Public Relations Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Market Size (2026) | USD 114.15 Billion |

| Market Size (2031) | USD 161.47 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

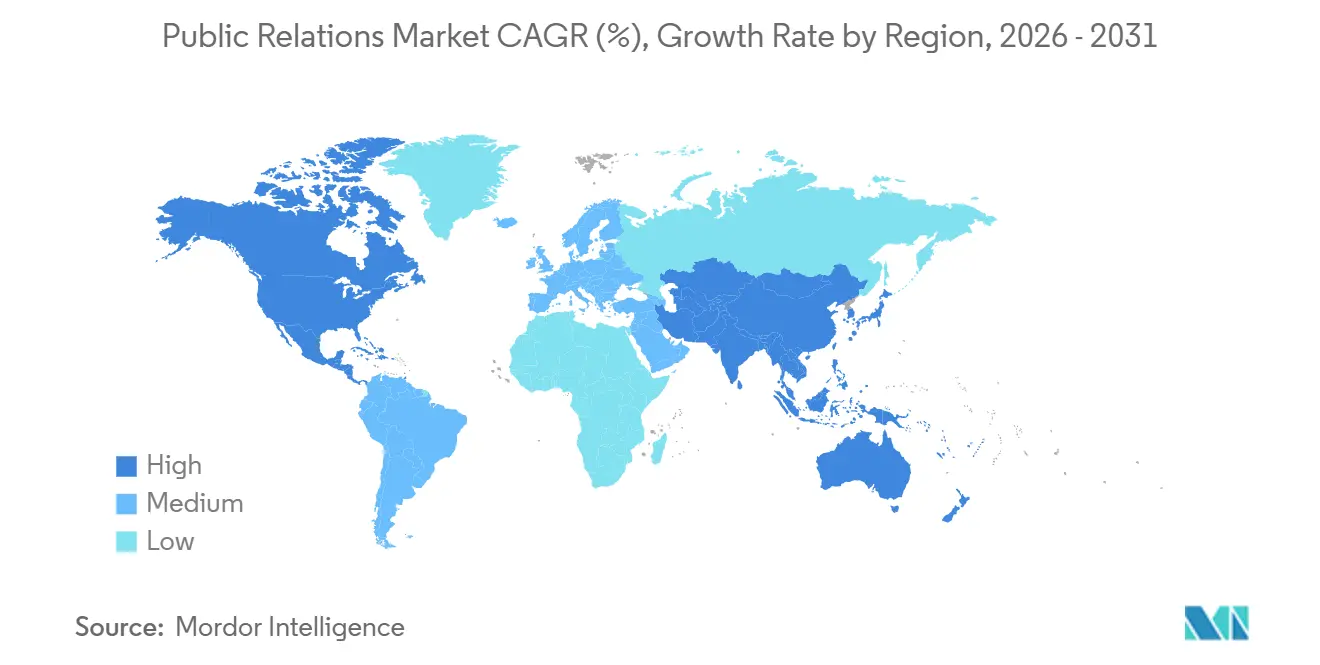

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Public Relations Market Analysis by Mordor Intelligence

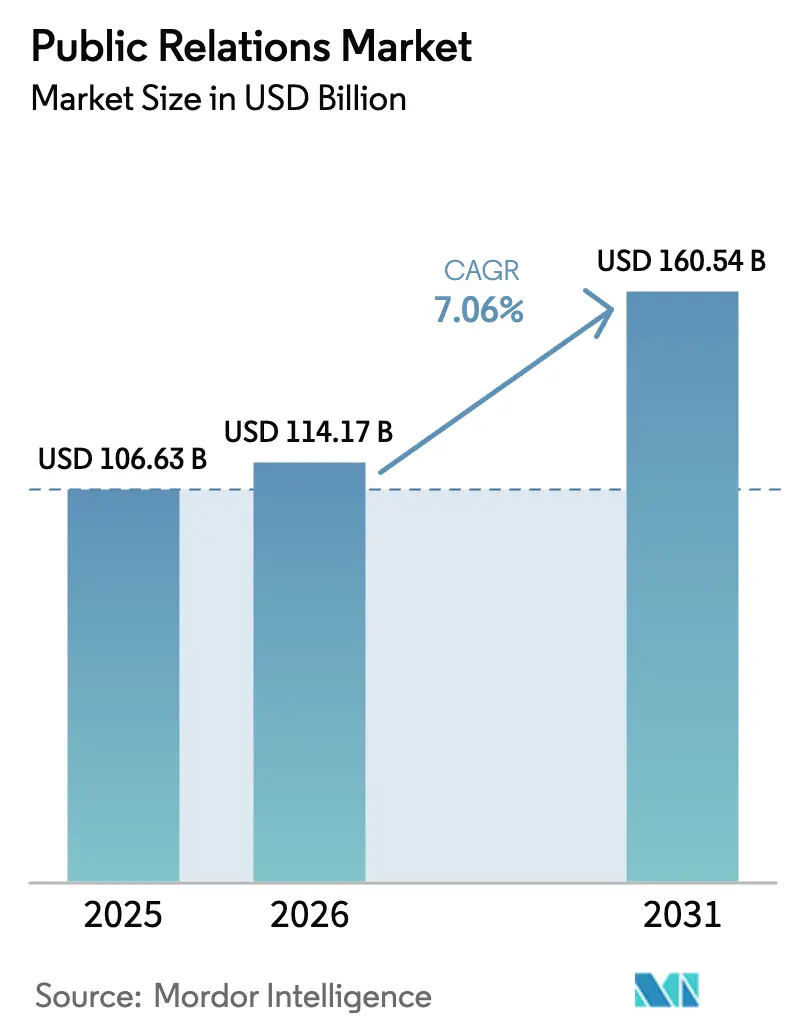

The public relations market size is projected to expand from USD 105.63 billion in 2025 and USD 114.15 billion in 2026 to USD 161.47 billion by 2031, registering a CAGR of 7.18% between 2026 to 2031. Intensifying regulatory disclosure requirements, rapid-fire social-platform crises, and the mainstreaming of AI-driven media analytics are pushing organizations to professionalize narrative management at a global scale. Holding companies are investing in predictive insight tools that compress reporting cycles from weeks to hours, while in-house content studios raise competitive pressure on routine execution tasks. Hybrid and virtual events have normalized post-pandemic engagement models, and influencer-commerce integrations continue to blur the line between earned and paid exposure. Against this backdrop, differentiated advisory services- particularly crisis preparedness, ESG communications, and investor relations- command premium fees, even as commoditized press-release distribution faces margin squeeze.

Key Report Takeaways

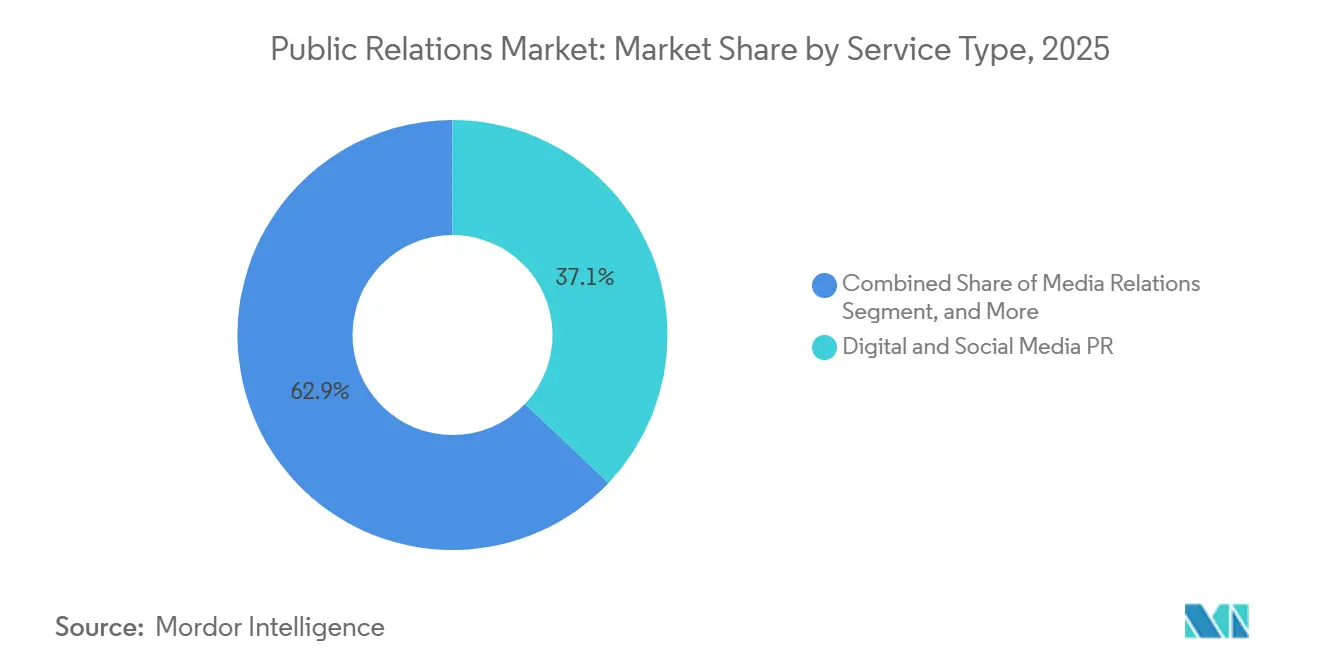

- By service type, digital and social media PR captured 40.27% of the public relations market share in 2025, while analytics and insights services is forecast to advance at a 7.42% CAGR through 2031.

- By channel, digital and online media accounted for 57.84% of 2025 spend, whereas influencer and creator-led media is projected to grow at 7.88% over the same horizon.

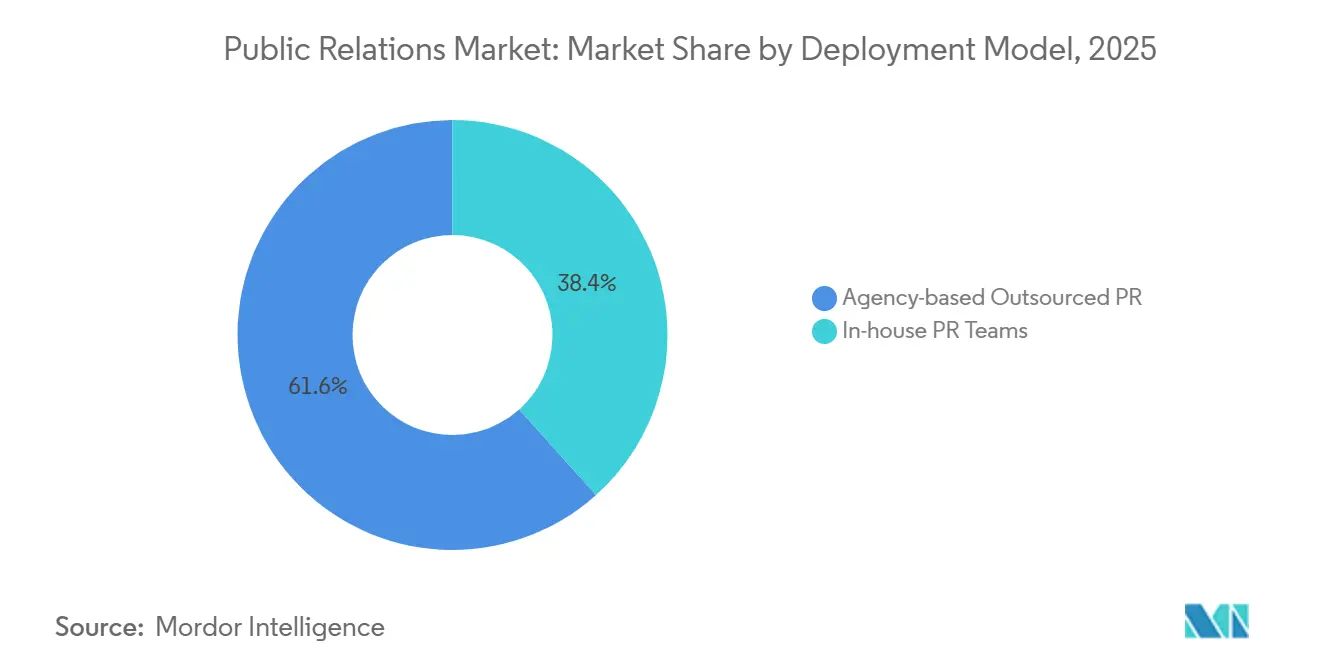

- By deployment, agency-based outsourced PR held 61.63% of budgets in 2025 and is expected to expand at a 7.64% CAGR to 2031.

- By organization size, large enterprises commanded 53.58% of expenditure in 2025, yet small and medium enterprises are set to rise at 8.02% through 2031.

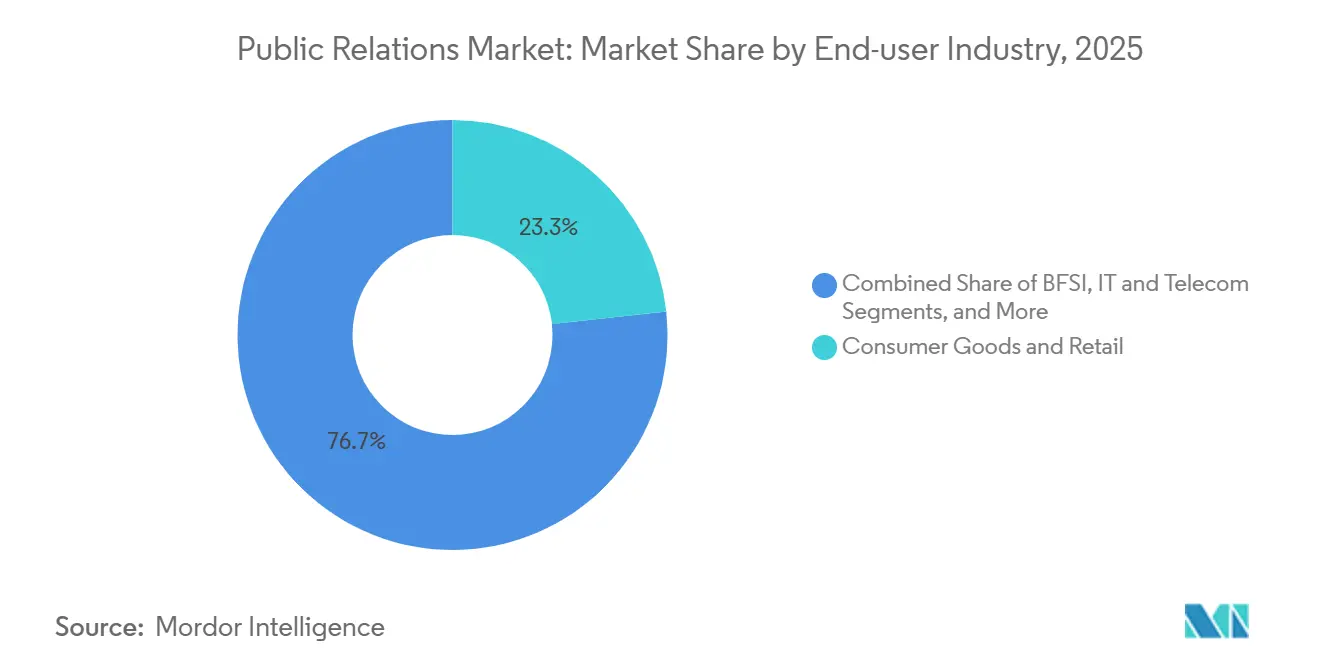

- By end-user industry, consumer goods and retail led with 23.26% share in 2025, while healthcare and life sciences is poised to increase at 7.96% during the forecast period.

- By geography, North America generated 34.77% of 2025 revenues, but Asia-Pacific is anticipated to accelerate at 8.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Public Relations Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Brand-Reputation Risk on Social Platforms in Asia | +1.2% | Asia-Pacific core, spillover to Middle East and Africa | Short term (≤ 2 years) |

| ESG-Driven Disclosure Mandates Elevating Corporate Narrative Management in Europe | +1.5% | Europe primary, North America secondary | Medium term (2-4 years) |

| Influencer-Led Earned-Media Boom Among North-American Consumer Brands | +1.3% | North America and Europe | Short term (≤ 2 years) |

| AI-Powered Media-Analytics Adoption Optimising PR Budget Allocation | +1.4% | Global | Medium term (2-4 years) |

| Expansion of Virtual and Hybrid Events post-COVID-19 | +0.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Venture-Capital Surge in Middle East and Africa Fueling Investor-Relations PR | +0.9% | Middle East and Africa primary, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ESG-Driven Disclosure Mandates Elevating Corporate Narrative Management in Europe

The European Union’s Corporate Sustainability Reporting Directive, effective for fiscal year 2025 filings, obliges roughly 50,000 companies to provide double-materiality assessments and seek external assurance. Supplemental guidance from the European Financial Reporting Advisory Group clarified Scope 3 emissions definitions, forcing issuers to convert technical data into plain-language narratives that satisfy investors, regulators, and community stakeholders.[1]European Financial Reporting Advisory Group, “Scope 3 Emissions Updates,” efrag.org Enforcement priorities announced by the European Securities and Markets Authority have already targeted greenwashing, prompting companies to route every sustainability statement through legal-compliance reviews before release.[2]European Securities and Markets Authority, “2024 Greenwashing Enforcement,” esma.europa.eu Agencies capable of reconciling divergent U.S. and EU disclosure rules now secure multi-year retainers, as cross-listed firms need consistent yet jurisdiction-compliant messaging for roadshows on both sides of the Atlantic.

AI-Powered Media-Analytics Adoption Optimizing PR Budget Allocation

Generative AI modules embedded in platforms such as Cision Vuelio Lumina, Meltwater AI Studio, and Onclusive predictive analytics now automate summarization, sentiment scoring, and ROI modeling across 40 languages. Vuelio Lumina cut manual clip reviews by 60% during 2025 pilots, while Meltwater AI Studio reduced content-production cycles from days to hours by auto-drafting press releases. Onclusive goes a step further by correlating earned-media volume with stock-price movements, enabling CFOs to link narrative share of voice to enterprise value. These capabilities democratize insight for mid-tier agencies and corporate teams, eroding the historic data-lake advantage enjoyed by holding-company networks.

Influencer-Led Earned-Media Boom Among North-American Consumer Brands

Influencer commerce generated USD 236 billion in earned-media value globally in 2026, with North American brands accounting for 42% of spend. Sephora’s 2025 micro-influencer program delivered USD 6.50 in return per dollar invested, tripling the efficiency of traditional paid channels. Walmart’s Creator platform attracted 15,000 influencers within its first quarter, generating 22 million impressions without incremental ad spend. Federal Trade Commission endorsement-guide updates now mandate full disclosure of brand–influencer ties, increasing compliance overhead yet validating the need for specialized agencies able to supervise multi-creator campaigns across jurisdictions.[3]Federal Trade Commission, “Endorsement Guides Update,” ftc.gov

Escalating Brand-Reputation Risk on Social Platforms in Asia

Algorithmic amplification and strict content-moderation rules on Weibo, WeChat, LINE, and KakaoTalk can elevate local missteps into region-wide crises within hours. Xiaomi’s data-privacy backlash in India in February 2025 triggered a 12% drop in sentiment scores inside two days, compelling a rapid public apology and independent audit. Weibo’s updated crisis-response guidelines require brands to answer trending negative hashtags inside two hours or face post-suppression, a timeline that only agencies with 24/7 multilingual monitoring can mee. Japan’s revised Corporate Governance Code similarly obliges listed firms to publish quarterly social-media risk disclosures, expanding the client base for specialized reputation analyticswithin vendors.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Measurement Standards Hindering ROI Transparency | -0.9% | Global | Medium term (2-4 years) |

| Data-Protection Regimes (GDPR, CPRA) Limiting Audience Targeting | -1.1% | Europe and North America primary, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Bilingual Digital-PR Talent Scarcity in High-Growth Non-English Markets | -0.6% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| In-house Content Studios Cannibalising Agency Retainers | -0.8% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Protection Regimes Limiting Audience Targeting

The General Data Protection Regulation and California Privacy Rights Act restrict third-party cookie use and mandate explicit consent for personal-data processing, dulling the precision of segmented outreach.[4]California Privacy Protection Agency, “CPRA Enforcement Actions,” cppa.ca.gov Google’s full cookie deprecation in Chrome by late 2024 removed a cornerstone of cross-site behavioral tracking. Subsequent guidance from the European Data Protection Board further requires opt-in consent for sentiment monitoring when special-category data is involved. Compliance costs rose as smaller brands struggled to build consent-management systems, prompting many to lean on large agencies with in-house counsel and automated workflows.

Fragmented Measurement Standards Hindering ROI Transparency

Despite the Barcelona Principles, only 38% of agencies applied AMEC’s framework consistently in 2024, leaving procurement teams to decode proprietary dashboards before approving budgets. Legacy advertising-value equivalency metrics still appear in nearly one-third of reports, undermining credibility with finance functions that demand objective attribution. Without consensus on sentiment-weighting or share-of-voice methodology, brands hesitate to scale spend, and many establish internal analytics teams, diverting revenue away from external partners.

Segment Analysis

By Service Type: Analytics Reshapes Budget Mix

Analytics and Insights Services will steer incremental spend as enterprises shift toward predictive sentiment modeling and CFO-friendly ROI dashboards. Digital and Social Media PR remains foundational, holding 40.27% of 2025 billings, yet commoditization looms as automation drafts posts and monitors feeds at negligible marginal cost. Crisis and Issues Management retains durable pricing power because social-platform velocity turns minor missteps into existential threats overnight. Investor and Financial Communications also outperforms, buoyed by Middle East fundraising waves that require global roadshows formatted to U.S. and EU disclosure norms. Meanwhile, Event and Experiential Communication benefits from hybrid-event tooling that tracks real-time engagement data, increasing accountability for sponsorship returns. Content Development, particularly executive ghostwriting on LinkedIn, is revitalized by algorithm changes that preference long-form leadership perspectives. As advisory lines thicken, public relations market revenues tilt toward higher-margin counsel while transactional press-release distribution declines.

The financial reweighting underscores a crucial distinction, while automation trims executional headcount, data-rich counsel commands premium retainers that safeguard agency profitability. Firms that bundle proprietary insight engines with domain experts now pitch a full-stack proposition- monitor, predict, and message- positioning analytics as the new gateway service for retainer expansion.

Note: Segment shares of all individual segments available upon report purchase

By Channel: Influencer and Creator-Led Media Gains Velocity

Digital and Online Media seized 57.84% of 2025 expenditure, yet brands are reallocating to creator ecosystems that convert directly at the point of discovery. TikTok Shop processed USD 20 billion in United States merchandise value during 2025, validating closed-loop earned commerce. Instagram’s affiliate link roll-out and YouTube’s live analytics similarly embed attribution into creator workflows, letting brands see revenue lift in real time. Traditional and Earned Media, especially tier-one financial outlets, still anchor thought leadership for regulated industries, but budgets migrate toward performance-tracked placements. The Federal Trade Commission’s tougher disclosure rules raise legal oversight costs, a burden smaller brands offset by favoring contextual sponsorships over large-scale influencer buys. Consequently, agencies capable of uniting influencer discovery, contract compliance, and live attribution within one dashboard capture growing share.

For B2B narratives, podcasts and LinkedIn newsletters blend evergreen content with measurable engagement, demonstrating that not all digital channels are equal. High-trust technical communities, from cybersecurity slack groups to health-care provider forums, remain niche yet influential arenas where specialized agencies secure premium rates for insider access.

By Deployment Model: Agencies Defend Retainers Through Specialization

Agency-based Outsourced PR held 61.63% of global spend in 2025, benefiting from cross-border regulatory complexity that in-house teams rarely navigate at scale. To protect margins, network firms invested more than GBP 250 million (USD 318 million) in AI and data analytics acquisitions, turning technology into a modern retainer hook. In-house units counter by internalizing low-complexity tasks- social listening, press-release drafting, creator outreach- yet still lean on agencies for crisis playbooks, merger messaging, or ESG cross-filing synchronization. As compliance horizons widen, agencies increasingly sell annual “risk-readiness” subscriptions that bundle scenario training, dark-site builds, and real-time media audits.

The bifurcation resembles management consulting, commoditized execution migrates inside the enterprise, while external counselors monetize uncertainty. Over the forecast period, agencies that cannot articulate a proprietary specialization risk shrinkage as procurement rationalizes duplicate vendor lists.

By Organization Size: SMEs Embrace Cloud-Based Platforms

Large Enterprises represented 53.58% of 2025 outlays, financed by multinational campaigns and quarterly crisis drills. Yet Small and Medium Enterprises are slated to outpace, expanding at 8.02% through 2031, driven by software subscriptions below USD 500 per month that emulate enterprise-grade monitoring and distribution. Cision, Meltwater, and Agility PR Solutions now market tiered packages with drag-and-drop dashboards, allowing SMEs to launch data-driven outreach without the six-figure licenses once mandatory.

Public relations market size growth within the SME segment also reflects democratized creator access. SaaS platforms such as AspireIQ match micro-influencers to local brands, slashing acquisition costs by up to 60% and broadening earned-media reach among niche audiences. While large enterprises will continue to dominate high-risk spend categories such as litigation communications, the swelling SME base guarantees a wider demand pool that agencies may tap through flexible, modular service menus.

By End-User Industry: Healthcare Compliance Drives Premium Pricing

Consumer Goods and Retail led overall revenue, buoyed by daily product drops and heavily monetized influencer programs. However, escalating regulatory guidance positions Healthcare and Life Sciences for faster expansion. The U.S. Food and Drug Administration’s December 2025 biosimilar-promotion rules clarified interchangeability claims, sparking immediate RFPs for physician-education campaigns. Simultaneously, the European Medicines Agency’s patient-communication survey revealed consumer preference for plain-language summaries, incentivizing pharma companies to outsource medical writing to specialist communicators.

Banking, Financial Services, and Insurance maintain stable demand as institutions navigate International Sustainability Standards Board climate-reporting frameworks. Government, entertainment, and travel sectors display recovery trends tied to post-pandemic mobility, with tourism rebounding to 96% of 2019 arrivals according to the United Nations World Tourism Organization. As regulatory intensity correlates with spend complexity, agencies deepen vertical benches, hiring scientific writers for life sciences, sustainability analysts for BFSI, and multilinguists for public-sector transparency mandates.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 34.77% of 2025 billings and will post mid-single-digit growth to 2031. Platform innovations such as Walmart Creator and Amazon’s livestream-analytics dashboards illustrate how retailer ecosystems can turbocharge earned commerce within weeks. The Federal Trade Commission’s stricter endorsement rules heighten legal-review throughput, favoring agencies that bundle counsel across brand portfolios. Canada and Mexico augment regional upside by mandating bilingual outreach to comply with privacy and cultural norms, expanding addressable demand for cross-border service suites.

Asia-Pacific is forecast to record an 8.21% CAGR, the fastest among all regions. High-velocity social platforms heighten crisis frequency, pushing brands to maintain 24/7 monitoring and rapid-response war rooms. Weibo’s two-hour policy on trending negativity, India’s data-sovereignty probes, and Japan’s governance code revisions collectively create a compliance-plus-reputation imperative that domestic agencies leverage for premium retainers. Public relations market revenues here rise not only on volume but on the complexity premium attached to a multilingual strategy across Mandarin, Hindi, Japanese, Korean, and Bahasa Indonesia.

Europe, the Middle East, and Africa together supply a multi-speed landscape. Europe’s ESG disclosure law enforces double-materiality reviews, driving consultative engagements with sustainability subject-matter experts. The Middle East records venture-capital surges headlined by Saudi Arabia’s Public Investment Fund, which allocates USD 750 million into tech and healthcare startups, each demanding investor-relations storytelling in both Arabic and English. In Africa, fintech hotspots in Nigeria and South Africa spur brand-building around financial inclusion narratives, although bilingual talent scarcity curtails rapid scale.

Competitive Landscape

No single provider controls more than 8% of global billings, yet the top ten networks collectively manage roughly 35%, leaving a broad mid-tier to differentiate on vertical depth or local language capability. Holding companies such as WPP, Omnicom, Publicis, Dentsu, and Interpublic continue to purchase analytics platforms to reinforce data-validated storytelling. Publicis invested in Q4 Inc. for live earnings-call sentiment analysis in January 2026. Omnicom’s USD 835 million acquisition of Flywheel Digital embeds retail-media attribution inside its communications stack, linking creator activation to point-of-sale data. Dentsu’s Crisis Navigator simulator employs large-language models to replicate multi-channel backlash scenarios, cutting client training costs by 40%.

Independent leaders such as Edelman and Brunswick scale through proprietary research and trust-barometer surveys, selling insight as a wedge into advisory mandates. Cloud platforms continue to democratize baseline services, undermining barriers that once protected mid-size agencies. Consequently, networks migrate upmarket toward crisis, ESG, and investor-relations counsel, while boutique consultancies occupy deep-vertical niches. The competitive dynamic now centers on intellectual capital rather than headcount alone, with data scientists, compliance lawyers, and sector specialists forming the new talent battleground.

Emerging white-space clusters include multilingual content hubs for non-English high-growth markets and integrated ESG narrative orchestration tools that align financial, sustainability, and employee messaging under one compliance screen. Agencies able to stitch these offerings into seamless dashboards lock in multi-year retainers, whereas generalists risk commoditization.

Public Relations Industry Leaders

WPP plc

Omnicom Group Inc.

Interpublic Group of Companies Inc.

Publicis Groupe S.A.

Dentsu Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Publicis Groupe acquired a minority stake in Q4 Inc., integrating real-time investor-sentiment analytics into its financial-communications practice.

- December 2025: U.S. Food and Drug Administration issued final biosimilar-promotion guidance, expanding healthcare PR opportunity sets.

- November 2025: Omnicom Group completed its USD 835 million Flywheel Digital purchase, linking retail-media attribution to earned influence.

- October 2025: Dentsu Group launched Crisis Navigator, an AI-based crisis simulation platform that cuts training cycles by 40%.

Global Public Relations Market Report Scope

Public relations is a strategic communication process that builds mutually beneficial relationships between organizations and their publics. It involves managing the spread of information between an organization and the public, aiming to influence public perception and maintain a positive image. Effective public relations strategies can enhance an organization's reputation, foster trust, and support its overall objectives.

The Public Relations Market Report is Segmented by Service Type (Media Relations, Digital and Social Media PR, Crisis and Issues Management, Event and Experiential Communication, Content Development and Thought Leadership, Analytics and Insights Services, and Investor and Financial Communications), Channel (Traditional/Earned Media, Digital/Online Media, and Influencer and Creator-led Media), Deployment Model (In-house PR Teams and Agency-based Outsourced PR), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Consumer Goods and Retail, BFSI, IT and Telecom, Healthcare and Life Sciences, Government and Public Sector, Entertainment and Media, Travel and Hospitality, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Media Relations |

| Digital and Social Media PR |

| Crisis and Issues Management |

| Event and Experiential Communication |

| Content Development and Thought Leadership |

| Analytics and Insights Services |

| Investor and Financial Communications |

| Traditional / Earned Media |

| Digital / Online Media |

| Influencer and Creator-led Media |

| In-house PR Teams |

| Agency-based Outsourced PR |

| Large Enterprises |

| Small and Medium Enterprises |

| Consumer Goods and Retail |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Entertainment and Media |

| Travel and Hospitality |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Service Type | Media Relations | |

| Digital and Social Media PR | ||

| Crisis and Issues Management | ||

| Event and Experiential Communication | ||

| Content Development and Thought Leadership | ||

| Analytics and Insights Services | ||

| Investor and Financial Communications | ||

| By Channel | Traditional / Earned Media | |

| Digital / Online Media | ||

| Influencer and Creator-led Media | ||

| By Deployment Model | In-house PR Teams | |

| Agency-based Outsourced PR | ||

| By Organisation Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-User Industry | Consumer Goods and Retail | |

| BFSI | ||

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Entertainment and Media | ||

| Travel and Hospitality | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the expected value of the public relations market by 2031?

The sector is forecast to reach USD 161.47 billion by 2031.

Which service line is growing fastest within public relations?

Analytics and Insights Services is projected to rise at a 7.42% CAGR through 2031.

Why are agencies still critical despite in-house content studios?

Enterprises rely on agencies for crisis management, ESG disclosure alignment, and investor-relations counsel that require regulatory fluency and 24/7 global coverage.

Which region is set to post the highest growth rate?

Asia-Pacific is on track for an 8.21% CAGR between 2026 and 2031, driven by social-platform volatility and expanding middle-class consumption.

How do data-protection laws impact public relations spending?

GDPR and CPRA restrictions reduce targeting precision, increasing compliance costs and favoring large agencies equipped with automated consent-management tools.