Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

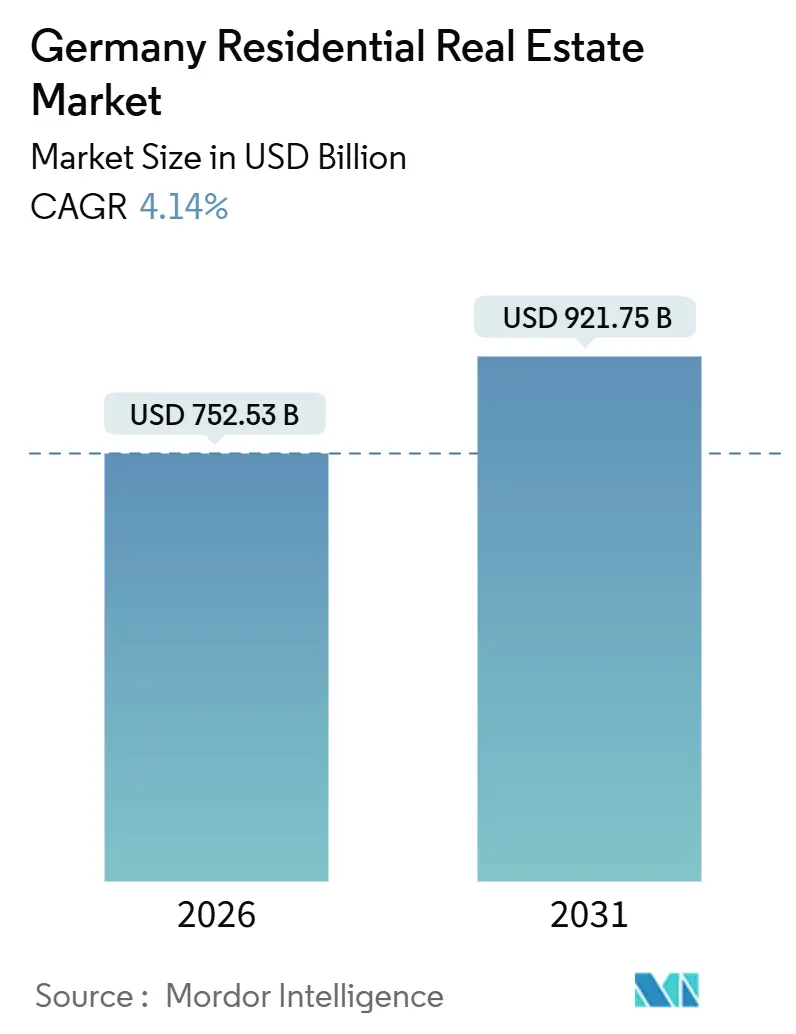

| Market Size (2026) | USD 752.53 Billion |

| Market Size (2031) | USD 921.75 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Residential Real Estate Market Analysis by Mordor Intelligence

The Germany real estate market size stands at USD 752.53 billion in 2026 and is projected to reach USD 921.75 billion by 2031, reflecting a 4.14% CAGR, underpinned by stringent energy-efficiency mandates, net-migration inflows, and modular-construction innovation[1]European Commission, “Energy Performance of Buildings Directive,” energy.ec.europa.eu. Institutional investors rotate capital toward retrofit-ready multifamily stock, while suburban households pivot to villas that promise energy autonomy and garden space. Affordable-housing stimulus worth USD 19.8 billion through 2027 accelerates social-rental starts and narrows the supply gap for lower-income renters [2]Federal Ministry for Housing, Urban Development and Building, “Social Housing,” bmwsb.bund.de. Mortgage-rate relief from 4.2% in 2023 to 3.3% in 2025 improves first-time-buyer affordability, yet rates above 3.5% still temper demand in Munich and Hamburg. Proptech adoption scales quickly as landlords deploy smart-metering and predictive-maintenance tools to lift net operating income and satisfy corporate green-lease clauses.

Key Report Takeaways

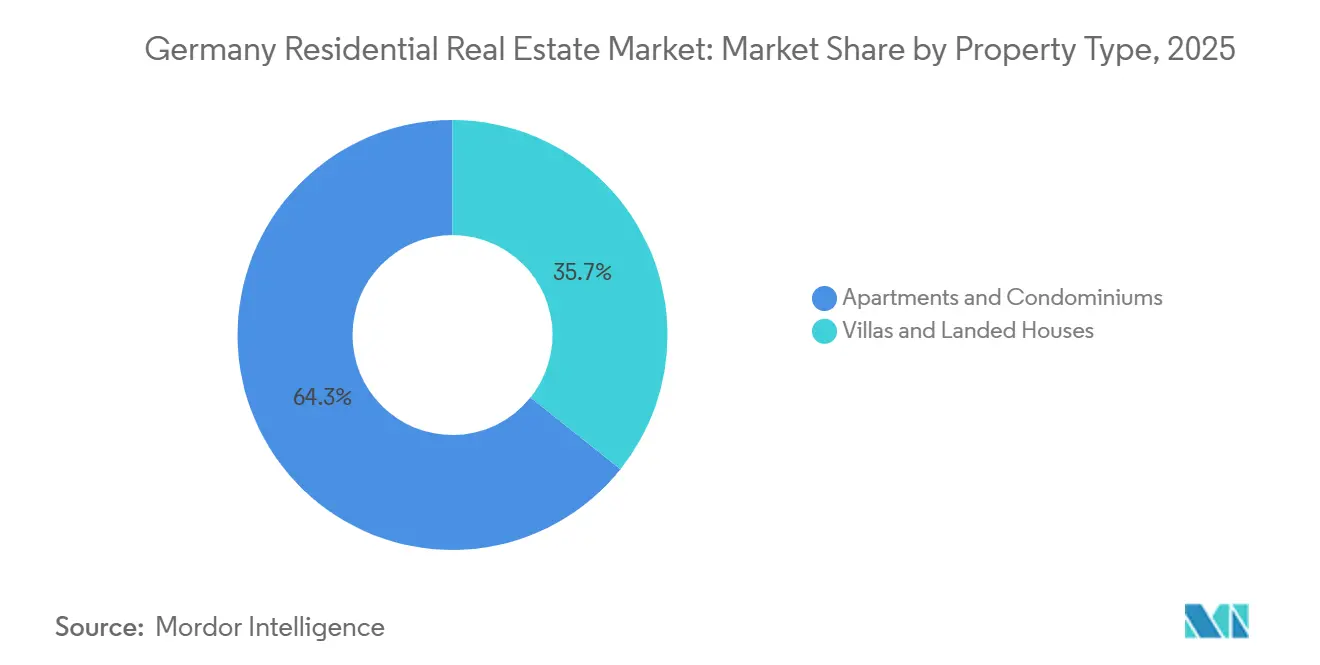

- Apartments and condominiums captured 64.26% of 2025 transaction value, whereas villas and landed houses are forecast to expand at a 5.19% CAGR through 2031.

- Mid-market units held 46.26% of spending in 2025, but the affordable tier is poised for a 5.22% CAGR under the Housing for All program.

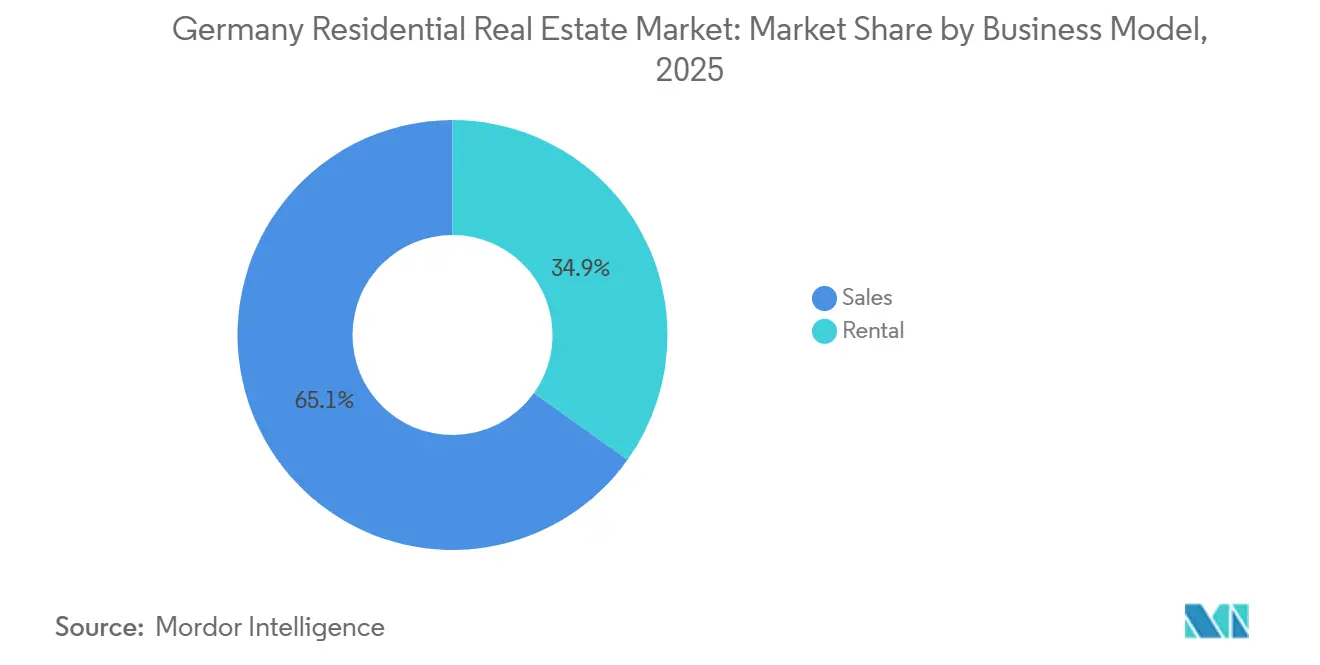

- Sales still represented 65.14% of activity in 2025, yet rental portfolios will rise at a 5.39% CAGR as institutions prize yield stability.

- Secondary-market resales commanded 70.14% of deals in 2025, while primary new-build transactions are projected to post a 5.43% CAGR on faster permitting.

- Berlin led with a 13.94% 2025 market share, and Leipzig is set to achieve the fastest city-level growth at a 5.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USD 19.8 billion Housing for All program | +0.9% | Leipzig, Cologne, Düsseldorf social zones | Short term (≤ 2 years) |

| EPC class D upgrade mandate | +0.8% | Berlin, Hamburg, Munich legacy stock | Medium term (2–4 years) |

| Mortgage rate rollback | +0.7% | National secondary cities | Short term (≤ 2 years) |

| Skilled Immigration Act reforms | +0.6% | Berlin, Munich, Frankfurt tech hubs | Medium term (2–4 years) |

| AI enabled modular construction | +0.5% | Hamburg, Leipzig, Düsseldorf | Medium term (2–4 years) |

| Corporate green lease clauses | +0.4% | Berlin, Munich, Frankfurt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

USD 19.8 Billion Housing for All Program Fast-Tracking Affordable Starts

Germany's federal government has pledged USD 19.8 billion to the "Housing for All" initiative through 2027. Annual funding will rise from USD 4.4 billion in 2026 to USD 6.0 billion in 2028. The initiative supports affordable housing via direct grants, low-interest public financing, and faster permitting, reducing approval timelines in pilot municipalities from 18 months to 9 months. The stimulus offsets a 105,000-unit national supply shortfall recorded in 2024, narrowing vacancy and stabilizing rents for 38% of renter households inside the income-eligibility band. Accelerated nine-month permitting cycles lower holding costs and enable modular suppliers to scale volume. Persistent fiscal backing through 2031 should sustain double-digit build rates in designated social-housing corridors.

EPC-Class-D Upgrade Mandate Catalyzing Deep Retrofits

Germany adopted the EU Energy Performance of Buildings Directive in mid-2025, compelling every home to reach at least Class D by 2033, an obligation that redirects USD 273 billion toward insulation, heat pumps, and smart thermostats. Vonovia earmarked USD 1.6 billion in 2024 to modernize 40,000 apartments a year, illustrating the capital shift toward green compliance[3]Vonovia SE, “Annual Report 2024,” vonovia.de. Pre-1990 units, 60% of which are rated below Class D, dominate Berlin and Ruhr portfolios and face elevated retrofit risk. Landlords weighing hefty upgrades or strategic disposals create a vibrant secondary-trading arena for specialist retrofit funds. The mandate, therefore, supports contractors, equipment makers, and ESG-linked financiers while raising entry hurdles for non-compliant stock.

Mortgage-Rate Rollback Unlocking First-Time Buyers

Fixed mortgage costs fell to 3.3% by mid-2025, trimming monthly payments on a USD 327,000 loan by USD 324 relative to 2023. Transaction counts in the USD 218,000–USD 436,000 price band rebounded 18% year-on-year, with Leipzig and Dresden booking the largest volume gains. Nevertheless, Munich and Hamburg remain unaffordable for average earners, implying a two-speed owner-occupier recovery. If rates dip toward 3% by 2027, pent-up demand from 180,000 households could propel additional sales, particularly in secondary cities where prices sit below USD 381,000.

Skilled-Immigration-Act Reforms Intensifying Rental Pressure

Streamlined visa pathways admitted 75,000 skilled workers in 2024, pushing Berlin and Munich vacancy rates below 2%. Median listing periods compressed to under two weeks, prompting landlords to automate tenant onboarding. Furnished units with fiber and IoT sensors fetch 8-12% rent premiums, a clear reward for ESG-certified assets. Corporate relocation clusters amplify the bifurcation between smart, green stock and legacy buildings. Sustained inflows will keep upward pressure on rents and underpin rental-yield resilience in tech corridors.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated 3.5% mortgage plateau | −0.9% | Munich, Hamburg, Stuttgart | Short term (≤ 2 years) |

| Timber and insulation price volatility | −0.6% | Bavaria, Baden-Württemberg | Medium term (2–4 years) |

| 2025 skilled labor wage hike | −0.5% | Berlin, Hamburg, Rhine-Ruhr | Short term (≤ 2 years) |

| Draft Airbnb caps | −0.3% | Berlin, Munich, Hamburg, Cologne | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

ECB Mortgage Plateau Weighing on Buyer Affordability

Ten-year fixed loans averaged 3.5% in late 2025, nearly double 2021 levels, lifting monthly payments above 40% of gross income for Munich properties priced at USD 708,000. Sales volumes in the USD 545,000-plus bracket fell more than one-fifth year-on-year. Developers face higher interest carry, adding up to USD 27,000 per unit, which compresses profit or inflates listing prices. Unless rates retreat toward 3% by 2027, premium-city owner-occupier momentum will lag the broader German real estate market recovery.

Material-Cost Volatility Squeezing Developer Margins

Timber swung between USD 196 and USD 262 per m³ in 2024-2025, while insulation costs jumped 12-18% on energy inflation. Mid-tier builders, lacking hedging scale, absorbed 8-12% margin erosion on fixed-price contracts. Thirty-four percent postponed land bids, delaying roughly 18,000 units. Large incumbents counteract volatility through multi-year supply agreements, but sustained swings could still shave 60 basis points off Germany real estate market CAGR through 2031.

Segment Analysis

By Property Type: Apartments Retain Urban Lion’s Share While Villas Drive Growth

Apartments and condominiums commanded 64.26% of the 2025 transaction value, underlining their entrenched role in dense metros that restrict greenfield land. The Germany real estate market size tied to villas and landed houses is forecast to expand at a 5.19% CAGR through 2031, lifted by home-office adoption and rooftop-solar self-sufficiency. Institutional portfolios remain apartment-heavy, with Vonovia’s 548,000 units 92% multifamily and LEG Immobilien’s 167,000 entirely flats, ensuring ample liquidity for urban assets. Leipzig and Dresden record brisk villa absorption, where USD 416,000 prices undercut Munich by 40%, widening the suburban affordability gap.

Energy autonomy fuels villa desirability, as 58% of single-family completions in 2025 included photovoltaic arrays compared with 12% of multifamily deliveries. The EPC mandate penalizes high-rise retrofits that cost USD 27,000-USD 38,000 per unit, nudging capital toward new-build townhouses in exurban belts. Apartment demand still stays solid in Berlin, Hamburg, and Frankfurt, where transit connectivity trumps space considerations, but rental premiums increasingly accrue to EPC-compliant towers outfitted with smart-home dashboards.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Price Band: Mid-Market Dominates Spend as Affordable Tier Accelerates

Mid-market homes captured 46.26% of 2025 spend, reinforced by Germany’s large cohort earning USD 43,600-USD 87,200. The affordable tier will outpace with a 5.22% CAGR through 2031 on the back of Housing for All subsidies and discounted municipal land parcels. Leipzig, Cologne, and Düsseldorf spearhead volume, offering developers 30-40% land rebates in exchange for 25-year rent caps. Luxury transactions cooled 14% year-on-year in 2025 as buyers awaited rate clarity and wealth-tax negotiations.

TAG Immobilien’s purchase of 1,200 affordable units in Leipzig and Chemnitz illustrates capital rotation into the subsidy-anchored bracket, funded partly by 1.8% KfW loans. Mid-market economics tighten, as USD 2,980 per m² build costs leave slim margins when buyers resist prices above USD 436,000. Consequently, developers embrace modular factories and bulk procurement to defend profitability, a trend likely to widen between tech-enabled builders and small family firms.

By Business Model: Rentals Gain Momentum despite Sales Supremacy

Sales still represented 65.14% of 2025 market value, yet rentals are on track for a 5.39% CAGR through 2031, benefiting from Germany’s 54% renter share and institutions hungry for inflation-indexed yield. Vonovia booked USD 2.3 billion in rental income in the first nine months of 2024, achieving 3.8% like-for-like rent growth despite Berlin rent caps. The Germany real estate market share of institutional rentals is likely to rise as pension funds and insurers bulk-buy multifamily blocks to match long-dated liabilities.

Mortgage arithmetic favors renting in premium hubs: a USD 436,000 condo costs USD 1,780 per month to service at 3.5% interest, compared with USD 1,200 median rent for a comparable flat. Leipzig, Dresden, and Erfurt nevertheless register brisk owner-occupier take-up where entry prices sit below USD 381,000 and expected appreciation of 5-7% underpins equity returns. Over the forecast window, a balanced tenure mix emerges, with rental portfolios densifying in metros and sales thriving in secondary growth belts.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Mode of Sale: Secondary Resales Prevail but New Builds Accelerate

Secondary resales accounted for 70.14% of 2025 transactions, a legacy of Germany’s aging housing stock where 78% of units predate 2000. Primary new-build sales will grow at a 5.43% CAGR to 2031, propelled by nine-month permitting under Construction Turbo rules and consumer preference for warranty and EPC compliance. Leipzig, Düsseldorf, and Frankfurt lead permit issuance as population growth tops 1.2% annually.

Ancillary transaction costs of 8-15% keep resale velocity muted, yet the EPC mandate will force sellers to invest USD 32,000-USD 54,000 in energy upgrades before listing, shrinking the resale price advantage. Vonovia’s delivery of 1,000 smart, Class A apartments in 2024 signals rising appetite for turnkey units that circumvent retrofit headaches. Modular delivery, with 14-month cycle times, feeds pipeline resilience, suggesting the German real estate market size attributable to new builds will steadily erode the resale share.

Geography Analysis

Berlin held 13.94% of 2025 market value, buoyed by a 3.7 million population and average rents of USD 17.18 per m², up 12% year-on-year. Vacancy tightened to 2.1% after Skilled-Immigration-Act flows, prompting municipal debates on stricter rent caps. Short-term rental returns deteriorated under an eight-week annual limit, steering investors toward long-lease multifamily assets equipped with carbon dashboards.

Munich and Hamburg command premium valuations of USD 708,000 and USD 566,000 median prices, respectively, yet sales volumes slipped 18-22% in 2025 as 3.5% mortgage rates eroded affordability. Both cities cap Airbnb stays at 90 days or mandate costly permits, reinforcing institutional dominance in regulated, high-occupancy portfolios. Frankfurt’s 75,000 finance jobs anchor 12,000 corporate-rental units, many under green-lease clauses that demand smart-meter rollouts.

Leipzig is projected to deliver the fastest 5.48% CAGR through 2031, fueled by net in-migration and USD 437 million in Housing for All subsidies. Median homes remain 57% cheaper than in Berlin, attracting first-time buyers and proptech landlords. Cologne, Düsseldorf, and the wider Rhine-Ruhr benefit from logistics corridors and airport connectivity, while secondary hubs such as Nuremberg and Dresden lure equity-minded households with USD 350,000 entry points and 4-6% appreciation.

Competitive Landscape

Market concentration remains moderate as the top five landlords own under 4% of Germany’s 23 million rental units. Vonovia, after the USD 2.5 billion purchase of 18,000 apartments in November 2025, controls 566,000 units and channels USD 1.6 billion annually into retrofit and modular-build programs. LEG Immobilien, focused on North Rhine-Westphalia, financed a USD 655 million green bond to upgrade 50,000 flats, demonstrating the funding edge of ESG issuers.

Mid-cap players prune peripheral holdings to recycle capital into growth corridors. Grand City Properties sold 3,200 non-core units for USD 459 million, redeploying proceeds into Berlin and Düsseldorf, where rent spreads exceed 200 basis points. TAG Immobilien partners with Kaufmann Bausysteme on 1,500 modular affordable apartments, cutting build costs 18% and aligning with subsidy thresholds.

Proptech challengers target fragmented ownership. Platforms offering AI-based maintenance scheduling and blockchain lease contracts claim 20-30% cost savings for landlords with fewer than 50 units. Municipal landlords such as SAGA Hamburg and Degewo leverage subsidized debt but lag in digitization, leaving scope for tech-service outsourcing. Regulatory guidance on tokenized fractional ownership remains a hurdle, yet the innovative capital channel could broaden retail access once prospectus thresholds clarify.

Germany Residential Real Estate Industry Leaders

Vonovia SE

Deutsche Wohnen SE

LEG Immobilien SE

Consus Real Estate

SAGA Unternehmensgruppe Hamburg

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Vonovia SE agreed to acquire 18,000 apartments across Berlin, Hamburg, and Leipzig for USD 2.5 billion, expanding presence in sub-2.5% vacancy districts.

- September 2025: LEG Immobilien SE closed a USD 655 million green bond, earmarked for heat pumps, insulation, and smart meters across 50,000 apartments.

- July 2025: TAG Immobilien AG and Kaufmann Bausysteme launched a USD 306 million modular scheme for 1,500 affordable apartments in Leipzig and Chemnitz.

- March 2025: Patrizia SE opened a USD 546 million open-ended fund targeting EPC-Class-B or better German residential stock.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the German residential real estate market as the aggregated monetary value of land and permanently constructed dwellings intended for private habitation, across single-family, multi-family, and mixed-use buildings that hold a majority residential share. According to Mordor Intelligence, rental flows and owner-occupied housing stock are covered alongside new-build and resale transactions to present a full-economy view.

Scope exclusion: temporary lodging such as serviced apartments or student dormitories is not quantified here.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing Home Resale)

- By Geography

- Berlin

- Hamburg

- Munich

- Cologne

- Frankfurt

- Dusseldorf

- Leipzig

- Rest of Germany

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and online surveys with residential brokers, planning officers, institutional landlords, and prop-tech lenders across Berlin, Munich, Frankfurt, and secondary cities helped us validate absorption rates, typical price per square meter, and rental escalation assumptions, ensuring regional nuances funnel into the national model.

Desk Research

Mordor analysts began with federal datasets such as Destatis dwelling completions, BaFin mortgage volumes, and Bundesbank property price indices, which were then cross-read with Eurostat urbanization statistics and German Construction Federation permit logs. We enriched gaps through trade bodies like the German Property Federation (ZIA) and peer-reviewed journals on housing affordability. Paid resources, notably D&B Hoovers for developer financials and Dow Jones Factiva for capital-market activity, supplied firm-level metrics that public sources missed. This list is illustrative; many further publications, filings, and customs extracts informed the desk phase.

Market-Sizing & Forecasting

A top-down model converts dwelling stock and average market price into a 2025 baseline, while selective bottom-up checks of developer revenues and sampled average selling price times units keep totals grounded. Key drivers include building permits issued, completion delays, median mortgage rates, net migration, vacancy levels, and the Mietspiegel rental index, which together explain demand and price tension. Forecasts employ multivariate regression with scenario overlays, letting us stress test interest-rate or immigration shocks before producing the 2030 outlook.

Data Validation & Update Cycle

Outputs pass multi-source checks, variance flags, and senior analyst review. Reports refresh yearly, with interim updates triggered by policy shifts or macro surprises, so clients receive numbers that remain current.

Why Mordor's Residential Real Estate Market In Germany Size & Share Analysis Baseline Commands Reliability

Published estimates often diverge because firms choose different asset scopes, price proxies, and refresh rhythms.

Key gap drivers include whether stock or transaction value is measured, how resale housing is treated, and if rental income streams are capitalized. Mordor selects a balanced scope, applies transparent variable layering, and updates annually, which keeps our baseline dependable for investors and policymakers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 722.61 B (2025) | Mordor Intelligence | - |

| EUR 29.6 T (2024) | Global Consultancy A | Captures total asset stock, minimal macro driver layering |

| USD 12.6 B (2024) | Industry Analyst B | Focuses new-build transactions only, excludes existing stock and rentals |

The comparison shows that, by selecting the right scope and grounding forecasts in verified housing, financing, and demographic variables, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can retrace and replicate.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Germany real estate market and its forecast growth?

The Germany real estate market size is USD 752.53 billion in 2026 and is expected to climb to USD 921.75 billion by 2031, growing at a 4.14% CAGR.

How will EPC mandates affect property investment strategies in Germany?

The EPC Class D requirement redirects about USD 273 billion into retrofits, making green-compliant assets more valuable and prompting landlords to modernize or divest older stock.

Which German city is forecast to grow fastest through 2031?

Leipzig is projected to lead with a 5.48% CAGR, driven by net in-migration, affordable entry prices, and Housing for All funding.

Why are rentals gaining ground over sales transactions?

Elevated mortgage costs, institutional demand for yield, and Germany’s 54% renter population are propelling rental portfolios to a 5.39% CAGR, outpacing sales growth.