Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

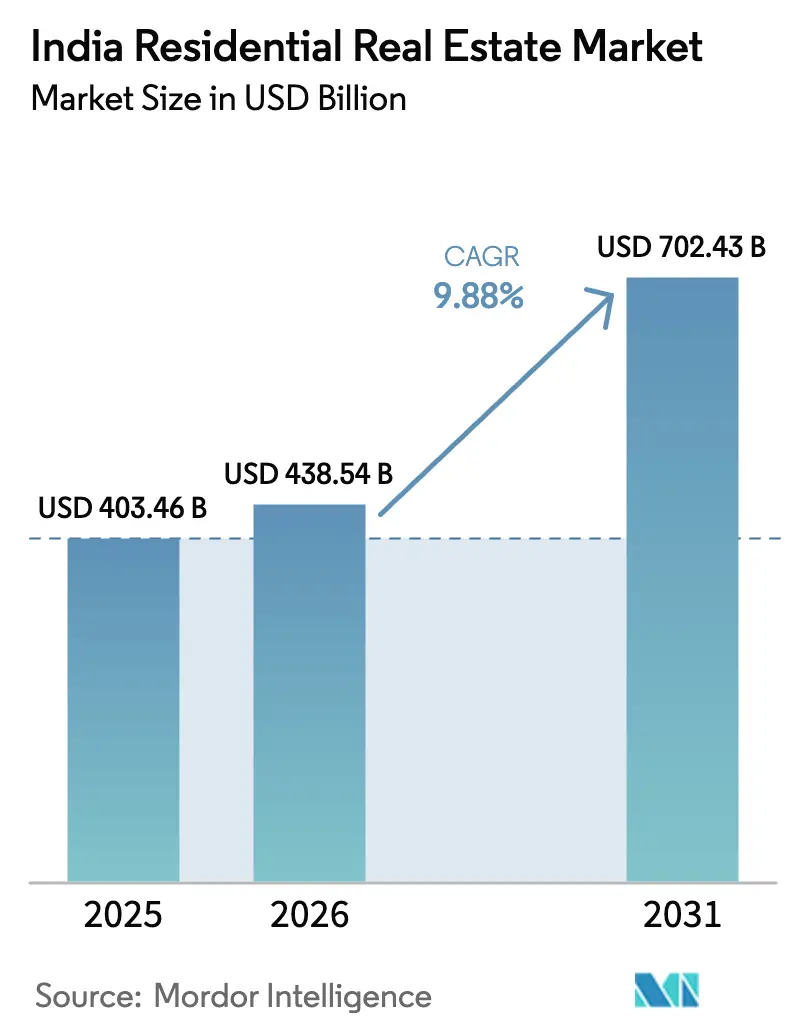

| Base Year Market Size (2025) | USD 403.46 Billion |

| Market Size (2026) | USD 438.54 Billion |

| Market Size (2031) | USD 702.43 Billion |

| Growth Rate (2026 - 2031) | 9.88% CAGR |

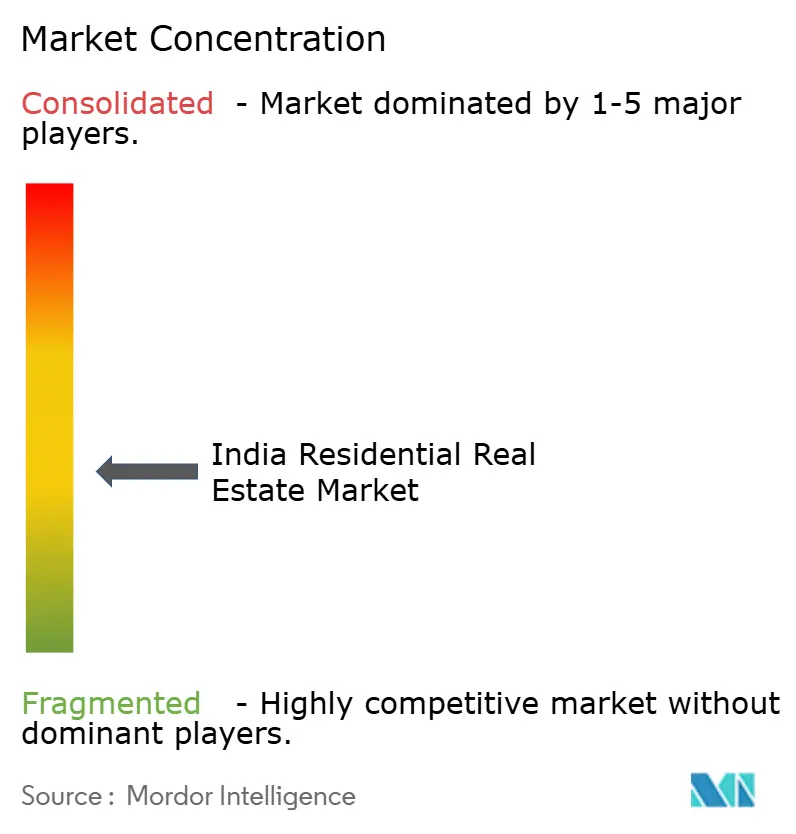

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Residential Real Estate Market Analysis by Mordor Intelligence

The India Residential Real Estate Market size is projected to be USD 403.46 billion in 2025, USD 438.54 billion in 2026, and reach USD 702.43 billion by 2031, growing at a CAGR of 9.88% from 2026 to 2031.

Demand is pivoting around easier mortgage terms after a 125-basis-point rate-cut cycle, the Union Budget’s green-home incentives, and a decisive shift of IT and Global Capability Center employment toward Tier-2 hubs. Completion-focused funds such as SWAMIH 2 and the Urban Challenge Fund are narrowing the affordable-housing deficit, while digitized land records shorten due diligence times for domestic and NRI buyers. Institutional capital continues to reshape the India residential real estate market through build-to-rent platforms and fractional-ownership vehicles that dilute traditional developer equity returns.

Key Report Takeaways

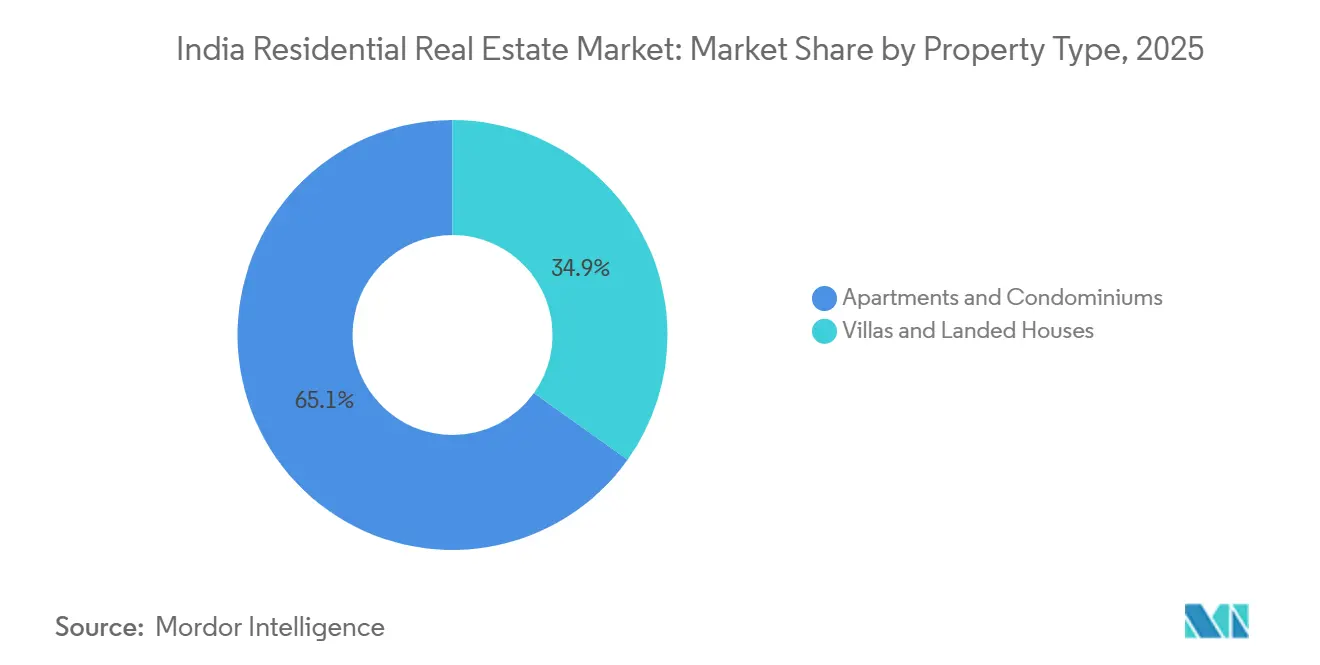

- By property type, apartments captured 65.14% of the Indian residential real estate market share in 2025, while villas and landed houses are forecast to grow at a 10.49% CAGR through 2031.

- By price band, the mid-market segment held 48.12% of the 2025 transaction value; the affordable segment is advancing at a 10.36% CAGR to 2031.

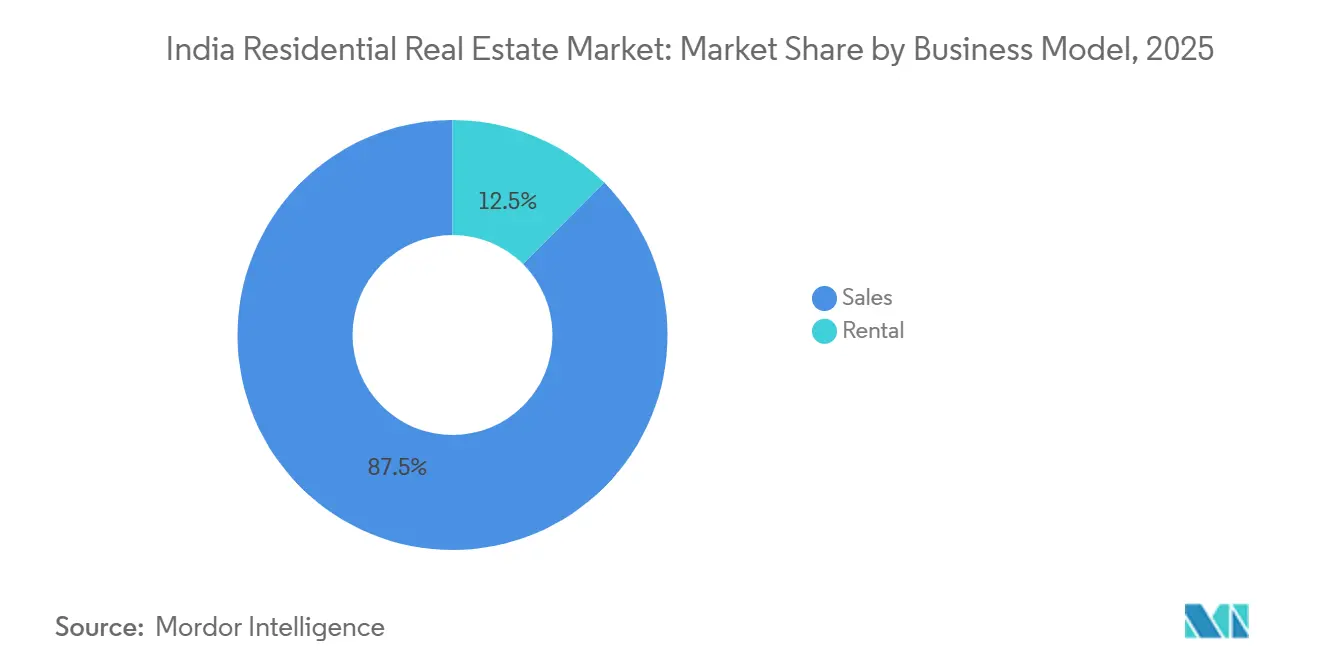

- By business model, the sales channel accounted for 87.54% of the 2025 value, yet rentals are projected to expand at a 10.70% CAGR through 2031.

- By mode of sale, primary transactions represented 63.67% of the 2025 value, while secondary transactions are set to rise at a 10.60% CAGR through 2031.

- By geography, the Rest of India, Tier-2, and Tier-3 cities captured 59.87% of the 2025 value; Hyderabad is the fastest-growing city with a 10.76% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RBI rate-cut cycle from Q4 2024 reinvigorating mortgage affordability across Tier-1 cities | +2.1% | Mumbai, Delhi-NCR, Bengaluru, Pune, Hyderabad, Chennai | Short term (≤ 2 years) |

| IT & GCC expansion into Tier-2 hubs unlocking fresh residential corridors | +1.8% | Coimbatore, Jaipur, Kochi, Visakhapatnam, Indore, Chandigarh | Medium term (2-4 years) |

| Near-completion of “Housing for All” targets releasing pent-up affordable demand | +1.6% | National (focus in Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan) | Long term (≥ 4 years) |

| Union Budget 2025 “green home” tax deductions accelerating sustainable unit launches | +1.5% | National (early gains in Bengaluru, Pune, Hyderabad) | Medium term (2-4 years) |

| API-based land-record digitization slashing NRI due-diligence timelines | +1.2% | National (early gains in Karnataka, Maharashtra, Tamil Nadu, Gujarat) | Short term (≤ 2 years) |

| Fractional ownership and REIT-lite platforms drawing millennial capital into premium projects | +1.0% | Mumbai, Bengaluru, Delhi-NCR, Pune, Hyderabad | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

RBI Rate-Cut Cycle From Q4 2024 Reinvigorating Mortgage Affordability Across Tier-1 Cities

The December 2025 repo cut to 5.25 % lowered average home-loan rates to 8.10 %, trimming monthly installments on a USD 60,000 loan by USD 385. Mortgage penetration in Tier-1 cities rose from 62 % in 2024 to 68 % in 2025 amid 422,765 unit sales[1]Ministry of Finance, “Union Budget 2025-26,” Indiabudget.gov.in . First-time buyers in the USD 60,000–120,000 bracket gain the most as banks pass through rate cuts within 90 days. The full demand impulse is set to coincide with the January-March 2026 purchase season when disbursements align with festival bonuses. Affordable EMI profiles are likely to keep the India residential real estate market on its projected growth trajectory.

IT & GCC Expansion into Tier-2 Hubs Unlocking Fresh Residential Corridors

Tier-2 cities added 187,000 new IT jobs in 2024, a 23 % jump that catalyzed housing launches within 10 km of new office clusters. Hyderabad’s 10.8 million sq ft office absorption and Pune’s 6.2 million sq ft reinforced sales spikes in Kokapet, Narsingi, Hinjewadi, and Kharadi. Lower land costs, often 35 % below Tier-1 averages, allow twin-bedroom units to be priced at USD 42,000–66,000. Single-window clearances in Tamil Nadu, Rajasthan, and Kerala have halved approval timelines, encouraging faster project rollouts. Sustained white-collar migration will keep the India residential real estate market anchored in these emerging corridors.

Near-Completion of “Housing for All” Targets Releasing Pent-Up Affordable Demand

PMAY-G has completed 2.82 million rural units, and PMAY-U has finished 91 lakh urban homes, together reaching 73 % of stated targets. The September 2024 launch of PMAY-U 2.0 earmarks 1 crore more units, enlarging an annual demand pool of almost 2 million households. States that dominate completions, Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan, still lack sufficient private supply in the USD 30,000–60,000 bracket, creating a structural gap. Interest subsidies up to USD 3,200 are available, yet awareness levels remain below 40 % in Tier-3 cities. Converting these latent buyers is vital for balanced growth within the India residential real estate market.

Union Budget 2025 “green home” tax deductions accelerating sustainable unit launches

The budget grants a USD 1,800 annual interest deduction on certified green homes in addition to the existing USD 2,400 cap, directly nudging high-income buyers toward IGBC- or LEED-rated projects[2]Indian Green Building Council, “Certified Residential Projects,” IGBC.in. Developers in Bengaluru, Pune, and Hyderabad fast-tracked 87 certified projects totaling 1.2 million sq ft in Q1 2026. The higher TDS threshold on rental income lowers compliance costs and could lift formal rental supply by 18% by 2028. Alignment with the Energy Conservation Building Code’s net-zero provisions further binds fiscal benefits to regulatory mandates. The result is a clear pipeline of green-tagged launches that will support premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peripheral micro-market inventory glut suppressing price appreciation | -1.10% | Delhi-NCR (Greater Noida West), Bengaluru (Yelahanka), Mumbai (Navi Mumbai periphery) | Medium term (2-4 years) |

| Skilled construction-labor diversion to infra megaprojects delaying completions | -0.90% | National (acute in Maharashtra, Uttar Pradesh, Karnataka, Tamil Nadu) | Medium term (2-4 years) |

| Potential FY 2026 capital-gains surcharge hikes discouraging short-term upgrades | -0.80% | National (higher impact in Mumbai, Delhi-NCR, Bengaluru) | Short term (≤ 2 years) |

| SEBI BRSR 2.0 ESG compliance costs squeezing mid-sized developer margins | -0.60% | National (listed developers in Mumbai, Bengaluru, Pune, Hyderabad) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Peripheral micro-market inventory glut suppressing price appreciation

Greater Noida West holds 47,000 unsold units, while Yelahanka carries 18,500, each representing more than 24 months of sales. Subvention schemes and assured buybacks dilute developer margins by up to 12 %. Lack of nearby Grade-A offices and slow infrastructure delivery reduces end-user demand. Similar oversupply in Navi Mumbai’s periphery confirms a pattern: distant micro-markets lag core zones on both price and absorption. Sticky inventory will act as a drag on the broader India residential real estate market pricing until cleared.

