Residential Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

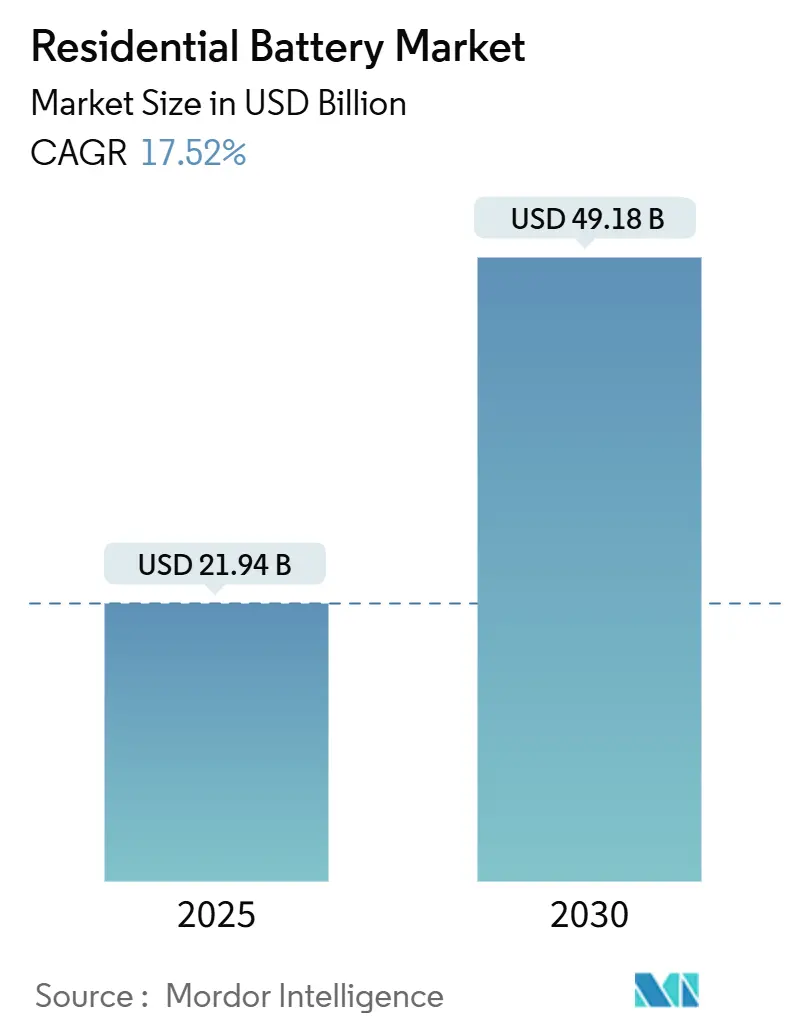

| Market Size (2025) | USD 21.94 Billion |

| Market Size (2030) | USD 49.18 Billion |

| Growth Rate (2025 - 2030) | 17.52% CAGR |

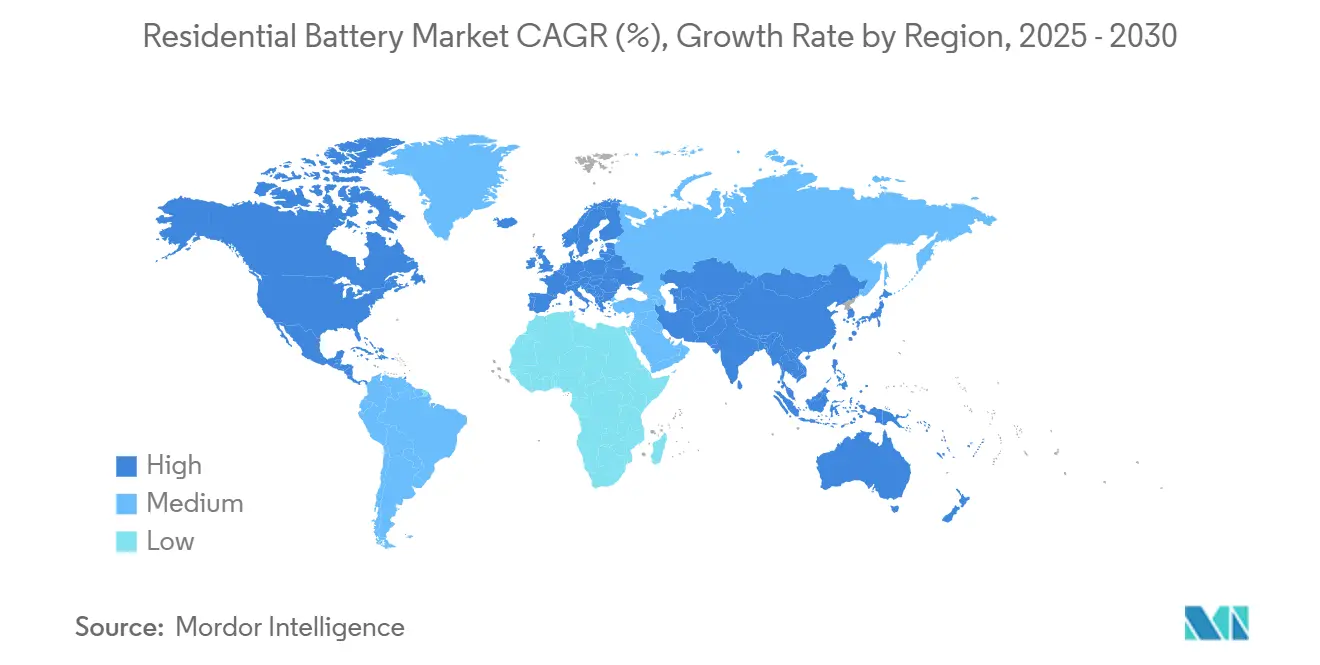

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

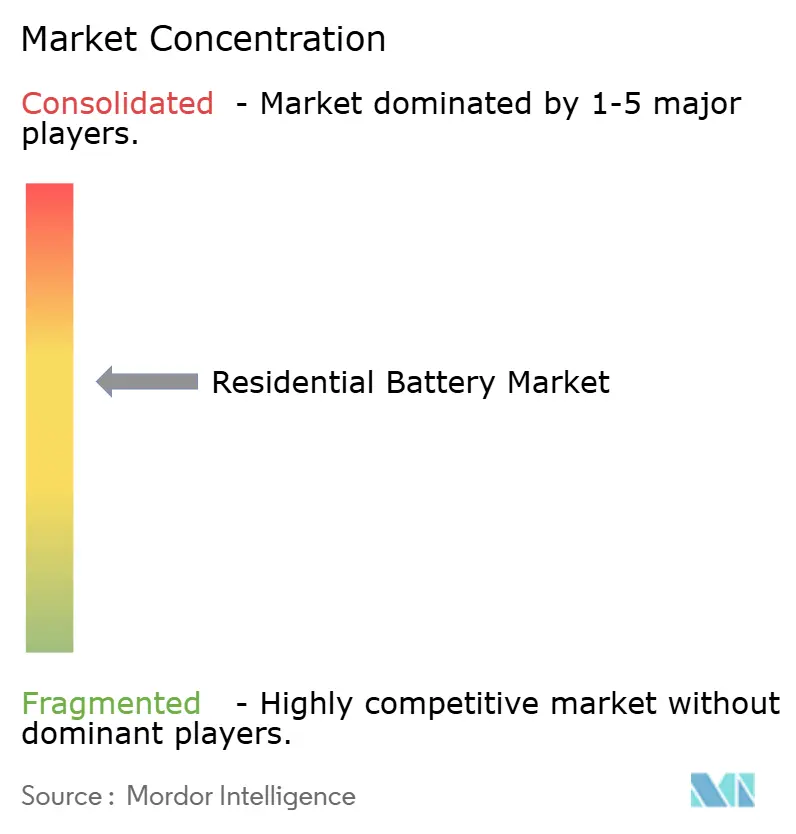

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Residential Battery Market Analysis by Mordor Intelligence

The Residential Battery Market size is estimated at USD 21.94 billion in 2025, and is expected to reach USD 49.18 billion by 2030, at a CAGR of 17.52% during the forecast period (2025-2030).

Cost compression in lithium-ion cells to USD 115 per kWh in 2024, the U.S. Inflation Reduction Act’s 30% tax credit, and rising rooftop-solar attachment rates are reshaping consumer economics and accelerating adoption. Aggressive policy incentives in Asia-Pacific, progressive net-metering reforms in North America, and tightening grid-reliability requirements in Europe collectively reinforce a flywheel of demand that positions the residential battery market as a critical pillar of distributed energy infrastructure. Automotive cell makers entering the sector are expanding supply, while digital sales platforms lower customer-acquisition costs and broaden access. At the same time, safety standards such as UL 9540A and IEC 63056 are raising the bar for product design, forcing manufacturers to integrate advanced battery-management software and safer chemistries to sustain momentum.

Key Report Takeaways

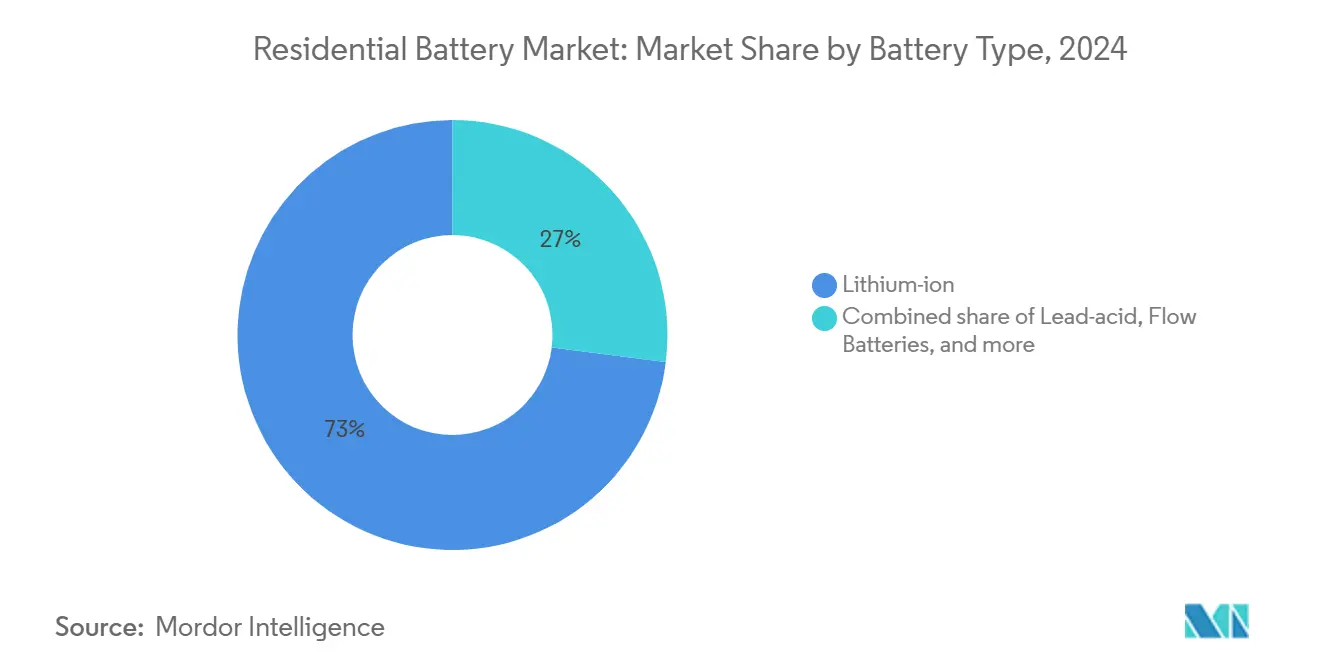

- By battery type, lithium-ion led with 73% revenue share in 2024; sodium-ion and nickel-based chemistries are projected to expand at a 19.5% CAGR through 2030.

- By application, self-consumption and backup held 68% of the residential battery market share in 2024, while virtual power plant and grid-service deployments are forecast to grow at an 18.0% CAGR to 2030.

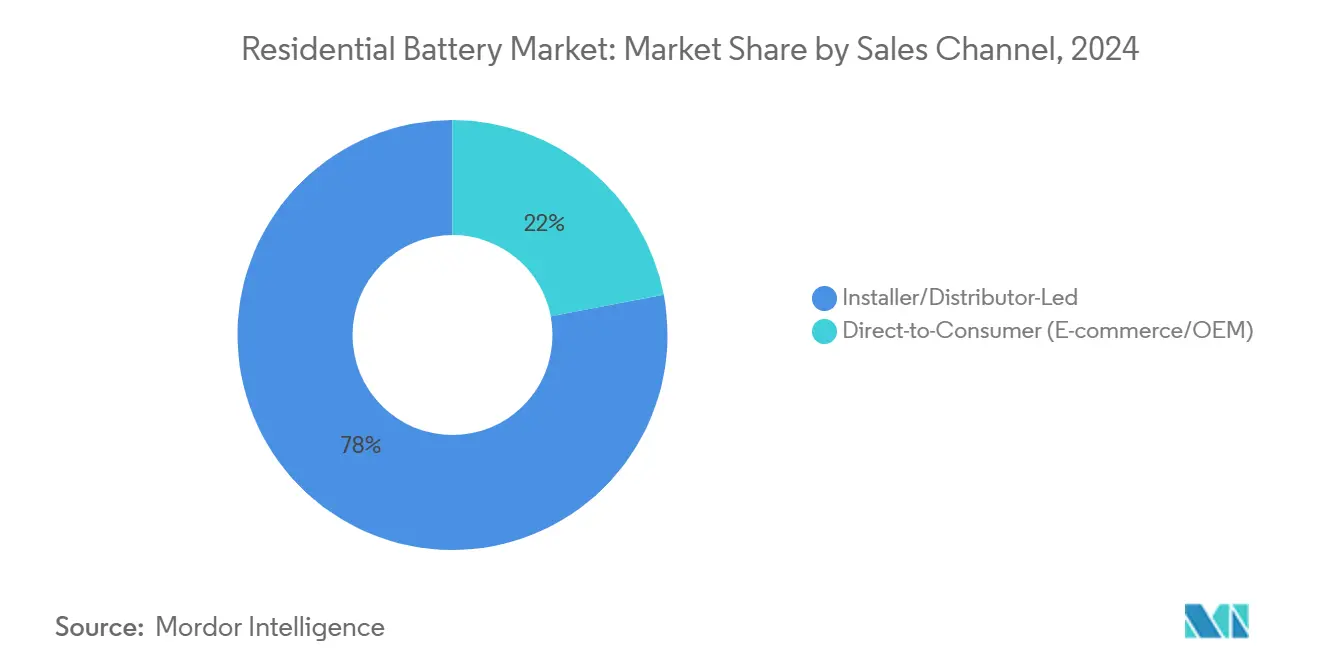

- By sales channel, installer and distributor-led routes accounted for 78% of the residential battery market size in 2024; direct-to-consumer channels are advancing at an 18.5% CAGR through 2030.

- By geography, Asia-Pacific captured 53% of the residential battery market share in 2024 and is set to expand at an 18.95% CAGR to 2030.

- Tesla, CATL, BYD, Enphase Energy, and Sonnen collectively controlled about 70% of 2024 deployments, with Tesla alone holding 45% of the residential battery market share.

Global Residential Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging rooftop-PV pairing mandates in Germany & Australia | +3.2% | Germany, Australia, with spillover to EU and APAC | Medium term (2-4 years) |

| U.S. Inflation Reduction Act 30% ITC extension to batteries | +4.5% | North America, with global supply chain impacts | Long term (≥ 4 years) |

| California NEM 3.0 sharpening self-consumption economics | +2.8% | California, with policy influence across North America | Medium term (2-4 years) |

| Japanese FIP scheme rewarding behind-the-meter VPP aggregation | +2.1% | Japan, with influence across APAC | Medium term (2-4 years) |

| South-Korean REC multipliers for residential ESS | +1.9% | South Korea | Medium term (2-4 years) |

| Dramatic Li-ion $/kWh cost drop below USD 250 for <15 kWh packs | +2.7% | Global, with strongest impact in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging rooftop-PV Pairing Mandates in Germany & Australia

Mandatory battery pairing with new rooftop solar in Germany and Australia is rewriting cost structures. Guaranteed volume allows manufacturers to increase production runs, driving per-unit cost savings that cascade through the residential battery market. In Australia, high retail tariffs and state rebates have compressed payback periods from 25 years in 2020 to 11 years in 2025, elevating storage from optional upgrade to standard component. German policy mirrors this trajectory by linking battery subsidies to solar performance guarantees, which standardizes sizing norms and simplifies installer workflows. These measures create predictable demand, enabling distributors to negotiate long-term supply agreements and allowing utilities to plan distribution-grid upgrades with clearer visibility on behind-the-meter capacity.

U.S. Inflation Reduction Act 30 % ITC Extension to Batteries

The U.S. Inflation Reduction Act’s 30% Investment Tax Credit now applies to standalone batteries, trimming homeowner payback by roughly one-third. Installations surged in 2024, with 11.9 GW of residential and small commercial capacity brought online more than any prior year(1)Business Council for Sustainable Energy, “Sustainable Energy in America Factbook 2025,” bcse.org. Manufacturers are re-tooling production lines for domestic assembly to capture additional Advanced Manufacturing credits, while financiers bundle transferable credits into structured deals that open the residential battery market to households with limited tax liability. Suppliers leverage the policy to pre-sell multiyear output, locking in lithium-ion cell procurement at favorable prices and hedging commodity risk.

California NEM 3.0 Sharpening Self-Consumption Economics

California’s third-generation net-metering rule slashes export compensation, so homeowners now design systems that maximize on-site use. Battery attachment rates on new rooftop arrays climbed sharply after April 2024, pushing the residential battery market size in the state past the 10 GWh cumulative mark. Community Choice Aggregators amplify the effect through rebates of USD 300 per kWh, which tilt economics further toward storage. Utilities benefit from peak-shaving capability, delaying distribution upgrades and reducing wholesale-market volatility.

Japanese FIP Scheme Rewarding Behind-the-Meter VPP Aggregation

Japan replaced feed-in tariffs with feed-in premiums that reward time-aligned exports and grid-service participation. Residential batteries aggregated into virtual power plants reached 3 GWh in 2023 and are on course for 14–24 GWh by 2030, making Japan a reference model for monetizing flexibility(2)Flow Batteries Europe, "Analysis of energy storage policies", flowbatterieseurope.eu. The policy compels manufacturers to embed advanced communications protocols and pushes aggregators to integrate AI-based dispatch that captures premium payments during high-demand intervals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Rising grid-connection & permitting queues across EU | -1.8% | European Union, with isolated impacts in North America |

| Fire-safety codes tightening for indoor installations (UL 9540A, IEC 63056) | -1.2% | Global, with strongest impact in North America and Europe |

| Limited second-life battery availability until 2027 | -0.9% | Global |

| Li-ion supply-chain exposure to critical-minerals price shocks | -1.3% | Global, with strongest impact in regions without domestic battery production |

| Source: Mordor Intelligence | ||

Rising Grid-connection & Permitting Queues across EU

Record solar adoption is overloading interconnection departments across Europe. Permitting backlogs stretch from weeks to months, delaying revenue recognition for installers and dampening the residential battery market. Spain’s subsidy-driven boom highlights the strain: distribution system operators now triage applications, often deferring small residential units while prioritizing utility-scale plants. The European Parliament flags raw-material cost inflation and supply security risks that compound the queue issue, prompting innovators to pioneer community batteries that satisfy multiple households under a single interconnection agreement.

Fire-safety Codes Tightening for Indoor Installations (UL 9540A, IEC 63056)

New tests such as UL 9540A demand cell-level thermal-runaway containment, raising design complexity and adding USD 150–250 per installation for certification and fire-suppression features. The EU Battery Regulation, effective August 2024, introduces serial-number tracking and hazardous-substance limits, forcing supply-chain audits. Smaller suppliers struggle to fund the required engineering, nudging the residential battery market toward higher consolidation around firms able to spread compliance costs over larger production volumes. Concurrently, chemistries with inherently lower flammability, such as aqueous sodium-ion and vanadium flow, gain strategic visibility.

Segment Analysis

By Battery Type: Sodium-ion Challenges Lithium Dominance

Lithium-ion held 73% of the residential battery market in 2024 because of mature supply chains and superior energy density. The residential battery market size for lithium-ion products crossed USD 13 billion in 2025, supported by cell prices below USD 139 per kWh. Yet supply-chain exposure to lithium carbonate price swings motivates policymakers to diversify chemistries. Sodium-ion manufacturers plan 40 GWh of annual capacity by 2030, leveraging abundant raw material availability.

The fastest-growing chemistries, sodium-ion and nickel-based variants, are expected to post a 19.5% CAGR, eroding lithium’s share in price-sensitive markets. Lead-acid retains pockets of demand where upfront cost trumps efficiency, mostly in emerging economies. Flow batteries, while niche, appeal to households that prioritize extended cycle life and tolerance to high ambient temperatures. Competitive positioning is shifting from one-size-fits-all energy density toward application-specific optimization, a transition that broadens the residential battery market and allows multiple chemistries to coexist.

Note: Segment shares of all individual segments available upon report purchase

By Application: VPP Integration Unlocks New Revenue Streams

Self-consumption and backup commanded about 68% of 2024 installations as families sought resilience during outages. The residential battery market size for this segment reached USD 14 billion in 2025. However, grid-service revenue stacking is accelerating. VPP programs pay homeowners for aggregated capacity, turning idle storage into an asset that earns monthly income. PG&E’s March 2025 launch enrolled thousands of systems, proving dispatch reliability and inspiring similar programs nationwide(3)Renewable Energy World, "PG&E launches ‘first of its kind’ virtual power plant program", renewableenergyworld.com.

Virtual power plant participation is projected to grow at an 18.0% CAGR, narrowing the cost gap for prospective buyers and encouraging utilities to shift peak-load forecasts. Off-grid and rural electrification remains smaller in volume but critical for regions with unreliable grids. The segmentation shows how policy and market design directly shape value creation pathways, expanding the residential battery market beyond pure self-reliance narratives.

By Sales Channel: Digital Platforms Disrupt Traditional Distribution

Installer-centric distribution accounted for 78% of shipments in 2024, thanks to complex permitting and rooftop-PV bundling. The residential battery market size that flows through installer networks hit USD 17 billion in 2025. Yet the rise of plug-and-play units and transparent online pricing is eroding this dominance. Direct-to-consumer platforms often backed by manufacturers are growing at an 18.5% CAGR, riding on e-commerce familiarity and remote commissioning technologies.

Search spikes after extreme weather events illustrate how consumers bypass intermediaries when urgency is high. Financing innovations such as oversized battery leasing at sub-USD 2,000 upfront change affordability optics and reduce payback anxiety. Installers now emphasize value-added services like system optimization and VPP enrollment to defend margins. The resulting multi-channel ecosystem makes the residential battery market more resilient to single-point disruptions and expands geographic reach.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominates the residential battery market with a 53% share in 2024 and maintains the fastest regional expansion at an 18.95% CAGR. Manufacturing economies of scale centered in China compress prices, while Japan’s feed-in premium and South Korea’s REC multipliers guarantee revenue for grid-service participation. The region recorded 3 GWh of behind-the-meter batteries in Japan alone by 2023, and South Korea’s policy roadmap targets 24.5 GW of cumulative storage by 2036. Governments fast-track safety approvals, enabling rapid product launches and reinforcing local supply chains for critical minerals.

North America ranks second. The residential battery market here is catalyzed by the Inflation Reduction Act’s generous credits and heightened climate-related outage risk. The United States added 11.9 GW of residential and small commercial storage in 2024, overtaking pumped hydro for the first time. California’s NEM 3.0 rules changed design economics overnight, and states such as Virginia and Texas now trial VPP incentives that pay homeowners for wholesale-market participation. Regional cell production subsidies attract global manufacturers seeking tariff-free access to the growing residential battery market.

Europe couples strong decarbonization targets with evolving regulations. Germany tops regional installs, while Spain’s subsidy program fuels rapid growth despite interconnection queues. The EU Battery Regulation enforces circular-economy requirements, including battery passports from 2027, shaping design for recyclability. The UK Energy Act 2023 releases GBP 2 billion to nurture a domestic supply chain, lifting the residential battery market size in the British Isles. Nonetheless, grid-connection delays and raw-material cost spikes temper near-term rollouts, prompting experimentation with community-scale storage that sidesteps individual interconnects.

Competitive Landscape

The residential battery market is moderately concentrated, yet competition is intensifying. Tesla led 2024 shipments with 45% market share, aided by an integrated hardware-software ecosystem and brand trust. CATL and BYD extend automotive scale into home storage, undercutting prices while offering high-cycle LFP packs. Enphase Energy leverages micro-inverter installed bases to upsell modular batteries and exploits Advanced Manufacturing credits to localize production in the United States. Sonnen differentiates through premium service bundles and early VPP participation.

Vertical integration is widening. Firms seek secure access to cells, power electronics, and energy-management algorithms to defend margins when pack prices fall. Sustainability credentials gain importance as the EU battery passport regime approaches. Companies invest in recycling partnerships to cap lifecycle emissions and secure reclaimed critical minerals.

Technology roadmaps show diversification: Tesla and Panasonic refine high-nickel chemistries for space-constrained markets, while CATL pilots sodium-ion for cost-sensitive regions. Flow-battery specialists court customers in hot climates where thermal runaway risk deters lithium. Strategic portfolio breadth becomes a hedge against commodity volatility and regulatory shifts, reinforcing the competitive hierarchy within the residential battery market.

Residential Battery Industry Leaders

-

Tesla Inc.

-

LG Energy Solution Ltd

-

Panasonic Holdings Corp.

-

BYD Co. Ltd

-

Sonnen GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sonnen partnered with Abundance Energy to roll out a Texas residential VPP with no upfront customer cost.

- December 2024: Invinity Energy Systems deployed its first ENDURIUM battery in Spain and reported a 24% cost reduction

- August 2024: Reliance Industries revealed plans to mass-produce LFP and sodium-ion cells by 2026.

- January 2024: AES Indiana secured approval for a 200 MW, 800 MWh standalone battery in Pike County.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the residential battery market as the yearly revenue generated from factory-built rechargeable batteries, mainly lithium-ion, lead-acid, flow, sodium-ion, and nickel-based chemistries, installed inside or alongside single-family and multi-family dwellings for self-consumption, backup, virtual-power-plant participation, or off-grid electrification.

Scope exclusion: Utility-scale, commercial, and portable device batteries lie outside this report's boundary.

Segmentation Overview

- By Battery Type

- Li-ion (LFP, NMC)

- Lead-acid (AGM, GEL)

- Flow Batteries (Vanadium, Zinc-Br)

- Sodium-ion and Nickel-based

- By Application

- Self-Consumption and Backup

- Virtual Power Plant/Grid Services

- Off-Grid/Rural Electrification

- By Sales Channel

- Direct-to-Consumer (E-commerce/OEM)

- Installer/Distributor-Led

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Egypt

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers, battery pack OEMs, inverter vendors, and energy-service aggregators across North America, Europe, Australia, China, and key emerging markets. Conversations focused on retail price dispersion, warranty claims, typical usable capacity per home, and expected participation in demand-response programs, letting us verify desk findings and refine cost-down assumptions.

Desk Research

We began with core energy statistics from sources such as the International Energy Agency, U.S. Energy Information Administration, Eurostat, and Japan's METI to pin down residential electricity demand and rooftop solar capacity. Trade data from UN Comtrade and Volza helped us trace battery imports, while patent analytics from Questel revealed emerging chemistries that could reshape supply outlook.

Company 10-K filings, inverter maker presentations, policy trackers from the IRENA database, and news feeds on Dow Jones Factiva grounded price trends and regulatory shifts that matter to home storage adoption. These references illustrate, not exhaust, the broader pool of studies and datasets our analysts checked for context and numeric baselines.

Market-Sizing & Forecasting

We applied a top-down construct that starts with installed residential rooftop solar capacity, average storage attachment rates, and typical kilowatt-hour per installation, which are then monetized using region-weighted average selling prices. Supplier roll-ups and channel checks offered bottom-up cross-tests, keeping totals realistic. Core variables include lithium-ion pack price (USD/kWh), household outage hours per year, feed-in-tariff evolution, retail electricity rates, and regional battery recycling mandates; each shows a measurable link to adoption and therefore enters our multivariate regression forecast to 2030. Gaps in bottom-up data, most common in emerging economies, were bridged by calibrated penetration proxies drawn from peer regions with similar grid reliability scores.

Data Validation & Update Cycle

Every draft model is rerun through automated variance screens, peer-reviewed by a senior analyst, and re-benchmarked against new shipment disclosures or policy changes. Reports refresh each year, with interim updates triggered when pack prices shift by more than ten percent or when major incentive programs are announced.

Why Mordor's Residential Battery Baseline Inspires Confidence

Published numbers often differ because firms select dissimilar chemistries, treat installer mark-ups differently, or refresh their models on uneven schedules. We flag these elements upfront so users see exactly what drives our totals.

Key gap drivers include competitors counting only lithium-ion units, using conservative attachment rates, or applying outdated 2022 price curves, whereas Mordor applies current 2024 ASPs and includes emerging sodium-ion pilots that already ship commercially.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.94 B | Mordor Intelligence | - |

| USD 14.35 B | Global Consultancy A | Excludes distributed virtual-power-plant contracts and uses 2023 ASPs |

| USD 10.92 B | Regional Consultancy B | Counts only lead-acid and lithium-ion, ignores flow and sodium-ion; lower attachment assumption |

In sum, our disciplined variable selection, transparent assumptions, and timely refresh cycle give decision-makers a balanced, reproducible baseline that bridges real shipment data with on-the-ground market signals.

Key Questions Answered in the Report

What is the expected CAGR for the residential battery market through 2030?

The residential battery market is projected to grow at a 17.52% CAGR between 2025 and 2030.

Which region currently leads the residential battery market?

Asia-Pacific leads with 53% of 2024 installations and maintains the fastest growth outlook.

How is California’s NEM 3.0 policy influencing battery adoption?

By cutting export credits, NEM 3.0 makes on-site consumption more valuable, driving higher battery attachment rates in new solar projects.

Why are sodium-ion batteries gaining attention within the residential battery industry?

Sodium-ion uses abundant raw materials, lowering supply-chain risk, and is forecast to expand at a 19.5% CAGR, challenging lithium dominance.

What share of 2024 residential battery deployments did Tesla hold?

Tesla accounted for roughly 45% of 2024 shipments, retaining leadership within a competitive field.

How are direct-to-consumer channels changing sales dynamics?

E-commerce and manufacturer websites are growing at an 18.5% CAGR, reducing dependence on installer networks and expanding market reach.

Page last updated on: