| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 1.88 Billion |

| Market Size (2030) | USD 2.27 Billion |

| CAGR (2025 - 2030) | 3.87 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Americas |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Radiation Hardened Electronics Market Analysis

The Radiation Hardened Electronics Market size is estimated at USD 1.88 billion in 2025, and is expected to reach USD 2.27 billion by 2030, at a CAGR of 3.87% during the forecast period (2025-2030).

The radiation hardened electronics industry is experiencing significant transformation driven by technological advancements in semiconductor manufacturing and design methodologies. Companies are increasingly focusing on developing innovative solutions using advanced processes like silicon-on-insulator (SOI) technology and radiation hardening-by-design (RHBD) approaches to create more reliable and efficient components. The integration of artificial intelligence and machine learning capabilities alongside rad-hard chips is enabling space equipment to perform advanced analytics independently, reducing the need for constant data transmission to Earth for processing.

The global space economy has demonstrated remarkable growth, reaching USD 384 billion in revenue in 2022, creating substantial opportunities for radiation hardened electronics manufacturers. This growth is complemented by the increasing number of active satellites orbiting Earth, which reached 7,316 in 2022, representing a significant 51% increase compared to the previous year. The trend toward smaller, more cost-effective satellites is driving manufacturers to develop compact, efficient radiation hardened components that maintain high performance while reducing size and power consumption.

The nuclear power sector continues to expand globally, with the number of operational reactors increasing from 411 in 2022 to 436 by May 2023, driving demand for radiation hardened electronics in power plant monitoring and control systems. The Asia-Pacific region is leading this expansion with 39 reactors under construction in 2022, demonstrating the growing importance of radiation hardened electronics in ensuring safe and efficient nuclear power generation. Countries like India have made significant progress, achieving a nuclear power capacity of 6.8 gigawatts between 2021 and 2023.

Recent technological innovations have focused on developing more cost-effective radiation hardened solutions, particularly for commercial applications in lower Earth orbit where radiation exposure is less severe. Manufacturers are exploring new approaches such as commercial-off-the-shelf (COTS) components with radiation tolerant electronics features, which offer a balance between performance and cost-effectiveness. This trend is particularly evident in the development of new memory technologies, with companies introducing radiation hardened memory versions of conventional memory products to meet the growing demand for reliable data storage in space applications.

Radiation Hardened Electronics Market Trends

Increasing Instances of Satellite Launches and Space Exploration Activities

The proliferation of satellite launches and space exploration activities has become a primary driver for the radiation hardened electronics market. According to industry estimates by the U.S. Government Accountability Office (GAO), an additional 58,000 satellites are expected to be launched into Earth's orbit by 2030. This surge in satellite deployments is driven by both government space agencies and private companies seeking to establish robust satellite networks for enhanced communication, security, and infrastructure capabilities.

The increasing complexity of space missions and the growing focus on interplanetary exploration have further intensified the demand for radiation hardened electronics. For instance, in 2023, significant developments included India's successful Chandrayaan 3 lunar landing on the Moon's South Pole and the subsequent launch of the Aditya L1 solar mission. These achievements highlight the critical role of radiation hardened electronics in ensuring mission success, as these components must withstand extreme radiation environments beyond Earth's protective atmosphere. The trend is further supported by major space agencies increasing their investments, with NASA's approved budget for the financial year 2022 amounting to approximately USD 24 billion, including significant allocations for space operations and exploration technology.

Understand The Key Trends Shaping This Market

Download PDF

Growing Adoption of Radiation Hardened Electronics in Power Management and Nuclear Environment

The adoption of radiation hardened electronics in power management and nuclear environments has seen substantial growth, driven by the increasing emphasis on safety and efficiency in nuclear power facilities. Inside nuclear power plants, electrical and electronic systems are exposed to high-energy radiations that can severely impact functionality and overall safety. Ionizing radiation creates electron-hole pairs that can alter transistor parameters and potentially destroy them, while also causing leakage currents between circuits. This has made the installation of radiation hardened electrical/electronic systems with proper shielding a critical requirement for system designers.

The expansion of nuclear power capabilities globally has further accelerated this trend. Several countries have recently taken significant steps to extend operations at existing nuclear power plants and build new ones. For instance, in July 2023, the UK government announced grants of EUR 157 million to support its nuclear power industry through a new body aimed at driving the rapid expansion of nuclear power plants. Similarly, the Ontario government announced the start of pre-development work to build up to 4800 MWe of new nuclear capacity at Bruce Power's existing site. These developments, coupled with the Polish Government's approval to purchase three Westinghouse AP1000 reactors for its first atomic power plant, demonstrate the growing importance of radiation hardened electronics in ensuring safe and reliable nuclear power generation.

Segment Analysis: By End-User

Space Segment in Radiation-Hardened Electronics Market

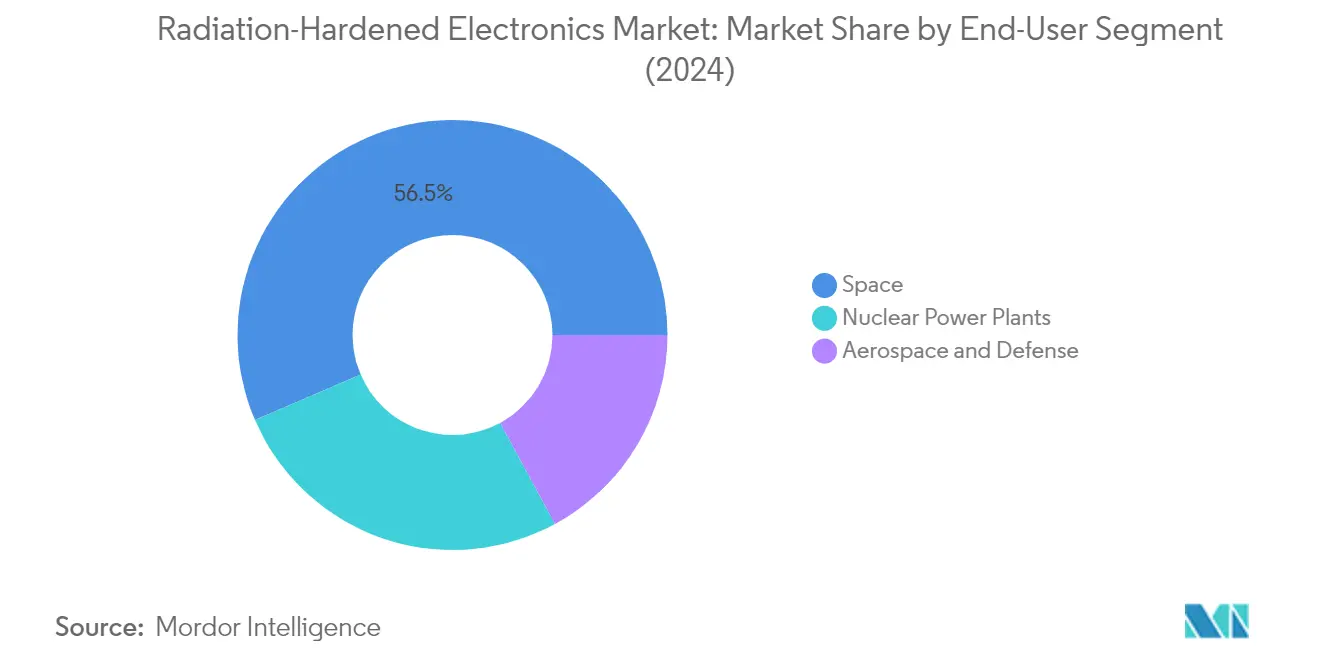

The Space segment dominates the radiation-hardened electronics market, commanding approximately 56% market share in 2024. This significant market position is primarily driven by the critical need for radiation-hardened components in satellites, spacecraft, and various space missions where exposure to radiation is exceptionally high. The segment's dominance is further strengthened by the increasing number of satellite launches, space exploration missions, and the growing commercial space industry. Major space agencies and private companies are investing heavily in new satellite constellations and deep space missions, which require highly reliable radiation-hardened electronics to ensure proper functionality in the harsh space environment. The segment's growth is also supported by the expanding applications of satellites in areas such as Earth observation, communication, navigation, and space-based internet services.

Nuclear Power Plants Segment in Radiation-Hardened Electronics Market

The Nuclear Power Plants segment is emerging as the fastest-growing segment in the radiation-hardened electronics market, with a projected growth rate of approximately 4% during 2024-2029. This accelerated growth is attributed to the increasing global focus on clean energy solutions and the subsequent expansion of nuclear power infrastructure worldwide. The segment's growth is driven by the critical need for reliable electronic systems that can withstand high radiation environments within nuclear facilities. The implementation of advanced safety systems, monitoring equipment, and control mechanisms in nuclear power plants is creating a strong demand for radiation-hardened electronics. Additionally, the modernization of existing nuclear facilities and the construction of new nuclear power plants across various regions are contributing to the segment's rapid growth trajectory.

Remaining Segments in End-User Segmentation

The Aerospace and Defense segment represents another crucial application area for radiation-hardened electronics, playing a vital role in military satellites, aircraft systems, and defense equipment. This segment's significance is underscored by the increasing integration of advanced electronic systems in modern military hardware and the growing emphasis on space-based defense capabilities. The segment benefits from continuous technological advancements in military electronics and the rising adoption of radiation-hardened components in critical defense applications. The aerospace sector, in particular, requires these specialized electronics for high-altitude aircraft operations and satellite communication systems, while the defense sector utilizes them in missile systems and military satellites.

Segment Analysis: By Component

Integrated Circuits Segment in Radiation-Hardened Electronics Market

The Integrated Circuits (ICs) segment dominates the radiation-hardened electronics market, commanding approximately 47% market share in 2024. This significant market position is attributed to ICs being fundamental building blocks of modern electronic devices, with their widespread adoption across major end-user industries including space, nuclear plants, and aerospace and defense. The segment's growth is particularly driven by the extensive use of power management ICs in space and nuclear power applications. Major manufacturers like Honeywell and BAE Systems continue to innovate in radiation-hardened microelectronics technologies, with developments in Silicon on Insulator Complementary Metal-Oxide-Semiconductor (SOI CMOS) technology specifically designed for digital and mixed-signal space microelectronics.

Memory Segment in Radiation-Hardened Electronics Market

The radiation-hardened memory segment is projected to exhibit the highest growth rate of approximately 4% during the forecast period 2024-2029. This accelerated growth is driven by increasing demands from space applications and military systems requiring reliable, radiation-hardened memory solutions. The segment's expansion is supported by technological advancements in various memory types including DRAM, NAND, and other non-volatile memories specifically designed for radiation-intensive environments. Recent developments in radiation-hardened memory technologies by key players focus on creating solutions that can withstand extreme radiation exposures while maintaining data integrity, particularly crucial for satellite operations and nuclear facility applications.

Remaining Segments in Component Market

The radiation-hardened electronics market also encompasses Microcontrollers & Microprocessors, Discrete components, and Sensors segments, each serving crucial roles in radiation-intensive applications. The Microcontrollers & Microprocessors segment is essential for providing computing capabilities in space and defense applications, while the Discrete segment offers critical components like radiation-hardened diodes and power transistors. The Sensors segment, though smaller in market share, remains vital for various monitoring and control applications in radiation-exposed environments. These segments collectively contribute to the comprehensive ecosystem of radiation-hardened electronics, supporting various mission-critical applications across space, defense, and nuclear power industries.

Radiation Hardened Electronics Market Geography Segment Analysis

Radiation-Hardened Electronics Market in the Americas

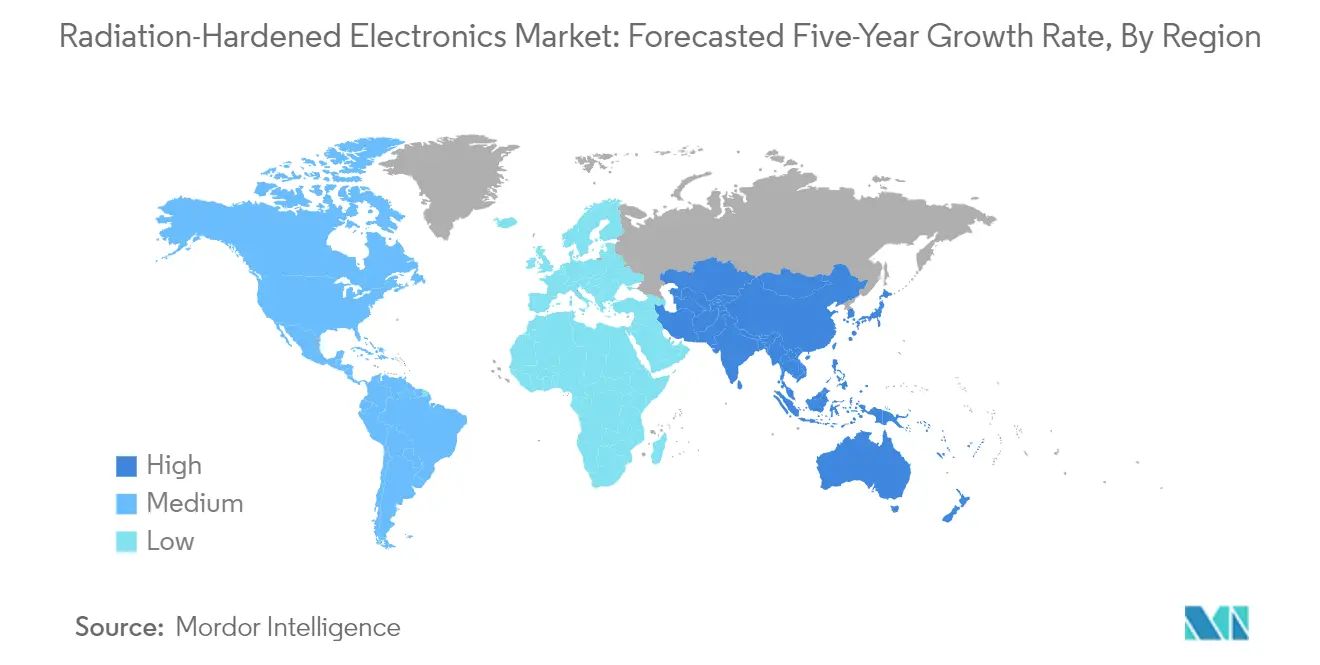

The Americas region continues to dominate the global radiation-hardened electronics market, commanding approximately 60% of the radiation-hardened electronics market share in 2024. This dominance is primarily attributed to the region being home to some of the world's leading space, aerospace, and defense organizations, particularly in the United States. The presence of major space agencies like NASA and private space companies such as SpaceX creates a robust demand for radiation-hardened components. The region's strong research and development infrastructure, supported by numerous prominent electronics manufacturing companies, contributes significantly to market growth. The increasing adoption of satellite-based telemetry and communication systems has further accelerated the demand for radiation-hardened electronics. The United States, in particular, maintains its position as a key market driver through its continuous investment in space exploration, defense applications, and nuclear power infrastructure. The region's focus on developing advanced radiation-hardening techniques and technologies, coupled with stringent quality standards and regulatory frameworks, ensures the production of highly reliable components for critical applications.

Radiation-Hardened Electronics Market in Europe

The European radiation-hardened electronics market has demonstrated consistent growth, recording approximately 3.5% growth annually from 2019 to 2024. The market's expansion is driven by the European Union's increasing focus on space exploration and satellite technology development. European countries, particularly Germany, France, and the United Kingdom, maintain significant aerospace and defense manufacturing capabilities, creating sustained demand for radiation-hardened electronics. The region's commitment to nuclear power infrastructure development has also contributed to market growth. European manufacturers are actively developing innovative radiation-hardening designs and technologies, particularly for aerospace applications. The presence of major semiconductor manufacturers and research institutions has enabled the region to maintain its competitive edge in developing advanced radiation-hardened solutions. The European Space Agency's continued investments and collaborative projects have further strengthened the market ecosystem, fostering innovation and technological advancement in radiation-hardened electronics.

Radiation-Hardened Electronics Market in Asia Pacific

The Asia Pacific radiation-hardened electronics market is positioned for robust growth, with projections indicating approximately 4.2% annual growth from 2024 to 2029. The region's market expansion is driven by increasing investments in space programs and commercial satellite projects, particularly in countries like China, Japan, and India. The growing semiconductor industry in the region has created a strong foundation for radiation-hardened electronics manufacturing. Countries are increasingly focusing on developing indigenous capabilities in military and defense electronics, driving demand for radiation-hardened components. The rise in nuclear power plant installations across various Asian countries has created additional demand channels. Research institutions in the region are actively working on innovative radiation-hardening designs, particularly for aerospace applications. The increasing collaboration between government agencies and private sector companies has created a favorable environment for market growth. The region's focus on developing cost-effective solutions while maintaining high reliability standards positions it as a significant player in the global market.

Radiation-Hardened Electronics Market in the Rest of the World

The Rest of the World region, encompassing the Middle East and Africa, represents an emerging market for radiation-hardened electronics. The market is characterized by growing investments in space programs and satellite technology development across various countries. The increasing focus on nuclear power generation in several nations has created new opportunities for radiation-hardened electronic components. The region is witnessing a rise in defense modernization programs, driving demand for advanced electronic systems capable of operating in harsh environments. Market vendors are expanding their presence through strategic partnerships and collaborations with local entities. The growing emphasis on developing indigenous capabilities in satellite manufacturing and space technology is expected to drive future market growth. The region's increasing focus on energy security and nuclear power development creates sustained demand for radiation-hardened electronics in power plant applications. The market continues to evolve with increasing investments in research and development activities.

Get Analysis on Important Geographic Markets

Download PDF

Radiation Hardened Electronics Market Overview

Top Companies in Radiation-Hardened Electronics Market

The radiation-hardened electronics market is characterized by continuous product innovation across major players, with companies focusing on developing advanced components for space, defense, and nuclear applications. Companies are demonstrating operational agility through strategic partnerships with semiconductor foundries and research institutions to enhance manufacturing capabilities while controlling costs. Market leaders are investing heavily in research and development to expand their product portfolios, particularly in areas like radiation-hardened components, memories, processors, and power management solutions. Strategic moves include vertical integration of manufacturing processes, development of proprietary radiation-hardening technologies, and expansion of testing and certification capabilities. Geographic expansion strategies are evident through the establishment of new manufacturing facilities, particularly in regions with growing space and defense sectors, while companies are also strengthening their distribution networks to improve market penetration and customer service capabilities.

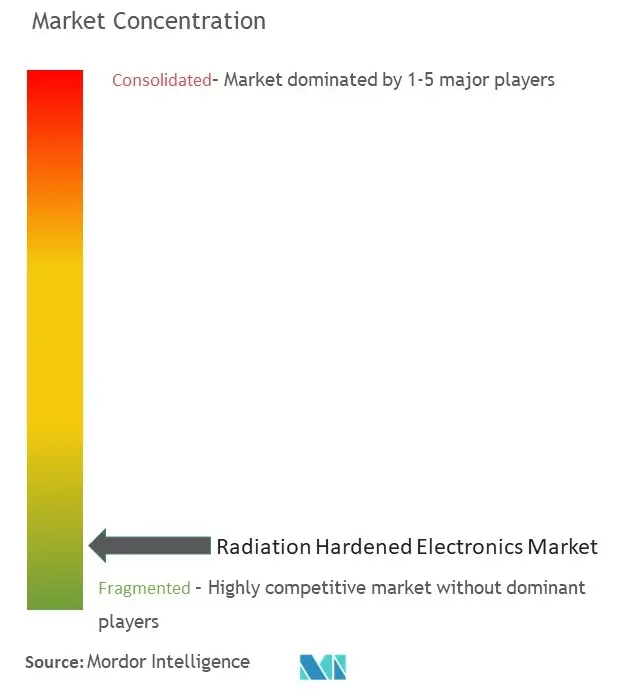

Consolidated Market Led By Global Conglomerates

The radiation-hardened electronics market exhibits a relatively consolidated structure dominated by large multinational conglomerates with diverse technological capabilities and extensive manufacturing resources. These established players leverage their strong financial positions, advanced research facilities, and long-standing relationships with government space agencies and defense contractors to maintain their market positions. The market shows a clear distinction between global technology conglomerates offering broad product portfolios and specialized manufacturers focusing on specific radiation-hardened semiconductors, with the former holding significant market share advantages due to their integrated capabilities and economies of scale.

The industry has witnessed strategic mergers and acquisitions aimed at expanding technological capabilities and market reach, with larger companies acquiring specialized firms to enhance their radiation-hardening expertise and product offerings. Market entry barriers remain high due to substantial capital requirements, complex certification processes, and the need for specialized manufacturing capabilities. Regional players are increasingly seeking partnerships with global leaders to access advanced technologies and expand their market presence, while established companies are pursuing collaborative agreements to share research and development costs and accelerate innovation cycles.

Innovation and Adaptability Drive Market Success

Success in the radiation-hardened electronics market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and meeting stringent reliability requirements. Incumbent players are focusing on developing next-generation radiation-hardening technologies, expanding their testing and qualification capabilities, and strengthening their supply chain relationships to maintain their market positions. Companies are also investing in advanced manufacturing processes and automation to improve production efficiency and reduce costs, while maintaining focus on quality assurance and compliance with evolving industry standards.

For contenders seeking to gain market share, differentiation through specialized product offerings and focus on emerging application areas presents viable opportunities. The high concentration of end-users in government space agencies and defense sectors necessitates strong relationship building and proven track records in product reliability. While substitution risk remains low due to the specialized nature of radiation-hardened components, regulatory compliance and export control restrictions significantly influence market dynamics. Companies must navigate complex regulatory environments while maintaining technological advancement and cost competitiveness to succeed in this demanding market.

Radiation Hardened Electronics Market Leaders

-

Honeywell International Inc.

-

BAE Systems PLC

-

Texas Instruments

-

Data Device Corporation

-

Frontgrade Technologies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Radiation Hardened Electronics Market News

- October 2023: Indian University (IU) announced that it had secured and would invest about USD 111 million over the next few years to advance its leadership in microelectronics and nanotechnology. The university has also made a provision of USD 10 million to launch the new Center for Reliable and Trusted Electronics, which aims to take forward research activities focused primarily on the modeling and simulation of radiation effects and the design of radiation-hardened technologies.

- June 2023: Texas Instruments (TI) announced an expansion of its manufacturing operation in Malaysia by building two new assembly and test factories in Kuala Lumpur and Melaka. Through this expansion, the company aims to extend its cost advantage and have greater control of the supply chain.

Radiation Hardened Electronics Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Raw Material Analysis for Radiation-Hardened Components

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Instances of Satellite Launches and Space Exploration Activities

- 5.1.2 Growing Adoption of Radiation Hardened Electronics in Power Management and Nuclear Environment

-

5.2 Market Challenges/Restraints

- 5.2.1 High Designing and Development Cost

6. MARKET SEGMENTATION

-

6.1 By End-user

- 6.1.1 Space

- 6.1.2 Aerospace and Defense

- 6.1.3 Nuclear Power Plants

-

6.2 By Component

- 6.2.1 Discrete

- 6.2.2 Sensors

- 6.2.3 Integrated Circuit

- 6.2.4 Microcontrollers and Microprocessors

- 6.2.5 Memory

-

6.3 By Geography***

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

- 7.1 Vendor Ranking Analysis

-

7.2 Company Profiles*

- 7.2.1 Honeywell International Inc.

- 7.2.2 BAE Systems PLC

- 7.2.3 Texas Instruments

- 7.2.4 Data Device Corporation

- 7.2.5 Frontgrade Technologies

- 7.2.6 STMicroelectronics International NV

- 7.2.7 Infineon Technologies AG

- 7.2.8 Microchip Technology Inc.

- 7.2.9 Micropac Industries Inc.

- 7.2.10 Renesas Electronic Corporation

- 7.2.11 Solid State Devices Inc.

- 7.2.12 Advanced Micro Devices, Inc.

- 7.2.13 Everspin Technologies Inc.

- 7.2.14 Vorago Technologies

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Radiation Hardened Electronics Market Industry Segmentation

Radiation hardening is a technique to design and manufacture electronics for use in high-altitude or hazardous applications where the fielded equipment is susceptible to damage and malfunctions caused by gamma and neutron radiation. The radiation-hardened electronics market comprises sophisticated radiation-hardened electronics systems used for various space, military, and commercial applications, such as satellite system power supply, switching regulators, microprocessors in the military, and control systems in nuclear reactors.

The radiation-hardened electronics market is segmented by end-user (space, aerospace and defense, and nuclear power plants), component (discrete, sensor, integrated circuit, memory, and microcontrollers and microprocessors), geography (Americas, Europe, Asia Pacific, and Rest of the World). The report offers the market size and forecasts in value (USD) for all the above segments.

| By End-user | Space |

| Aerospace and Defense | |

| Nuclear Power Plants | |

| By Component | Discrete |

| Sensors | |

| Integrated Circuit | |

| Microcontrollers and Microprocessors | |

| Memory | |

| By Geography*** | Americas |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Radiation Hardened Electronics Market Research FAQs

How big is the Radiation Hardened Electronics Market?

The Radiation Hardened Electronics Market size is expected to reach USD 1.88 billion in 2025 and grow at a CAGR of 3.87% to reach USD 2.27 billion by 2030.

What is the current Radiation Hardened Electronics Market size?

In 2025, the Radiation Hardened Electronics Market size is expected to reach USD 1.88 billion.

Who are the key players in Radiation Hardened Electronics Market?

Honeywell International Inc., BAE Systems PLC, Texas Instruments, Data Device Corporation and Frontgrade Technologies are the major companies operating in the Radiation Hardened Electronics Market.

Which is the fastest growing region in Radiation Hardened Electronics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Radiation Hardened Electronics Market?

In 2025, the Americas accounts for the largest market share in Radiation Hardened Electronics Market.

What years does this Radiation Hardened Electronics Market cover, and what was the market size in 2024?

In 2024, the Radiation Hardened Electronics Market size was estimated at USD 1.81 billion. The report covers the Radiation Hardened Electronics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Radiation Hardened Electronics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Radiation Hardened Electronics Market Research

Mordor Intelligence provides comprehensive insights into the radiation hardened electronics market through detailed industry analysis and market data. Our research extensively covers radiation hardened components, radiation hardened processors, and radiation hardened memory segments, offering stakeholders a thorough understanding of market dynamics. The report pdf includes in-depth market forecasts, growth trends, and competitive landscape analysis of key players in the aerospace electronics sector, with special focus on emerging technologies in radiation hardened semiconductors and radiation tolerant electronics. Our coverage spans regional markets including the Asia Pacific radiation-hardened electronics market and Europe radiation-hardened electronics market, providing actionable intelligence for strategic decision-making.

Beyond market research, our consulting expertise helps organizations navigate the complex landscape of radiation hardened electronics development and implementation. We support clients with technology scouting for advanced radiation hardening techniques, R&D and patent analysis for innovative solutions, and competition assessment in the rapidly evolving rad hardened electronics space. Our services include product claims assessment for new radiation resistant electronics solutions, customer need analysis for specific applications, and comprehensive evaluation of emerging technologies in radiation hardened microelectronics. Through B2B surveys and expert interviews, we provide strategic insights that help businesses identify growth opportunities and optimize their market positioning.