| Study Period | 2019 - 2030 |

| Market Volume (2025) | 57.36 Million tons |

| Market Volume (2030) | 69.75 Million tons |

| CAGR | 3.99 % |

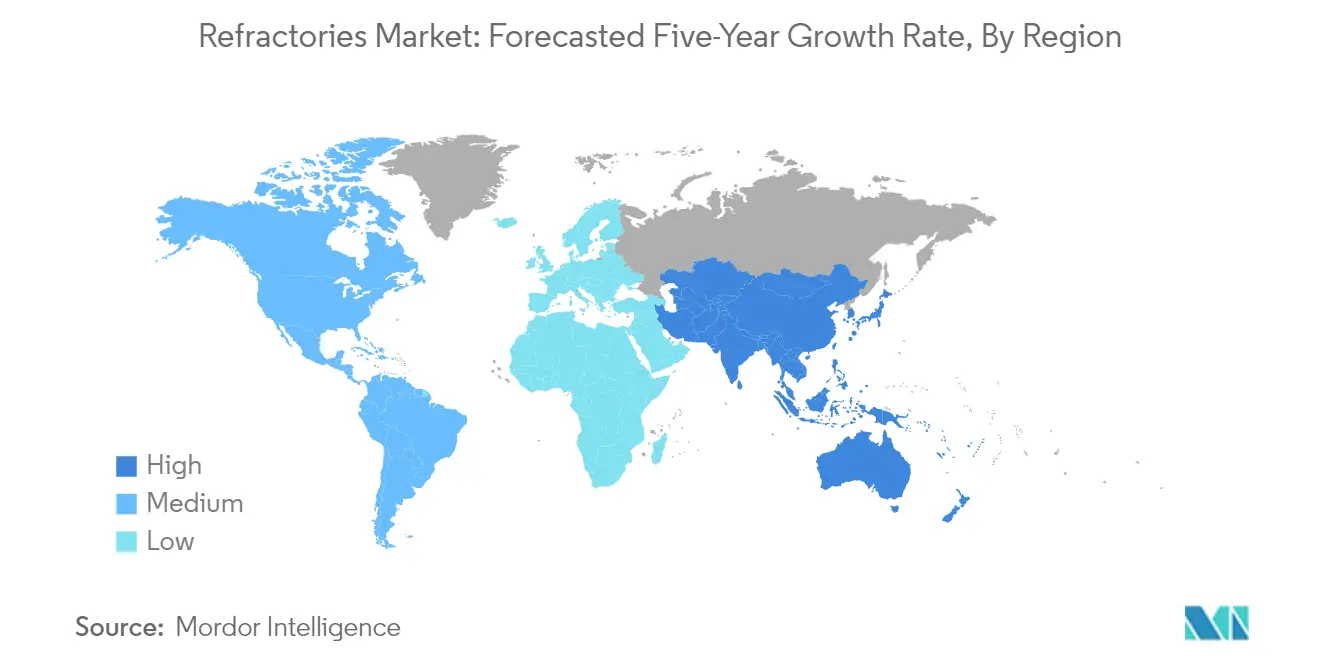

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

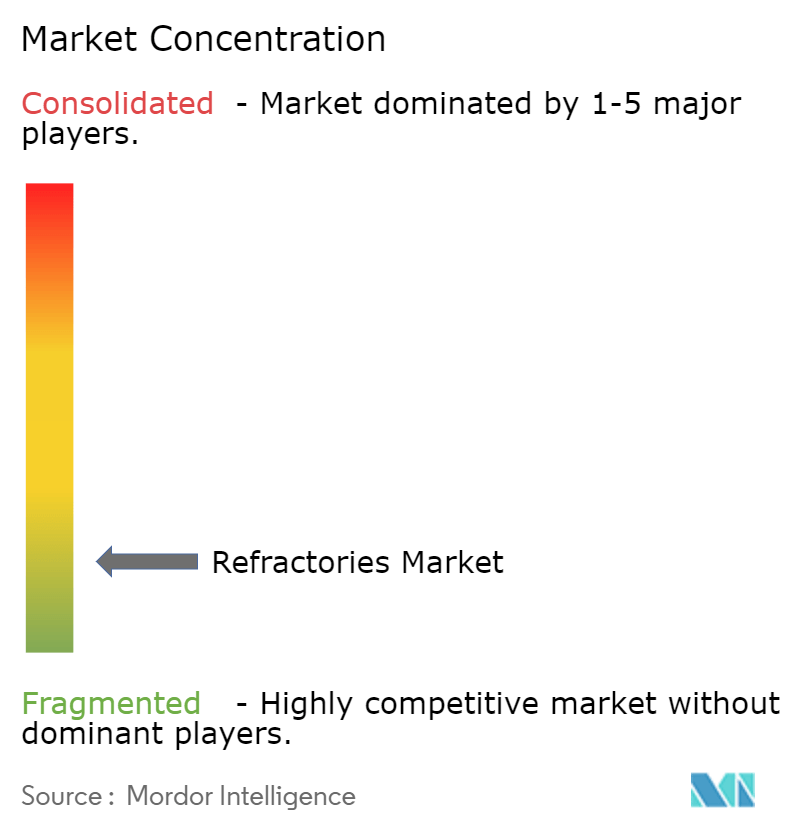

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Refractories Market Analysis

The Refractories Market size is estimated at 57.36 million tons in 2025, and is expected to reach 69.75 million tons by 2030, at a CAGR of 3.99% during the forecast period (2025-2030).

The global refractories industry is experiencing significant transformation driven by evolving environmental regulations and technological advancements in manufacturing processes. Government agencies worldwide are implementing stricter guidelines regarding the usage and disposal of refractory materials, compelling manufacturers to invest in sustainable production methods and eco-friendly alternatives. This regulatory pressure has led to increased research and development activities focused on developing environmentally compliant refractory solutions. The chemical sector, a major end-user of refractory materials, demonstrated resilience with global chemical production increasing by 2.0% in 2023, indicating sustained demand for refractory materials in chemical processing applications.

The construction and infrastructure sectors continue to be significant drivers of refractory demand, particularly in emerging economies. The cement industry, a crucial end-user segment, has shown remarkable growth, with US cement production reaching 95 million tons in 2022, marking the highest production volume since 2010. This growth is complemented by extensive infrastructure development projects across Asia-Pacific, Middle East, and African regions, where governments are investing heavily in construction activities. The increasing focus on urbanization and industrial development in these regions has created substantial opportunities for refractory manufacturers.

The glass industry has emerged as a particularly dynamic sector for refractory applications, with European glass packaging production recording a 3% increase in the first half of 2022 compared to the same period in 2021. This growth is driven by increasing demand for sustainable packaging solutions and technological advancements in glass manufacturing processes. Major glass manufacturers are investing in capacity expansion and modernization projects, implementing advanced refractory solutions to improve operational efficiency and reduce energy consumption. The industry is witnessing a shift towards specialized refractory materials that can withstand higher temperatures while maintaining longer service life.

The refractories market is experiencing a notable shift towards advanced monolithic refractories and specialized shaped refractories designed for specific applications. Manufacturers are focusing on developing high-performance refractory products that offer superior thermal efficiency, longer service life, and reduced maintenance requirements. This trend is particularly evident in the power generation and petrochemical sectors, where operational efficiency and reliability are crucial. The industry is also witnessing increased adoption of automation and digital technologies in refractory manufacturing processes, leading to improved product quality and consistency. These technological advancements are reshaping the competitive landscape, with companies investing in research and development to maintain their market position.

Refractories Market Trends

Continuous Usage of refractories in the Iron and Steel Industry

The iron and steel industry continues to be the primary driver for the global refractories market, accounting for approximately 70% of total refractory materials consumption. Refractories play a crucial role in this industry due to their exceptional ability to withstand temperatures ranging from 260°C (500°F) to 1850°C (3400°F) without significant changes in their physical properties, making them indispensable for steel manufacturing processes. These materials find extensive applications in internal furnace linings for iron and steel production, heating furnaces for steel processing, vessels for metal and slag transportation, flues or stacks for hot gas conduction, and various other critical applications within the steel manufacturing process.

The robust growth in global steel production continues to drive demand for refractories. According to the World Steel Association, the production of crude steel across 63 countries reached 142.4 million metric tons (Mt) in February 2023, indicating strong ongoing demand for refractory materials. Major steel-producing nations continue to expand their production capabilities, with China leading at 80.1 Mt, followed by India (10 Mt), Japan (6.9 Mt), the United States (6 Mt), and Russia (5.6 Mt) in February 2023. New investments in the sector, such as Essar's announced plan in September 2022 to invest USD 4 billion in building a four-mtpa steel complex in Saudi Arabia by 2025, further demonstrate the industry's growth trajectory and sustained demand for refractory materials.

Understand The Key Trends Shaping This Market

Download PDF

Increase in the Production of Non-ferrous Metals

The growing production of non-ferrous metals globally has emerged as a significant driver for the refractory industry, with these materials being essential for various applications such as primary aluminum production, copper and alloy smelting, reduction cells, melting/holding furnaces, and casting operations. According to the United States Geological Survey (USGS), the global smelter production of aluminum reached 69,000 metric tons in 2022, representing an increase from 67,500 metric tons in 2021. The year-end capacity of aluminum smelters worldwide reached 77,000 metric tons in 2022, indicating continued expansion in production capabilities and subsequent demand for refractory materials.

The copper and nickel sectors have also demonstrated significant growth, further driving refractory demand. The global mine production of copper reached 22,000 metric tons in 2022, compared to 21,200 metric tons in 2021, while the total refinery production of copper increased to 26,000 metric tons in 2022. Similarly, nickel production showed substantial growth, with global mine production reaching 3,300,000 metric tons in 2022, a significant increase from 2,730,000 metric tons in 2021. Indonesia, as the world's largest producer, achieved production of 1,600,000 metric tons of nickel in 2022, demonstrating the robust growth in the non-ferrous metals sector and its increasing demand for refractory materials.

Segment Analysis: Product Type

Clay Refractory Segment in Global Refractories Market

The clay refractory segment dominates the global refractories market, holding approximately 55% market share in 2024. This segment's prominence is driven by its extensive applications across various industries, particularly in high-temperature industrial processes. Clay refractories, which include high alumina, fireclay, and insulating materials, are preferred due to their cost-effectiveness and versatility. The segment's dominance is particularly evident in the iron and steel industry, where these refractory materials are crucial for lining furnaces and other high-temperature equipment. The widespread adoption of clay refractories is also supported by their excellent thermal shock resistance, chemical stability, and mechanical strength at elevated temperatures, making them indispensable in cement kilns, glass furnaces, and other industrial applications.

Non-Clay Refractory Segment in Global Refractories Market

The non-clay refractory segment is experiencing robust growth in the global refractories market, projected to expand significantly from 2024 to 2029. This segment, which includes magnesite brick, zirconia brick, silica brick, chromite brick, and other specialized refractory products, is witnessing increased adoption due to its superior performance characteristics. The growth is primarily driven by the rising demand for high-performance refractories in critical applications where traditional clay-based materials may not meet the stringent requirements. Non-clay refractories are gaining traction in advanced industrial applications due to their exceptional properties such as higher thermal stability, better corrosion resistance, and improved slag resistance. The segment's growth is further supported by technological advancements in manufacturing processes and increasing investments in research and development to enhance product performance.

Segment Analysis: End-User Industry

Iron & Steel Segment in Refractories Market

The iron and steel segment continues to dominate the global refractories market, commanding approximately 63% of the total market share in 2024. This substantial market position is primarily driven by the extensive use of refractory materials in various steelmaking processes, including blast furnaces, basic oxygen furnaces, electric arc furnaces, and continuous casting operations. The segment is also experiencing the highest growth trajectory, projected to expand at approximately 4% through 2024-2029, driven by increasing steel production, particularly in emerging economies. The segment's growth is further supported by the rising demand for high-quality steel products in construction, automotive, and infrastructure development sectors. Major steel-producing countries like China, India, and Japan continue to invest in modernizing their steel manufacturing facilities, incorporating advanced refractory products to improve operational efficiency and reduce environmental impact. The segment's dominance is reinforced by ongoing technological advancements in refractory materials that enhance durability and performance in high-temperature steel manufacturing processes.

Cement Segment in Refractories Market

The cement segment represents a significant growth opportunity in the refractory industry, with a projected growth rate of approximately 4% during 2024-2029. This robust growth is primarily attributed to the expanding construction sector and infrastructure development activities across developing regions. The segment's growth is driven by increasing urbanization rates, government infrastructure initiatives, and the modernization of cement manufacturing facilities. Refractory manufacturers are focusing on developing specialized products that can withstand the harsh operating conditions in cement kilns while providing improved energy efficiency. The adoption of advanced refractory solutions in cement production is also being driven by stricter environmental regulations and the need for more sustainable manufacturing processes. Additionally, the growing trend toward larger capacity kilns and the increasing use of alternative fuels in cement production is creating demand for more sophisticated refractory solutions with enhanced thermal shock resistance and chemical stability properties.

Remaining Segments in End-User Industry

The remaining segments in the refractories market, including energy and chemicals, non-ferrous metals, ceramics, and glass, collectively play a vital role in shaping market dynamics. The energy and chemicals segment is driven by the expansion of petrochemical facilities and power generation plants, while the non-ferrous metals segment benefits from growing aluminum and copper production. The ceramics segment is influenced by the increasing demand for technical ceramics in various industrial applications, and the glass segment is supported by the growing demand from the construction and automotive sectors. These segments are characterized by their unique requirements for specialized refractory materials, driving innovation in product development. The diversity of these end-user industries provides market stability and opportunities for refractory manufacturers to develop specialized solutions catering to specific industrial needs.

Refractories Market Geography Segment Analysis

Refractories Market in Asia-Pacific

The Asia-Pacific region maintains its position as the dominant force in the global refractories market, driven by robust industrial growth across multiple sectors. The region's market dynamics are primarily shaped by China's massive manufacturing base, India's rapid industrialization, Japan's technological advancement in refractory applications, and South Korea's strong presence in the steel and electronics sectors. The presence of major steel producers, growing infrastructure development, and increasing investments in industrial capacity expansion continue to fuel the demand for refractory materials across the region. The market is characterized by a strong manufacturing base, technological innovations, and an increasing focus on high-performance refractory materials.

Refractories Market in China

China dominates the Asia-Pacific refractories market, accounting for approximately 72% of the regional market share in 2024. The country's market is driven by its massive steel industry, which remains the world's largest despite recent production adjustments. China's refractory sector benefits from extensive raw material reserves, established manufacturing infrastructure, and integrated supply chains. The government's focus on industrial upgrading and environmental protection has led to increased demand for higher-quality refractory products. The cement, glass, and non-ferrous metals industries also contribute significantly to refractory consumption, while recent initiatives in infrastructure development and industrial modernization continue to drive market growth.

Refractories Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 6% during 2024-2029. The country's refractory market is experiencing rapid expansion driven by ambitious infrastructure development plans, growing steel production capacity, and increasing investments in manufacturing sectors. The government's initiatives like "Make in India" and focus on domestic manufacturing capabilities have created substantial opportunities for refractory manufacturers in India. The modernization of existing industrial facilities, expansion of cement production capacity, and growing focus on energy efficiency in industrial processes are further driving the demand for advanced refractory materials in the country. Leading the way, the top 10 refractory companies in India are playing a pivotal role in this growth trajectory.

Refractories Market in North America

The North American refractories market demonstrates a mature and technologically advanced landscape, characterized by high-quality standards and innovative applications. The region's market is primarily driven by the United States, Canada, and Mexico, each contributing uniquely to the overall market dynamics. The focus on energy efficiency, environmental regulations, and technological advancement in manufacturing processes continues to shape the demand for specialized refractory products. The region's strong presence in the automotive, aerospace, and energy sectors maintains steady demand for high-performance refractory materials.

Refractories Market in United States

The United States maintains its position as the largest market in North America, holding approximately 72% of the regional market share in 2024. The country's refractory market benefits from its diverse industrial base, including steel production, cement manufacturing, and glass industries. The ongoing modernization of manufacturing facilities, increasing focus on energy efficiency, and growing demand from the chemical and petrochemical sectors drive market growth. The country's emphasis on research and development in refractory technologies and materials science continues to foster innovation in high-performance refractory products. Notably, refractory companies in USA are at the forefront of these advancements, contributing significantly to the market's evolution.

Refractories Market in Mexico

Mexico emerges as the fastest-growing market in North America, with an expected growth rate of approximately 3% during 2024-2029. The country's refractory market is experiencing significant expansion driven by increasing industrial investments, a growing automotive sector, and rising steel production capacity. The strategic location, competitive manufacturing costs, and free trade agreements with major economies continue to attract industrial investments. The modernization of existing manufacturing facilities and increasing focus on energy-efficient production processes are creating new opportunities for refractory manufacturers in the country.

Refractories Market in Europe

The European refractories market represents a sophisticated landscape characterized by high technological standards and stringent quality requirements. The region encompasses major industrial economies including Germany, the United Kingdom, Italy, and France, each contributing significantly to the market dynamics. The focus on sustainable manufacturing practices, energy efficiency, and environmental regulations continues to drive innovation in refractory products. The region's strong presence in the automotive, aerospace, and industrial manufacturing sectors maintains consistent demand for advanced refractory materials.

Refractories Market in Germany

Germany maintains its position as the largest refractory market in Europe, driven by its robust industrial base and technological leadership. The country's market benefits from its strong presence in automotive manufacturing, the chemical industry, and steel production. The ongoing focus on Industry 4.0 initiatives, sustainable manufacturing practices, and technological innovation continues to drive the demand for high-performance refractory materials. The country's emphasis on research and development in material sciences and industrial processes fosters continuous innovation in refractory technologies.

Refractories Market in United Kingdom

The United Kingdom emerges as the fastest-growing market in Europe, driven by increasing investments in industrial modernization and infrastructure development. The country's refractory market is experiencing significant transformation with a focus on energy-efficient manufacturing processes and sustainable production practices. The modernization of existing industrial facilities, growing emphasis on clean energy technologies, and increasing investments in advanced manufacturing sectors are creating new opportunities for refractory manufacturers. The country's strong research capabilities and focus on material innovation continue to drive advancements in refractory technologies.

Refractories Market in South America

The South American refractories market demonstrates significant potential for growth, driven by industrial development and infrastructure expansion across the region. Brazil emerges as both the largest and fastest-growing market in the region, followed by Argentina. The market benefits from the region's rich mineral resources, growing steel production capacity, and increasing investments in manufacturing sectors. The modernization of industrial facilities, focus on energy efficiency, and growing demand from construction and infrastructure sectors continue to drive market growth. The region's emphasis on sustainable manufacturing practices and technological advancement creates opportunities for innovative refractory solutions.

Refractories Market in Middle East & Africa

The Middle East & Africa refractories market shows promising growth potential, driven by increasing industrialization and infrastructure development across the region. South Africa emerges as the largest market while Saudi Arabia shows the fastest growth potential in the region. The market benefits from significant investments in oil & gas infrastructure, growing cement production capacity, and expanding manufacturing sectors. The region's focus on economic diversification, industrial development, and infrastructure expansion creates sustained demand for refractory materials. The modernization of existing industrial facilities and increasing emphasis on energy-efficient manufacturing processes continue to drive market growth across the region.

Get Analysis on Important Geographic Markets

Download PDF

Refractories Industry Overview

Top Companies in Refractories Market

The global refractories market features prominent players like RHI Magnesita, Krosaki Harima Corporation, and Shinagawa Refractories leading the industry through continuous innovation and strategic expansion. These refractory companies are increasingly focusing on developing specialized refractory solutions for high-temperature applications while investing in research and development to improve product performance and durability. The industry witnesses regular product launches targeting specific end-user requirements, particularly in the steel, cement, and glass manufacturing sectors. Operational excellence is being achieved through vertical integration strategies, with major players securing their raw material supply chains through ownership of mining operations. Strategic moves in the market are characterized by geographic expansion through acquisitions and joint ventures, particularly in emerging markets, while companies are also investing in sustainable manufacturing practices and digital technologies to optimize production processes.

Fragmented Market with Active M&A Landscape

The global refractories market exhibits a fragmented structure where the top five companies collectively serve less than a third of the global market demand, indicating significant opportunities for market consolidation. The competitive landscape is characterized by a mix of large multinational corporations with vertically integrated operations and regional specialists focusing on specific product segments or geographical markets. Major players are increasingly pursuing vertical integration to gain competitive advantages in cost management and supply chain control, while regional players leverage their local market knowledge and customer relationships.

The market has witnessed significant merger and acquisition activities, with companies actively pursuing inorganic growth strategies to expand their geographical presence and strengthen their product portfolios. Notable transactions include acquisitions in emerging markets like India and China, as well as strategic partnerships to enhance technological capabilities. Companies are also focusing on acquiring specialized refractory manufacturers to broaden their product offerings and gain access to new customer segments, while simultaneously investing in modernizing existing facilities to improve operational efficiency.

Innovation and Integration Drive Future Success

Success in the refractories market increasingly depends on companies' ability to innovate while maintaining cost competitiveness through efficient operations and strategic sourcing. Incumbent players are strengthening their market positions by investing in research and development, focusing on high-performance products, and expanding their service offerings to include technical support and customized solutions. The ability to provide comprehensive solutions rather than standalone products is becoming crucial, as end-users seek partners who can offer both products and technical expertise to optimize their operations.

For contenders looking to gain market share, the focus needs to be on developing specialized products for specific applications while building strong distribution networks and technical service capabilities. The industry's high dependence on the steel sector necessitates diversification into other end-user industries to reduce risk exposure. While substitution risk remains relatively low due to the essential nature of refractories in high-temperature applications, companies must stay ahead of environmental regulations affecting manufacturing processes and product compositions. Building long-term relationships with key customers through value-added services and technical support is becoming increasingly important for sustainable growth.

Refractories Market Leaders

-

RHI Magnesita N.V.

-

Chosun Refractories

-

Krosaki Harima Corporation

-

Puyang Refractories Group Co., Ltd.

-

Shinagawa Refractories Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Refractories Market News

- October 2024: Shinagawa Refractories Co., Ltd. has acquired the entire issued share capital of Gouda Refractories B.V. from Andus Group B.V. Gouda Refractories, based in the Netherlands, is a prominent manufacturer of alumina refractories and offers a range of refractory services.

- March 2024: RHI Magnesita N.V. declared its plan to purchase Resco Group, valuing the deal at an enterprise value of up to USD 430 million. Resco Group, headquartered in the United States, specializes in producing alumina monolithics and offers diverse refractories. These include both basic and non-basic types, shaped and unshaped, catering to industries such as petrochemicals, cement, aluminum, and steel-making.

- October 2023: RHI Magnesita N.V. acquired the refractory businesses of the Preiss-Daimler Group (“P-D Refractories”), located in Germany, the Czech Republic, and Slovenia. P-D Refractories produces alumina-based refractories tailored for industrial applications across various process industries. Their diverse product lineup includes high-alumina specialties and bricks made from bauxite, andalusite, silica, fireclay, and magnesite.

Refractories Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Substantial Usage of Refractories in the Iron and Steel Industry

- 4.1.2 Growing Demand for Refractories from Cement and Energy Sectors

-

4.2 Restraints

- 4.2.1 Environmental and Health Risks Associated with Refractories

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 Product Type

- 5.1.1 Non-clay Refractory

- 5.1.1.1 Magnesite Brick

- 5.1.1.2 Zirconia Brick

- 5.1.1.3 Silica Brick

- 5.1.1.4 Chromite Brick

- 5.1.1.5 Other Product Types (Carbides, Silicates)

- 5.1.2 Clay Refractory

- 5.1.2.1 High Alumina

- 5.1.2.2 Fireclay

- 5.1.2.3 Insulating

-

5.2 End-user Industry

- 5.2.1 Iron and Steel

- 5.2.2 Energy and Chemicals

- 5.2.3 Non-ferrous Metals

- 5.2.4 Cement

- 5.2.5 Ceramic

- 5.2.6 Glass

- 5.2.7 Other End-user Industries

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-east and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Chosun Refractories

- 6.4.2 HWI (Platinum Equity Advisors, LLC)

- 6.4.3 Imerys

- 6.4.4 Krosaki Harima Corporation

- 6.4.5 Puyang Refractories Group Co., Ltd

- 6.4.6 Refratechnik

- 6.4.7 RHI Magnesita N.V.

- 6.4.8 Saint-Gobain

- 6.4.9 Shinagawa Refractories Co. Ltd

- 6.4.10 Vesuvius

- *List Not Exhaustive

- 6.5 List of Other Prominent Companies

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Investments and Research on the Recycling of Refractories

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Refractories Industry Segmentation

A refractory material is resistant to decomposition by heat, pressure, or chemical attack at high temperatures and retains strength and form. For their safe, low-maintenance, and cost-effective operations, refractories are used as the primary material for internal linings in large industrial equipment.

The refractories market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into non-clay refractory and clay refractory. The end-user industry segments the market into iron and steel, energy and chemicals, non-ferrous metals, cement, ceramics, glass, and other end-user industries (pulp and paper processing, lime production, vessel incineration, and heat treating). The report also covers the market size and forecasts for the refractories market in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Product Type | Non-clay Refractory | Magnesite Brick | |

| Zirconia Brick | |||

| Silica Brick | |||

| Chromite Brick | |||

| Other Product Types (Carbides, Silicates) | |||

| Clay Refractory | High Alumina | ||

| Fireclay | |||

| Insulating | |||

| End-user Industry | Iron and Steel | ||

| Energy and Chemicals | |||

| Non-ferrous Metals | |||

| Cement | |||

| Ceramic | |||

| Glass | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-east and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Refractories Market Research FAQs

How big is the Refractories Market?

The Refractories Market size is expected to reach 57.36 million tons in 2025 and grow at a CAGR of 3.99% to reach 69.75 million tons by 2030.

What is the current Refractories Market size?

In 2025, the Refractories Market size is expected to reach 57.36 million tons.

Who are the key players in Refractories Market?

RHI Magnesita N.V., Chosun Refractories, Krosaki Harima Corporation, Puyang Refractories Group Co., Ltd. and Shinagawa Refractories Co., Ltd. are the major companies operating in the Refractories Market.

Which is the fastest growing region in Refractories Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Refractories Market?

In 2025, the Asia Pacific accounts for the largest market share in Refractories Market.

What years does this Refractories Market cover, and what was the market size in 2024?

In 2024, the Refractories Market size was estimated at 55.07 million tons. The report covers the Refractories Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Refractories Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Refractories Market Research

Mordor Intelligence provides a comprehensive analysis of the global refractories industry. We leverage our extensive experience in industrial materials research to deliver detailed insights. Our expert analysts explore refractory materials applications across various sectors. These range from furnace lining materials to specialized solutions for the steel industry. The report includes major players, such as North American refractories companies and leading manufacturers in India, offering a complete perspective on refractory products and technologies.

This detailed market analysis is available as an easy-to-download report PDF. It provides stakeholders with actionable insights into refractory industry trends and opportunities. The study covers various segments, including alkaline refractories, bauxite refractory castables, and magnesia zircon products. It also examines the performance of top refractory companies in the world. Our analysis benefits decision-makers across the value chain, from refractory manufacturers to end-users in the non-ferrous metals sector. It offers crucial data on market dynamics in key regions, including the GCC countries and emerging economies.