Market Trends of UAE Property & Casualty Insurance Industry

This section covers the major market trends shaping the UAE Property & Casualty Insurance Market according to our research experts:

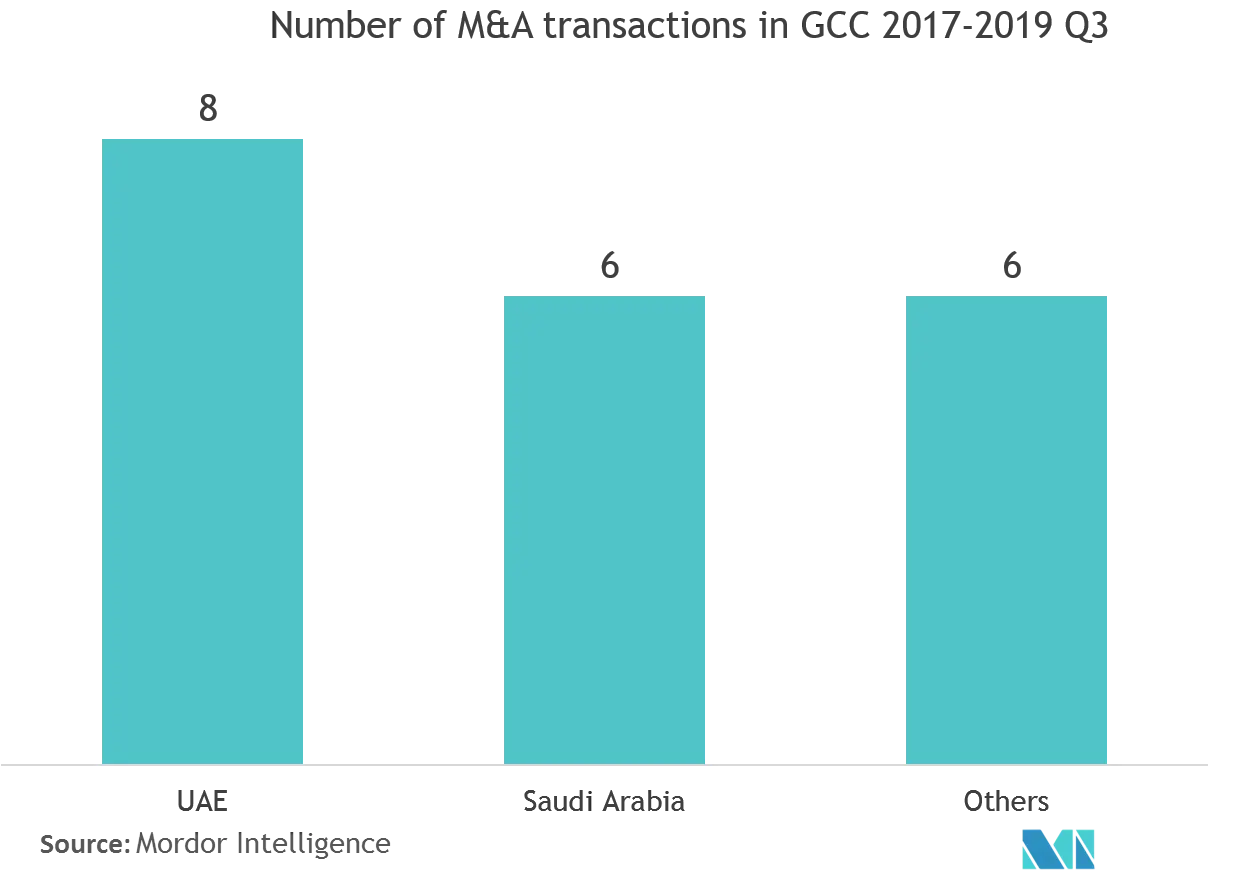

Growing Consolidation

High operating costs, combined with a strengthening regulatory environment, are driving the GCC insurance sector toward consolidation. As a result, the share of the top 20 listed insurance companies in the region (based on GWP) increased from 50.9% in 2016 to 57.9% in 2018. The region witnessed 22 mergers and acquisitions (including on-going deals) between 2017 and Q3 2019. There were eight deals in the United Arab Emirates and six in Saudi Arabia, cumulatively accounting for approximately 64% of the total deal volume. In 2019 alone, the region observed six mergers and acquisitions, and this trend is expected to continue, to enable firms to increase their operational efficiencies and reduce costs.

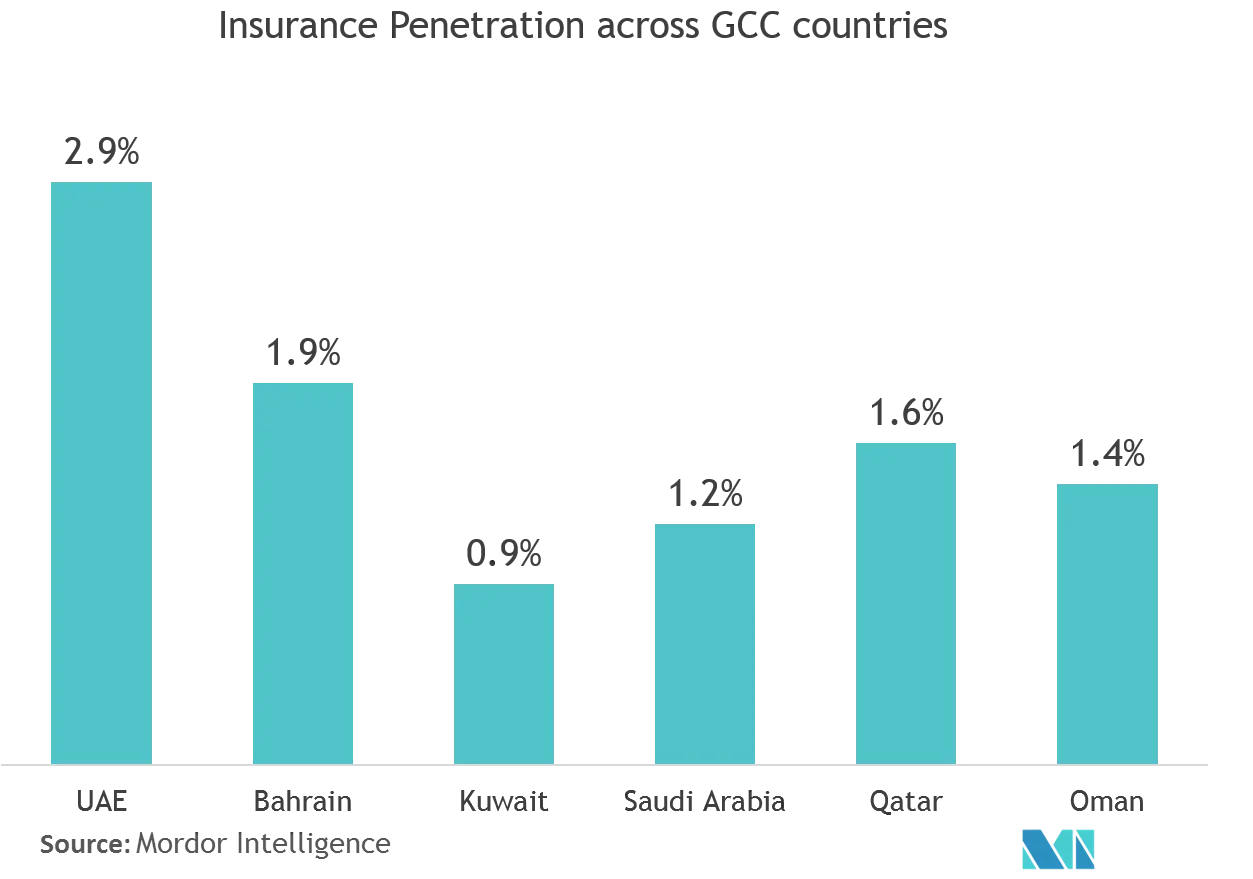

The United Arab Emirates has the Highest Insurance Penetration across GCC Countries

Insurance penetration in the individual GCC markets differ significantly, with the United Arab Emirates averaging at 2.9%, followed by Bahrain (1.9%), Qatar (1.6%), Oman (1.4%), and Saudi Arabia (1.2%). Kuwait recorded the lowest average insurance penetration, at 0.9%, in 2018. Low penetration is primarily attributed to low awareness regarding the importance of insurance products and the relatively underdeveloped life insurance market. Moreover, monetary support provided to nationals in the region make the need for insurance redundant for that segment of the population. In the United Arab Emirates, the rate of insurance penetration remains the highest compared to other GCC countries, largely owing to the diversified population base, which majorly comprises expatriates, and the rollout of mandatory health and motor insurance schemes.