| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 3.62 Billion |

| Market Size (2030) | USD 4.66 Billion |

| CAGR (2025 - 2030) | 5.20 % |

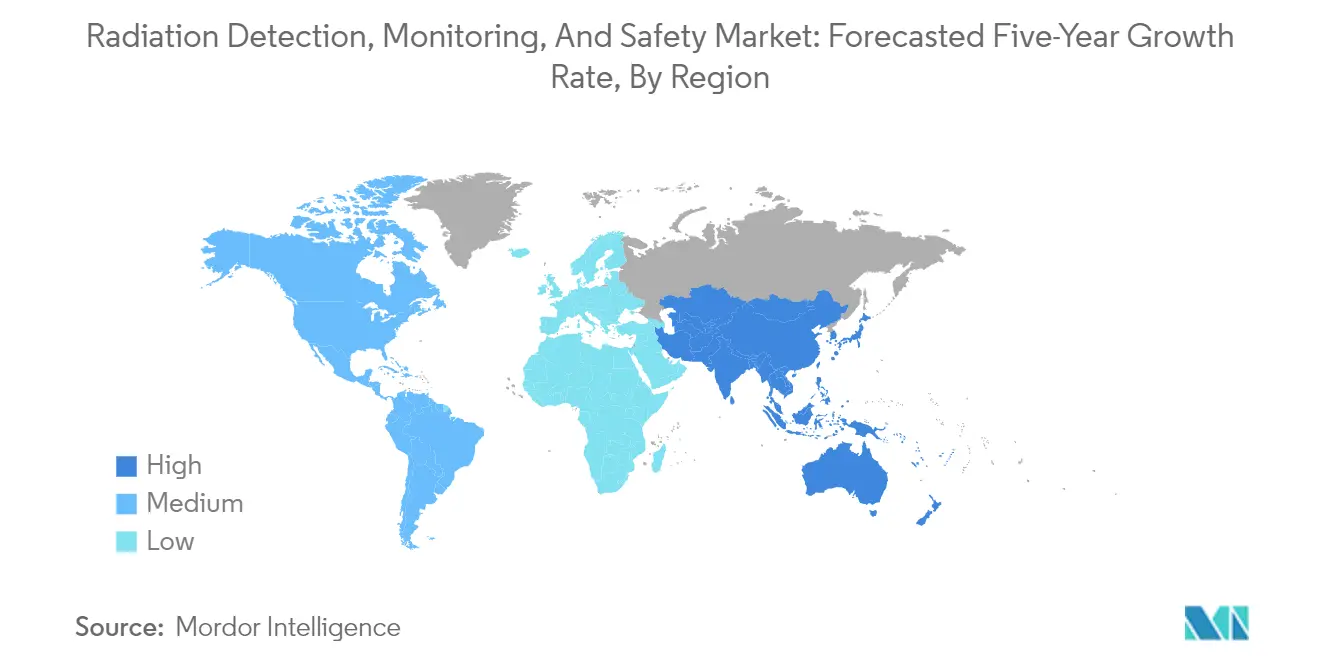

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Radiation Detection, Monitoring, And Safety Market Analysis

The Radiation Detection, Monitoring, And Safety Market size is estimated at USD 3.62 billion in 2025, and is expected to reach USD 4.66 billion by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

The radiation detection, monitoring, and safety market is experiencing significant transformation driven by the expanding nuclear power sector and industrial applications. According to the World Energy Outlook report, nuclear power capacity is projected to grow by over 15% through 2040, with total generating capacity expected to reach 13,418 GWe. This expansion is particularly evident in emerging economies, where governments are investing heavily in nuclear infrastructure development and modernization programs. The industry is witnessing increased emphasis on advanced radiation measurement technologies and automated monitoring systems, particularly in critical infrastructure facilities and nuclear power plants.

The manufacturing sector's robust growth is creating substantial opportunities for radiation detection equipment and monitoring solutions, particularly in quality control and non-destructive testing applications. In China, industrial production registered a 4.6% increase in 2023 compared to the previous year, according to the National Bureau of Statistics, indicating strong demand for radiation monitoring system equipment in manufacturing processes. The integration of artificial intelligence and machine learning capabilities in radiation measurement systems is enabling more precise measurements and real-time monitoring capabilities, enhancing both efficiency and safety protocols across industrial applications.

The industry is witnessing a significant shift toward more sophisticated and integrated radiation monitoring systems, particularly in critical infrastructure and security applications. Nuclear power facilities are increasingly adopting advanced radiation detector technologies that offer improved sensitivity, accuracy, and real-time monitoring capabilities. The trend toward digital transformation has led to the development of networked radiation monitoring systems that can provide instantaneous alerts and comprehensive data analytics, enabling more effective radiation protection management and emergency response protocols.

The market is experiencing notable advancement in personal radiation detector devices, with a focus on developing more compact, accurate, and user-friendly solutions. Manufacturers are introducing innovative features such as wireless connectivity, cloud-based data management, and mobile application integration in their radiation detection equipment products. These technological improvements are particularly important as nuclear power is expected to contribute approximately 8.5% to global power generation by 2040, necessitating enhanced radiation protection measures and monitoring capabilities across the nuclear power sector and related industries.

Radiation Detection, Monitoring, And Safety Market Trends

Growing Nuclear Power Infrastructure & Safety Requirements

The expanding global nuclear power infrastructure has become a primary driver for radiation safety equipment adoption. According to recent data from the Energy Information Administration (EIA), China alone operates 55 nuclear power reactors as of May 2023, with substantial electricity generation capacity reaching 69 terawatt-hours in early 2024. This rapid expansion of nuclear facilities necessitates comprehensive radiation monitoring equipment to ensure worker safety, environmental protection, and compliance with stringent regulatory requirements.

The increasing focus on nuclear energy as a clean power source has led to significant investments in safety infrastructure. For instance, ExxonMobil projects that by 2040, the global nuclear energy demand will reach approximately 45 quadrillion BTUs, highlighting the critical need for advanced radiation protection device systems. This growth in nuclear power generation has spurred the development of more sophisticated radiation monitoring equipment, including automated reader instruments, electronic radiation measuring devices, and comprehensive facility monitoring systems that provide real-time radiation level tracking and early warning capabilities.

Understand The Key Trends Shaping This Market

Download PDF

Rising Cancer Cases and Medical Applications

The increasing prevalence of cancer cases worldwide has significantly driven the demand for radiation dosimeter and monitoring equipment in medical applications. According to the American Cancer Society's latest projections, over 2 million new cancer cases are expected to be diagnosed in the United States in 2024, while the Globocan estimates suggest that globally, more than 30 million individuals will be living with cancer by 2040. This substantial patient population requires precise radiation monitoring during diagnostic procedures and treatment, driving the adoption of advanced radiation sensor equipment.

The medical sector's growing reliance on radiation-based treatments and diagnostics has necessitated more sophisticated monitoring systems. According to the Society for Radiological Protection, while naturally occurring background radiation contributes to 88% of annual radiation exposure, medical procedures account for the remaining 12%, emphasizing the critical need for accurate radiation monitoring in healthcare settings. This has led to increased adoption of personal dosimeters, area process monitors, and environmental radiation monitors across healthcare facilities, particularly in radiology departments, emergency care units, and nuclear medicine facilities where radiation exposure must be carefully controlled to ensure patient and staff safety.

Industrial Applications and Safety Compliance

The manufacturing sector's increasing adoption of non-destructive testing (NDT) methods has emerged as a significant driver for radiation detection and monitoring equipment. Industrial radiography, utilizing various radiation-based techniques including gamma-ray scanning and neutron radiography, requires sophisticated detection equipment to ensure worker safety while maintaining product quality. These applications demand high-precision monitoring systems capable of detecting multiple types of radiation across various industrial environments, from automotive manufacturing to aerospace component testing.

The stringent safety regulations governing industrial radiation usage have further accelerated the adoption of advanced monitoring systems. Industrial facilities are increasingly implementing comprehensive radiation monitoring solutions that combine personal dosimeters, area monitors, and automated detection systems to create multi-layered safety protocols. This trend is particularly evident in sectors dealing with radioactive materials, such as metal recycling facilities and industrial radiography operations, where continuous monitoring is essential for preventing exposure risks and ensuring regulatory compliance.

Healthcare Infrastructure Modernization

The ongoing modernization of healthcare infrastructure globally has become a crucial driver for the radiation detection and monitoring market. Healthcare facilities are increasingly incorporating advanced diagnostic and imaging technologies that utilize radiation, necessitating sophisticated monitoring systems to ensure safety compliance. This modernization includes the installation of new diagnostic radiology equipment and the integration of medical isotopes in various procedures, creating a sustained demand for radiation portal monitor solutions.

The emphasis on radiation safety in modern healthcare settings has led to the implementation of comprehensive monitoring systems that protect both patients and healthcare workers. These systems include real-time radiation monitoring devices, personal dosimeters for medical staff, and environmental monitoring systems that track radiation levels throughout medical facilities. The integration of these technologies is particularly crucial in specialized departments such as interventional radiology, nuclear medicine, and radiation therapy units, where precise radiation monitoring is essential for maintaining safety standards while delivering effective patient care.

Segment Analysis: By Product Type

Detection and Monitoring Segment in Radiation Detection, Monitoring, and Safety Market

The Detection and Monitoring segment dominates the global radiation detection, monitoring, and safety market, holding approximately 69% market share in 2024. This segment primarily includes personal dosimeters, area process monitors, environmental radiation detectors, surface contamination monitors, and radioactive material monitors. The segment's dominance is attributed to its widespread adoption across healthcare, energy, and power industries, along with increasing implementation at security checkpoints in airports and public spaces. The availability of advanced instruments, such as automated reader instruments, electronic radiation measurement instruments, alarm badges, and thermoluminescent dosimeters (TLDs), has significantly expanded the application range of detection and monitoring devices. Furthermore, the development of autonomous robots and mobile sensor networks for spatial distribution of radiation levels has created new opportunities in this segment, while the emergence of photonic radiation detectors has enabled their use in high-radiation environments for critical medical, industrial, and research applications.

Safety Segment in Radiation Detection, Monitoring, and Safety Market

The Safety segment is experiencing the fastest growth in the radiation detection, monitoring, and safety market, projected to grow at approximately 7% during the forecast period 2024-2029. This growth is driven by increasing concerns related to radiation exposure and stringent government regulations regarding safety standards for working in radiation-prone zones. The segment's expansion is further supported by the rising demand for lead-free protective aprons that maintain the highest IEC standards while offering maximum comfort to users. The innovative Bi-Layer technology in these products provides enhanced radiation protection against secondary or scatter radiation, making them particularly valuable in medical and industrial applications. Additionally, the segment is witnessing significant technological advancements in personal protective equipment (PPE) design and materials, focusing on lightweight, comfortable, and highly effective radiation protection solutions for professionals working in radiation-exposed environments.

Segment Analysis: By End-User Industry

Medical and Healthcare Segment in Radiation Detection, Monitoring, and Safety Market

The Medical and Healthcare segment dominates the radiation detection, monitoring, and safety market, holding approximately 32% of the market share in 2024. This significant market position is driven by the increasing adoption of dosimeters and detectors across various medical applications, including radiology, emergency care, dentistry, nuclear medicine, and therapy applications. The segment's prominence is further strengthened by the rising implementation of radiation therapy in cancer treatment, where proper medical radiation measurement, monitoring, and safety equipment are essential to detect radiation exposure in the environment. The widespread use of diagnostic radiology equipment and medical isotopes in hospitals has also contributed to the segment's dominance. Additionally, the increasing investments in cancer therapy facilities and the promotion of nuclear medicine applications have further solidified the segment's leading position in the market.

Homeland Security and Defense Segment in Radiation Detection, Monitoring, and Safety Market

The Homeland Security and Defense segment is projected to exhibit the highest growth rate of approximately 10% during the forecast period 2024-2029. This exceptional growth is attributed to the increasing demand for radiation detectors in commercial and public hotspots, particularly in airports and critical infrastructure facilities. The segment's growth is driven by substantial investments from governments worldwide to equip their armed forces with modern defense weapons platforms and next-generation technologies. The rising focus on preventing nuclear terrorism and the need for sophisticated nuclear radiation detection systems at borders, seaports, and public spaces has created a strong growth trajectory. The segment is witnessing increased adoption of advanced technologies such as portable gamma radiation detection systems and automated radiation detection capabilities for counterterrorism applications.

Remaining Segments in End-User Industry

The Industrial, Energy and Power, and Other End-user Industries segments collectively form a substantial portion of the radiation detection, monitoring, and safety market. The Industrial segment is particularly significant in applications such as non-destructive testing, quality control in manufacturing, and worker safety in various industrial processes. The Energy and Power segment plays a crucial role in nuclear power plant safety and monitoring, while also supporting radiation protection in conventional power generation facilities. The Other End-user Industries segment encompasses diverse applications, including environmental monitoring, research institutions, and waste management facilities. These segments continue to evolve with technological advancements and increasing safety regulations across different industries.

Radiation Detection, Monitoring, And Safety Market Geography Segment Analysis

Radiation Detection, Monitoring, and Safety Market in North America

North America continues to dominate the global radiation detector market, holding approximately 41% of the market share in 2024. The region's leadership position is attributed to its advanced healthcare infrastructure, extensive nuclear power operations, and stringent regulatory framework for radiation safety. The presence of major radiation detection equipment companies like Thermo Fisher Scientific, Mirion Technologies, and Landauer has created a robust ecosystem for innovation and product development. The region's commitment to homeland security and defense applications has driven significant investments in radiation monitoring system technologies, particularly at borders, airports, and critical infrastructure facilities. The healthcare sector remains a primary growth driver, with increasing adoption of radiation therapy and diagnostic imaging procedures requiring sophisticated monitoring equipment. The industrial sector, particularly in oil and gas, manufacturing, and mining, continues to demonstrate strong demand for radiation safety equipment. Additionally, the region's focus on nuclear power plant safety and monitoring has sustained the demand for advanced radiation detection systems and personal dosimetry solutions.

Radiation Detection, Monitoring, and Safety Market in Europe

The European market for radiation detection, monitoring, and safety equipment has demonstrated steady growth, registering approximately 4% annual growth from 2019 to 2024. The market is characterized by its strong emphasis on nuclear safety equipment, with countries like France maintaining significant nuclear power operations. The region's regulatory landscape continues to evolve with stringent safety standards driving the adoption of advanced radiation monitoring systems. The healthcare sector remains a crucial end-user, with increasing investments in radiation therapy and diagnostic imaging facilities. Industrial applications, particularly in manufacturing and petrochemical sectors, continue to drive demand for radiation safety equipment. The region's focus on border security and illicit material detection has led to increased deployment of radiation monitoring systems at key checkpoints. Research institutions and laboratories across Europe maintain steady demand for sophisticated radiation detection equipment. The market also benefits from ongoing technological advancements in radiation monitoring systems, particularly in wireless and real-time monitoring solutions.

Radiation Detection, Monitoring, and Safety Market in Asia-Pacific

The Asia-Pacific region represents the most dynamic market for radiation detection, monitoring, and safety equipment, with projections indicating approximately 9% growth annually from 2024 to 2029. The market is driven by rapid industrialization, expanding nuclear power infrastructure, and increasing healthcare investments across major economies like China, Japan, and India. The region's growing focus on nuclear power generation has created substantial demand for radiation monitoring systems and safety equipment. Healthcare modernization initiatives across developing economies are driving the adoption of advanced radiation therapy equipment, necessitating sophisticated monitoring solutions. The industrial sector, particularly manufacturing and mining, continues to expand its usage of radiation detection equipment for quality control and worker safety. Rising awareness about radiation safety in healthcare settings has led to increased adoption of personal dosimetry solutions. The market is also benefiting from government initiatives to enhance border security and prevent illicit trafficking of radioactive materials. Technological advancements and increasing local manufacturing capabilities are making radiation detection solutions more accessible across the region.

Radiation Detection, Monitoring, and Safety Market in Latin America

The Latin American market for radiation detection, monitoring, and safety equipment is experiencing steady development, driven by growing industrial applications and healthcare sector modernization. The region's expanding oil and gas sector, particularly in countries like Brazil and Venezuela, creates significant demand for radiation monitoring equipment. Nuclear power development initiatives, though limited, contribute to market growth through requirements for sophisticated radiation detection systems. The healthcare sector's modernization efforts, especially in cancer treatment facilities, drive demand for radiation monitoring solutions. Industrial applications, particularly in mining and manufacturing, continue to adopt radiation safety equipment to ensure worker protection. The market benefits from increasing awareness about radiation safety and regulatory compliance requirements. Regional governments' focus on enhancing border security has led to growing adoption of radiation detection systems at key checkpoints. The market also sees increasing demand from research institutions and laboratories requiring precise radiation measurement capabilities.

Radiation Detection, Monitoring, and Safety Market in Middle East & Africa

The Middle East and African market for radiation detection, monitoring, and safety equipment demonstrates growing potential, driven by increasing investments in nuclear power infrastructure and healthcare modernization. The region's oil and gas industry remains a significant consumer of radiation detection equipment, particularly in the Gulf Cooperation Council countries. Healthcare sector development, especially in advanced medical facilities across major urban centers, drives demand for radiation monitoring solutions. The market benefits from increasing awareness about radiation safety in industrial applications, particularly in mining and manufacturing sectors. Growing focus on border security and prevention of illicit material trafficking has led to increased adoption of radiation surveillance systems. The development of nuclear power facilities, particularly in countries like Saudi Arabia and the UAE, creates demand for comprehensive radiation monitoring solutions. Research institutions and educational facilities across the region maintain steady demand for radiation detection equipment. The market also sees growth from increasing industrial safety regulations and compliance requirements.

Get Analysis on Important Geographic Markets

Download PDF

Radiation Detection, Monitoring, And Safety Industry Overview

Top Companies in Radiation Detection, Monitoring, and Safety Market

The market is characterized by companies focusing heavily on technological innovation, particularly in developing next-generation radiation detection equipment systems and smart monitoring solutions. Companies are investing substantially in research and development to create more precise, portable, and user-friendly radiation detection equipment, with an emphasis on incorporating artificial intelligence and machine learning capabilities. Strategic partnerships and collaborations with research institutions and government agencies have become increasingly common to enhance product development and market reach. Operational agility is demonstrated through companies expanding their manufacturing capabilities while simultaneously developing specialized solutions for different end-user segments. Geographic expansion strategies are primarily focused on emerging markets, particularly in the Asia-Pacific and Middle East regions, where nuclear power development and healthcare infrastructure are growing rapidly.

Market Dominated by Specialized Technology Leaders

The radiation detection, monitoring, and safety market exhibits a mix of large conglomerates and specialized technology providers, with companies like Thermo Fisher Scientific, General Electric, and Mirion Technologies holding significant market positions. These established players leverage their extensive distribution networks, comprehensive product portfolios, and strong research capabilities to maintain their market dominance. The market structure is relatively consolidated in developed regions, with a handful of key players controlling major market share through their established brand presence and technological expertise. Regional markets, particularly in developing economies, show more fragmentation with local players focusing on specific application segments or geographical territories.

The market has witnessed significant merger and acquisition activity, with larger companies acquiring specialized technology providers to expand their product offerings and geographical presence. Companies are particularly interested in acquiring firms with complementary technologies or a strong presence in emerging markets. This consolidation trend is driven by the need to achieve economies of scale, enhance technological capabilities, and expand market reach. Strategic partnerships between radiation detection equipment companies and healthcare providers, research institutions, and government agencies have become increasingly common, creating integrated solution offerings and strengthening market positions.

Innovation and Adaptability Drive Market Success

For incumbent companies to maintain and expand their market share, focus needs to be placed on continuous product innovation, particularly in developing more accurate and cost-effective detection solutions. Companies must invest in research and development to create products that address emerging challenges in radiation safety while maintaining compliance with evolving regulatory standards. Building strong relationships with end-users across different sectors, particularly in healthcare and nuclear power, is crucial for understanding changing market needs and developing targeted solutions. Additionally, established players need to optimize their manufacturing and distribution networks to improve cost efficiency and market responsiveness.

New entrants and smaller players can gain market share by focusing on specialized market segments or geographical regions where larger players have limited presence. Developing innovative technologies that offer superior performance or cost advantages compared to existing solutions can help in establishing market presence. Companies need to consider the high concentration of end-users in specific sectors like healthcare and nuclear power, while being mindful of potential regulatory changes that could impact market dynamics. The threat of substitution remains relatively low due to the specialized nature of radiation detection equipment, but companies must stay ahead of technological advancements to maintain their competitive edge. Building strategic partnerships with established players or local distributors can help in overcoming market entry barriers and accessing new customer segments.

Radiation Detection, Monitoring, And Safety Market Leaders

-

Arktis Radiation Detectors Ltd.

-

Amray Group Limited

-

Burlington Medical Llc

-

Centronic Ltd

-

Teledyne FLIR Systems INC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Radiation Detection, Monitoring, And Safety Market News

- January 2024: The US military made the decision to upgrade its radiation detection equipment by adopting the new "Radiological Detection System" produced by D-Tect Systems, a division of Ludlum based in Utah. This system is modular, allowing for customization with various external probes to meet specific detection needs, such as alpha or neutron detection. The outdated AN/PDR-77 and AN/VDR-2 radiation detectors, which had been in use for 35 years, were replaced with this new technology.

- October 2023: Honeywell launched an infrared-based FS24X Plus Flame Detector to detect and stop hydrogen flames from growing into major fires. It protects workers and facilities from risks associated with hydrogen production and use. Honeywell's FS24X Plus can detect rainy, foggy, or smoky flames. To be specific, infrared radiation is electromagnetic radiation with wavelengths extended beyond visible light and shorter than radio waves, and it is often used to transmit information.

Radiation Detection Monitoring and Safety Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.5 Technology Snapshot

-

4.6 Market Drivers

- 4.6.1 Increasing Incidence of Cancer and Other Chronic Diseases

- 4.6.2 Growing Use of Drones for Radiation Monitoring

-

4.7 Market Restraints

- 4.7.1 Stringent Government Regulations

- 4.7.2 Lack of Skilled Radiation Professionals

5. MARKET SEGMENTATION

-

5.1 By Product Type

- 5.1.1 Detection and Monitoring

- 5.1.2 Safety

-

5.2 By End-user Industry

- 5.2.1 Medical and Healthcare

- 5.2.2 Industrial

- 5.2.3 Homeland Security and Defense

- 5.2.4 Energy and Power

- 5.2.5 Other End-user Industries

-

5.3 By Geography***

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia

- 5.3.4 Australia and New Zealand

- 5.3.5 Latin America

- 5.3.6 Middle East and Africa

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles*

- 6.1.1 Amray Group Limited

- 6.1.2 Arktis Radiation Detectors Ltd

- 6.1.3 Burlington Medical LLC

- 6.1.4 Centronic Ltd

- 6.1.5 Teledyne FLIR Systems Inc.

- 6.1.6 Landauer Inc. (Fortive Corporation)

- 6.1.7 Mirion Technologies Inc.

- 6.1.8 Radiation Detection Company

- 6.1.9 RAE Systems Inc. (Honeywell International Inc.)

- 6.1.10 Thermo Fisher Scientific Inc.

- 6.1.11 Unfors RaySafe AB

- 6.1.12 ORTEC (Ametek Inc.)

- 6.1.13 Fuji Electric Co. Ltd

- 6.1.14 ATOMTEX SPE

7. INVESTMENT ANALYSIS

8. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Radiation Detection, Monitoring, And Safety Industry Segmentation

The market is defined by the revenue generated from the sale of radiation detection, monitoring, and safety products offered by different market players for a diverse range of end-user industries.

The radiation detection monitoring and safety market is segmented by product type (detection & monitoring, safety), end-user industry (medical & healthcare, industrial, homeland security & defense, energy & power, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Product Type | Detection and Monitoring |

| Safety | |

| By End-user Industry | Medical and Healthcare |

| Industrial | |

| Homeland Security and Defense | |

| Energy and Power | |

| Other End-user Industries | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Radiation Detection Monitoring and Safety Market Research FAQs

How big is the Radiation Detection, Monitoring, And Safety Market?

The Radiation Detection, Monitoring, And Safety Market size is expected to reach USD 3.62 billion in 2025 and grow at a CAGR of 5.20% to reach USD 4.66 billion by 2030.

What is the current Radiation Detection, Monitoring, And Safety Market size?

In 2025, the Radiation Detection, Monitoring, And Safety Market size is expected to reach USD 3.62 billion.

Who are the key players in Radiation Detection, Monitoring, And Safety Market?

Arktis Radiation Detectors Ltd., Amray Group Limited, Burlington Medical Llc, Centronic Ltd and Teledyne FLIR Systems INC are the major companies operating in the Radiation Detection, Monitoring, And Safety Market.

Which is the fastest growing region in Radiation Detection, Monitoring, And Safety Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Radiation Detection, Monitoring, And Safety Market?

In 2025, the North America accounts for the largest market share in Radiation Detection, Monitoring, And Safety Market.

What years does this Radiation Detection, Monitoring, And Safety Market cover, and what was the market size in 2024?

In 2024, the Radiation Detection, Monitoring, And Safety Market size was estimated at USD 3.43 billion. The report covers the Radiation Detection, Monitoring, And Safety Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Radiation Detection, Monitoring, And Safety Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Radiation Detection, Monitoring, And Safety Market Research

Mordor Intelligence provides comprehensive insights into the radiation detection, monitoring, and safety industry. Our expert analysis and consulting services cover the complete spectrum of radiation detection equipment, radiation safety equipment, and radiation monitoring systems. The report offers a detailed analysis of various technologies, including gamma radiation detection, nuclear radiation detection, and radiological detection equipment. Our expertise also extends to radiation protection solutions, radiation measurement instruments, and advanced radiation sensors that form the backbone of modern safety infrastructure.

Stakeholders gain valuable insights through our detailed examination of radiation dosimeter technologies, personal radiation detectors, and radiation portal monitors. The report, available as an easy-to-download PDF, includes comprehensive analysis of radiation contamination monitoring systems, radioactivity monitoring solutions, and radiation alert systems. We provide detailed evaluations of radiation surveillance technologies, nuclear safety equipment, and radiation protection devices. This enables businesses to make informed decisions. Our research methodology ensures thorough coverage of radiation measurement trends and emerging technologies in the RDMS sector, delivering actionable intelligence for industry participants.