Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 0.78 Trillion |

| Market Size (2030) | USD 1.26 Trillion |

| Growth Rate (2025 - 2030) | 10.13% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Real Estate Market Analysis by Mordor Intelligence

The India Real Estate Market size is estimated at USD 0.78 trillion in 2025, and is expected to reach USD 1.26 trillion by 2030, at a CAGR of 10.13% during the forecast period (2025-2030).

Rapid urbanization, a growing middle class, and formalization under the Real Estate Regulation and Development Act (RERA) continue to propel demand across residential and commercial assets while rising institutional capital, technology adoption, and sustainability initiatives strengthen long-term fundamentals. Regulatory reforms, expanding mortgage availability, the expansion of Global Capability Centers (GCCs), and the deepening REIT ecosystem further diversify revenue streams, even as cost inflation and land bottlenecks temper margins for smaller developers. Fragmentation persists, yet scale advantages accrue to national developers and conglomerates that can navigate approvals, digitize sales processes, and meet green-building standards. Against this backdrop, the India real estate market is positioned to raise its GDP contribution from the current 7% to 13-15% by 2030, underscoring its strategic priority for policymakers and investors alike.

Key Report Takeaways

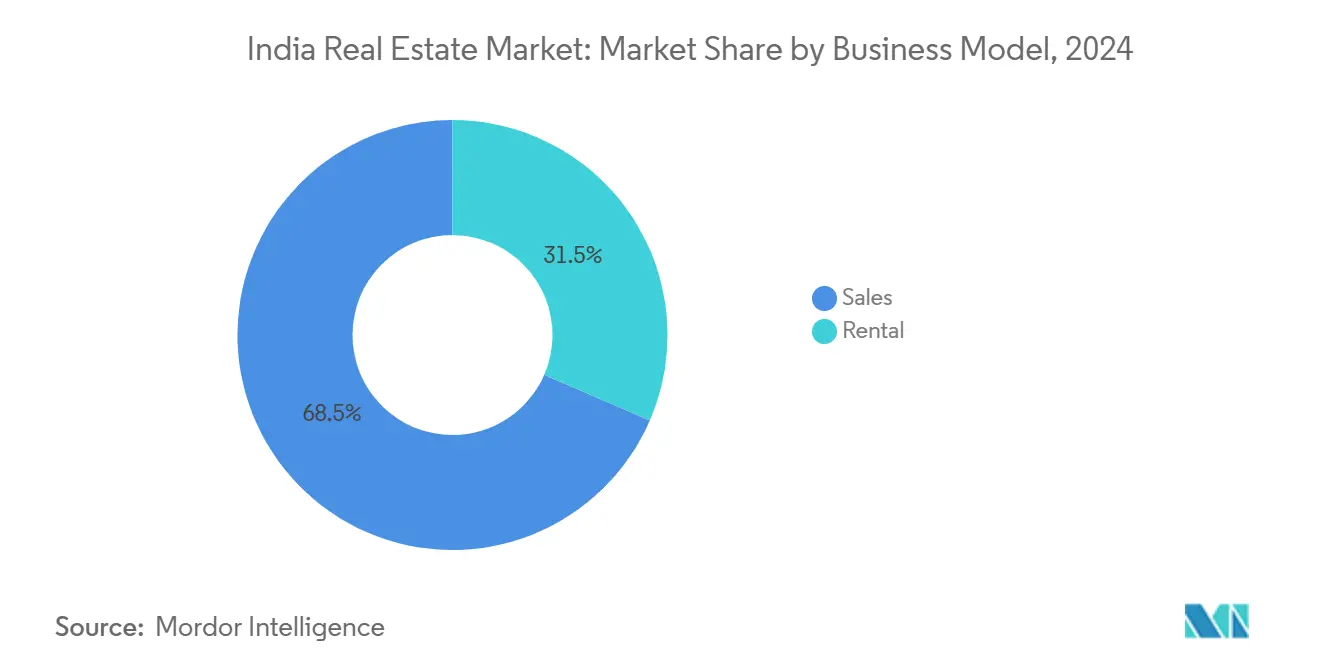

- By business model, sales secured 68.5% of the India real estate market share in 2024; rental is forecast to expand at a 10.84% CAGR through 2030.

- By property type, residential commanded 69.5% of the India real estate market share in 2024; commercial is advancing at a 10.71% CAGR to 2030.

- By end-user, individuals and households held 65.4% of the India real estate market size in 2024; corporates and SMEs are projected to grow at a 10.92% CAGR through 2030.

- By city, the Mumbai Metropolitan Region led with 27.1% of the India real estate market share in 2024, while Hyderabad records the highest projected CAGR at 11.23% to 2030.

India Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and rising incomes driving housing demand across metros and growth corridors | +2.8% | National, with concentration in metros and emerging Tier-2 cities | Long term (≥ 4 years) |

| GCC/IT-ITeS expansion and manufacturing/warehousing growth fueling commercial and industrial demand | +2.3% | Bengaluru, Hyderabad, Mumbai, Chennai, emerging Tier-2 cities | Long term (≥ 4 years) |

| Home loan availability and stable EMIs supporting affordable and mid-income segments | +2.1% | National, with higher impact in Tier-2/3 cities | Medium term (2-4 years) |

| Regulatory reforms (RERA) and formalization improving transparency and investor confidence | +1.9% | National, with varying enforcement across states | Medium term (2-4 years) |

| REITs and institutional capital deepening liquidity and exit avenues | +1.2% | Major metros with Grade A assets | Medium term (2-4 |

| Source: Mordor Intelligence | |||

Urbanization and Rising Incomes Drive Metropolitan Expansion

India's rapid urbanization and rising incomes are reshaping its metropolitan landscape. By 2030, urban dwellers will make up 38% of India's population, spurring a need for about 78 million new homes. This urban growth is also fueling the development of mixed-use corridors, seamlessly integrating housing with retail and office spaces. Developers are increasingly targeting Tier-2 cities, which now represent 44% of recent land acquisitions, drawn by the allure of lower entry costs and swifter approvals. A case in point is the land values along the Mumbai–Nagpur Expressway, which have surged 3.7 times over the past decade. This spike in value is attributed to enhanced connectivity, which has not only reduced commute times but also lured in manufacturing tenants. As disposable incomes rise, so does the appetite for luxury. In the Delhi-NCR region, premium property launches witnessed significant price escalations in 2024–25, driven by a constrained inventory. In a bid to fortify urban centers and explore new suburban territories, developers are now increasingly pairing residential towers with co-working spaces and lifestyle amenities.

GCC Expansion Drives Commercial Real Estate Transformation

GCCs are playing a pivotal role in reshaping the commercial real estate landscape. Global Capability Centers (GCCs) have increased their share of newly leased office space to 35%, up from 25% in 2022, and are poised to generate 4.5 million jobs by 2030. Advanced engineering hubs in Hyderabad, Bengaluru, and tier-2 cities like Coimbatore are now seeking tech-enabled, green-certified campuses. In response, developers are shifting focus to plug-and-play floor plates, data-center adjuncts, and round-the-clock utilities, while also incorporating co-living spaces for their rotating staff. This expanded presence not only diversifies portfolio concentration but also fosters the growth of ancillary retail and logistics clusters in southern and western corridors.

Home-Loan Accessibility Supports Affordable Housing Expansion

Affordable housing in India is witnessing significant growth, supported by favorable policies and financial incentives. Stable policy rates, the Pradhan Mantri Awas Yojana-Urban 2.0 subsidy, and extended mortgage tenures are driving homeownership for first-time buyers. The scheme offers an interest subsidy of up to 4% on loans equivalent to USD 300,000, significantly reducing effective EMIs for Economically Weaker Sections and Middle-Income Groups. Anticipated cuts from the Reserve Bank further enhance affordability, particularly in Mumbai and Pune, where price-to-income ratios are tight. In response, developers are introducing compact units, utilizing digitized booking and construction-linked payment plans to speed up cash conversion cycles and alleviate balance-sheet pressures.

Regulatory Reforms Enhance Market Transparency Despite Implementation Gaps

Regulatory reforms in the real estate market aim to enhance transparency and improve stakeholder confidence. Project registration, escrow segregation, and milestone-linked payments, mandated by the Real Estate Regulation and Development Act, bolster buyer confidence and enhance funding access. In Maharashtra, authorities granted conditional extensions to 541 lapsed schemes, striking a balance between consumer protection and developer viability. New legislation aims to digitize the 1908 Registration Act, introducing Aadhaar-based authentication and online title checks to combat fraud. However, inconsistent enforcement in some states has led to project delays, prompting civic associations to advocate for stricter timelines. Overall, while reforms broaden the channel for institutional funds, builders face increased compliance costs.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land acquisition, approvals, and compliance timelines delaying project execution | -1.8% | National, with acute impact in NCR, Mumbai, and emerging cities | Medium term (2-4 years) |

| Construction cost escalation and funding constraints for smaller developers | -1.4% | National, with higher impact on mid-tier developers | Short term (≤ 2 years) |

| Affordability pressures in Tier-1 cities limiting absorption at higher price points | -1.1% | Mumbai, Delhi NCR, Bengaluru, Chennai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land Acquisition Complexities Create Project Execution Bottlenecks

Land acquisition challenges remain a critical barrier to timely project execution. Title aggregation, variations in stamp duty, and delays due to litigation frequently prolong construction timelines. A dispute over a mere 1,600 m² on the Delhi–Dehradun Expressway held up a 200 km stretch until the Supreme Court stepped in, underscoring how minor parcels can significantly influence major projects. International developers, like Panattoni, have publicly called for more efficient single-window clearances to hasten warehouse constructions. While state amendments aim to reduce fraud by limiting the registration of certain unverified documents, they inadvertently complicate procedures. Smaller builders, often lacking legal expertise, tend to shy away from contested plots, paving the way for wealthier peers to consolidate.

Construction Cost Inflation Pressures Developer Margins

Construction costs have been rising steadily, putting significant pressure on developer profit margins. From 2021 to 2025, material and labor costs surged by 39%. As a result, the average cost of residential construction hit USD 33 per square foot. Wage inflation, meanwhile, spiked at 25% during the 2024–25 period. Steel prices fluctuated between USD 760 and USD 780 per metric tonne, and diesel prices stabilized around USD 1.10 per liter, leading to budgeting challenges. To counteract this volatility, developers are pre-booking commodities and utilizing off-site precast methods to minimize waste. However, mid-tier firms lacking scale procurement continue to face margin erosion. This has driven many of these firms to forge joint-development alliances with landowners, allowing them to share risks more effectively[1]Legal Correspondent, “Expressway land row stalls project,” The Economic Times, economictimes.indiatimes.com.

Segment Analysis

By Business Model: Sales Dominance Faces Rental Acceleration

In 2024, sales accounted for 68.5% of the Indian real estate market size. A cultural preference for property ownership and financial benefits such as mortgage interest deductions supported this. Homebuyer confidence improved as RERA implemented stricter escrow rules and penalized delays in project deliveries. This led to higher conversion rates, even for projects in early stages. Developers launched projects in bulk during festive seasons and introduced price locks to manage rising input costs. Additionally, institutional participation in resale transactions increased after REIT listings, which provided liquid exit options and reduced discount rates on established office spaces.

