Republic Of Ireland Renewable Energy Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Volume (2026) | 9.12 gigawatt |

| Market Volume (2031) | 18.75 gigawatt |

| Growth Rate (2026 - 2031) | 15.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Republic Of Ireland Renewable Energy Market Analysis by Mordor Intelligence

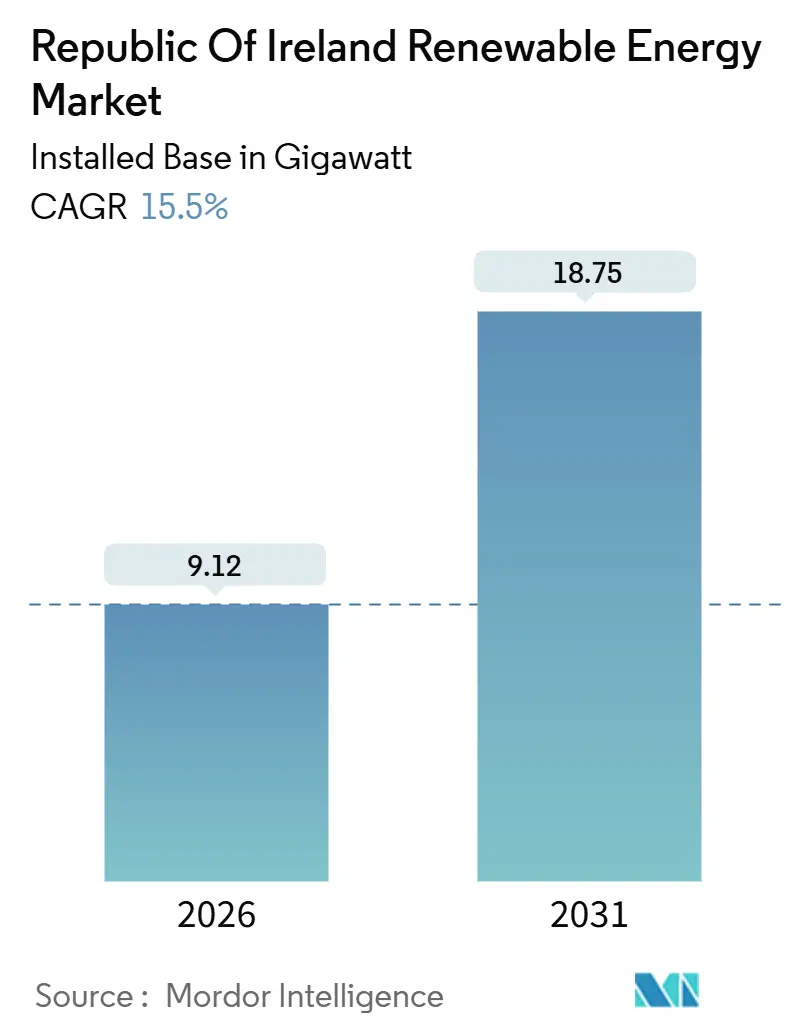

The Republic Of Ireland Renewable Energy Market size in terms of installed base is expected to grow from 9.12 gigawatt in 2026 to 18.75 gigawatt by 2031, at a CAGR of 15.5% during the forecast period (2026-2031).

This trajectory reflects an economy-wide shift away from fossil fuel reliance, with auction-backed offshore wind, utility-scale solar under corporate PPAs, and accelerating residential rooftop adoption driving new capacity additions. Falling onshore wind strike prices, a 72 MW hyperscale solar PPA benchmark below EUR 60 per MWh, and a 7 GW offshore pipeline slated for 2028-2031 further underscore the Republic of Ireland renewable energy market’s structural momentum. Grid investments prioritized for hydrogen-ready transmission corridors, port upgrades along the South Coast, and data-center co-located renewables are reshaping project economics, while curtailment in congested coastal nodes and planning bottlenecks remain headwinds.

Key Report Takeaways

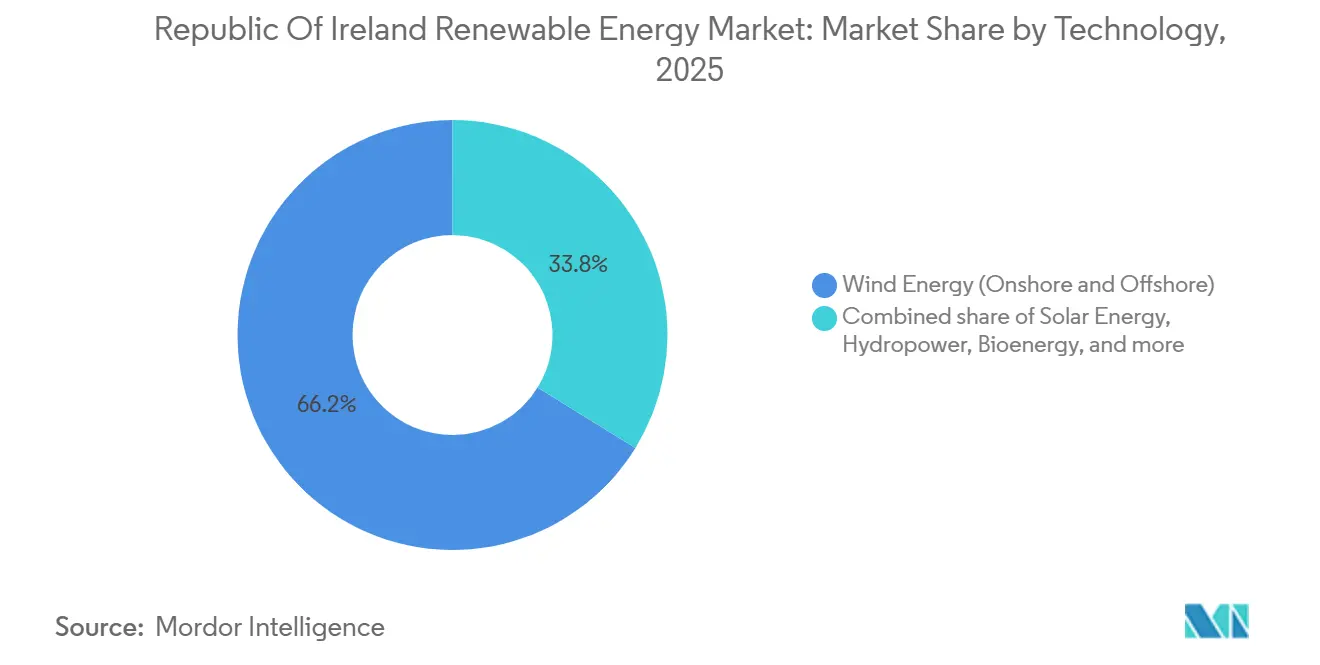

- By technology, wind energy held 66.2% of the Republic of Ireland's renewable energy market share in 2025, and bioenergy is projected to expand at a 90.4% CAGR through 2031.

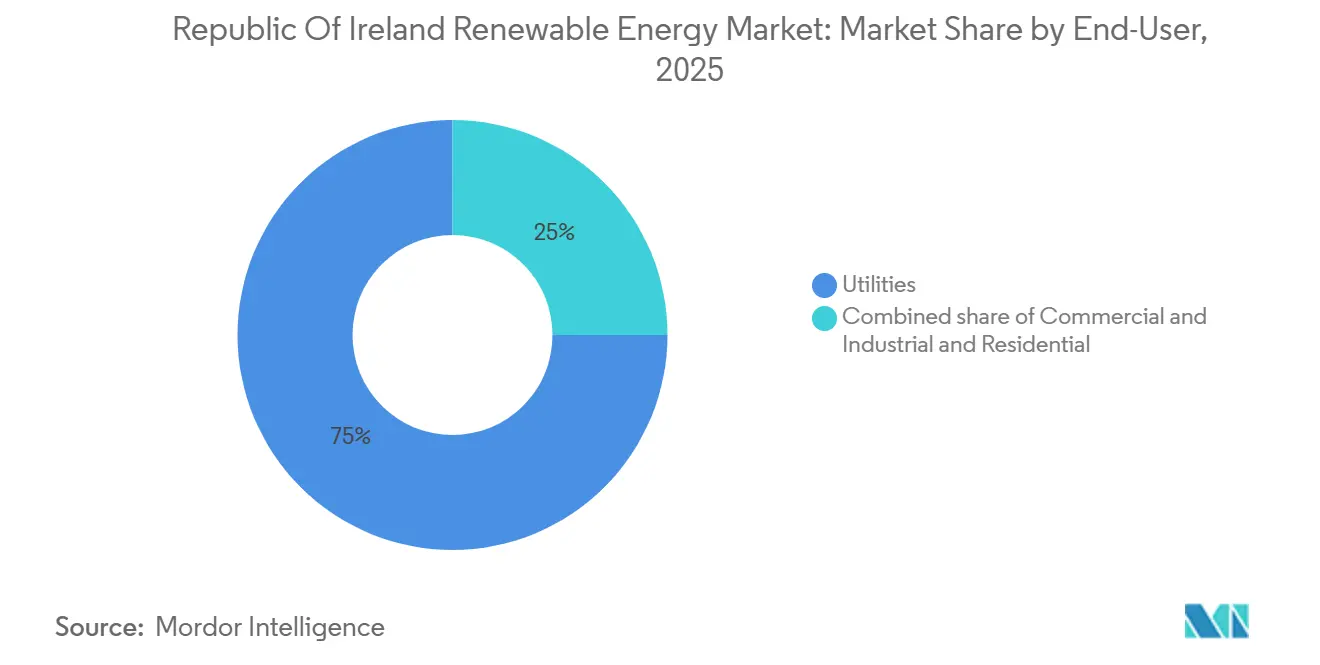

- By end-user, utilities controlled 75% of installed capacity in 2025, whereas residential solar is forecast to grow at a 25.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Republic Of Ireland Renewable Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Offshore-Wind Leasing in Celtic & Irish Seas | 4.2% | National, with concentration in South & East coasts | Long term (≥ 4 years) |

| Government-Backed RESS Auctions | 3.8% | National, early gains in Munster & Connacht | Medium term (2-4 years) |

| Corporate PPAs Driving Utility-Scale Solar Build-out | 2.6% | National, Leinster & Munster lead | Short term (≤ 2 years) |

| Hydrogen-Ready Transmission Grid Investments | 1.9% | National, priority corridors in East & South | Long term (≥ 4 years) |

| Repowering of Ageing Onshore Wind Fleet | 1.7% | National, legacy sites in West & Midlands | Medium term (2-4 years) |

| Data-Centre Energy Demand Growth in Leinster | 1.3% | Leinster, spillover to adjacent counties | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Offshore-Wind Leasing in Celtic & Irish Seas

Ireland’s offshore pipeline reached 7 GW in 2025, split between fixed-bottom projects in the Irish Sea and floating arrays in the Atlantic. The inaugural 900 MW Tonn Nua auction in 2024 cleared at EUR 150 per MWh, reflecting higher costs for first-of-kind floating platforms. Ørsted’s 800 MW Clogher Head scheme adds a 200 MW electrolyzer, converting surplus output into green hydrogen for industrial buyers.[1]Ørsted A/S, “Clogher Head Offshore Wind Project Overview,” ØRSTED.COM, orsted.com Cross-border links to the United Kingdom’s 4.5 GW Celtic Sea leases create export optionality, yet seabed-mapping delays have postponed 1.2 GW of Irish projects. Supply-chain tightness for dynamic cables could push several floating arrays beyond 2030.

Government-Backed RESS Auctions

RESS 3-5 allocated 2.9 GW in 2024-2025, with onshore wind securing 68% and solar 22%. Onshore wind strike prices fell 12% between RESS 3 and RESS 4 to EUR 72.58 per MWh, signaling efficiency gains and cheaper project finance. Battery-paired hybrids captured 180 MW in RESS 5, demonstrating policy support for firm-capacity solutions. Sub-5 MW Small-Scale RESS awards to rooftops reduce reliance on congested distribution networks. However, grid connection delays of up to 24 months remain a binding constraint on projects awarded in RESS 3.

Corporate PPAs Driving Utility-Scale Solar Build-out

Hyperscale companies executed 450 MW of solar PPAs in 2024-2025, with Microsoft’s 72 MW Lenalea contract setting a sub-EUR 60 per MWh benchmark.[2]Microsoft Corporation, “Microsoft Signs Irish Renewable PPA,” MICROSOFT.COM, microsoft.com Merchant developers now deploy bifacial modules and single-axis trackers that improve yields by over 12%. Lightsource BP, BayWa r.e., and others are lining up 320 MW for 2026-2027, although land-use objections continue to slow planning approvals. Corporate procurement is therefore reshaping the Republic of Ireland renewable energy market by creating a pricing gap between hyperscale buyers and smaller off-takers still reliant on RESS.

Hydrogen-Ready Transmission Grid Investments

EirGrid’s EUR 1.2 billion upgrade plan channels capital to reinforce the East-West interconnector and build hydrogen-capable substations. Priority corridors in Leinster and Munster will enable the 7 GW offshore pipeline to connect without triggering curtailment once assets go live after 2028. Interim, storage-linked hybrids and synchronous condensers mitigate frequency deviations. Transmission readiness is pivotal for unlocking green hydrogen hubs along the South Coast and feeding data-center loads.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Congestion in South-West & West Coastal Nodes | -2.4% | Munster & Connacht, coastal counties | Medium term (2-4 years) |

| Slow Planning Approval Processes for Large-Scale Projects | -1.8% | National, acute in rural counties | Short term (≤ 2 years) |

| Rising CAPEX due to Local Content & Inflationary Pressures | -1.5% | National, offshore wind and floating platforms most affected | Medium term (2-4 years) |

| Limited Pumped-Storage & Long-Duration Storage Options | -1.2% | National, critical for Leinster & Munster offshore wind integration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion in South-West & West Coastal Nodes

Curtailment exceeded 11% of available wind output in 2024 as 110 kV lines from Munster struggled to evacuate coastal production. The North-South Interconnector, delayed to 2028, leaves developers dependent on localized batteries such as ESB’s 100 MW Aghada site that absorbs excess generation but only for two-hour windows. Capital is shifting toward inland sites or to floating offshore projects positioned closer to load centers.

Slow Planning Approval Processes for Large-Scale Projects

An Bord Pleanála stretched average consent timelines for >50 MW projects to 22 months in 2025 amid heavier public consultations.[3]An Bord Pleanála, “Strategic Infrastructure Consent Statistics,” PLEANALA.IE, pleanala.ie Simply Blue Group’s Emerald floating wind timetable slipped a year after additional bird-migration studies. Developers now pre-file environmental data and community benefit plans, adding EUR 2-5 million in soft costs and compressing margins on marginal sites.

Segment Analysis

By Technology: Wind Dominance Meets Bioenergy Surge

Wind energy captured 66.2% of installed capacity in 2025, and repowering projects such as SSE's 105 MW Galway upgrade lifted onshore output without expanding footprints.[4]SSE Renewables, “Galway Wind Park Repowering,” SSERENEWABLES.COM, sserenewables.com The Republic of Ireland's renewable energy market size for onshore wind is projected to reach 9.3 GW by 2031 at a 9.4% CAGR, while a 4.2 GW fixed-bottom and 2.8 GW floating offshore pipeline positions the segment for 22.1% annual growth. Bioenergy capacity, anchored by 18 new anaerobic digestion facilities, is rising at a 90.4% CAGR, reflecting dispatchable generation demand that complements intermittent wind and solar. Small hydropower remains capped at 240 MW, though ESB's 300 MW Turlough Hill expansion would double long-duration storage when commissioned in 2030.

Solar's corporate-driven build-out totals 720 MW installed or under construction, and the Republic of Ireland renewable energy market size for solar is forecast to double between 2026 and 2031. Ocean energy retains pilot status; DP Energy's 5 MW wave project relies on EU Innovation Fund support to bring levelized costs below EUR 150 per MWh by decade's end. Technology diversification is therefore broadening the Republic of Ireland's renewable energy market beyond its historic wind focus.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Utilities Lead, Residential Accelerates

Utilities owned 75% of capacity in 2025, yet households are closing the gap as Microgeneration Support Scheme feed-in tariffs shorten rooftop solar paybacks to under nine years. Residential installations doubled to 8,200 in 2024, and the segment is set to log a 25.4% CAGR to 2031, driven by high retail tariffs averaging EUR 0.32 per kWh. Commercial and industrial players are hedging power costs through behind-the-meter assets, exemplified by Kerry Group's 12 MW solar system meeting 18% of factory demand.

Utilities are pivoting to hybrid assets that satisfy EirGrid's firm-capacity rules. Energia's 50 MW Castlepook wind-plus-battery plant demonstrates how pairing 20 MW of storage secures priority dispatch. By 2031, hybrid configurations could carry 12% of the Republic of Ireland's renewable energy market share, further diluting the traditional dominance of stand-alone wind farms.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Leinster, Munster, and Connacht account for 92% of projected capacity additions through 2031. Leinster remains the largest consumer due to data-center concentration, yet a 2024 connection moratorium is redirecting new projects to Munster. The Republic of Ireland renewable energy market size for Munster is forecast to exceed 6 GW by 2031 on the back of a 3.2 GW offshore pipeline and bioenergy build-out tied to dairy agriculture.

Connacht hosts 1.2 GW of operating onshore wind but suffers 14% curtailment pending the 400 kV North-South Interconnector in 2028. Ulster’s cross-border links allow power exports to Northern Ireland, though dual planning regimes add up to nine months to project approvals. Upgraded ports at Cork, Waterford, and Shannon Foynes command EUR 450 million in investment, placing the South Coast at the center of floating offshore assembly.

Data-center developers are installing 420 MW of co-located renewables across Dublin, Meath, and Kildare, yet grid upgrades worth EUR 800 million will not be operational until 2028. Inland counties with strong wind resources remain underdeveloped, confirming that transmission readiness, not resource quality, will shape the next wave of the Republic of Ireland renewable energy market.

Competitive Landscape

The five largest players, SSE Renewables, ESB, Energia, Ørsted, and Mainstream Renewable Power, account for 58% of installed capacity, reflecting moderate concentration. Incumbents exploit balance-sheet strength to dominate RESS allocations, while new entrants target niches such as floating offshore wind or wave energy. Greencoat Renewables and Brookfield grow through asset acquisitions, with Greencoat’s EUR 180 million purchase of 120 MW in 2024 widening its portfolio to 580 MW.

Technology advances are redrawing cost curves: Vestas V162-6.2 MW turbines in SSE’s Galway repowering deliver 22% higher capacity factors than legacy units, and bifacial solar modules at Lightsource BP’s 85 MW Milltown site lift yields by 14%. Compliance with EirGrid’s DS3 grid-support rules favors projects integrating synchronous condensers or grid-forming inverters, elevating technically sophisticated developers.

Hybrid projects that monetize curtailed output via batteries or hydrogen electrolysis illustrate strategic diversification: Energia’s Castlepook and Ørsted’s Clogher Head electrolyzer exemplify how developers convert surplus energy into new revenue streams. As floating offshore, agrivoltaics, and hydrogen hubs mature, competitive intensity in the Republic of Ireland renewable energy market is set to rise.

Republic Of Ireland Renewable Energy Industry Leaders

ESB Generation & Trading

SSE Renewables

Statkraft Ireland Ltd

Energia Group

Greencoat Renewables plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DP Energy and ESB unveiled plans for a 100 MW wind farm, enhancing collaborative project delivery.

- May 2025: HitecVision and Reinova Partners created an Irish platform via the acquisition of a 166 MW wind portfolio from Greencoat Renewables.

- May 2025: Ireland opened its fifth renewables auction (RESS 5) with indexation upgrades.

- April 2025: The government announced EUR 1 billion for offshore grid links to the Celtic Sea.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Republic of Ireland renewable energy market as the total installed generating capacity (megawatts and gigawatts) coming from wind, solar-PV, hydro, bioenergy, geothermal, and emerging ocean technologies that feed the public grid or accredited behind-the-meter schemes. Self-consumption micro-generation is included once it is registered in national statistics.

Energy-from-waste incineration and pure renewable-energy certificate trading are excluded.

Segmentation Overview

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed developers, network operators, EPC contractors, and equipment suppliers across Leinster, Munster, and Connacht. Dialogues tested grid-constraint anecdotes, auction bid behavior, and post-construction capacity factors, enabling us to adjust secondary numbers before model lock-in.

Desk Research

We collated baseline capacity and policy data from open-access authorities such as the Sustainable Energy Authority of Ireland, Central Statistics Office, Eurostat, the International Energy Agency, and EirGrid's generation connection register. Broader economic signals were drawn from Budget Statements and Euro-denominated exchange files. Company-specific build plans and typical capex ranges were screened through D&B Hoovers and news archives in Dow Jones Factiva, which helped us benchmark realistic commissioning timelines and cost curves.

Installed-capacity additions reported in planning portals, tender notices (Tenders Info), and patent clusters (Questel) supplied early indicators of pipeline momentum, while peer-reviewed journals clarified load-factor assumptions for offshore wind and utility-scale solar. This list is illustrative; many other niche publications and databases supported validation.

Market-Sizing & Forecasting

A top-down build, starting with historical SEAI capacity by technology, is projected through 2030 using auction awards, connection offers, and typical realization rates. Results are cross-checked through selective bottom-up roll-ups of announced projects and sampled average selling prices multiplied by expected annual additions. Key drivers baked into our equations include RESS auction capacity ceilings, offshore license rounds, corporate PPA uptake, median construction lead times, and forecast grid-reinforcement milestones. Multivariate regression with scenario analysis captures sensitivities to permitting slippage and capex inflation; missing micro-generation data are infilled via panel-sales penetration rates validated during interviews.

Data Validation & Update Cycle

Outputs pass analyst peer review, variance screens against SEAI monthly dashboards, and capacity-factor sanity checks. We refresh the model annually or within four weeks of any material policy or auction event.

Why Mordor's Republic Of Ireland Renewable Energy Baseline Commands Reliability

Published estimates often diverge because firms pick different metrics, scopes, and refresh cadences.

Key gap drivers here are (i) Mordor's capacity-based scope versus others' revenue focus, (ii) our inclusion of registered micro-generation, and (iii) annual model refresh aligning with RESS auction cycles, whereas some providers freeze assumptions for multiple years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 7.53 GW installed base (2024) | Mordor Intelligence | - |

| USD 3.9 B value (2023) | Regional Consultancy A | counts project capex only; omits micro-generation and hydro refurbishments |

| USD 0.76 B value (2022) | Trade Journal B | narrower technology list; older base year; uses average wholesale power price revenue method |

These comparisons show that, by anchoring estimates to transparent grid-connected capacity and continuously updated policy variables, Mordor delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

How large is the Republic of Ireland renewable energy market in 2026?

Installed capacity reaches 9.12 GW in 2026, and it is forecast to double to 18.75 GW by 2031.

Which technology leads new capacity additions over 2026-2031?

Offshore wind anchors growth with a 7 GW pipeline, supported by fixed-bottom and floating projects scheduled for 2028-2031.

What support scheme underpins most new projects?

The Renewable Electricity Support Scheme (RESS) awarded 2.9 GW in auctions 3-5 during 2024-2025, providing 15-year fixed-price contracts to winners.

Why are corporate PPAs important in Ireland?

Hyperscale buyers signed 450 MW of solar PPAs in 2024-2025, setting price benchmarks below RESS levels and accelerating merchant solar economics.

What is the key grid challenge facing developers?

Congestion in South-West and West coastal nodes causes curtailment exceeding 11% of wind output, pending major transmission upgrades due by 2028.

How fast is residential solar growing?

Shipments doubled in 2024, and residential rooftop capacity is projected to grow at a 25.4% CAGR through 2031 under the Microgeneration Support Scheme.