Market Trends of Puerto Rico Home Mortgage Finance Industry

Increase in Economic Growth and GDP per capita

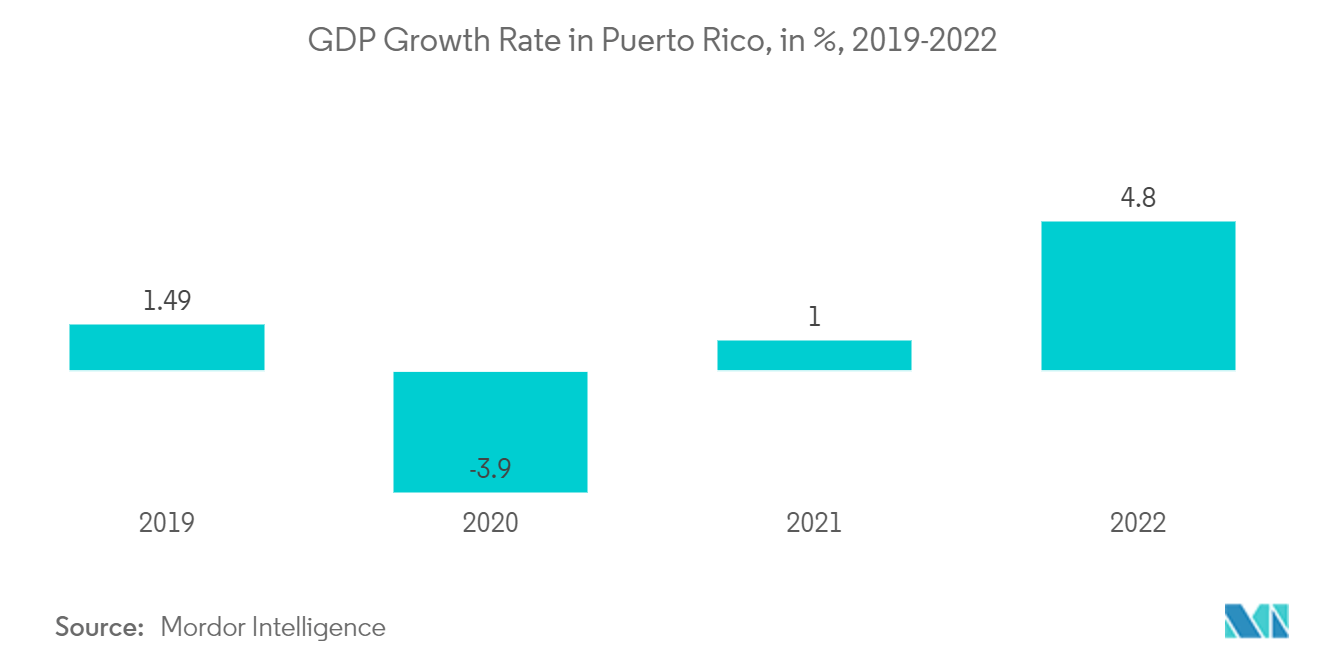

Puerto Rico's economy was in a severe structural decline for more than ten years before it experienced a string of natural calamities, including hurricanes, earthquakes, and the COVID-19 pandemic beginning in 2017. Nearly half of the populace lived below the federal poverty level as a result of the Government's default on a large portion of its debt. Although there are many explanations for these issues, their roots go back 40 years.

By maximizing revenue collection and lowering government-wide spending, government efficiency measures aim to streamline and transform Puerto Rico's government to deliver essential services to the popular and business sector more effectively while ensuring the sustainability of those services over time given population trends. Such policy changes will have a short-term contractionary effect on the economy, but they are essential for long-term improvements in service delivery, budgetary sustainability, and government efficiency. Through FY2051, the combined effect of these two dynamics will continue to be quite favorable for fiscal reductions.

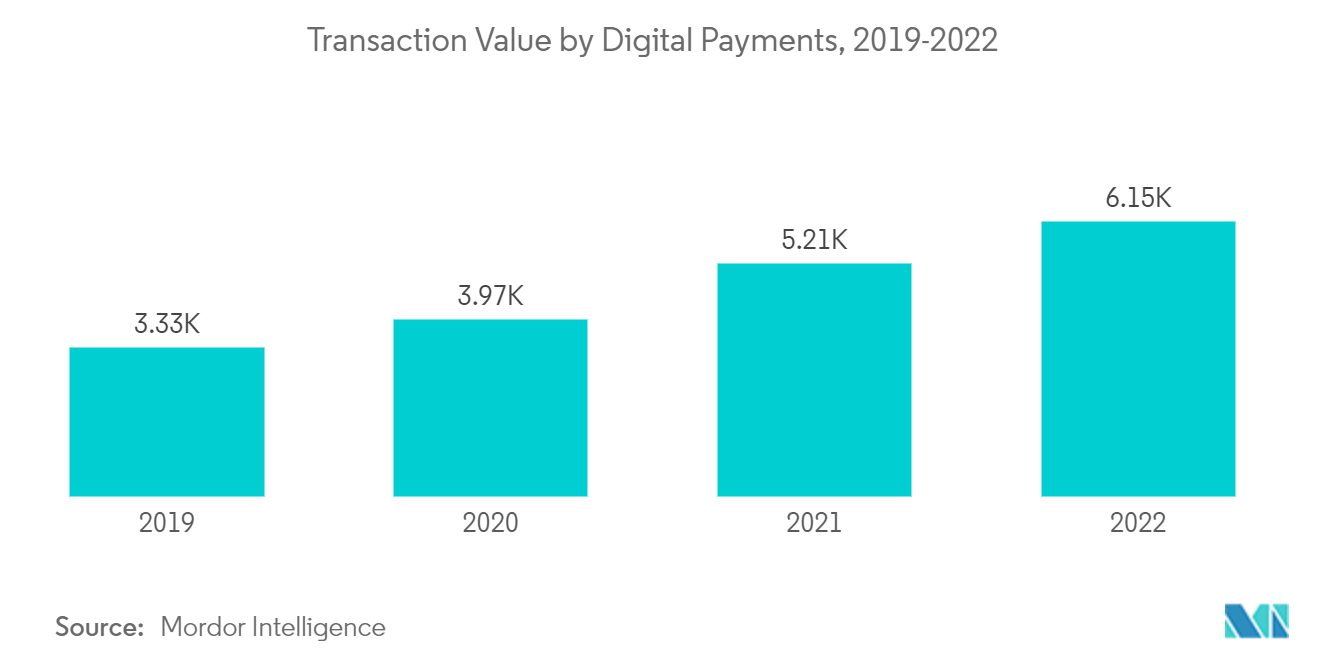

Rising FinTech Companies in Lending Space Drives the Market

Fintech, or technological innovation in financial operations, can open up the market for more financial services, boost efficiency and competitiveness, and lower prices and frictions.

Decentralized finance (Defi), which is a type of financial intermediation based on crypto assets, has grown by leaps and bounds in the last two years. This is because it has pushed innovation to a whole new level and may have made businesses more efficient and opened up new investment opportunities.Defi and conventional financial intermediaries are becoming more integrated. Even though its market is still small, unregulated Defi presents legal uncertainty as well as market, liquidity, and cyber concerns.

Policies that proportionally target incumbents and fintech companies are required. More stringent capital, liquidity, and operational risk-management standards for neobanks are preferred (at the entity and group levels), commensurate with their risks. Because incumbent banks' current business models might not be as long-lasting as those of more technologically sophisticated banks, prudential supervision may need to pay more attention to the soundness of these institutions.