Skilled Construction-Labor Diversion to Infra Megaprojects Delaying Residential Completions

Bharatmala II and multiple metro builds absorbed 1.2 million skilled workers, hiking daily wages by roughly 20 % in 2024-25. Residential projects in Bengaluru, Pune, and Hyderabad face six-month delays as labor availability drops below 70 % of need. Higher mechanization offers relief but requires capital that small and mid-sized developers lack. The labor deficit is expected to persist until at least 2027, tightening project timelines. Completion delays undermine buyer trust and could inflate inventory-carrying costs within the India residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartment Dominance Drives Urban Density

Apartments accounted for a leading 65.14% of the India residential real estate market size in 2025, reflecting entrenched urban preferences for gated security and shared amenities[3]Economic Times, “Residential Sales and Office Absorption 2024,” Economictimes.indiatimes.com . Villas and landed houses are slated to expand at a 10.49% CAGR through 2031, surpassing apartments’ 9.6% pace as dual-income households prioritize private gardens and larger layouts. Bengaluru, Hyderabad, Pune, and Chennai captured 72% of villa demand, with projects such as Prestige City and Sobha Neopolis illustrating renewed developer focus on horizontal formats. Land scarcity keeps Mumbai and Delhi-NCR anchored to vertical stock, yet suburban corridors offer limited villa pockets financed by NRI capital inflows.

Developers launched 47 villa projects totaling 8,200 units during 2024-25, mainly on 50-plus-acre land parcels where economies of scale cushion construction costs. Customization flexibility, a clear title, and faster hand-overs offset the higher ticket sizes that average USD 220,000-430,000. Regulatory oversight under RERA has trimmed apartment delays, improving confidence, whereas villas often fall outside escrow mandates. Even so, lifestyle shifts and work-from-home norms ensure a stable pipeline for landed homes that will steadily enlarge their share of the India residential real estate market.

By Price Band: Mid-Market Stability Anchors Growth

The mid-market bracket of USD 60,000-180,000 held a dominant 48.12% share in 2025. Credit-linked subsidies, employer-assisted housing, and the RBI’s 125-basis-point easing cycle underpin demand stability. Affordable units under USD 60,000 are projected to grow at a 10.36% CAGR through 2031, buoyed by PMAY-U 2.0 and completion financing via SWAMIH 2. Developers had cut affordable launches by 54% in early 2025, chasing luxury margins; however, fresh government funds are pushing brownfield completions in high-deficit states.

Luxury units above USD 180,000 formed 42% of H1 2026 launches, led by DLF, Oberoi Realty, and Macrotech projects. Equities-driven wealth creation and NRI repatriation uphold this segment even as higher capital-gains levies loom. Future demand hinges on green-home tax deductions and branded-residence appeal, cushioning luxury prices. The dual-track trend keeps the India residential real estate market well diversified across income cohorts.

By Business Model: Sales Dominance Reflects Ownership Preferences

Sales transactions represented 87.54% of 2025 market value, underscoring a cultural bias toward ownership and tax incentives such as Section 24(b). Rental transactions are forecast to rise at a 10.70% CAGR through 2031, propelled by institutional build-to-rent capital worth USD 3 billion and the co-living expansion by operators like Stanza Living. Bengaluru leads with a 4.45% gross yield, while Mumbai and Gurugram hover near 4.1%.

The increased TDS threshold on rental income and growing professional management are expected to raise formal supply by nearly one-fifth by 2028. Still, sales will remain sizable because of inter-generational wealth planning and mortgage tax shields. The healthy coexistence of both channels supports liquidity and portfolio diversification across the India residential real estate market size spectrum.

By Mode of Sale: Primary Market Leadership Signals New Supply Confidence

Primary sales made up 63.67% of 2025 value thanks to 390,000 new launches and stronger RERA enforcement. Secondary deals are set to climb at a 10.60% CAGR, moving from 43% of unit volumes in 2025 toward almost half the market by 2031. Digitized land records that verify titles in hours rather than weeks have increased buyer confidence in ready-to-occupy stock.

States such as Karnataka and Maharashtra captured 62 % of resale value, aided by NRI interest. Fractional-ownership platforms now curate premium resale inventory, easing exit options for early buyers. Faster capital churn in the resale space will keep liquidity healthy and broaden participation in the India residential real estate market.

Geography Analysis

Hyderabad leads growth prospects, clocking a forecast 10.76% CAGR through 2031 as 10.8 million sq ft of 2024 office absorption translates into brisk housing demand in Kokapet, Narsingi, and Financial District micro-markets. Steady infrastructure, Outer Ring Road upgrades, and the 56-km metro Phase II operational by late 2025 will reduce commute times and lift mid-market ticket prices to USD 82 per square foot. Bengaluru, Mumbai, and Delhi-NCR still aggregate 40.13% of value, yet diverge in momentum: Bengaluru enjoys 8-10% annual price rises in Whitefield, while Mumbai’s land scarcity pushes developers toward vertical redevelopments financed by GIC and Blackstone. Delhi-NCR’s Greater Noida West inventory glut exceeds 24 months of sales, holding price growth to a modest 3-4% and prompting subvention schemes that erode developer margins.

Pune occupies a stable 12% share of national transactions; its Hinjewadi and Kharadi corridors command premiums of USD 14-22 per square foot over peripheral locations thanks to sustained IT leasing. Chennai’s OMR stretch logs 7-9% annual appreciation on the back of automotive and pharma expansion, although its 3.85% rental yield trails Bengaluru’s 4.45%, reflecting slower job creation. Ahmedabad and Kolkata combine for 8% of value, characterized by lower ticket sizes around USD 54,000 that attract first-time owners. The migration of IT and GCC roles to Coimbatore, Jaipur, Kochi, Visakhapatnam, Indore, and Chandigarh keeps Tier-2 cities prominent; their land costs run 30-40% below Tier-1 averages, enabling 2-bedroom units at USD 42,000-66,000.

State RERA enforcement shapes momentum: MahaRERA’s stringent escrow and reporting norms have cut delays by 28% since 2019, whereas UP-RERA’s capacity gaps permit project extensions in 40% of delayed schemes. Affordable-band shortages persist in states like Uttar Pradesh and Bihar despite PMAY progress, spurring brownfield redevelopment via SWAMIH 2. Across metros and emerging hubs alike, land parcels within 3 km of operational metro stations secure premiums up to 60%, reinforcing the transit-oriented development thesis that underpins sustained expansion of the India residential real estate market.

Competitive Landscape

The top 10 developers captured just 18% of national unit sales in FY 2025, underlining a fragmented field where regional specialists and unorganized builders still dominate. Brands such as DLF, Godrej Properties, Prestige, Macrotech, and Brigade leverage institutional capital and green certifications to win city-center parcels, enabling 8-12% price premiums in luxury formats. Mid-caps like Casagrand and Total Environment lean on local land banks but feel a tighter squeeze from rising ESG costs and labor-rate inflation. SEBI’s BRSR 2.0 framework increases reporting overhead yet enhances buyer trust, favoring scaled players over smaller peers.

Institutional money reshapes balance sheets. Singapore’s GIC invested USD 504 million alongside DLF for a Gurugram luxury project in February 2025, demonstrating foreign appetite for marquee developments. Fractional platforms Strata, PropShare, and hBits pooled USD 300 million in 2024-25, lowering entry barriers and compressing developer equity timelines. SM-REIT guidelines promise USD 1.2 billion of new liquidity by 2027, potentially providing mid-tier builders with alternatives to high-cost private debt. Early tech adopters such as Godrej and Macrotech use virtual tours and AI-driven lead scoring to cut sales cycles by up to 20%, setting benchmarks peers must follow.

Green certification uptake remains an opportunity. IGBC’s 412-million-sq-ft residential portfolio represents less than 15 % of new annual launches, yet Union Budget tax perks have pushed Prestige, Oberoi Realty, and Kolte-Patil to fast-track Platinum ratings. Rising buyer awareness about operating-cost savings may widen demand for certified stock. As compliance outlays, land scarcity, and customer expectations converge, market share should gravitate toward transparent, well-capitalized entities, steadily reshaping the competitive contours of the India residential real estate market.

India Residential Real Estate Industry Leaders

Godrej Properties

Prestige Estate

DLF

Phoenix Mills

L&T Realty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Godrej Properties unveiled Godrej MSR City, a 40-acre Bengaluru mixed-use township slated to earn USD 420 million in sales while targeting IGBC Platinum status.

- March 2025: Godrej Properties launched Godrej Riverine in Noida, banking on the new metro extension and faster NRI title verification.

- February 2025: DLF and GIC formed a joint venture for a USD 504 million luxury project on Gurugram’s Golf Course Road.

- January 2025: Macrotech bought a 25-acre Wadala parcel for USD 222 million, planning a 2,400-unit vertical community.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Indian residential real-estate market comprises all newly built or existing housing units, apartments, condominiums, villas, and plotted houses traded for owner-occupation or personal rental within the country's legal residential zones. Activity spans primary launches, secondary resales, and lease transactions denominated in Indian rupees and converted to constant 2025 US dollars for comparability.

Scope exclusion: Second-home investments located outside India and informal self-built dwellings remain outside this study.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing Home Resale)

- By Geography

- Bengaluru

- Mumbai

- Delhi-NCR

- Hyderabad

- Pune

- Chennai

- Ahmedabad

- Kolkata

- Rest of India

Detailed Research Methodology and Data Validation

Primary Research

We interview developers, housing finance officers, brokerage heads, and buyers' associations across eight metros and select Tier II cities. Conversations test absorption assumptions, typical ticket sizes, land cost shifts, and sentiment on interest rate moves, enabling us to fine-tune supply elasticity and buyer affordability curves.

Desk Research

Our analysts first collate macro inputs such as national accounts, household income tables, and repo rate trends from the Reserve Bank of India, Ministry of Housing & Urban Affairs, and National Housing Bank. City-level launch and absorption grids are gathered from Knight Frank, JLL, and CREDAI releases, while registration data and stamp duty collections are pulled from state revenue portals for price validation. Company filings and quarterly investor decks flesh out developer pipelines. Paid databases like D&B Hoovers and Dow Jones Factiva supply historical revenue series and news on major builders.

These sources are illustrative only; many additional public records, trade journals, and proprietary datasets are reviewed for cross-checks.

Market-Sizing & Forecasting

A top-down build begins with urban household counts, income cohorts, and savings ratios to size the potential demand pool, which is then filtered through mortgage eligibility and prevailing penetration rates. Results are cross-verified through bottom-up roll-ups of reported unit sales by the twenty largest developers and sampled average selling prices. Key variables include housing loan growth, new project approvals, unsold inventory months, cement price inflation, and repo rate changes. Forecasts deploy a multivariate regression linking unit launches, credit cost, and GDP per capita to achieved sales, with scenario checks around policy incentives such as PMAY U extensions.

Data Validation & Update Cycle

Every model run passes three layers: automated variance flags, peer review, and a lead analyst sign-off. Outputs are reconciled with fresh launch tallies and registration figures before publication. Mordor refreshes the dataset each year, issuing interim updates when policy shocks, rate moves, or material project cancellations arise.

Why Our India Residential Real Estate Baseline Commands Reliability

Published market values often diverge because firms pick different transaction scopes, price index bases, and refresh cadences.

We acknowledge those disparities upfront.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 399.11 B (2025) | Mordor Intelligence | - |

| USD 258 B (2024) | Regional Consultancy A | Excludes secondary market resales and applies 2024 exchange rates |

| USD 36 020 B (2024) | Trade Journal B | Aggregates land transactions and commercial plots under residential tag |

In sum, Mordor's disciplined scope definition, dual track modeling, and annual refresh yield a balanced, transparent baseline that decision makers can trace to clearly stated variables and reproducible steps.

Key Questions Answered in the Report

How large is the India residential real estate market in 2026?

The India residential real estate market size stands at USD 438.54 billion in 2026 and is projected to reach USD 702.43 billion by 2031.

Which city is expected to grow the fastest to 2031?

Hyderabad leads with a forecast CAGR of 10.76% on the back of strong office absorption and pharma-sector expansion.

What policy supports affordable housing demand?

PMAY-U 2.0, launched in September 2024, targets 1 crore additional urban units and offers interest subsidies up to USD 3,200 for eligible buyers.

How are green-home incentives influencing new launches?

Union Budget 2025 introduced an extra USD 1,800 interest deduction for certified green homes, prompting 87 IGBC-rated projects in Q1 2026 alone.

Page last updated on: