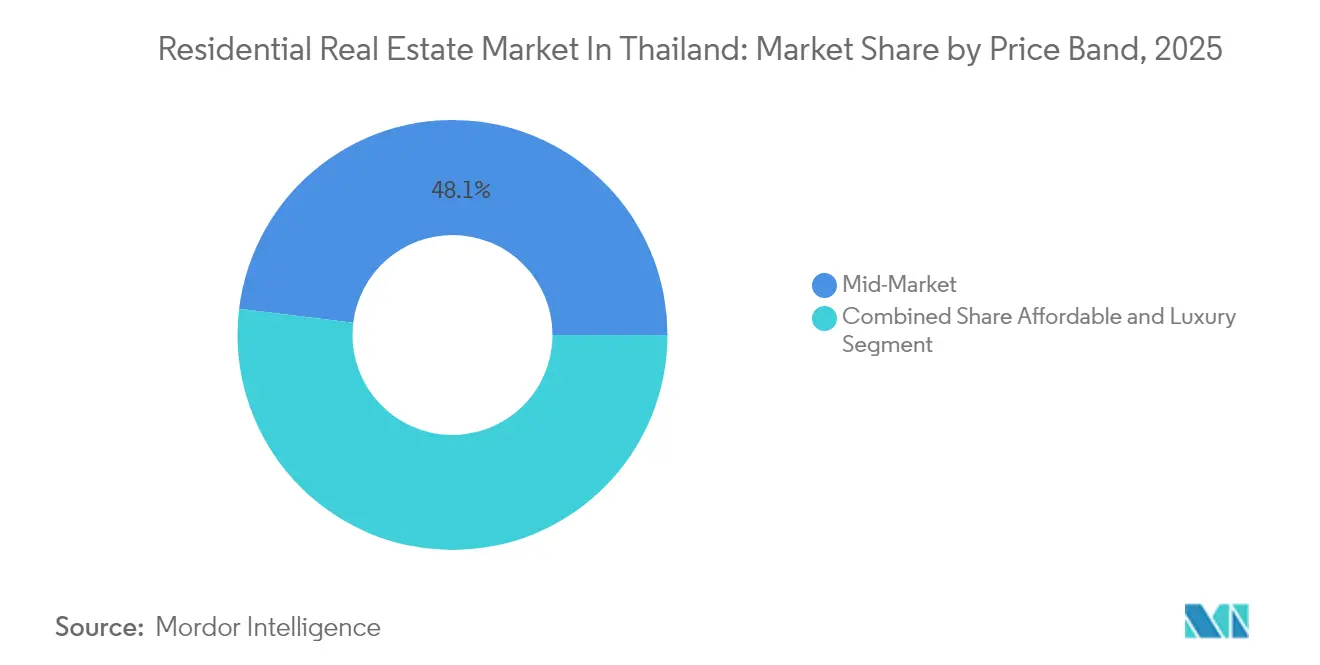

- By price band, mid-market offerings represented 48.05% of total value in 2025, whereas luxury units are expanding at a 6.03% CAGR through 2031.

- By mode of sale, primary transactions accounted for 60.55% share of the Thailand residential real estate market size in 2025 and are increasing at a 6.22% CAGR to 2031.

- By geography, Bangkok controlled 46.55% of Thailand residential real estate market share in 2025; Phuket is forecast to grow at a 6.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and migration into Bangkok | +1.2% | Bangkok Metropolitan Region; secondary cities | Long term (≥ 4 years) |

| Growing middle-class demand for condos | +1.0% | Bangkok, Chiang Mai, Phuket, urban corridors | Long term (≥ 4 years) |

| Tourism and expatriate inflows | +0.9% | Phuket, Pattaya, Bangkok, resort destinations | Medium term (2-4 years) |

| Government incentives and mortgage programs | +0.8% | National, concentrated in Bangkok and provincial centers | Medium term (2-4 years) |

| Shift toward vertical, integrated communities | +0.6% | Bangkok Metropolitan Region; major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanization and migration into Bangkok and major cities boosting housing demand

Urbanization and migration trends are significantly influencing housing demand in Bangkok and other major cities in Thailand. As Thailand's primate city, Bangkok attracts a significant influx of rural-to-urban migrants. This trend bolsters the city's ability to absorb new housing units, even in times of national economic softening. Investments in mass-transit lines, notably the Yellow Line, are unlocking peripheral lands. This has enabled luxury projects in Bangna-Trad to command unit prices exceeding USD 555,000. Meanwhile, secondary corridors like Khon Kaen and Nakhon Ratchasima are witnessing quicker per-capita GDP growth, suggesting a slow but steady spread of capital. Developers with a national presence are strategically acquiring land along rail extensions, positioning themselves for this expanding multi-nodal landscape[1]World Bank Group, “Thailand Economic Monitor: Navigating Urban Futures,” worldbank.org.

Growing middle-class population driving demand for condominiums and townhouses

The growing middle-class population in Thailand is significantly influencing the demand for condominiums and townhouses. Even as Thailand's GDP growth eased to 2.0% in 2025, surveys reveal the nation's burgeoning middle class remains steadfast in its urban ownership aspirations. In response, developers are rolling out mid-to-upper-mid projects, seamlessly blending retail, co-working spaces, and health amenities. A prime example is Central Pattana's ambitious USD 417 million mixed-use pipeline. The allure of proximity to quality education is evident, with Four Seasons Private Residences securing a notable USD 111 million in sales, predominantly from families hailing from China. However, a prevailing debt overhang is straining affordability. In a bid to navigate this challenge, developers are forging partnerships, offering innovative solutions like bundled deferred down-payments and rent-to-own options.

Tourism and expatriate inflows creating demand for second homes and rental properties

The tourism and expatriate markets are witnessing significant growth, creating increased demand for second homes and rental properties. Thanks to the recent same-sex marriage legislation, tourist arrivals are set to surge by an additional 4 million annually, translating to a USD 2 billion boost in visitor receipts. In Phuket, the price of luxury villas has seen a twofold increase over the past two years, driven by a surge in demand from Russian and European buyers eyeing long-term stays. Meanwhile, Asset World Corp’s hospitality division has not only rebounded but now boasts a revenue that's 63% higher than pre-COVID levels. They're strategically reinvesting this cash flow into branded residences, catering to the growing short-let demand. While foreign companies now enjoy clearer regulations on land holdings, expanding the pool of potential investors, they also face new challenges due to lease-term restrictions.

Government incentives and mortgage programs supporting homeownership

Governments worldwide are implementing targeted measures to make homeownership more accessible, particularly for low- and middle-income groups. With the "Happy Home" and "Happy Life" schemes, interest rates are capped at around 3% for five years. This move is designed to ease entry for buyers eyeing units priced under USD 83,000. Additionally, fee waivers have slashed transfer charges to a mere 0.01% until June 2026, effectively cutting closing costs by 99%. These combined measures have led to a rise in mortgage originations, despite banks tightening their risk assessments. The "Homes for Thais" initiative, offering 300,000 units with no-down-payment options, bolsters demand, especially for urban low-income earners. Yet, the success of these programs is contingent on lenders' willingness and the pace of household debt reduction.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oversupply in condominium markets | -1.4% | Bangkok Metropolitan Region; major urban centers | Short term (≤ 2 years) |

| High household debt levels limiting affordability | -1.1% | National, acute in lower-income segments | Medium term (2-4 years) |

| Regulatory restrictions on foreign ownership | -0.3% | Resort destinations; luxury segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oversupply in condominium markets leading to slower absorption rates

The condominium market is currently grappling with an oversupply, leading to slower absorption rates and market challenges. In Q2 2025, new condominium launches plummeted to just 373 units, marking a staggering 94.2% decline and the lowest point in 16 years. This sharp drop underscores a significant pullback by developers. Meanwhile, unsold inventory has surged to about 74,000 units, predominantly located in Bangkok’s suburban areas. To move this stock, sellers are resorting to steep discounts and offering rent guarantees. While financially robust players are seizing the opportunity to acquire distressed properties at attractive prices, the market still anticipates a sluggish absorption period of up to 24 months. As the market seeks to rebalance, price increases are expected to remain muted, squeezing profit margins and pushing back the timeline for new developments.

High household debt levels limiting affordability for some buyers

High household debt levels are increasingly impacting affordability for buyers, particularly first-time purchasers. With households averaging liabilities of USD 16,800 and a debt-service ratio hitting 22.3%, many families are either postponing purchases or opting for smaller units. In response to concerns over rising non-performing loans, commercial banks scaled back residential lending by 10.1% year-over-year in Q2 2024. While government debt-consolidation programs provide a temporary reprieve, lasting solutions hinge on boosting incomes and enhancing financial literacy. This financial strain is especially pronounced for first-time buyers. In light of this, developers are increasingly turning to staged-payment and rent-to-own models, extending their cash-conversion cycles.

Segment Analysis

By Business Model: Sales Dominant but Rentals Gain Momentum

Sales transactions commanded 68.35% of the Thailand residential real estate market share in 2025, reflecting enduring cultural preferences for ownership and the influence of mortgage incentives. New-build promotions, reduced transfer fees, and tax deductions kept transaction pipelines active even as macro uncertainty persisted. However, rental income prospects in central Bangkok and resort zones are strengthening as expatriate headcounts recover. The rental subsector is forecast to expand at a 5.58% CAGR, underpinned by flexible-living demand and asset-light tendencies among younger professionals. Institutional landlords are scaling portfolios, and developers such as Central Pattana are introducing branded co-living towers that extract premium rents through amenity bundles.

The Thailand residential real estate market continues to evolve toward hybrid tenure models. Developers market rent-to-own pathways that convert leases into down-payments, bridging affordability gaps created by high household debt. Prop-tech platforms simplify tenant screening and yield analytics, enticing family offices to allocate capital to build-to-rent strategies. Regulatory support, including fast-track visa renewals for high-skilled expatriates, further enlarges the occupier base. Sales volumes will likely remain dominant, but recurring cash-flow projects are poised to supply a growing share of developers’ earnings.

Note: Segment shares of all individual segments available upon report purchase

By Property Type: Condominiums Rule, Villas Accelerate

Apartments and condominiums made up 63.25% of the Thailand residential real estate market size in 2025 thanks to land scarcity in metropolitan Bangkok and well-established finance channels. High-rise projects continue to debut along new transit nodes, offering buyers secure entry prices and extensive facilities. Some developers retrofit ageing towers with energy-management systems to stay competitive. Meanwhile, villas and landed houses, though smaller in base, are projected to grow fastest at a 6.44% CAGR. The pandemic catalyzed demand for larger floorplates and outdoor space, trends still resonating in 2025.

Villa pipelines are heaviest in suburban Bangkok districts such as Ratchaphruek and in tourism-centered provinces like Phuket. Magnolia Quality Development Corporation’s USD 3.5 billion Forestias highlights how integrated master plans can blend low-density housing, senior living, and forest conservation for premium positioning. Condominium builders respond by adding villa-style features—private gardens, duplex layouts, and touch-less access systems—within vertical envelopes. Environmental and wellness certifications double as marketing levers and future-proof valuations against tightening building codes.

By Price Band: Mid-Market Anchors Volume, Luxury Drives Growth

Mid-market homes sustained a 48.05% share of total transactions in 2025, serving Thailand’s broad middle-income bracket. Product offerings emphasize efficient layouts, shared workspaces, and easy access to rail corridors. Price ceilings hover around USD 194,000, the threshold tied to transfer-fee reductions, creating a sweet spot for both buyers and lenders. Yet, luxury stock is set to log the quickest 6.03% CAGR, propelled by resilient purchasing power among domestic elites and foreign investors. Projects such as Four Seasons Private Residences Bangkok prove appetite for trophy assets that command prices exceeding USD 5.5 million.

Developers in the mid-segment streamline construction via standardized modular components to retain margin. In contrast, luxury builders invest in branded collaborations with hospitality groups, art curations, and concierge tech that elevate service levels. Currency fluctuations and geopolitical shifts periodically alter foreign inflows, but investment diversification motives sustain top-tier demand. Over time, the Thailand residential real estate market is likely to display a barbell structure, with the most robust momentum sitting at affordable and luxury extremities.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Sale: Primary Units Lead Volume and Value

Primary sales represented 60.55% of the Thailand residential real estate market share in 2025, buoyed by purchasers’ trust in warranty protections and the allure of modern designs. Developers differentiate through smart-home ecosystems, green roofs, and community retail clusters, which secondary stock rarely matches. The primary channel is forecast to post a 6.22% CAGR through 2031 as integrated township concepts proliferate. Mortgage banks often attach preferential rates to new launches, reinforcing first-hand uptake.

Secondary-market activity remains essential for mobility within the housing ladder. However, oversupply in certain condominium belts has narrowed bid-ask spreads, favoring buyers. Legal shifts around foreign leases add diligence costs to pre-owned transactions, nudging some investors back toward developer-backed inventory. Over the medium term, the dual-track market should converge once post-2023 oversupply clears and macro stability improves.

Geography Analysis

In 2025, Bangkok accounted for 46.55% of the total market value, supported by its diverse employment sectors and high-quality health and education facilities. Despite a 19% decline in new property launches, average house prices increased by 22% year-over-year, reaching USD 187,000. This reflects developers' focus on profitability over volume. Rising land costs and traffic congestion are driving vertical development, while plans for Southeast Asia’s tallest tower indicate long-term market confidence. Extensions of rapid-transit lines, such as the Pink and Orange Lines, are improving cross-river connectivity and unlocking suburban development opportunities. Additionally, eco-friendly upgrades in central districts highlight the city’s transition toward compliance with green building standards.

Phuket is the fastest-growing market, projected to achieve a 6.69% CAGR through 2031, driven by a recovery in tourism. The planned USD 2.2 billion international airport is expected to increase passenger capacity, stimulating hospitality-focused residential developments. Despite stricter lease regulations, villa absorption rates remain strong due to demand from Russian and European buyers. However, the island faces challenges such as road congestion and water supply issues. Developers are addressing these concerns by concentrating projects near proposed light-rail corridors and collaborating with utility providers to ensure sustainable resources.

Secondary cities, including Pattaya, Chiang Mai, Khon Kaen, and Nakhon Ratchasima, are attracting middle-class relocators seeking affordable living options. The Thai government’s "Homes for Thais" program is channeling subsidies to areas along upcoming rail lines, increasing land values ahead of construction. Regional universities and medical tourism hubs are generating consistent white-collar demand, while local authorities are introducing incentive packages to attract developers. Once major infrastructure projects are completed, this "Rest of Thailand" group is expected to surpass Bangkok’s growth, contributing to a more balanced national housing market.

Competitive Landscape

Thailand's residential market is moderately concentrated, with the five largest developers accounting for approximately 55% of the active project value. Prominent publicly listed companies such as Central Pattana, Asset World Corp, Sansiri, and MQDC leverage extensive land banks and diversified cash flow streams to manage market fluctuations. Central Pattana, in particular, oversees 37 residential projects under three distinct brands and utilizes its mall portfolio for cross-marketing homes, a strategy that earned the company 12 Asia Executive Team awards in 2024.

Corporate strategies in 2025 are characterized by significant adjustments. Leading developers have reduced mass-market launches, reallocating resources toward premium townships where strong presales help offset increased input costs. Partnerships with investors from Japan, China, and the Middle East provide both patient capital and expertise in designing integrated mixed-use developments. Additionally, financial flexibility allows these developers to acquire distressed plots from smaller, over-leveraged builders, driving further industry consolidation.

Technological advancements and adherence to ESG standards are emerging as critical competitive factors. MQDC incorporates research-based well-being metrics into its project designs, while Sansiri's "Living App" offers residents services such as concierge support, security, and energy tracking. Publicly listed companies are now disclosing scope-3 emission pathways in compliance with Securities and Exchange Commission regulations. Early adopters of these practices benefit from preferential terms offered by green lenders and institutional asset managers, creating a competitive edge over smaller firms that have yet to modernize their governance frameworks.

Thailand Residential Real Estate Industry Leaders

Pruksa Real Estate

Supalai

Sansiri

AP Thai

Origin Property

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Transfer and mortgage fees on homes priced below USD 194,000 were cut to 0.01% until Jun 2026. The Ministry of Finance projects the measure will add about 30,000 transactions per year.

- January 2025: The government broke ground on the first 50,000 units under the “Homes for Thais” project, launching a nationwide pipeline that targets 300,000 affordable houses by 2028.

- September 2024: Central Pattana committed USD 417 million for five mixed-use projects—headlined by the USD 125 million Central Krabi complex—scheduled to open between 2025 and 2026.

- August 2024: Dusit International signed a long-term management partnership for the 52-story KingsQuare Residence in Bangkok, adding a sixth property to its branded-residence portfolio ahead of the 2026 opening.

Thailand Residential Real Estate Market Report Scope

Residential real estate includes housing for individuals, families, or groups of people to live on. Furthermore, the report provides key insights into the Thai residential real estate market. It includes technological developments, trends, and initiatives taken by the government in this sector. It also focuses on the market dynamics, such as factors driving the market, restraints to the market growth, and opportunities going forward. Additionally, the competitive landscape of the Thai residential real estate market is depicted through the profiles of active key players. In the report, the Thai Residential Real Estate market is segmented by Property Type (Apartments and Condominiums, Landed Houses, and Villas) and by Key Cities (Bangkok, Chiang Mais, Nontha Buri, and Samut Prakan). The report offers market size and forecasts for the Thai Residential Real Estate Market in value (USD billion) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

How large is the Thailand residential real estate market in 2026?

It was valued at USD 31.71 billion in 2026, with a projected climb to USD 40.68 billion by 2031.

What CAGR is expected for Thailand’s residential sector to 2031?

The market is forecast to register a 5.11% CAGR over 2026-2031.

Which geography is expanding fastest within Thailand’s housing landscape?

Phuket leads with a projected 6.69% CAGR, buoyed by tourism and foreign villa demand.

What policy has most recently supported first-time buyers?

Transfer and mortgage fees were cut to 0.01% on homes priced below USD 194,000 until June 2026.

Which property type is showing the strongest growth momentum?

Villas and landed houses are projected to grow at a 6.44% CAGR as buyers prioritize space and privacy.

How are developers responding to condominium oversupply?

They are deferring new launches, offering discounts, and acquiring distressed assets while pivoting to premium, lower-density projects.

Page last updated on: