| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 0.67 Billion |

| Market Size (2030) | USD 1.29 Billion |

| CAGR (2025 - 2030) | 13.95 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Qatar Managed Services Market Analysis

The Qatar Managed Services Market size is estimated at USD 0.67 billion in 2025, and is expected to reach USD 1.29 billion by 2030, at a CAGR of 13.95% during the forecast period (2025-2030).

Qatar's managed services landscape is undergoing significant transformation driven by the rapid digitalization of businesses and infrastructure development. The country's robust digital infrastructure, evidenced by its impressive 99% internet penetration rate, has created a fertile ground for managed services adoption. This digital foundation is further strengthened by the establishment of multiple state-of-the-art data centers and the implementation of advanced networking technologies. The integration of emerging technologies such as artificial intelligence, cloud managed services, and IoT has become increasingly critical for businesses seeking to maintain competitive advantages in their respective sectors.

The market is characterized by a strong presence of small and medium-sized enterprises (SMEs), which form the backbone of Qatar's private sector. According to recent data, more than 96% of the 25,000 businesses registered in Qatar's private sector are classified as SMEs, representing a significant opportunity for managed service providers (MSPs). These enterprises are increasingly recognizing the value proposition of managed services, which can reduce IT costs by 25-45% while improving operational efficiency by 45-65%. This shift towards managed services is particularly pronounced in areas such as cloud managed services, cybersecurity, and managed infrastructure services.

The landscape of managed services in Qatar has been significantly enhanced by strategic partnerships between local and international technology providers. A notable development is Qatar becoming the 55th Azure Region globally with Microsoft's establishment of a dedicated cloud data center, marking a significant milestone in the country's digital infrastructure development. This has been complemented by the launch of MEEZA's fourth data center, M-VAULT 4, at the Qatar Science and Technology Park, further expanding the country's data center capabilities and managed services ecosystem.

The market is witnessing a notable shift towards specialized and industry-specific managed services solutions, particularly in sectors such as banking, healthcare, and government services. Service providers are increasingly focusing on developing tailored solutions that address specific industry requirements while maintaining compliance with local regulations and standards. This trend is supported by the growing adoption of hybrid cloud solutions and the increasing demand for integrated managed security services, reflecting the evolving needs of Qatar's business environment and its alignment with global technology trends.

Qatar Managed Services Market Trends

Growing Demand for Outsourcing of Non-Core Operations and Lack of In-House Capabilities Among Key End Users in the Country

Qatar's digital transformation journey has created an unprecedented demand for IT outsourcing services of non-core operations, driven by the country's remarkable internet penetration rate of 99.653% according to the World Bank. Organizations across various sectors are increasingly recognizing the benefits of delegating their IT infrastructure management and security operations to specialized managed services providers, allowing them to focus on their core business objectives. This trend is particularly evident in sectors like healthcare, where spending is projected to grow by 2.2% through 2023, creating opportunities for managed operations to handle secure workflow automation, monitor optimal staffing, and centralize dashboards.

The lack of in-house capabilities has become more pronounced as organizations adopt emerging technologies such as IoT, big data analytics, and cloud computing. This is exemplified by the banking sector's aggressive digital transformation initiatives, where institutions like Dukhan Bank have launched comprehensive online services and electronic payment gateways, necessitating robust managed security services to protect sensitive financial data. The increasing complexity of managing hybrid IT environments and the need for specialized expertise in areas such as cybersecurity and cloud infrastructure management has made outsourcing to managed services providers an attractive proposition for organizations looking to optimize their operational efficiency while maintaining high security standards.

Understand The Key Trends Shaping This Market

Download PDF

Growing Availability of Diversified Offerings Supported by Partnerships Between Local MSPs and Large-Scale Organizations

The Qatar managed services landscape has witnessed a significant evolution through strategic partnerships between local MSPs and global technology leaders, creating a comprehensive ecosystem of diversified service offerings. Notable examples include the partnership between Klouder and Ooredoo, enabling enhanced disaster recovery capabilities and managed cloud services for customers. These collaborations have created one-stop-shop solutions that combine local market expertise with world-class technology capabilities, allowing organizations to access a broader range of specialized services while maintaining local support and compliance requirements.

The strategic alliance between Microsoft and Atos, expanded to Qatar in 2023, demonstrates the growing sophistication of managed services offerings in the country. This partnership specifically addresses the accelerated pace of digital transformation and cloud adoption opportunities, supporting large enterprises with comprehensive managed services solutions. Similarly, Zerone Hi-Tech's extended partnership with Microsoft for managed services has enhanced managed cloud services and enabled easier movement of customer workloads to the cloud, with infrastructure hosted locally on dedicated VM hosting for faster deployment. These partnerships have significantly expanded the range of available services, from basic managed infrastructure services to advanced cloud solutions and managed cybersecurity services.

Supportive Government Policies and Development of Local Landscape Due to the Recent Changes in Geopolitical Conditions

Qatar's government has implemented progressive policies to foster the growth of the managed services sector, with the Qatar National Vision 2030 serving as a cornerstone for digital transformation initiatives. The country's strategic focus on developing its digital infrastructure is evidenced by its top ranking in the Digital Accessibility Rights Evolution (DARE) Index, demonstrating its commitment to creating an inclusive and technologically advanced ecosystem. These initiatives have been supported by substantial investments in digital infrastructure, including the development of smart cities and the implementation of advanced technologies across government services.

The transformation of Qatar's local IT landscape has been accelerated by recent geopolitical changes, leading to increased emphasis on developing domestic technological capabilities and partnerships with international technology providers. This is exemplified by significant investments in data center infrastructure, such as MEEZA's launch of its fourth data center building, M-VAULT 4, which hosts the Microsoft Cloud data center region. The government's commitment to digital transformation is further demonstrated through initiatives like the TASMU Smart Qatar Programme, which enhances digital skills, access, motivation, and trust across the population, specifically targeting those at risk of digital exclusion. These supportive policies have created a favorable environment for managed services providers to expand their operations and offer innovative solutions to meet the growing demand for digital services.

Segment Analysis: By Type

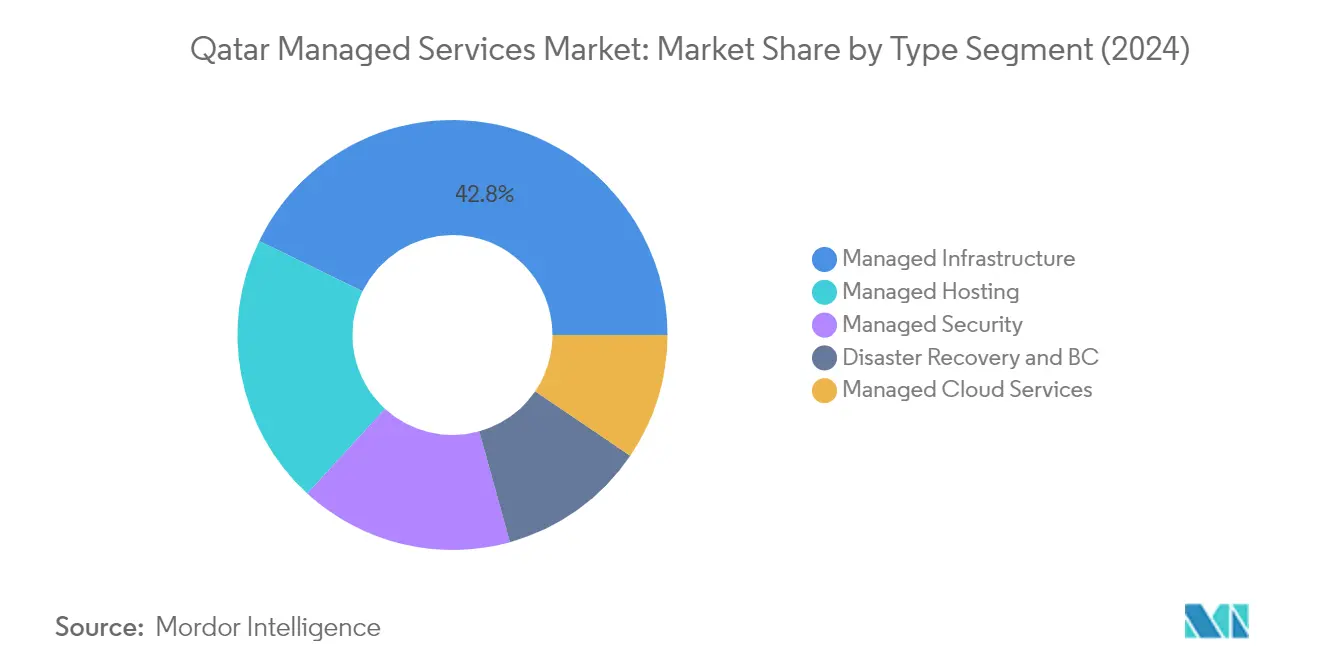

Managed Infrastructure Segment in Qatar Managed Services Market

The Managed Infrastructure segment dominates the Qatar Managed Services Market, commanding approximately 43% market share in 2024. This significant market position is driven by the increasing adoption of managed infrastructure services by organizations looking to optimize their technology foundation and reduce operational complexities. Companies in Qatar are increasingly shifting towards managed infrastructure services to obtain standardized and cost-efficient services, enabling them to focus on their core business while minimizing risk and increasing infrastructure uptime. The segment's prominence is further strengthened by the growing demand from small and medium enterprises that prefer to outsource their IT infrastructure components due to budget constraints and the need to focus on core competencies.

Managed Cloud Services Segment in Qatar Managed Services Market

The Managed Cloud Services segment is experiencing the highest growth trajectory in the Qatar Managed Services market, with an expected growth rate of approximately 15% during the forecast period 2024-2029. This accelerated growth is primarily driven by the increasing cloud adoption across multiple industries and organizations' inability to manage all crucial cloud-related tasks in-house. The segment's growth is further fueled by the rising adoption of hybrid cloud solutions, particularly among small and medium enterprises (SMEs) in Qatar. The expansion of major cloud service providers and their partnerships with local managed service providers is creating a robust ecosystem for managed cloud services delivery, supporting this segment's rapid growth.

Remaining Segments in Qatar Managed Services Market

The Qatar Managed Services market encompasses several other significant segments including Managed Hosting, Managed Security, and Disaster Recovery & Business Continuity Services. The Managed Hosting segment plays a crucial role in providing application and data center management services, particularly beneficial for organizations looking to outsource their hosting requirements. The Managed Security segment has gained increasing importance with the rising cybersecurity concerns and regulatory compliance requirements. Meanwhile, the Disaster Recovery & Business Continuity Services segment continues to be vital for organizations seeking to ensure business resilience and data protection in an increasingly digital business environment.

Segment Analysis: By End-User Vertical

Government Segment in Qatar Managed Services Market

The Government sector dominates the Qatar Managed Services Market, commanding approximately 36% market share in 2024. This significant market position is driven by the government's increasing focus on digital transformation initiatives and smart city projects. The sector's dominance is reinforced by Qatar's Vision 2030 and the TASMU Smart Qatar Programme, which emphasize the digitization of government services and operations. Government agencies are increasingly partnering with managed service providers to handle routine IT maintenance and management tasks, enabling them to focus on core government matters while ensuring data centers, network infrastructure, telecommunications, and cloud resources operate securely and reliably.

IT & Telecom Segment in Qatar Managed Services Market

The IT & Telecom sector is emerging as the fastest-growing segment in the Qatar Managed Services Market, with a projected growth rate of approximately 15% during 2024-2029. This remarkable growth is primarily driven by the rapid adoption of 5G technology, increasing implementation of BYOD policies, and the growing need for high-end security solutions to manage expanding data volumes. The sector's growth is further accelerated by telecom operators' continuous pressure to deliver innovative services at competitive costs while maintaining customer retention in an increasingly competitive market environment.

Remaining Segments in Qatar Managed Services Market

The other significant segments in the Qatar Managed Services Market include BFSI, Oil & Gas, Healthcare, and various other end-user verticals. The BFSI sector maintains a strong presence due to its increasing focus on digital transformation and cybersecurity requirements. The Oil & Gas sector continues to be a crucial component of the market, driven by the need for advanced IT infrastructure and security solutions. The Healthcare sector is showing promising growth potential with the increasing adoption of digital health solutions and telemedicine platforms. Other end-user verticals, including retail, education, and logistics, collectively contribute to the market's diversity and overall growth momentum.

Qatar Managed Services Market Geography Segment Analysis

Managed Services Market in North America

The North American managed services market continues to demonstrate robust growth, driven by the increasing adoption of cloud technologies and digital transformation initiatives across industries. The region's market is characterized by a strong presence of managed service providers offering comprehensive solutions ranging from managed security services to cloud migration services. Organizations, particularly small and medium enterprises (SMEs), are increasingly relying on managed services to ensure the optimal usage of technology while transforming and scaling their businesses. The market is witnessing a significant shift toward bundled services, as companies prefer integrated solutions over discrete offerings. The healthcare sector has emerged as a key growth driver, with organizations embracing managed services to handle electronic health records and new reimbursement models. Additionally, telecom service providers in the region are expanding beyond traditional voice and data services to offer sophisticated managed service solutions, particularly in areas such as remote workforce management and cloud security.

Managed Services Market in Europe

The European managed services landscape has evolved significantly, with organizations across the region increasingly relying on managed service providers to maintain a competitive advantage and ensure operational efficiency. The market is characterized by robust growth in managed security services, particularly in response to Europe's stringent data protection regulations. The region has witnessed substantial development in cloud-based solutions and digital transformation initiatives, with managed service providers playing a crucial role in helping organizations navigate complex technological challenges. The United Kingdom, Germany, and France continue to be the primary growth drivers, with significant adoption across banking, manufacturing, and automotive sectors. The emergence of autonomous driving and connected vehicles in the automotive industry has created new opportunities for managed service providers, particularly in handling large data volumes and real-time decision-making systems. The market is also seeing increased demand for factory-based approaches in quality assurance, data migration, and training processes.

Managed Services Market in Asia Pacific

The Asia Pacific managed services market demonstrates strong growth potential, driven by increasing digital transformation initiatives and the rapid evolution of IT infrastructure across the region. China's managed services market is experiencing significant expansion, particularly in telecommunications and managed cloud services sectors, with service providers focusing on reducing security risks and optimizing operations for end users. The Indian market is witnessing substantial growth in the banking sector, with extensive adoption of managed cloud services and managed storage services. Japan's market is characterized by the growing adoption of managed multi-cloud environments as strategic platforms for driving innovation and competitive edge. The region is experiencing a notable shift toward cloud-based infrastructure, with organizations increasingly seeking managed services to handle complex IT environments and ensure cybersecurity compliance. Small and medium enterprises in the region are particularly active in adopting managed services to overcome budget constraints and maintain compliance with data protection laws.

Managed Services Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, presents unique opportunities in the managed services market, driven by the growing digital transformation initiatives and increasing adoption of cloud technologies. Latin America is witnessing a booming start-up ecosystem that is driving the need for well-managed service providers to help scale businesses through outsourcing day-to-day operations. The region is experiencing significant growth in cloud-managed and subscription-based services, particularly benefiting small and medium-sized businesses by providing access to sophisticated ICT capabilities. The Middle East market is characterized by increasing investments in cybersecurity and digital infrastructure, with a focus on supporting various sectors including oil and gas, banking, and government services. The African market is gradually evolving, with organizations increasingly recognizing the value of managed services in optimizing their IT operations and ensuring business continuity while managing costs effectively. The demand for managed hosting services and managed data services is also on the rise, reflecting the growing need for efficient and secure IT solutions.

Get Analysis on Important Geographic Markets

Download PDF

Qatar Managed Services Industry Overview

Top Companies in Qatar Managed Services Market

The Qatar managed services market features prominent players like MEEZA QSTP, GBM Qatar, Diyar United Company, Ooredoo QPSC, and Mannai Corporation leading the competitive landscape. These companies are driving innovation through expanded cloud capabilities, AI-powered solutions, and advanced cybersecurity offerings while maintaining operational excellence through standardized service delivery frameworks. Strategic partnerships with global technology leaders like Microsoft, IBM, Cisco, and VMware have enabled local providers to enhance their service portfolios and technical capabilities. Companies are increasingly focusing on developing specialized industry solutions for key sectors like government, BFSI, and oil & gas while expanding their geographic presence across the Middle East region. The market is characterized by continuous investment in next-generation technologies, talent development programs, and customer experience enhancement initiatives to maintain competitive advantage.

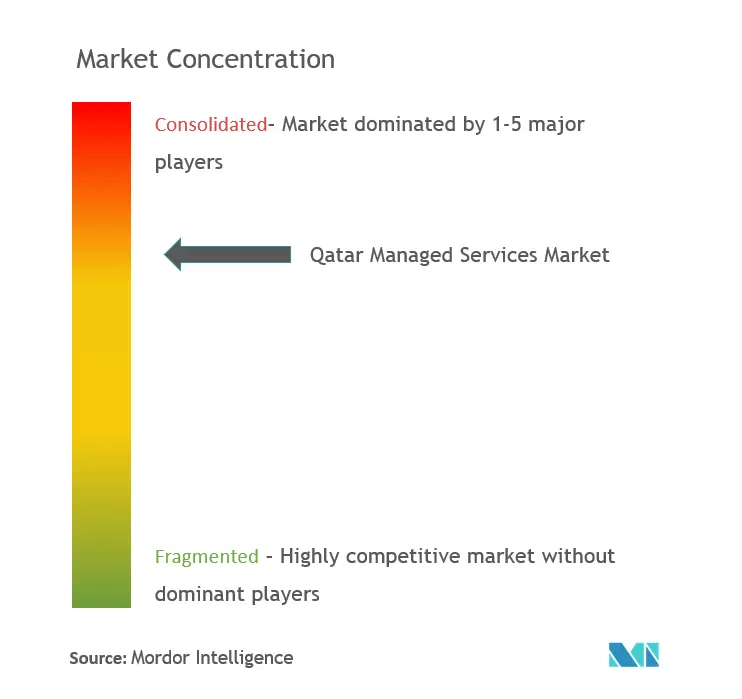

Market Dominated by Regional Technology Conglomerates

The competitive landscape is primarily dominated by well-established regional technology conglomerates that have built a strong local presence and relationships over decades of operation in Qatar. These players leverage their deep understanding of the local business environment, extensive partner ecosystems, and comprehensive service portfolios spanning IT infrastructure, applications, and security domains. The market structure reflects a moderate level of consolidation, with the top players accounting for a significant share while leaving room for specialized providers in niche segments like managed security services and cloud services.

The market has witnessed increased merger and acquisition activity as companies seek to expand their technical capabilities and market reach. Global IT services companies are entering the Qatar market through acquisitions and strategic partnerships with local players to establish a presence in this growing market. This trend is driving consolidation while also bringing global best practices and innovative service delivery models to the market. Local players are responding by strengthening their domain expertise, investing in emerging technologies, and expanding their managed services portfolios to maintain their competitive positions.

Innovation and Specialization Drive Future Success

Success in the Qatar managed services market increasingly depends on providers' ability to deliver innovative, industry-specific solutions while maintaining service excellence and cost competitiveness. Incumbent players need to continue investing in emerging technologies like AI, IoT, and cloud while developing deep vertical expertise in key sectors like government, financial services, and oil & gas. Building strong cybersecurity capabilities, achieving relevant certifications, and maintaining compliance with evolving regulations are critical for maintaining market leadership. Companies must also focus on talent development and retention while optimizing their delivery models to improve operational efficiency.

For new entrants and challenger firms, the path to success lies in identifying and focusing on underserved market segments or specialized service areas where they can build distinctive capabilities. Developing strong partnerships with global technology providers while maintaining local market understanding and relationships is essential. Companies need to carefully evaluate customer concentration risks and build diversified client portfolios across industries. The ability to demonstrate a clear value proposition, maintain service quality, and build long-term client relationships while managing competitive pressures on pricing will be crucial for gaining market share. Regulatory compliance and data sovereignty requirements will continue to influence service delivery models and market entry strategies.

Qatar Managed Services Market Leaders

-

MEEZA QSTP LLC

-

Gulf Business Machines Qatar W.L.L.

-

Diyar Group

-

Paramount Computer Systems FZ-LLC

-

Ooredoo Q.P.S.C

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Qatar Managed Services Market News

- January 2022 - Microsoft and Vodafone Qatar announced that they are expanding their current collaboration to offer more digital solutions to businesses across the country. Vodafone's IoT product and service offerings will incorporate Microsoft Azure to help the firms unify their respective technology portfolios. Vodafone's IoT solutions hosted on Microsoft Azure are projected to offer highly secure, dependable, and tailored features and benefits to Qatar's commercial clients, including public and private organisations and governmental entities.

- June 2022 - In order to offer cloud network managed services in Qatar, Starlink W.L.L. and Huawei, a major international supplier of ICT infrastructure and smart devices, inked a memorandum of understanding (MoU). For Qatar's expanding enterprise customer needs, Starlink W.L.L. will provide fully managed networks, including Wi-Fi, LAN, and WAN Network solutions, which enable scalability and flexibility on demand.

Qatar Managed Services Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Growing Demand for Outsourcing of Non-core Operations and Lack of In-house Capabilities Among Key End Users in the Country

- 4.2.2 Growing Availability of Diversified Offerings Supported by Partnerships Between Local MSPs And Large-Scale Organizations

- 4.2.3 Supportive Government Policies and Development of Local Landscape due to the Recent Changes in Geopolitical Conditions

-

4.3 Market Challenges

- 4.3.1 Operational and Regulatory Concerns

-

4.4 Market Opportunities

- 4.4.1 Increased Awareness on the Security Threats Faced by Local Enterprises

-

4.5 Relative Positioning of Key Stakeholders in the Qatari Managed Services Industry

- 4.5.1 System Integrators

- 4.5.2 ISP's

- 4.5.3 Telecom Providers

- 4.5.4 Hosting and Storage Providers

- 4.6 Base Indicator Analysis of the ICT Sector in Qatar (ICT Industry Spending, Digitization, Internet Penetration, etc.)

- 4.7 Impact of COVID-19 on the Managed Services Industry

5. QATAR IT SERVICES MARKET OUTLOOK

- 5.1 IT Services Industry Estimates and Forecasts

- 5.2 Evolution of IT Services Industry and Coverage on the Key Factors Driving Adoption

- 5.3 Analysis of the Key IT Services Vendors - Qatar Computer Services, Octaware, Vistas Global WLL

- 5.4 Market Outlook

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Managed Infrastructure (Network and Desktop)

- 6.1.2 Managed Hosting (Application and Data Center)

- 6.1.3 Managed Security

- 6.1.3.1 Asset Management and Monitoring

- 6.1.3.2 Threat Intelligence and Management

- 6.1.3.3 Risk and Compliance

- 6.1.3.4 Other Managed Securities

- 6.1.4 Managed Cloud Services (Cloud-based Services Outsourced to MSPs)

- 6.1.5 Disaster Recovery and Business Continuity Services

-

6.2 By End-user Vertical

- 6.2.1 Government

- 6.2.2 BFSI

- 6.2.3 Oil and Gas

- 6.2.4 IT and Telecom

- 6.2.5 Healthcare

- 6.2.6 Other End-user Verticals (Retail, Education, Logistics, etc.)

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 MEEZA QSTP LLC

- 7.1.2 Gulf Business Machines Qatar WLL

- 7.1.3 Diyar Group

- 7.1.4 Ooredoo Q.P.S.C

- 7.1.5 Mannai Coproration

- 7.1.6 Paramount Computer Systems FZ-LLC

- 7.1.7 Paladion Qatar WLL

- 7.1.8 Advanced Business Computing (ABC) Group

- 7.1.9 Navlink Inc.

- *List Not Exhaustive

8. FUTURE OUTLOOK OF THE MARKET

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Qatar Managed Services Industry Segmentation

Managed services are outsourcing on a proactive basis certain processes and functions intended to improve operations and cut expenses. They simplify IT operations, increase user satisfaction, and improve service quality while reducing operating costs. Managed services options range from short-term post-go-live assistance to long-term application operations.

The Qatar Managed Services Market is segmented by Type (Managed Infrastructure, Managed Hosting, Managed Security (Asset Management and Monitoring, Threat Intelligence and Management, Risk and Compliance, Other Managed Securities), Managed Cloud Services (Cloud-based services outsourced to MSPs), Disaster Recovery and Business Continuity Services) and End-user Vertical (Government, BFSI, Oil and Gas, IT and Telecom, Healthcare, Other End-user Verticals (Retail, Education, Logistics, etc.)

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Type | Managed Infrastructure (Network and Desktop) | ||

| Managed Hosting (Application and Data Center) | |||

| Managed Security | Asset Management and Monitoring | ||

| Threat Intelligence and Management | |||

| Risk and Compliance | |||

| Other Managed Securities | |||

| Managed Cloud Services (Cloud-based Services Outsourced to MSPs) | |||

| Disaster Recovery and Business Continuity Services | |||

| By End-user Vertical | Government | ||

| BFSI | |||

| Oil and Gas | |||

| IT and Telecom | |||

| Healthcare | |||

| Other End-user Verticals (Retail, Education, Logistics, etc.) | |||

Need A Different Region or Segment?

Customize Now

Qatar Managed Services Market Research FAQs

How big is the Qatar Managed Services Market?

The Qatar Managed Services Market size is expected to reach USD 0.67 billion in 2025 and grow at a CAGR of 13.95% to reach USD 1.29 billion by 2030.

What is the current Qatar Managed Services Market size?

In 2025, the Qatar Managed Services Market size is expected to reach USD 0.67 billion.

Who are the key players in Qatar Managed Services Market?

MEEZA QSTP LLC, Gulf Business Machines Qatar W.L.L., Diyar Group, Paramount Computer Systems FZ-LLC and Ooredoo Q.P.S.C are the major companies operating in the Qatar Managed Services Market.

What years does this Qatar Managed Services Market cover, and what was the market size in 2024?

In 2024, the Qatar Managed Services Market size was estimated at USD 0.58 billion. The report covers the Qatar Managed Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Qatar Managed Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Qatar Managed Services Market Research

Mordor Intelligence provides a comprehensive analysis of the managed services landscape in Qatar. We leverage our extensive expertise in IT managed services research. Our detailed report covers a full spectrum of services, including cloud managed services, managed security services, and managed print services. The analysis encompasses crucial areas such as managed operations, managed cybersecurity services, and managed network services. This provides stakeholders with detailed insights into the evolving MSP ecosystem. Our research methodology incorporates extensive analysis of managed hosting services and managed data services. This information is available in an easy-to-download report PDF format.

The report offers invaluable insights for stakeholders involved in managed mobility services, managed backup services, and managed infrastructure services. Organizations seeking to understand managed application services and technology management services will find comprehensive coverage of managed connectivity solutions and managed storage services. The analysis extends to emerging areas, including managed IoT services, managed workplace services, and managed telecommunications. It also covers managed business services and managed communication services. Our report particularly benefits organizations exploring IT outsourcing services opportunities in Qatar's dynamic technology landscape.