The rental market is expected to grow at a 10.84% CAGR by 2030. This growth is driven by increasing workforce mobility, the expansion of organized co-living operators, and corporate demand for managed housing. Regulations for Small & Medium REITs are enabling fractional ownership, which helps formalize landlord portfolios and stabilize cash flows. PropTech platforms like Blox use AI-based pricing tools to reduce vacancy periods and improve tenant screening, enhancing transparency and scalability. As housing affordability becomes more challenging in tier-1 cities, many young professionals are choosing to rent near transit hubs instead of buying homes in distant suburbs, contributing to a growing preference for renting.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Property Type: Commercial Acceleration Challenges Residential Dominance

Residential held 69.5% of the India real estate market share in 2024, anchored by unmet housing demand across income strata. Affordable schemes like PMAY-U 2.0 drive mid-income housing launches, while premium builders use green certifications to justify higher prices for high-net-worth buyers. In 2025, inventory overhang in major metros dropped below 8 months due to controlled supply releases and strong bookings during the festival season. Rising land costs have made vertical high-rises more common, but plotted developments are becoming popular in satellite towns where improved infrastructure has reduced commute times.

Commercial stock in the India real estate market is expected to grow at a 10.71% CAGR through 2030, supported by GCC expansions, omni-channel retail growth, and increased data center capacity. Developers are converting older central business district towers into hybrid offices with wellness features and touchless technology to meet post-pandemic requirements. Warehousing is meeting additional demand from e-commerce and manufacturing. Tier-2 logistics parks, with rental rates 20-25% lower than metro areas, are encouraging the development of regional networks. This growth in the sector diversifies revenue streams and provides a safeguard against slowdowns in the residential market.

By End-user: Corporate Demand Drives Market Evolution

Individuals and households controlled 65.4% of the India real estate market share in 2024, reflecting demographic dividend and cultural ownership aspirations. PMAY subsidies, zero-stamp-duty initiatives by some states, and longer loan tenures improve affordability, though price-to-income ratios in major metros remain high. Developers are using digital sales platforms with 3-D walkthroughs and instant mortgage pre-approvals, which reduce customer acquisition costs and speed up decision-making.

Corporate and SME occupiers are expected to grow at a 10.92% CAGR in the India real estate market, supported by GCC expansions, manufacturing policy incentives, and the growth of flexible space providers. Leasing strategies now include co-working spaces, which make up to 25% of portfolio footprints, to manage head-count fluctuations. Institutional funds like Nuvama–C&W’s USD 204 million Prime Offices Fund are focusing on Grade A+ towers with sustainability certifications, encouraging developers to upgrade older buildings for energy compliance. SMEs are using industrial condos in government-supported clusters, benefiting from plug-and-play utilities and simplified approvals.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

India's real estate market is mainly concentrated in six major metros, while secondary cities are attracting more capital and talent. The Mumbai Metropolitan Region holds a 27.1% market share, supported by its strong financial services sector, premium retail areas, and solid infrastructure projects. These factors help maintain price stability despite affordability challenges. Redevelopment in central areas like Worli and Lower Parel is adding new inventory without expanding the urban footprint, reducing supply-side risks.

Southern markets are showing stronger growth in the India real estate market. Hyderabad leads with an 11.23% forecast CAGR, driven by Telangana's single-window clearances and land bank auctions, which reduce project timelines. Bengaluru benefits from steady IT hiring and a growing data-center industry, boosting both office and residential demand, though traffic congestion and water scarcity remain concerns. Chennai uses its port connectivity to attract logistics and automotive businesses, while planned metro extensions improve the appeal of outer-ring suburbs[2]Property Desk, “Hyderabad absorbs record office space,” The Hindu, thehindu.com.

Tier-2 and Tier-3 cities are becoming more significant in the India real estate market, accounting for 44% of land transactions in 2024–25. Better highways, industrial corridors, and e-commerce logistics hubs support this growth. For example, land values near Samruddhi Circle in Nagpur increased 3.7× over the past decade due to the Mumbai–Nagpur Expressway, which reduces freight times. Colliers highlights 17 emerging cities, including Coimbatore, Indore, and Amritsar, where spiritual tourism and digital services are driving mixed-use developments. Retail developers plan to add 25 million sq ft in these cities by 2029, supported by rising incomes and limited organized supply. This diversification reduces concentration risks and strengthens the long-term demand for India's real estate market.

Competitive Landscape

India's real estate market remains fragmented, with national developers, regional specialists, and PropTech disruptors competing for market share. DLF, Godrej Properties, and Oberoi Realty benefit from strong brand recognition and access to cheaper debt. However, their combined share of primary sales in 2025 is expected to remain below 20%, leaving significant opportunities for mid-tier players. This fragmentation enables strategic site swaps and joint-development agreements, where landowners provide land, and developers contribute capital and execution capabilities.

Consolidation is gaining momentum in the India real estate market as large conglomerates seek inorganic growth. Adani's planned USD 1.5 billion acquisition of Emaar India is set to create a top-five portfolio, reflecting a focus on scale and steady rental income. Similarly, the partnership between Ajmera Realty and Rustomjee in Bandra redevelopment demonstrates how collaborations can reduce approval risks and speed up project launches. Future consolidation is likely to focus on smaller builders with financial difficulties, as they face challenges like rising costs[3]Corporate Bureau, “Adani in talks for Emaar India,” The Economic Times, economictimes.indiatimes.com.

Technology and sustainability are becoming key competitive factors in the India real estate market. Blox uses AI to reduce the time from search to sale and lower marketing costs. Blackstone and Panchshil Realty's USD 2.4 billion data-center project in Navi Mumbai, with a capacity of 500 MW, combines renewable energy goals with critical infrastructure, targeting the growing digital asset market. Developers pursuing LEED certifications now account for over 370 projects covering 8.5 million m², which helps attract tenants and strengthen portfolios. These strategies highlight a shift from relying on land-bank speculation to focusing on operational efficiency and service-driven value creation.

India Real Estate Industry Leaders

-

DLF Ltd

-

Macrotech Developers (Lodha Group)

-

Godrej Properties

-

Prestige Estates Projects

-

Oberoi Realty

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Maharashtra government approved the Maharashtra Housing Policy 2025 'My House, My Right', targeting Rs 70,000 crore (USD 8.4 billion) investment to create 3.5 million affordable housing units by 2030 through public-private partnerships and slum rehabilitation programs.

- March 2025: Bagmane Constructions acquired Cognizant Technology Solutions' Chennai headquarters for Rs 612 crore (USD 74 million), planning redevelopment of the 590,000 sq ft campus into an office park with scope for 3 million sq ft of space.

- March 2025: Adani Group entered advanced acquisition talks to purchase Emaar India for USD 1.4-1.5 billion, marking a significant consolidation move in India's real estate sector.

- February 2025: Blackstone and Panchshil Realty announced a strategic partnership to develop India's largest hyperscale data center with 500 MW capacity in Navi Mumbai, involving investment exceeding Rs 20,000 crore (USD 2.4 billion) across 14 buildings totaling 3 million square feet.

India Real Estate Market Report Scope

The real estate sector includes various phases of property dealings, including developing, selling, buying, leasing, and management processes in the commercial sector, residential sector, etc.

The report provides a comprehensive background analysis of the market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry.

The real estate industry in India is segmented by property type (residential, office, retail, hospitality, and industrial) and cities (Mumbai, Delhi, Pune, Chennai, Hyderabad, and Bangalore). The report offers market size and forecasts for all the above segments in value (USD).

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the India real estate market in 2025?

The India real estate market size is USD 0.78 trillion in 2025, with a projected 10.13% CAGR to 2030.

Which segment is growing fastest within India real estate?

The rental segment is the fastest within business models, expected to post a 10.84% CAGR through 2030.

Why is Hyderabad outperforming other cities?

Investor-friendly policies, large land parcels and surging GCC demand drive Hyderabad’s forecast 11.23% CAGR, the highest among Indian metros.

What role do REITs play in India?

REITs democratize access to Grade A assets; four listed trusts manage USD 17 billion and outperform the broader realty index.

How are input costs affecting developers?

Construction inputs rose 39% over four years, squeezing margins for small developers and spurring joint-development alliances.

What is the expected GDP contribution of real estate by 2030?

The sector’s share of GDP is projected to rise from 7% in 2025 to 13–15% by 2030.

Page last updated on: