| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 4.78 Billion |

| Market Size (2030) | USD 7.42 Billion |

| CAGR (2025 - 2030) | 9.19 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Oman Residential Real Estate Market Analysis

The Oman Residential Real Estate Market size is estimated at USD 4.78 billion in 2025, and is expected to reach USD 7.42 billion by 2030, at a CAGR of 9.19% during the forecast period (2025-2030).

The Omani real estate market landscape is experiencing significant transformation driven by demographic shifts and changing market dynamics. Expatriates, who constitute approximately 40% of Oman's population, continue to be a crucial demand driver in the residential real estate sector. However, the market faces challenges with oversupply, particularly in Muscat, where approximately 87,000 residential units remain unoccupied, representing nearly 20% of the total residential supply. This oversupply situation has led to significant price adjustments, with average apartment rental values declining by 10-15% and villa rental values dropping by 15-25% over the recent period.

The government's ambitious urban development initiatives are reshaping the residential landscape across Oman. In June 2023, the launch of Sultan Haitham City marked a significant milestone, with plans to accommodate 100,000 people in 20,000 new residences. The project encompasses 19 integrated residential communities equipped with comprehensive amenities, including 23 mosques and 11 health facilities. Additionally, the Ministry of Housing and Urban Planning has unveiled plans to develop future sustainable cities in Salalah, Nizwa, Sohar, and Muscat, spanning an area of 5 million square meters, demonstrating the government's commitment to sustainable urban development.

The market is witnessing a surge in waterfront and integrated tourism complex (ITC) developments, enhancing the premium residential segment. The Hayy al Sahil project in Quriyat, launched in May 2023, represents a significant development with 400 housing units in its first phase, offering permanent residency options for overseas investors. The project's total investment of RO385 million encompasses various phases, including the development of 1,600 housing units in the second phase and 3,000 units in the final phase, along with luxury waterfront villas and comprehensive amenities.

Premium residential developments, particularly in locations like Al Mouj and Muscat Hills, have demonstrated greater market resilience. These areas experienced a more moderate decline in rental values of around 10% and have maintained relative stability, particularly in the high-end villa segment. The real estate market is also seeing innovative developments like the three massive waterfront projects planned by Oman's Ministry of Housing and Urban Planning for the governorates of Dhofar, Musandam, and South Al Batinah, including the USD 40 million Rathath Boulevard project in Dhofar and the Aames Bay Development in Musandam, valued at RO6.9 million.

Oman Residential Real Estate Market Trends

Government Initiatives and Infrastructure Development

The Omani government's aggressive infrastructure development initiatives are significantly driving the real estate market. In June 2023, the launch of Sultan Haitham City marked a major milestone, with plans to construct 20,000 new residences across 19 integrated residential communities, complete with comprehensive amenities including 23 mosques and 11 health facilities. This development demonstrates the government's commitment to creating sustainable urban communities that cater to modern living requirements while maintaining cultural values. The project's comprehensive planning includes essential services like healthcare facilities designed to serve varying population capacities, with two health centers capable of serving 20,000 patients and six centers serving 10,000 patients each.

The Ministry of Housing and Urban Planning's commitment to developing integrated housing projects across multiple governorates further strengthens the market momentum. In January 2023, the ministry signed eight new contracts worth over OMR 150 million (USD 389.55 million) across Muscat, North Al Batinah, and South Al Batinah. These projects include the construction of integrated cities featuring 1,050 homes in the Wilayat of Amerat and 1,350 housing units in the Halban district, both equipped with modern utilities and comprehensive community facilities. Additionally, the development of three waterfront projects in South Batinah, covering areas of 10,990 square meters and 222,441 square meters in Barka and 180,425 square meters in Mussanah, demonstrates the government's focus on creating diverse residential options.

Understand The Key Trends Shaping This Market

Download PDF

Growing Expatriate Population and Tourism

The expanding expatriate population and tourism sector are driving substantial growth in Oman's real estate market. From 2023 onwards, there has been a sustained increase in expatriate numbers, leading to heightened demand for rental accommodation throughout Muscat. The government's progressive policies, including the introduction of the usufruct system allowing expatriates over 23 years old to purchase housing units in multi-story residential buildings for 99 years, have created new market opportunities. This system provides significant benefits, including the right to own housing units personally or in partnership with first-degree relatives, access to financing with real estate collateral, and the ability to sell residential units after four years.

The tourism sector's growth has catalyzed the development of integrated tourism complexes (ITCs) and luxury residential properties. Leading real estate developers in Oman, like Muriya, have responded to this trend with projects such as Amazi in Hawana Salalah and Fanar Views, offering waterfront living options with high potential returns in the year-round rental market. These developments combine residential offerings with tourism amenities, including hotels, retail outlets, and recreational facilities. For instance, the Fanar Views project provides fully furnished, serviced townhouses and villas with access to hotel amenities, beaches, and sports facilities, catering to both permanent residents and tourists seeking premium accommodation options.

Strategic Urban Planning and Sustainable Development

Strategic urban planning initiatives are fundamentally reshaping Oman's residential real estate landscape. The Greater Muscat master plan, scheduled for completion in early 2023, represents a comprehensive approach to urban development, focusing on land use optimization, population distribution, economic growth, and the integration of public transport networks. This master plan particularly emphasizes the development of sustainable green spaces that support community prosperity while protecting the natural environment, making it a significant driver for residential real estate development. The integration of parts of Barka into Greater Muscat has created new opportunities for residential development in previously underutilized areas.

In February 2023, the Ministry of Housing and Urban Planning launched ambitious plans to develop future sustainable cities in Salalah, Nizwa, Sohar, and Muscat, covering an area of 5 million square meters. These cities are designed to accommodate between 50,000 to 130,000 people, with housing units ranging from 10,000 to 30,000 per development. The planning emphasizes the creation of integrated urban communities with essential services and modern amenities. This strategic approach to urban development includes the allocation of 23,000 residential land plots and the processing of over 30,000 applications for ownership verification and registration, demonstrating the government's commitment to sustainable urban growth and housing accessibility.

Segment Analysis: By Type

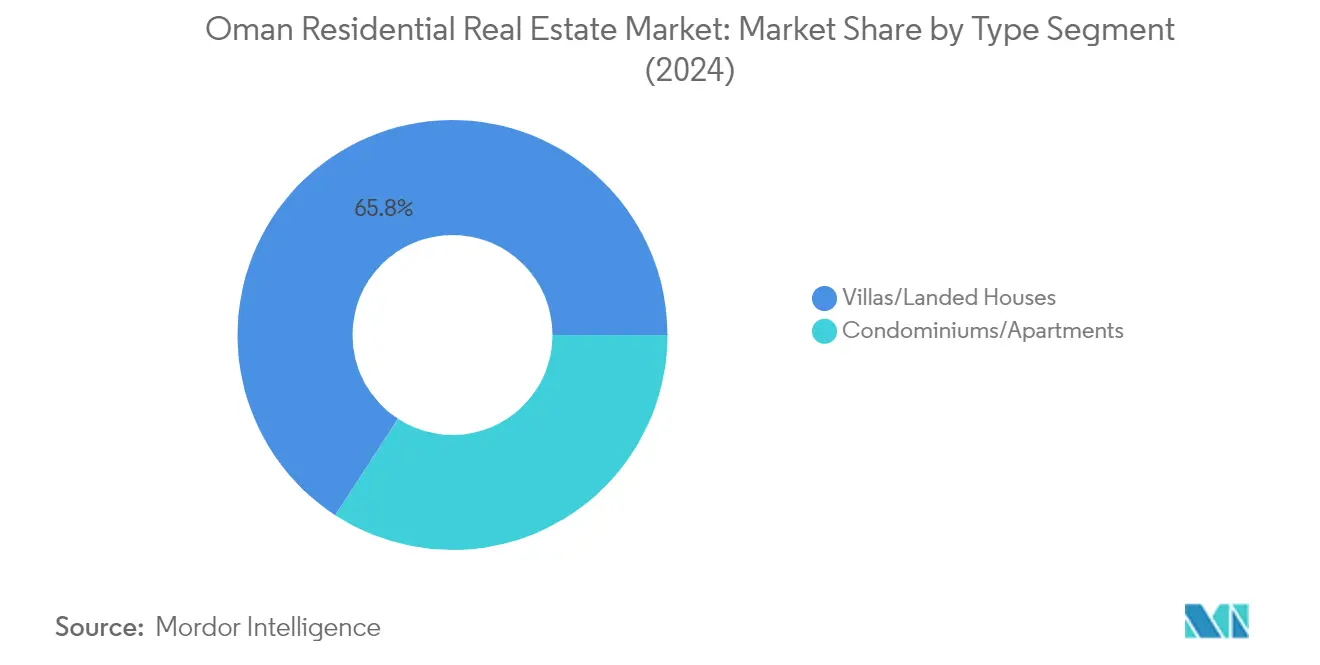

Villas/Landed Houses Segment in Oman Residential Real Estate Market

The villas and landed houses segment continues to dominate the Oman residential real estate market, commanding approximately 66% market share in 2024. This segment's prominence is particularly evident in premium locations like Muscat Hills and Al Mouj, where high-end villas with outdoor gardens and private swimming pools remain highly sought after. The segment's strong performance is supported by increasing demand from both local and international buyers seeking spacious living environments. Recent developments like the Sultan Haitham City project, which includes numerous luxury villas, and the LA VIE project in Muscat Hills, featuring premium residential units, demonstrate the robust growth potential in this segment. The preference for villas is further reinforced by changing lifestyle preferences post-pandemic, with more families prioritizing larger living spaces and private outdoor areas. Additionally, the demand for residential housing in these areas has contributed to rising house prices in Oman.

Condominiums/Apartments Segment in Oman Residential Real Estate Market

The condominiums and apartments segment is experiencing the fastest growth in the Oman residential real estate market, with projections indicating approximately 7% growth from 2024 to 2029. This accelerated growth is driven by several factors, including urbanization trends and the increasing demand for affordable residential property options in major cities. The segment is witnessing significant developments, particularly in integrated tourism complexes like Muscat Bay, which offers luxury apartments with world-class amenities. The growth is further supported by government initiatives promoting affordable housing and the development of smart cities. Recent projects like the Hayy al Sahil in Quriyat, which includes 400 housing units in its first phase, and the Residences at Mandarin Oriental, featuring 156 premium branded residences, exemplify the segment's dynamic expansion and diversification. The availability of Oman apartments for sale in these developments highlights the segment's appeal to a diverse range of buyers seeking property for sale in Muscat Oman.

Oman Residential Real Estate Industry Overview

Top Companies in Oman Residential Real Estate Market

The residential real estate market in Oman is characterized by continuous innovation and strategic developments from key players like Al Mouj Muscat, Al Raid Group, Wujha Real Estate, and Al-Taher Group. Real estate companies in Oman are increasingly focusing on sustainable development practices and smart home technologies, with several players incorporating home automation systems and energy-efficient designs in their projects. Market leaders are expanding their portfolios through integrated residential neighborhoods and mixed-use developments, particularly in prime locations like Muscat and Dhofar. Strategic partnerships with government entities and international developers have become a common trend, enabling companies to leverage expertise and resources for large-scale projects. Operational agility is demonstrated through flexible payment plans, digital marketing initiatives, and enhanced property management services, while product innovation is evident in the increasing focus on lifestyle-oriented residential communities with comprehensive amenities.

Market Structure Shows Dynamic Competitive Environment

The Oman residential real estate market exhibits a fragmented structure with a mix of established local developers and international players. Local conglomerates maintain a strong presence through their deep understanding of the market and established relationships with government entities, while international players bring global expertise and innovative development concepts. The market is experiencing gradual consolidation through joint ventures and strategic partnerships, particularly in large-scale integrated residential projects. Real estate developers in Oman are increasingly forming alliances with technology providers and facility management firms to enhance their service offerings and maintain a competitive advantage. The presence of government-backed developers has also shaped the competitive landscape, particularly in affordable housing segments and integrated residential neighborhoods.

The market is characterized by increasing competition in premium residential segments, particularly in key cities like Muscat, where developers are differentiating themselves through unique architectural designs and lifestyle amenities. Property management services have become a key differentiator, with companies expanding their service portfolios to include comprehensive maintenance and facility management solutions. The market has seen the emergence of specialized players focusing on specific segments such as luxury villas and smart homes, while established players are diversifying their portfolios across different residential property types and price segments. Cross-border partnerships and knowledge transfer agreements are becoming more common as companies seek to enhance their technical capabilities and market reach.

Innovation and Adaptation Drive Future Success

Success in the real estate business in Oman increasingly depends on companies' ability to adapt to changing consumer preferences and technological advancements. Incumbents are strengthening their market position through investments in digital platforms, sustainable building practices, and enhanced customer service capabilities. Market leaders are focusing on developing integrated communities that offer comprehensive lifestyle solutions, while also expanding their presence in emerging residential hotspots. The ability to offer flexible payment plans, maintain strong relationships with financial institutions, and provide value-added services has become crucial for maintaining market share. Companies are also investing in research and development to introduce innovative housing solutions that address evolving customer needs while maintaining cost efficiency.

For contenders looking to gain ground, success factors include developing niche market segments, forming strategic partnerships with established players, and leveraging technology for operational efficiency. The market shows moderate substitution risk, primarily from the rental segment, requiring developers to demonstrate clear value propositions for property ownership. Regulatory compliance, particularly in areas of sustainable development and foreign ownership, continues to shape market dynamics and competitive strategies. Companies that can effectively navigate government initiatives, such as the Sorouh program, while maintaining project quality and timely delivery, are better positioned for growth. The increasing focus on customer experience and after-sales service has become a critical differentiator in the market, with successful players investing in comprehensive property management solutions.

Oman Residential Real Estate Market Leaders

-

Al Mouj Muscat

-

Al Raid Group

-

Wujha Real Estate

-

Al-Taher Group

-

Maysan Properties SAOC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Oman Residential Real Estate Market News

- October 2022, Al Mouj Muscat launched phase 2 of Zunairah Mansions in the Shatti District. The new phase of the mansions comes in different styles and features six opulent bedrooms with a built-up area of 933 square meters, a garage, covered parking for up to six automobiles, and roomy servant quarters.

- April 2022, Oman Post and Asyad Express signed a partnership agreement with WUJHA Real Estate to invest, design, and develop land aligned with the land investment plan.

Oman Residential Real Estate Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Overview

- 4.2 Residential Real Estate Buying Trends, along with Socioeconomic and Demographic Insights

- 4.3 Government Initiatives and Regulatory Aspects

- 4.4 Insights into the Size of Real Estate Lending and Loan to Value Trends

- 4.5 Insights into Interest Rate Regime for General Economy and Real Estate Lending

- 4.6 Insights into Rental Yields in the Residential the Real Estate Sector

- 4.7 Insights into Capital Market Penetration and REIT Presence in the Residential Real Estate Sector

- 4.8 Insights into Affordable Housing Support provided by Government and Public-Private Partnerships

- 4.9 Impact of COVID-19 on the Market

- 4.10 Insights into Technology and Startups in the Real Estate Segment (Broking, Social Media, Facility Management, and Property Management)

5. Market Dynamics

- 5.1 Drivers

- 5.2 Restraints

- 5.3 Opportunities

-

5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products and Services

- 5.4.5 Intensity of Competitive Rivalry

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Apartments and Condominiums

- 6.1.2 Villas and Landed Houses

-

6.2 By Key Cities

- 6.2.1 Muscat

- 6.2.2 Dhofar

- 6.2.3 Musandam

7. COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

-

7.2 Company Profiles

- 7.2.1 Al Mouj Muscat

- 7.2.2 Al Raid Group

- 7.2.3 Wujha Real Estate

- 7.2.4 Al-Taher Group

- 7.2.5 Maysan Properties SAOC

- 7.2.6 Orascom Development Holding AG

- 7.2.7 Harbor Real Estate

- 7.2.8 Edara Real Estate LLC

- 7.2.9 Savills

- 7.2.10 Abu Malak Global Enterprises Muscat

- 7.2.11 Al Madina Real Estate Company Muscat

- 7.2.12 Better Homes

- 7.2.13 Coldwell Banker

- 7.2.14 Engel & Voelkers

- 7.2.15 Hilal Properties

- 7.2.16 Saraya Bandar Jissah*

- *List Not Exhaustive

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

9. APPENDIX

- 9.1 Macroeconomic Indicators (GDP breakdown by Sector, Contribution of Construction to the Economy, etc.)

- 9.2 Key Production, Consumption, and Exports and Import Statistics of Construction Materials

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Oman Residential Real Estate Industry Segmentation

Residential real estate is land built for people to live and cannot be utilized for commercial or industrial purposes. This happens when someone purchases land designated for residential use, which becomes real property and contains a wide range of potential homes, from houses to houseboats and neighborhoods ranging from the poorest slum to the wealthiest suburban development.

The residential real estate market in Oman is segmented by type (apartments and condominiums and villas and landed houses) and by key cities (Muscat, Dhofar, and Musandam). The report offers the market sizes and forecasts for the residential real estate market in Oman based on revenue in USD billion for the above segments.

A complete assessment of the residential real estate market in Oman includes an assessment of the economy and the contribution of sectors in the economy, a market overview, market size estimation for key segments, and emerging trends in the market segments in the report. Further, the report sheds light on the market trends like growth factors, restraints, and opportunities in this sector. The competitive landscape of the residential real estate market in Oman is depicted through the profiles of active key players.

| By Type | Apartments and Condominiums |

| Villas and Landed Houses | |

| By Key Cities | Muscat |

| Dhofar | |

| Musandam |

Need A Different Region or Segment?

Customize Now

Oman Residential Real Estate Market Research FAQs

How big is the Oman Residential Real Estate Market?

The Oman Residential Real Estate Market size is expected to reach USD 4.78 billion in 2025 and grow at a CAGR of 9.19% to reach USD 7.42 billion by 2030.

What is the current Oman Residential Real Estate Market size?

In 2025, the Oman Residential Real Estate Market size is expected to reach USD 4.78 billion.

Who are the key players in Oman Residential Real Estate Market?

Al Mouj Muscat, Al Raid Group, Wujha Real Estate, Al-Taher Group and Maysan Properties SAOC are the major companies operating in the Oman Residential Real Estate Market.

What years does this Oman Residential Real Estate Market cover, and what was the market size in 2024?

In 2024, the Oman Residential Real Estate Market size was estimated at USD 4.34 billion. The report covers the Oman Residential Real Estate Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Oman Residential Real Estate Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Oman Residential Real Estate Market Research

Mordor Intelligence provides a comprehensive analysis of the Oman residential real estate sector. We leverage our extensive expertise in real estate market analysis to deliver valuable insights. Our research examines property for sale in Oman, including freehold properties in Oman and various housing segments. The report offers detailed insights into Oman real estate companies and developers. It also tracks house prices in Oman and market dynamics across key regions like real estate Muscat and other major cities.

Stakeholders in the Oman real estate market can access detailed data on residential housing trends, property prices, and investment opportunities. The report, available as an easy-to-read PDF download, covers crucial aspects such as houses to rent in Oman and Oman apartments for sale. It includes a comprehensive analysis of real estate developers in Oman. Our research supports decision-making for investors, developers, and industry professionals. They can better understand property for sale in Muscat Oman and broader market dynamics, with a focus on residential property developments and emerging opportunities in the sector.