Qatar Foodservice Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2 Billion |

| Market Size (2030) | USD 3.09 Billion |

| Growth Rate (2025 - 2030) | 9.11% CAGR |

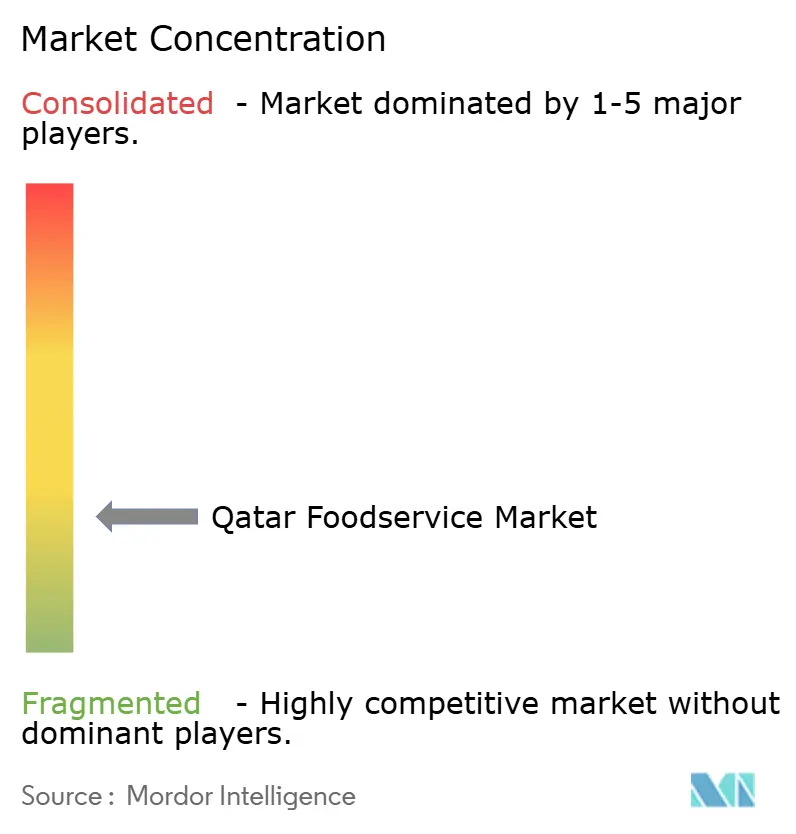

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Qatar Foodservice Market Analysis by Mordor Intelligence

The Qatar foodservice market size is valued at USD 2.00 billion in 2025 and is predicted to reach USD 3.09 billion by 2030, advancing at a 9.11% CAGR, underscoring vigorous short- and medium-term expansion. Rising inbound tourism, a young and overwhelmingly expatriate population, and compulsory electronic payments are collectively raising transactional volumes and average checks across the Qatar foodservice market. Cloud kitchens, digital ordering, and autonomous delivery pilots are remapping operating models, while premium full-service restaurants leverage the Michelin Guide Doha and “Taste of Qatar” ratings to capture upscale demand. Strategic food security facilities at Hamad Port and a freight master plan mitigate import-centric supply chain risk, bolstering continuity of menu offerings and price stability. A fragmented operator base and streamlined licensing for cloud kitchens leave white-space for new entrants to scale swiftly across the Qatar foodservice market.

Key Report Takeaways

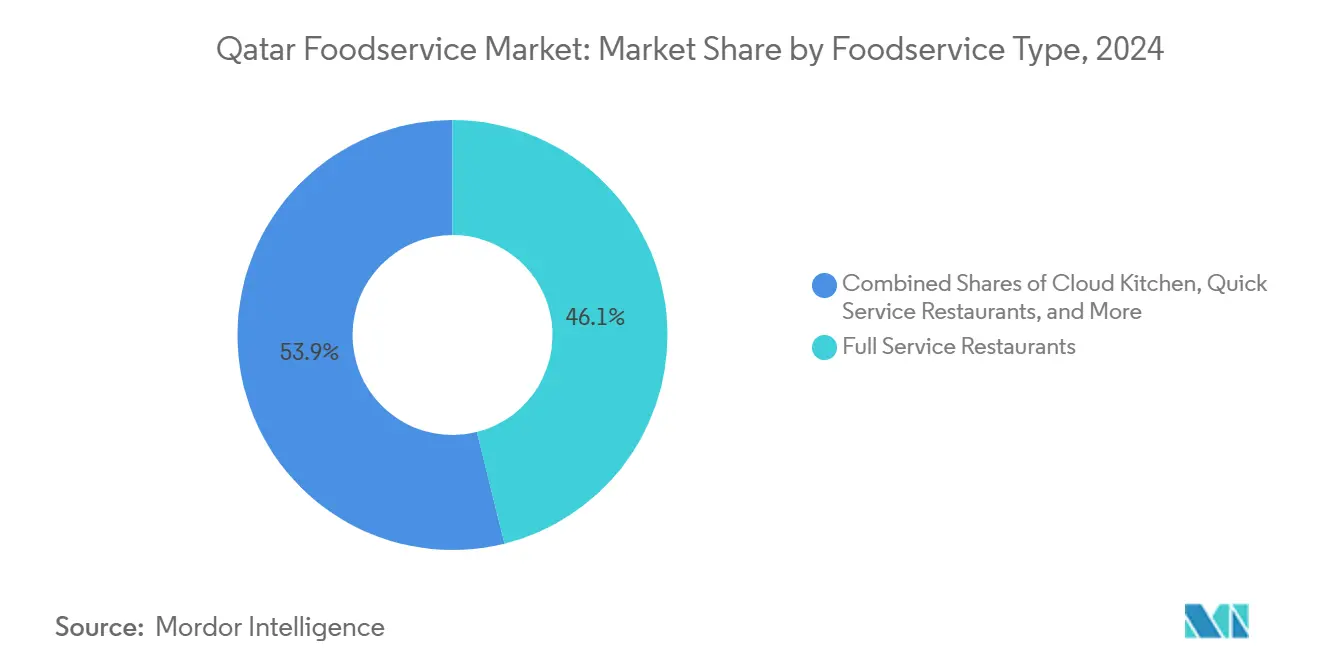

- By foodservice type, Full Service Restaurants led with 46.12% of the Qatar foodservice market share in 2024, while Cloud Kitchens are projected to expand at an 18.01% CAGR between 2025-2030.

- By outlet, independent operators accounted for 70.11% of the Qatar foodservice market size in 2024; chained outlets are forecast to grow at a 9.12% CAGR to 2030.

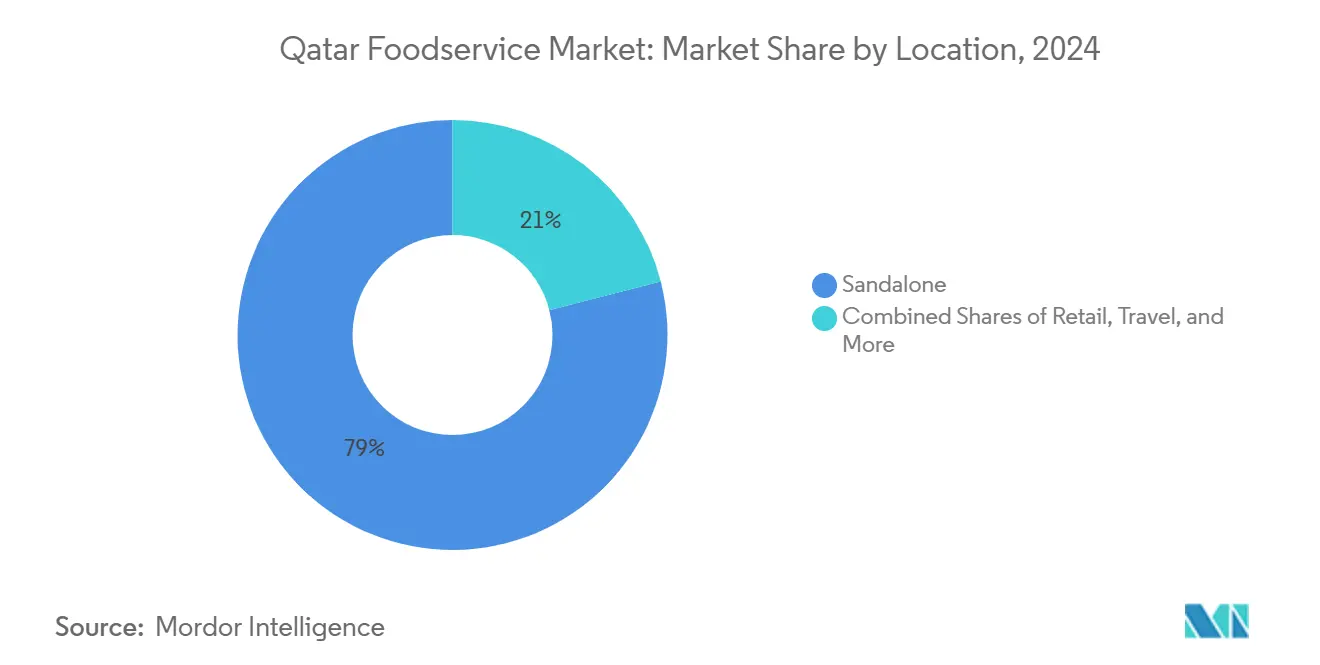

- By location, standalone venues captured 79.00% share in 2024, and travel-linked sites will post the fastest 11.02% CAGR through 2030.

- By service type, dine-in retained a 65.40% share of the Qatar foodservice market size in 2024, while the delivery channel is set to accelerate at a 12.30% CAGR to 2030.

Qatar Foodservice Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding tourism sector, increasing international and regional visitors | +2.1% | National, with concentration in Doha, West Bay, and Hamad International Airport | Medium term (2-4 years) |

| Widespread adoption of food delivery apps and online ordering platforms | +1.8% | National, with highest penetration in urban centers | Short term (≤ 2 years) |

| Rising disposable incomes & large expatriate base | +1.6% | National, with premium segments in Doha and Al Rayyan | Long term (≥ 4 years) |

| Growing trend for international cuisines and QSR | +1.3% | National, with franchise concentration in major districts | Medium term (2-4 years) |

| Integration of digital technologies, contactless payment and self-service kiosks | +1.0% | National, with early adoption in malls and airports | Short term (≤ 2 years) |

| Large, young demographic favoring frequent dining out and fast service | +0.9% | National, with highest impact in educational and business districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Sector Expansion Drives Premium Dining Demand

In 2024, Qatar recorded 5.08 million visitor arrivals, with plans to achieve 6 million by 2030, aligning with its National Vision 2030, as reported by Qatar News Agency[1]Qatar News Agency, "Ministry of Transport Finalizes Qatar Freight Master Plan", www.qna.org.qa. Leveraging the momentum from post-World Cup tourism, Qatar's foodservice sector is experiencing significant growth in demand. In February 2025, Qatar Tourism launched the "Taste of Qatar" initiative in partnership with Ipsos, introducing restaurant ratings across seven distinct dining categories. This initiative highlights the strategic focus on positioning culinary experiences as a core element of Qatar's tourism appeal. Additionally, the Michelin Guide Doha 2025 further reinforces this strategy by establishing high-quality benchmarks, enhancing Qatar's global reputation as a dining destination. The synergy between tourism and foodservice is driving substantial growth, with travel-related establishments, such as those in airports, hotels, and leisure destinations, achieving a robust 11.02% CAGR as they expand their capacities. Qatar's compact geography and its technologically adept population create an ideal environment for testing and adopting innovative foodservice technologies. This is exemplified by Talabat's autonomous delivery trials conducted in collaboration with Qatar Foundation, showcasing the country's commitment to integrating advanced solutions into its foodservice landscape.

Digital Platform Proliferation Reshapes Service Delivery

In Qatar, food delivery apps have reshaped dining habits. Talabat, a key player, grew from a modest team of 6 in 2017 to a robust workforce of over 160 in 2024, solidifying its market leadership, as reported by Invest Qatar[2]Invest Qatar, “Investor spotlight: talabat Qatar,” invest.qa. In 2024, the Ministry of Commerce and Industry rolled out new licensing guidelines for cloud kitchens, expediting the approval process for delivery-centric operators. Sub-kitchen licenses now see approvals in just 1-2 days, cutting through previous bureaucratic delays. These updated regulations pave the way for four innovative cloud kitchen models: independent segmented units, cohesive multi-brand setups, kitchen-as-a-service platforms, and hubs run by aggregators. E-commerce transactions in Qatar hit 7.90 million in September 2024, marking a 43% surge from the previous year, underscoring the nation's growing digital embrace in the foodservice realm. Furthermore, digital platforms are not just focusing on profits; they're championing sustainability. Initiatives like minimizing disposable cutlery and testing electric vehicle fleets highlight their commitment to environmental stewardship, all while appealing to budget-conscious consumers.

Expatriate Demographics Fuel Premium Consumption

Qatar's expatriate population, which constitutes over 85% of the total residents, drives a distinct demand for international cuisines and premium dining experiences, as highlighted by the IMF[3] IMF Staff, “Artificial Intelligence in Qatar – Assessing the Potential Economic Impacts,” imf.org. By Q4 2024, the employed population reached 2.28 million, with unemployment at just 0.10%, reflecting strong purchasing power across various demographic groups. This affluent expatriate community favors a diverse range of culinary options, including Asian and European fine dining, niche coffee shops, and dessert bars. In Q4 2024, the Ministry of Labour processed 30,156 new recruitment applications, indicating workforce growth and a corresponding rise in foodservice demand. With a non-Qatari to Qatari national ratio of 7.95:1, expatriates dominate private sector employment and exhibit higher dining-out frequencies along with a preference for international cuisines. This demographic composition sustains demand for authentic ethnic restaurants, premium casual dining, and convenience-focused service formats catering to busy professionals.

International Cuisine Expansion Accelerates Market Premiumization

Qatar's diverse demographic and increasing disposable incomes fuel a growing appetite for international cuisines. Full Service Restaurants, holding a 46.12% market share, are diversifying their menu offerings. Meanwhile, the Qatar Investment Authority's potential stake in McDonald's China operations underscores a sovereign capital's keen interest in global Quick Service Restaurant (QSR) assets, highlighting the foodservice sector's growth potential. In another move, Msheireb Properties has teamed up with TGP International to craft a premier food hall at Msheireb Galleria. This initiative not only underscores an institutional commitment to community-centric culinary hubs but also dovetails with Qatar's urban innovation agenda, melding cultural heritage with contemporary dining. The rise of specialized segments—ranging from juice bars and dessert spots to ethnic fine dining—underscores a discerning consumer base willing to pay a premium for genuine culinary experiences.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent compliance with food safety and environmental regulations | -1.2% | National, with enhanced enforcement in high-traffic areas | Medium term (2-4 years) |

| Supply chain disruptions due to dependence on imported food products | -0.9% | National, with critical impact on specialty and fresh ingredients | Short term (≤ 2 years) |

| High rents & outlet saturation in prime districts | -0.7% | Concentrated in Doha, West Bay, and major mall locations | Long term (≥ 4 years) |

| Skill shortages and workforce gaps in hospitality and foodservice sectors | -0.6% | National, with acute impact on specialized culinary roles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance Framework Intensifies Operational Complexity

Qatar's Ministry of Public Health manages the Watheq system, which has registered nearly 9,000 food establishments to ensure adherence to robust monitoring protocols. This system enforces Law No. 8 of 1990, which regulates human food control. It requires compliance with ISO 17020 international accreditation standards and works in coordination with agencies such as the Ministry of Commerce and Industry, the Ministry of Municipality, and customs authorities. Cloud kitchen operators face additional regulatory requirements, including approvals from the Urban Planning Department, fire safety certifications from Civil Defence, and food handling permits from the Ministry of Public Health. Regulations mandate that cloud kitchens maintain separate networks for water, electricity, and sewage, along with designated entrances for delivery personnel and industrial-grade ventilation systems. These requirements increase capital investments and operational complexity. To ensure compliance, authorities conduct periodic inspections and may impose penalties, including temporary suspensions, permanent license revocations, and monetary fines. These enforcement measures expose operators across all market segments to compliance risks.

Import Dependency Exposes Supply Chain Vulnerabilities

Qatar depends on imports for over 90% of its food products, making the nation vulnerable to structural supply chain risks. To address this, Qatar's National Food Security Strategy 2030 focuses on diversification. The strategy limits imports from any single country to 50-55% for commodities currently sourced from suppliers holding over 70% market share. It also requires at least three commercial partnerships for each product category. The Strategic Food Security Facilities at Hamad Port, with a storage capacity exceeding 500,000 square meters, are designed to maintain reserves for 11 essential commodities, including sugar, wheat, rice, and edible oil, ensuring 2-8 months of consumption. Finalized in February 2024, the Qatar Freight Master Plan aims to strengthen supply chain resilience by integrating ground freight systems. Qatar seeks to rank among the top 15 countries in the World Bank's Logistics Performance Index, as noted by the Ministry of Transport. While these infrastructure developments reduce supply disruption risks, they necessitate significant capital investment and close coordination between government agencies and private sector partners.

Segment Analysis

By Foodservice Type: Cloud Kitchens Disrupt Traditional Models

While Full Service Restaurants maintain a dominant 46.12% market share in 2024, Cloud Kitchens are experiencing rapid growth with a projected 18.01% CAGR through 2030. The Ministry of Commerce and Industry has simplified the licensing process, enabling four distinct cloud kitchen models: segmented independent units, unified multi-brand operations, kitchen-as-a-service platforms, and aggregator-operated hubs. Full Service Restaurants are benefiting from Qatar Tourism's "Taste of Qatar" initiative. This program, in partnership with Ipsos, evaluates fine dining, upscale casual, and casual dining categories, providing opportunities for quality differentiation. Quick Service Restaurants are leveraging Qatar's mandatory electronic payment system. With POS transaction volumes reaching 37.26 million in September 2024, they are optimizing order processing and enhancing customer throughput.

Café and Bars are catering to the preferences of Qatar's expatriate population. Specialist coffee and tea shops, in particular, are gaining popularity among professionals in Doha's vibrant business districts. Regulations require cloud kitchens to maintain separate areas for preparation, cooking, storage, and packaging. Additionally, they are prohibited from operating within residential units, ensuring compliance with the standards of traditional foodservice establishments. Talabat's expansion from just 6 to over 160 employees highlights the scalability of delivery-focused business models. Simultaneously, autonomous vehicle trials with Qatar Foundation signal a shift toward technology-driven service advancements.

Note: Segment shares of all individual segments available upon report purchase

By Outlet: Independent Operations Dominate Despite Chain Expansion

Independent outlets command 70.11% market share in 2024, reflecting Qatar's entrepreneurial foodservice ecosystem, while chained outlets accelerate at 9.12% CAGR as international franchises establish regional presence. Qatar Investment Authority's potential investment in McDonald's China operations signals sovereign recognition of QSR franchise value creation potential. Independent operators benefit from agility in menu customization, local market responsiveness, and cultural authenticity, particularly important given Qatar's diverse expatriate population exceeding 85% of residents.

Chained outlets leverage standardized operations, brand recognition, and economies of scale in procurement and marketing, enabling rapid expansion across Qatar's compact geography. The Ministry of Labor's processing of 30,156 new recruitment applications in Q4 2024 indicates continued workforce availability for expansion initiatives. Independent outlets face increasing pressure from rising rental costs in prime districts, with small retail spaces commanding QR 300-400 per square meter monthly, while restaurants in outdoor mall areas pay QR 130-180 per square meter. The Msheireb Properties food hall development represents hybrid models that combine independent operator creativity with institutional infrastructure support

By Locations: Travel Segments Capitalize on Infrastructure Investment

In 2024, standalone locations hold a commanding 79.00% market share. However, travel-linked establishments exhibit the highest growth potential, with a projected CAGR of 11.02%. This growth is driven by Qatar's expanding tourism sector and ongoing infrastructure developments. Hamad International Airport's capacity expansion and the Qatar National Vision 2030, which targets 6 million annual visitors, are fueling sustained demand for travel-related food services. Meanwhile, retail spaces in malls face approximately 20% vacancy rates, offering foodservice operators opportunities to secure prime locations at competitive rental terms. Lodging-related restaurants are benefiting from the growth of Qatar's hospitality sector. With fewer than 100 Qatari nationals employed across the sector, there is significant growth potential for international hospitality chains.

The Qatar Freight Master Plan enhances supply chain efficiency through the integration of intermodal transportation systems, particularly benefiting travel and retail segments that depend on consistent inventory management. Leisure locations are leveraging Qatar's post-World Cup tourism momentum, with visitor arrivals reaching 5.08 million in 2024. Standalone operations, meanwhile, maintain the flexibility to innovate their concepts and adapt operations. The Strategic Food Security Facilities at Hamad Port, with over 500,000 square meters of storage capacity, strengthen supply chain resilience across all location types.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Delivery Growth Challenges Traditional Models

In 2024, dine-in services hold a 65.40% market share, highlighting Qatar's strong social dining culture and the preferences of its expatriate population. At the same time, delivery services are experiencing significant growth, with a 12.30% CAGR driven by the expansion of digital platforms and evolving consumer behaviors. Talabat, a leading player in this space, has expanded its workforce from 6 to over 160 employees, showcasing the scalability of delivery-focused business models, as noted by Invest Qatar. In September 2024, POS transactions reached QR 8.05 billion, reflecting the seamless integration of dine-in and delivery channels supported by mandatory electronic payment infrastructure. Takeaway services occupy a middle ground, leveraging consumer demand for convenience while avoiding the complexities of delivery logistics.

Revised cloud kitchen licensing guidelines introduce four distinct models, enabling delivery-optimized operations and reducing capital requirements compared to traditional dine-in establishments. Talabat's partnership with Qatar Foundation to deploy autonomous delivery vehicles demonstrates a technology-driven evolution in services, which could further boost the delivery segment's growth. In September 2024, e-commerce transactions climbed to 7.90 million, a 43% year-over-year increase, underscoring the continued digital adoption across foodservice channels. Dine-in operators are adapting by implementing digital ordering systems, contactless payment options, and enhanced hygiene protocols. Meanwhile, delivery services are advancing sustainability efforts by piloting electric vehicle fleets and reducing the use of disposable cutlery.

Geography Analysis

Qatar's foodservice market leverages its strategic location as a GCC hub and its compact size to enhance supply chain efficiency and service delivery. Covering 11,586 square kilometers, Qatar facilitates rapid market penetration and consistent service standards across the country. The Doha metropolitan area, which hosts the majority of foodservice establishments, drives most consumer demand. The country's post-World Cup infrastructure developments, including improved transportation and hospitality facilities, have created sustained growth momentum, with visitor numbers reaching 5.08 million in 2024 and targeting 6 million by 2030, aligning with the Qatar National Vision 2030. The Strategic Food Security Facilities at Hamad Port, with over 500,000 square meters of storage capacity, establish Qatar as a regional food distribution hub while strengthening domestic supply chain resilience. Additionally, GCC labor mobility and trade agreements support regional integration by enabling workforce flexibility and optimizing ingredient sourcing across Gulf markets.

The National Food Security Strategy 2030 mandates limiting single-country imports for commodities to 50-55%, requiring at least three commercial partnerships per product category. This diversification strategy reduces supply chain risks while allowing foodservice operators to source premium ingredients from various regions, enhancing menu authenticity. Qatar's compact geography supports efficient last-mile delivery systems, as demonstrated by Talabat's autonomous vehicle trials, which highlight advancements in logistics technology. The Qatar Freight Master Plan's integration of intermodal transportation systems improves supply chain efficiency, placing Qatar among the top 15 countries in the World Bank's Logistics Performance Index. Urban centers like Doha, Al Rayyan, and Al Wakrah benefit from economies of scale in foodservice operations, while emerging districts are poised to grow with planned infrastructure and population increases.

Cross-border investment trends highlight regional integration opportunities, such as the Qatar Investment Authority's potential investment in McDonald's China, reflecting sovereign interest in global foodservice assets. With expatriates comprising over 85% of Qatar's population, there is significant demand for authentic international cuisines. Qatar's affluent population further supports premium dining options and innovative service formats. The country's proximity to major population centers enables rapid concept testing, with successful formats scaling across the national market in months rather than years. Initiatives like the Michelin Guide Doha 2025 and Qatar Tourism's "Taste of Qatar" enhance Qatar's reputation as a culinary destination, attracting food tourists and boosting international brand recognition.

Competitive Landscape

Top Companies in Qatar Foodservice Market

Qatar's foodservice market exhibits fragmented competition with a concentration score of 3 out of 10, creating substantial white-space opportunities for both local entrepreneurs and international franchise expansion. The market structure enables diverse strategic approaches, from independent operators leveraging cultural authenticity and menu customization to chained concepts capitalizing on brand recognition and operational standardization. Nearly 9,000 food establishments registered with the Ministry of Public Health's Watheq system indicate market depth, while the processing of 30,156 new recruitment applications in Q4 2024 suggests continued capacity expansion across the sector.

Technology adoption emerges as a key competitive differentiator, with Talabat's expansion from 6 to 160+ employees demonstrating scalability potential for digital-first business models, while autonomous delivery trials with Qatar Foundation indicate service innovation leadership. The mandatory electronic payment infrastructure levels the competitive playing field, enabling smaller operators to compete with established chains through seamless digital transaction processing. Strategic positioning varies significantly across market segments, with cloud kitchen operators leveraging the Ministry of Commerce and Industry's streamlined licensing framework to achieve rapid market entry and cost-efficient expansion. Premium dining concepts benefit from Qatar Tourism's "Taste of Qatar" initiative and Michelin Guide recognition, creating quality differentiation opportunities that justify higher price points.

Emerging disruptors focus on sustainability initiatives, with delivery platforms implementing reduced disposable cutlery programs and electric vehicle fleet pilots to capture environmentally conscious consumer segments. The Msheireb Properties food hall development represents institutional investment in community-driven culinary destinations, combining independent operator creativity with professional property management and marketing support. Competitive intensity remains moderate due to market fragmentation, though rising rental costs in prime districts create barriers for new entrants while benefiting established operators with long-term lease agreements.

Qatar Foodservice Industry Leaders

-

Al Mana Restaurants & Food Company

-

Almuftah Group

-

Americana Restaurants International PLC

-

M.H. Alshaya Co. WLL

-

Teatime

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Alshaya Group opened the first Chipotle Mexican Grill restaurant in Qatar, marking the brand’s debut in the market. The launch expanded Alshaya’s portfolio of international foodservice brands and brought Chipotle’s signature customizable Mexican cuisine to diners in Qatar.

- July 2025: Americana Restaurants signed an exclusive franchise agreement to bring the premium Greek café and retail brand Carpo to the Middle East. The agreement granted Americana exclusive rights to operate Carpo stores in Kuwait and Qatar.

- June 2025: Qatar Airways partnered with acclaimed French chef Yannick Alléno to elevate its culinary offerings both in the air and on the ground. As part of this collaboration, the airline opened the Pavyllon restaurant in the Qatar Airways Al Safwa First Lounge at Hamad International Airport in Doha.

- April 2025: Signature by MARZA Restaurant, Qatar’s largest multi-cuisine dining destination, officially opened in the Midmac Roundabout on Salwa Road. The restaurant introduced “Chai Story,” a 24-hour tea counter serving authentic South Indian delicacies paired with Samovar tea.

Qatar Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Café and Bars | By Cuisine | Bars & Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee & Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars & Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee & Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms