Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

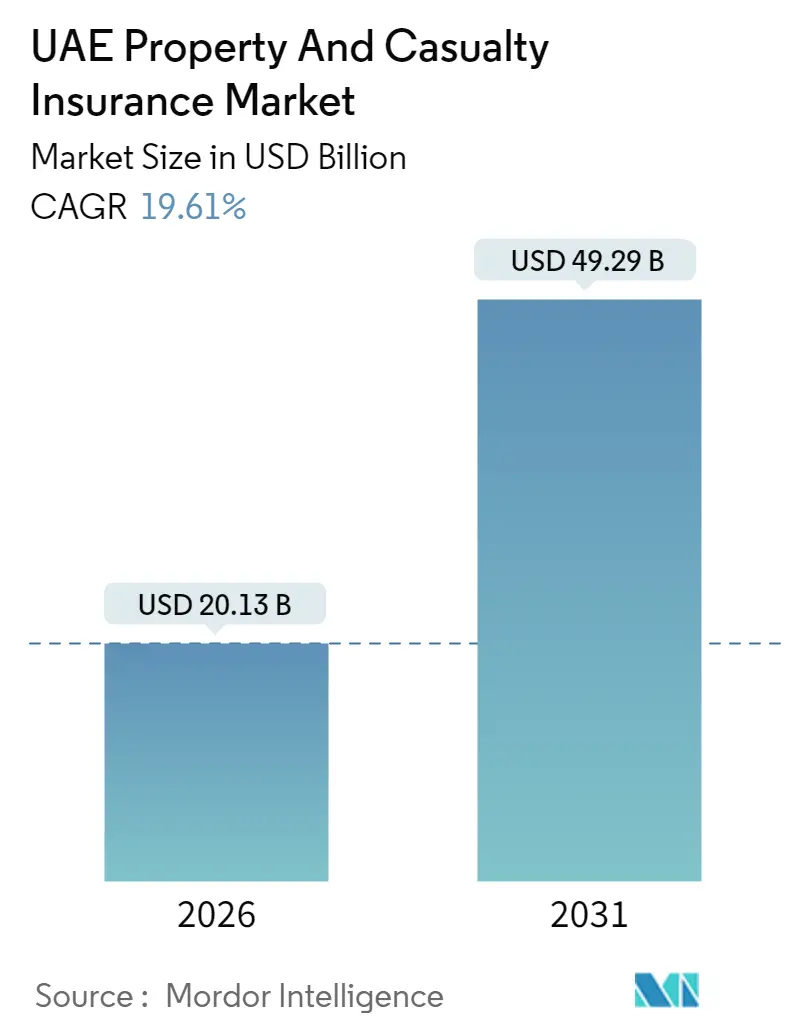

| Market Size (2026) | USD 20.13 Billion |

| Market Size (2031) | USD 49.29 Billion |

| Growth Rate (2026 - 2031) | 19.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Property And Casualty Insurance Market Analysis by Mordor Intelligence

The UAE property and casualty insurance market was valued at USD 16.83 billion in 2025 and estimated to grow from USD 20.13 billion in 2026 to reach USD 49.29 billion by 2031, at a CAGR of 19.61% during the forecast period (2026-2031). This expansion is fueled by strict mandatory‐cover rules, the USD 100 billion construction pipeline, and a nationwide pivot to digital distribution that is reshaping risk selection and claims handling. Regulatory tightening under Federal Decree-Law No. 48 of 2023 places solvency and conduct at the center of supervisory oversight, giving well-capitalized underwriters a clear advantage. April 2024 flood losses of more than USD 650 million sharpened underwriting discipline and catalyzed flood-specific endorsements, while the launch of AI-supported reinsurer RIQ in Abu Dhabi global market underscores the sector’s ability to attract fresh capital. Intensifying bancassurance and aggregator penetration promises broader customer reach, particularly in motor and property lines, where standardized products and high purchasing frequency favor online channels.

Key Report Takeaways

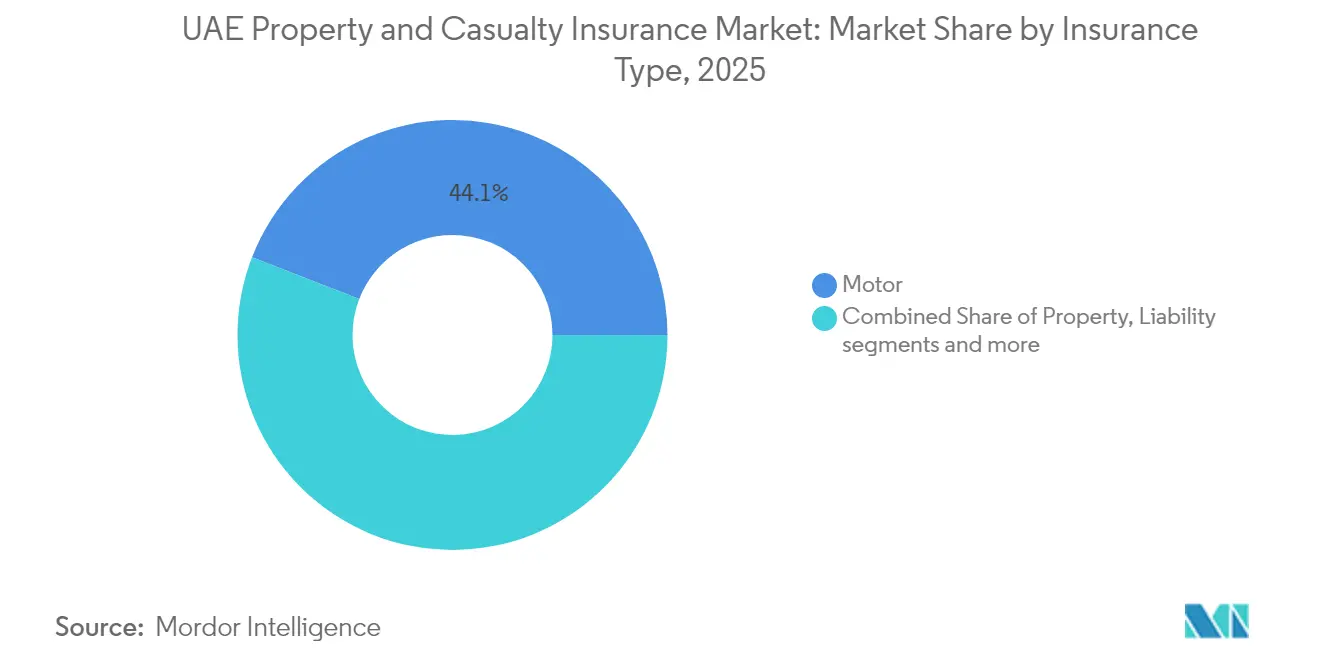

- By insurance type, motor policies accounted for 44.12% of the UAE property and casualty insurance market share in 2025; cyber and digital-risk cover is projected to expand at a 12.08% CAGR through 2031.

- By distribution channel, brokers led with 47.88% revenue share in 2025, while bancassurance is forecast to grow at 10.29% CAGR to 2031.

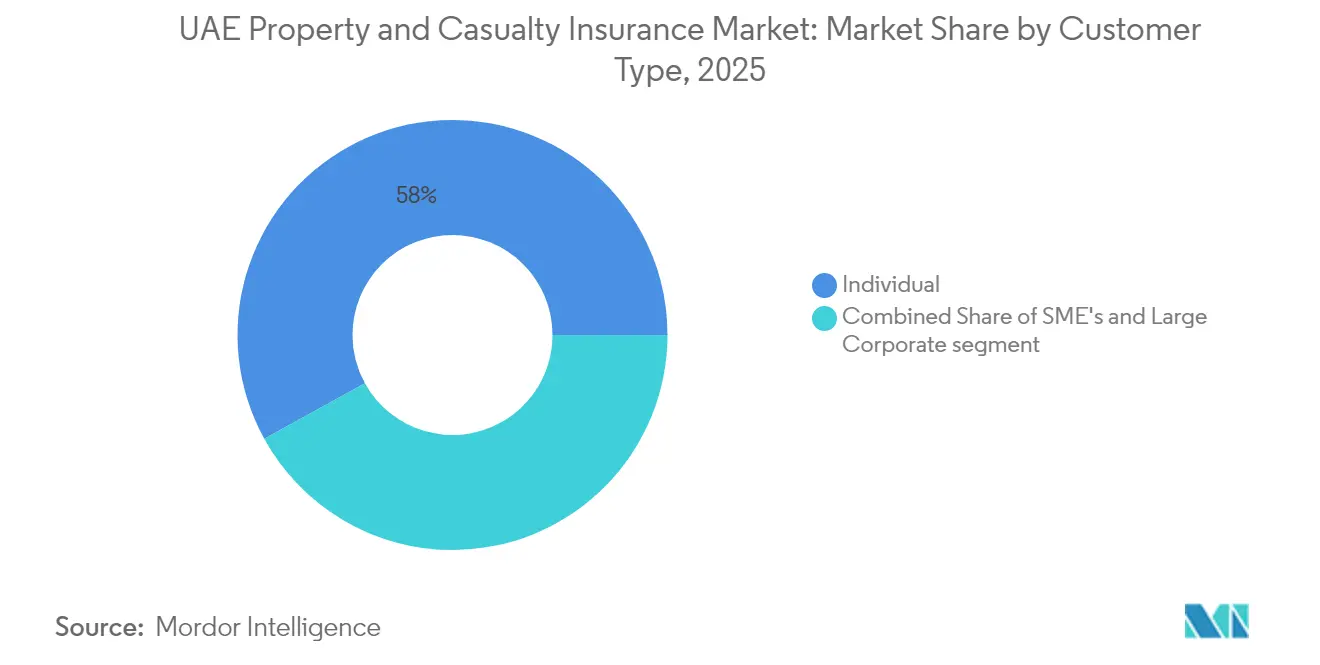

- By customer type, individual buyers held 58.02% of written premiums in 2025, whereas large corporate and government risks are set to grow at 10.97% CAGR over 2026-2031.

- By end industry, automotive lines captured 24.83% share of the UAE property and casualty insurance market size in 2025; the electric-vehicle ecosystem is advancing at 15.1% CAGR.

- By region, Dubai commanded 59.72% revenue in 2025; Abu Dhabi is delivering the strongest growth at 12.05% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Property And Casualty Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory motor insurance & rising vehicle parc | +4.2% | UAE-wide, strongest in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Construction boom & mega-projects pipeline | +5.8% | Dubai and Abu Dhabi core, spillover to Northern Emirates | Medium term (2–4 years) |

| Stronger solvency regulation boosting consumer trust | +2.1% | UAE-wide | Long term (≥ 4 years) |

| Growth of digital/aggregator distribution | +3.4% | Urban centers | Medium term (2–4 years) |

| Climate-driven flood events heightening risk awareness | +2.9% | Flood-prone lowlands | Short term (≤ 2 years) |

| EV adoption generating demand for specialised cover | +1.6% | Early-adopter emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Motor Insurance & Rising Vehicle Parc

Federal Decree-Law No. 14 of 2024 on traffic regulation obliges every registered vehicle to carry locally underwritten third-party liability, anchoring a stable premium stream even during economic slowdowns[1]United Arab Emirates Federal Government, “Federal Decree-Law No. 14 of 2024 on Traffic Regulation,” uaelegislation.gov.ae. Dubai alone counted almost 26,000 electric cars by late 2023, creating demand for products such as Sukoon’s “InsureMyTesla,” which bundles battery and charger protection with higher third-party limits. GIG Gulf’s instant Orange Card through UAE PASS simplifies cross-border compliance for motorists who regularly drive into Oman. Compulsory status insulates the line from price wars, while rising ADAS and telematics adoption provide underwriters with richer data for granular pricing.

Construction Boom & Mega-Projects Pipeline

More than USD 100 billion worth of residential, hospitality, and infrastructure works are either underway or tendered, led by super-tall towers that account for 90% of global projects in this class[2]Allianz Global Corporate & Specialty, “Engineering & Construction Market Overview,” agcs.allianz.com. Developers increasingly arrange owner-controlled insurance programmes to consolidate coverage and reduce premium leakages, with global reinsurers supplying capacity for single-site limits that often exceed USD 2 billion. Completed assets transition into operational property programmes, ensuring long-tail growth for the UAE property and casualty insurance market. Abu Dhabi’s industrial zones add large energy and logistics schemes, broadening engineering and delaying start-up exposure.

Stronger Solvency Regulation Boosting Consumer Trust

Since January 2024, the Central Bank has enforced risk-based capital, tighter reserving, and annual “skilled-person” reviews, compelling insurers to strengthen governance and clean up legacy books[3]Clyde & Co, “Insurance Regulation Update UAE,” clydeco.com. The Sanadak ombudsman now offers a structured path for dispute resolution, further bolstering policyholder confidence. Higher barriers to entry encourage consolidation and attract well-rated reinsurers, improving retention capacity and lowering frictional cessions.

Growth of Digital/Aggregator Distribution

Lookinsure and similar portals let customers compare more than 10 insurers in real time, compressing the quote-to-bind cycle to minutes. The April 2024 Open Finance Regulation obliges all insurers to open application-program interfaces for data and payment initiation, enabling fintech partnerships and personalized offers. Banks such as Abu Dhabi Commercial Bank have embedded end-to-end motor policies inside their wealth apps, driving bancassurance volumes.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price competition squeezing underwriting margins | -3.7% | UAE-wide, intensified in Dubai market | Short term (≤ 2 years) |

| Heavy reliance on foreign reinsurance capacity | -2.4% | UAE-wide with global reinsurance market exposure | Medium term (2-4 years) |

| Rising repair-cost inflation on technology-laden vehicles | -1.8% | UAE-wide, concentrated in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Fragmented broker channel causing churn | -1.3% | UAE-wide with urban market concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Competition Squeezing Underwriting Margins

Insurers posted an average combined ratio of 122% in H1 2024, highlighting inadequate pricing discipline, especially in commoditized motor and medical policies. Aggregators amplify price visibility, pushing carriers toward premium-centred tactics that erode profitability. The broker channel, which captured 48.30% of 2024 premiums, often prioritizes commission maximization over risk-adequate pricing, adding to pressure on technical margins.

Heavy Reliance on Foreign Reinsurance Capacity

Higher global catastrophe losses have hardened reinsurance rates, raising cedant costs in the UAE. Currency mis-matches emerge because treaties are predominantly denominated in USD, while retail premiums accrue in AED. The launch of RIQ at Abu Dhabi Global Market, seeded with USD 1 billion, is a first step toward domestic capacity but remains modest compared with national exposure.

Segment Analysis

By Insurance Type: Motor Dominance Drives Digital Innovation

Motor policies contributed 44.12% of the UAE property and casualty insurance market share in 2025, a result of compulsory cover and a 5% annual rise in vehicle registrations. The UAE property and casualty insurance market size linked to cyber and digital-risk lines is on track to climb 12.08% annually to 2031, reflecting heightened ransomware activity and the government’s aggressive digitization agenda. Engineering and construction mirror the USD 100 billion project pipeline, while marine and aviation lines leverage the nation’s global logistics hub status.

Demand for specialty EV cover is intensifying as government targets call for 50% of on-road units to be electric or hybrid by 2050. Products such as InsureMyTesla bundle a charger, battery, and roadside-assist benefits, differentiating on features instead of price. Custodial risk insurance for digital assets, introduced under the “OneInfinity” banner, extends the UAE property and casualty insurance market by insulating Web3 custodians against hot-wallet hacks. Liability products gain traction under stricter professional-indemnity mandates, lifting average policy limits across legal, architectural, and accounting professions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Bancassurance Disrupts Traditional Models

Brokers maintained 47.88% of premiums in 2025 through their ability to place complex energy, marine, and mega-project risks. Yet, bancassurance is growing 10.29% per year as banks leverage transaction data to pre-fill quote screens and offer installment payments that remove upfront sticker shock. Aggregators are surging in standardized lines, pushing underwriters to deploy real-time rating engines and straight-through policy issuance.

Traditional agent networks still serve personal accident and SME property buyers in smaller emirates, but growth is sluggish compared with digital channels. The Open Finance framework will accelerate embedded insurance propositions, enabling ride-hailing apps, airlines, and retailers to deliver single-click coverage. Direct insurer websites have improved net promoter scores following AI chatbot deployments that cut claims-settlement turnaround.

By Customer Type: Corporate Segment Drives Premium Growth

Individual policyholders generated 58.02% of written premiums in 2025, anchored by mandatory motor and home covers. Large corporations and government entities, however, are expanding premiums at an 10.97% CAGR by bundling multi-line towers that include property, cyber, marine, and general liability in a single slip. Mega health-care operator PureHealth processed over 25 million claims in H1 2024, illustrating the scale of enterprise needs.

SMEs remain price-sensitive but are increasingly adopting package products sold via digital kiosks in free zones. The government segment’s steady capex on strategic logistics corridors, smart-city platforms, and renewable power plants feeds a growing demand for project-specific covers. Data-rich corporate buyers also expect parametric and usage-based solutions that require high-frequency IoT feeds, nudging insurers to modernize core systems.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-Industry: Automotive Transformation Reshapes Risk Profiles

Automotive risks captured 24.83% of 2025 premiums after heavy vehicle turnover and a preference for comprehensive cover. Fast-charging infrastructure rollouts create ancillary property, equipment breakdown, and environmental-impairment exposures. Real estate and construction is the second-largest class, benefiting from an unbroken string of luxury hospitality and branded-residence launches. Oil and gas portfolios evolve as ADNOC invests in carbon-capture and petrochemical expansion, requiring bespoke wording for untested process technology.

Trade and logistics enjoy tailwinds from Jebel Ali Port expansion, which adds container-terminal capacity and drives cargo liability volumes. Healthcare facilities need ever-higher malpractice limits, while the manufacturing base in Sharjah and Ras Al Khaimah demands combined property-business interruption wraps. Renewable energy projects add solar panels and battery-storage covers that extend the UAE property and casualty insurance market into green-finance territory.

Geography Analysis

Dubai continues to anchor more than half of the UAE property and casualty insurance market, undergirded by the Dubai International Financial Centre’s mature legal regime, which draws international capacity providers and establishes the city as the region’s reinsurance placement hub. Experience from the April 2024 cloud-burst spurred widespread adoption of parametric flood riders, lifting the non-motor average premium per policy by nearly 20% in the following 12 months. The emirate’s AI-driven claims-triage pilots cut average settlement time from 14 days to under 5 days, sharpening customer retention and facilitating upsells into cyber and home covers.

Abu Dhabi is the fastest-growing geography, posting 12.05% CAGR on the strength of public-sector building, large energy projects, and a concerted push to localize reinsurance through the ADGM-based RIQ platform, which targets USD 10 billion in assumed liabilities over five years. The emirate’s public health insurer Daman recorded 84% profit growth over three years, underscoring the efficacy of vertically integrated care and cover models. Pro-enterprise regulation, including tax holidays in free zones, fosters specialty manufacturing clusters that require bespoke, multilined programs.

Northern Emirates collectively account for a rising sliver of the UAE property and casualty insurance market. Fujairah’s deep-sea bunkering and Ajman’s growing SME manufacturing base keep marine hull and cargo lines buoyant. Ras Al Khaimah’s construction of resort islands and integrated entertainment districts expands demand for erection-all-risk and third-party liability policies. Cross-emirate mobility, aided by seamless e-policy recognition, encourages insurers to design pooled programs that travel with both assets and personnel, supporting premium diversification.

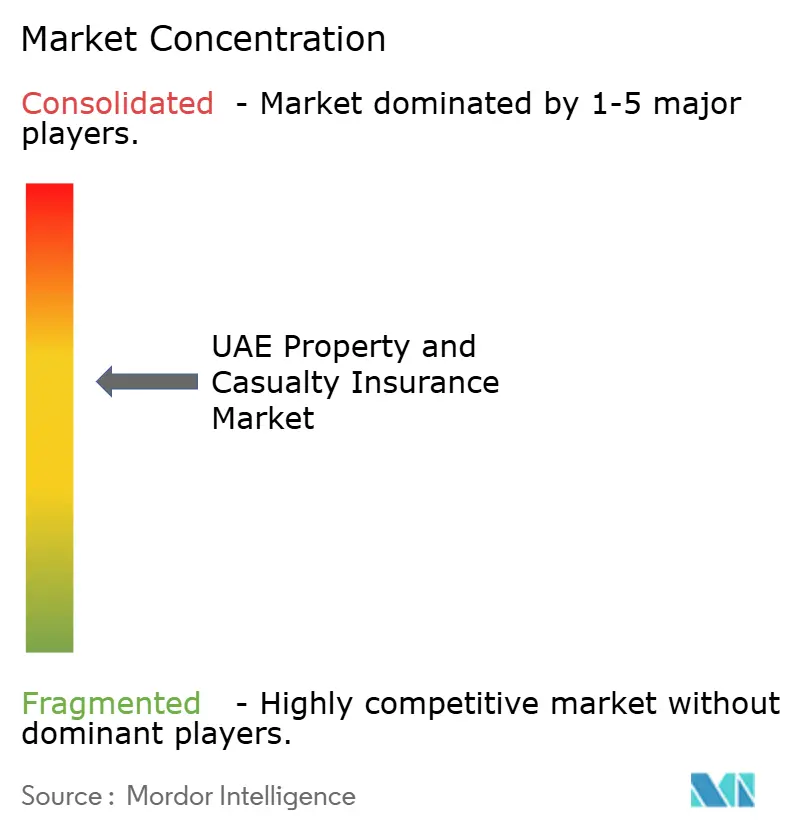

Competitive Landscape

Market concentration stands at a moderate level: the five largest carriers together write roughly 40-45% of premiums, enabling mid-tier specialists to thrive alongside national champions. Orient Insurance leads, taking advantage of DIFC’s treaty placement advantages and a diversified commercial book. Sukoon’s September 2024 acquisition of Chubb’s local life portfolio broadened its cross-sell reach and created economies of scale in shared services. ADNIC’s 51% purchase of Allianz Saudi Fransi signals intent to build a pan-GCC footprint able to leverage data, product, and capacity synergies.

Digital excellence is rapidly becoming a defining differentiator. Insurers deploying AI-based fraud detection models report double-digit reductions in loss ratios within one renewal cycle. The April 2024 Open Finance mandate forces all carriers to participate in API ecosystems, opening the door for embedded-insurance challengers to capture micro-moments in travel, retail, and gig-economy workflows. White-space opportunities remain in cyber, parametric climate covers, and EV-specific motor policies, where underwriting data is scarce and incumbents have yet to scale offerings.

International entrants are strengthening DIFC branches to tap the UAE property and casualty insurance market’s above-regional growth. HDI Global opened a DIFC office in July 2024, focusing on industrial-fire and engineering lines for multinational clients. Local innovators are exporting expertise; Sukoon Takaful rebranded and now bundles Sharia-compliant cover with digital servicing for retail segments in neighbouring markets. Combined, these dynamics reinforce the UAE as the Middle East’s most competitive and innovation-driven general-insurance arena.

UAE Property And Casualty Insurance Industry Leaders

Assicurazioni Generali SpA

National General Insurance Co. (PSC)

OMAN INSURANCE COMPANY PSC

ORIENT INSURANCE PJSC

ABU DHABI NATIONAL INSURANCE COMPANY

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: International Holding Company (IHC) launched RIQ, a reinsurance platform in Abu Dhabi Global Market with USD 1 billion equity and AI-enabled underwriting.

- March 2025: GIG Gulf released instant Orange Card issuance via UAE PASS for seamless UAE-Oman travel

- January 2025: Oman Insurance officially rebranded as Sukoon Insurance, marking a strategic move to modernize its identity while reinforcing customer trust, while keeping its existing covers intact.

- September 2024: CBUAE approved OneInfinity digital-asset custodial risk insurance offered by OneDegree and Dubai Insurance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates property-and-casualty insurance market as all gross written premiums from motor, property, engineering, liability, marine, and other non-life classes that protect physical assets or cover third-party risks. These classes are tracked in line with the Central Bank of the UAE's statutory returns and the IFRS 17 reporting framework, ensuring premiums are counted when they are written rather than earned.

Scope Exclusion: Life, savings, and standalone medical policies sit outside this sizing.

Segmentation Overview

- By Insurance Type

- Motor

- Property (Home & Commercial)

- Liability

- Marine & Aviation

- Engineering & Construction

- Other Specialty Lines (Energy, Cyber, Credit)

- By Distribution Channel

- Direct (Online & Branch)

- Brokers

- Bancassurance

- Aggregator Websites

- Agents

- By Customer Type

- Individual / Retail

- SME

- Large Corporate & Government

- By End-industry

- Automotive

- Real Estate & Construction

- Oil & Gas

- Trade & Logistics

- Healthcare

- Manufacturing

- Retail & Hospitality

- Others

- By Region

- Abu Dhabi

- Dubai

- Sharjah

- Fujairah

Detailed Research Methodology and Data Validation

Primary Research

Our team conducted structured interviews with underwriting managers across composite insurers, brokers that channel fleet and SME risks, and actuarial consultants in Dubai and Abu Dhabi. These conversations validated tariff movements, average sum-insured drift, and reinsurance cost pushes, filling critical gaps left by desk research.

Desk Research

We rely first on publicly available regulator filings from the Central Bank of the UAE, the Insurance Authority's annual statistical reports, and the Federal Competitiveness and Statistics Centre, which give audited premiums, claims, and insurer counts. Macro context is enriched through Ministry of Economy national-accounts data, Dubai Statistics Center construction-permit trends, and Emirates Transport motor-registration bulletins, all of which signal exposure pools. Company 10-K statements, DIFC supervisory communiqués, and reputable press such as The National supplement the picture when new rules or large catastrophe losses shift market behavior.

Access to D&B Hoovers and Dow Jones Factiva lets Mordor analysts screen insurer revenue splits, capital adequacy notes, and acquisition pipelines that rarely surface in press releases. The sources listed illustrate our secondary groundwork and are not exhaustive; many other databases and trade journals underpin data checks.

Market-Sizing & Forecasting

The model starts with a top-down build that rolls forward regulator-reported 2024 premiums using growth in fleet registrations, new-build floor area, and average policy rate adjustments that we confirmed in primary calls. Results are then sense-checked through selective bottom-up sampling of carrier premium income and broker channel splits. Key variables include motor vehicle parc, housing completions, industrial project capex, inflation in repair parts, and regulatory mandates expanding compulsory covers. A multivariate regression links these drivers to premium growth, and ARIMA smoothing captures short-term shocks such as April 2024 flood claims. Where carrier roll-ups under- or overshoot the macro projection, gaps are prorated based on historical retention ratios.

Data Validation & Update Cycle

Outputs pass anomaly screens, year-on-year variance thresholds, and peer review by a senior analyst panel before sign-off. The model refreshes every twelve months, with interim updates triggered by material events; a final pass is completed immediately prior to publication, so clients receive the latest view.

Why Our UAE Property & Casualty Insurance Baseline Commands Reliability

Published estimates differ, and the gaps usually stem from inconsistent class coverage, varying FX conversions, or one-off catastrophe loadings.

Key gap drivers here are scope (some publishers fold health into non-life), differing pricing-cycle assumptions, and shorter refresh cadences than Mordor's disciplined annual update.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.83 bn (2025) | Mordor Intelligence | |

| USD 10.70 bn (2024) | Regional Consultancy A | Health premiums excluded; limited broker channel sampling. |

| USD 10.05 bn (2023) | Trade Journal B | Pre-IFRS 17 definitions; no catastrophe-load adjustment. |

| USD 11.80 bn (2024F) | Industry Study C | Groups medical with non-life; five-year-old exchange rates. |

Taken together, the comparison shows that when scope, rate cycles, and FX are aligned, our 2025 baseline sits logically between older, narrower counts and broader health-inclusive tallies, demonstrating why decision-makers can depend on Mordor's transparent, variable-driven approach.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected size of the UAE property and casualty insurance market by 2031?

The UAE property and casualty insurance market size is forecast to reach USD 49.29 billion by 2031, up from USD 16.83 billion in 2025.

Which emirates is growing fastest in property and casualty premiums?

Abu Dhabi is expanding at a 12.05% CAGR through 2031, fueled by infrastructure projects and new reinsurance capacity.

How large is motor insurance within the overall market?

Motor policies held 44.12% UAE property and casualty insurance market share in 2025, underpinned by compulsory cover and a growing vehicle parc.

What regulatory change has had the biggest impact since 2023?

Federal Decree-Law No. 48 of 2023 transferred insurance oversight to the Central Bank, ushering in stricter solvency and conduct rules that strengthen consumer confidence.